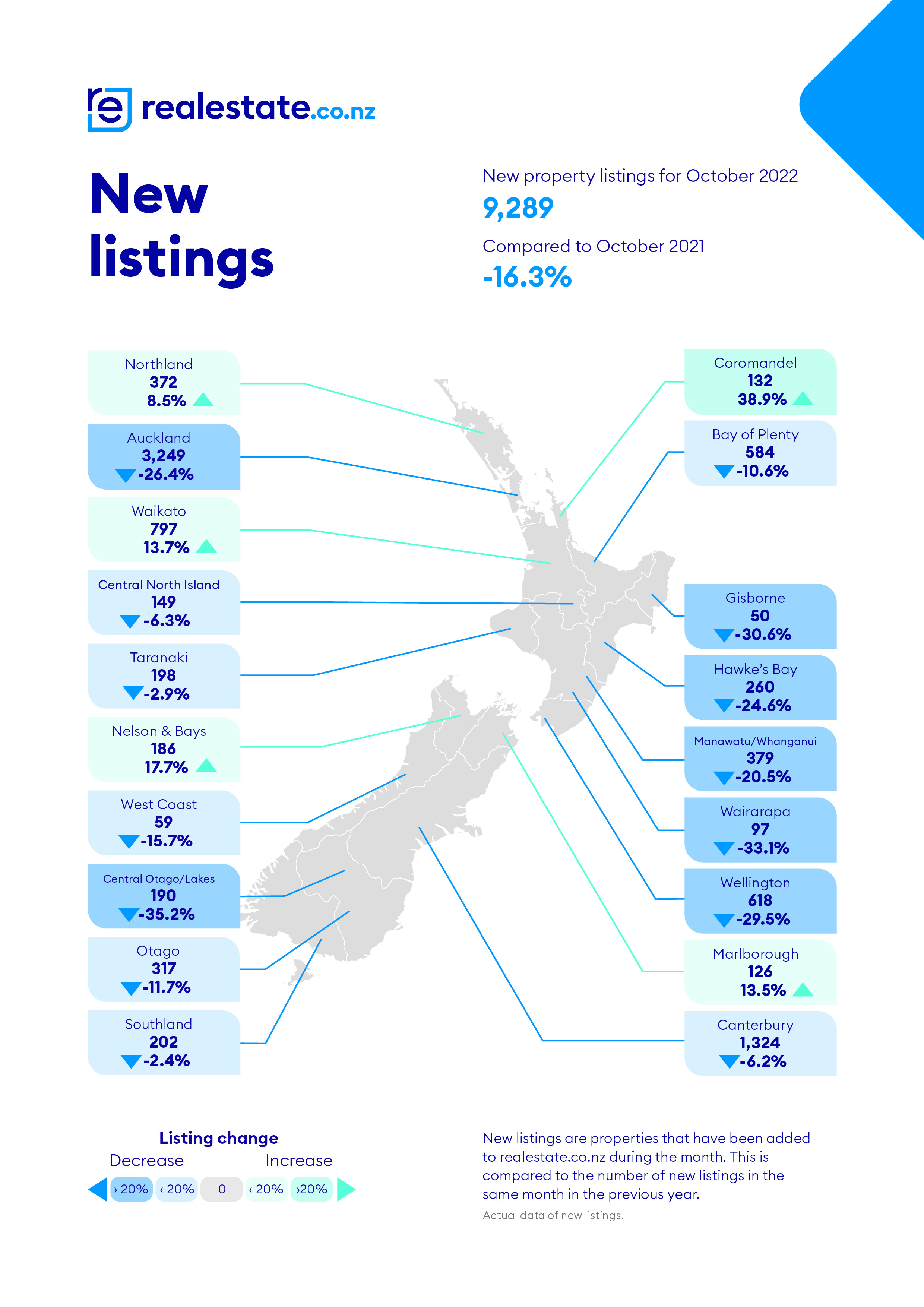

New residential property listings surged in October, suggesting a spring bounce has arrived for vendors.

However unless that's matched by a similar surge in buying activity, the market may start summer flooded with unsold stock.

Property website Realestate.co.nz received 9289 new listings in October, a sharp increase after new listings were under 8000 in each of the four previous months.

It's normal for new listings to increase sharply in October as warmer weather kicks in. However last month's new listings were down 16.3% compared to October last year and down 9.2% compared to October 2019, before the fallout from the Covid pandemic starting wreaking havoc in the market.

That suggests that even if there is a commensurate lift in sales, overall activity levels could be lower this summer than in previous years.

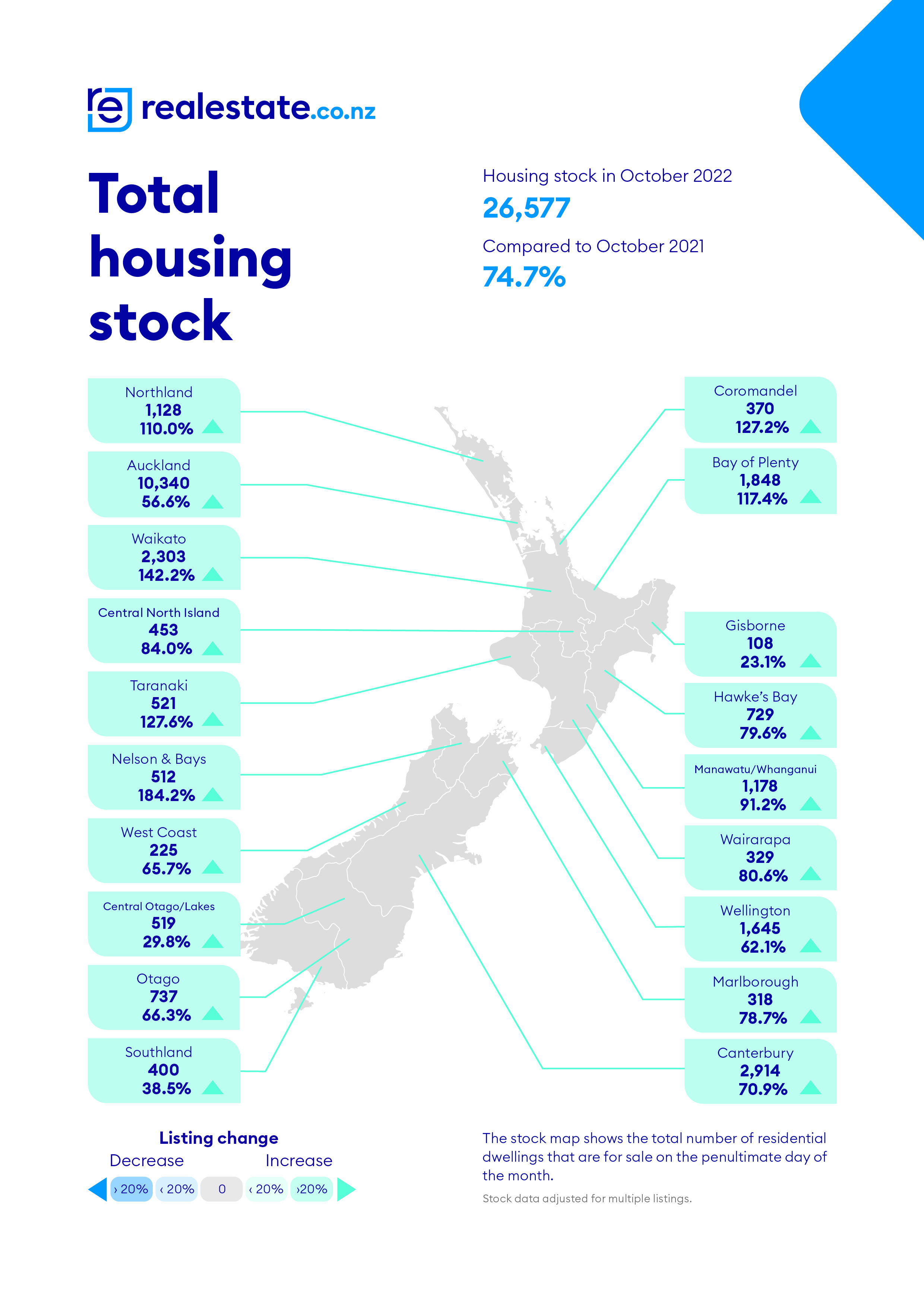

But if any increase in sales volumes is lower than the lift in new listings, that could weigh heavily on the market, because the total stock of properties for sale is already high.

Realestate.co.nz had a total of 26,577 residential properties for sale at the end of October this year. That's up 74.7% compared to the same time last year, and up 19.1% compared to the end of October 2019.

So buyers still have plenty of choice. And if sales numbers fail to lift in line with new listings, it will likely result in stock levels going even higher.

However it's likely to be the middle of this month before the Real Estate Institute of NZ releases its October sales figures, which will give a better idea of how the market is likely to fare as we head towards the end of the year.

See the charts below for the Realestate.co.nz's regional listing and stock for figures for October this year compared to October 2021.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

101 Comments

A sales volume jump seems unlikely given the banks stress testing new mortgages at considerably higher rates and the trend of rising mortgage rates.

Will be interesting to see where listing levels are come the end of summer.

That's causing much pain for those who bought "off the plan" in a low interest environment and are now failing the tests at higher rates.

Banks are still exposed to this market because they underwrite non-recourse loans for those very development projects on the basis of those off-plan sales. Hopefully, Megan Woods has her chequebook handy to bail distressed developers out and add the houses to KO's asset base.

Why should we (taxpayers) bail out developers?

It will be a very expensive undertaking too -each townhouse would likely cost circa 150k more than it would have costed if built by KO on their own land. Even once you take out profit margin and ‘buy at cost’.

And isn’t KO’s budget already at its limits?

Look I am not totally averse to the idea but a lot of questions. And will the government bend its own design rules to buy them ?

Would rather see taxpayer money go towards bailing out FHB who purchased in the last couple of years and find themselves underwater, than bailing out those who took commercial risks.

I would not like to see the tax of people who used to subsidise those that already own a home.

I would just keep distorting our rooted housing market.

Flush it out, if they have to sell then they have to sell...and thus enable the market to adjust to something like normal.

That is true, but if we had to choose, I'd rather we socialized the losses of many rather than socialized the losses of a few who took a risk for commercial gain.

If we're going to bail out home owners, we'd probably we best looking at the likes of the Australian New Liberals' monetary reset plan. By giving an amount per person it's helping renters and homeowners worst affected by previous years' policy shenanigans without unduly bailing out speculators.

A Monetary Reset [that]would:

- Give every Australian adult an identical sum of government-created money;

- Require those who had debt to use that money to pay down their debt;

- Sell Treasury Bonds to banks, precisely as is currently done in deficit financing; and

- Require those with less debt than the amount issued to purchase Treasury Bonds from banks, from which they will earn interest income.

This would not create any additional money and put inflationary pressure on the economy, but rather, it would change the asset backing the money from private debt, to reserves and government bonds.

We cant and shouldnt be bailing out anyone. This is a part of capitalism. if we give money to all then inflation and the boom gets worse. if we rescue people from making poor investment decisions then everyone will start making them....

Gotta let people fail to make it work better next time

Exactly I made huge mistakes and no one bailed me out.

If we bail these developers out then lets tax developers more. They can't just get a bail out for making a poor business decision, makes absolutely no sense. House prices were/are at the most unaffordable prices ever. 10X in a lot of cases when is this a good business decision to build more unaffordable housing, not to mention interest rates at an all time low. Interest rates were always going to go up at some stage.

Homeowners just made 40%+ capital gains in the last couple of years. Developers have been rolling in it, and every tradie drives a flash ute.

It is mental that we are even talking about bailouts. Entitlement mentality.

B-b-b-b-b-but South Canterbury Finance?

Hey now, don't go there! Those were important and well-connected "own two feet" folk who needed a taxpayer bailout.

I agree. My only point was that if there were a bailout, one such as the above that does not bailout the problem source of our malaise - speculation - is preferable. (And its design to avoid inflation is an important part of it.)

It doesn't have to be every townhouse project and definitely not to be bought at face value. Just compensate the developers with well-designed, unsold stock at "distressed" values.

It will be a very expensive undertaking too

Doesn't have to be new monies either - simply redirect the $1m a day that is currently spent on cramming people into motel rooms. At least, this way the Crown ends up with new assets on its balance sheet.

Its who decides on the compensation, the value of the product and so on.

Most (especially politicians) underestimate the lack of skill, knowledge and commercial nous of govt employees - they get screwed over by clever business people time and time again. And when the private sector do fail are very good at convincing govt to help them out.

That's where consultants play a good role in the machinery of government.

But the government would rather bring people in-house and clip their wings with mind-numbing PR processes and red-tape; unless of course the consultant in discussion is a cabinet minister's husband.

Consultants that charge $4000 a day for doing nothing and bringing in their graduates to clock up the hours, yeah sounds great.

Should definitely buy it up cheap. If developers fall, Kainga Ora should be looking to employ the folk who actually do the building, to finish off in-progress developments or build more supply. No need for a large-scale bail out of investors.

Bail outs are a nonsense. Let them fail, let the liquidator sell to the highest bidder who can complete and on sell at a lower price than originally expected.

Creative destruction. Bail outs just keep the market from operating efficiently.

Exactly! Any compensation will again shift the risk profile of property so in the future developers and first home owners take on even more risk because they know they have government backing if things go bad.

Not to mention set a terrible precedent for how businesses operate, by giving them the incentive for if they get that big, the government will take the risk off them for whatever decisions they make. Look at the lack of accountability in the GFC in the US, the day of the bailout they gave themselves bonuses and congratulated themselves on swindling the government at the expense of the taxpayers.

Agree. I am against bail outs of developers.

However could be an opportunity for KO to deploy builders for their own projects, once capacity is freed up with the slump in private sector building.

Pay just above bus drivers.... no builders and chipies will goto Aussie to build the million houses

overall activity levels could be lower this summer than in previous years.

No sht? (Sarc)

The new listings are down on previous Octobers in most places, but despite that due to the low volume of sales occurring the overall amount of stock is hugely up on previous Octobers.

Supply is smothering demand. Prices will need to fall to balance the two.

Browsing Interests auction data it's still patchy. Some well presented properties selling at or above RV, a handful each week below but most passed in. The HPI data will be intriguing.

With half an ear to the ground, prices look to be stalling or declining in that entry-middle bracket, and crazy prices are still to be had at the leisure and high end.

Nothing happened in Spring, now we look forward to Summer for some miracle

"High levels of stock" then the article describes a stock level 25% lower than last year. It's too early for this.

I think people with property who do not need to sell will wait for stability, even a moron can understand prices are going down at the moment, this is at its base a serviceability issue.

Is there anyone who cannot afford the extra 160pw. EASILY doable for couples with 800k mortgage and paying 1 year 5.99 vs 2.99%

160pw per person? My calc on a 30 year mortgage on your numbers is over $320 per week extra in payments.

But yes many should be able to cope especially if they have had decent pay rises over the past year. So I don’t see that many forced sales.

It’s more prospective home buyers, including FHBs, where demand is getting smashed, with stress testing over 8%.

Yes I mentioned couple, yes per person.

Dwelling on the short-term doesn't make a successful property investor.

Astute property investors have a different mindset. They're far more interested in seeing the big picture and thinking about longer-term opportunities, than dwelling on weekly interest rate fluctuations and the auction clearance rate of the day.

Thus, enlightened investors are out and about enjoying our curious world - while the familiar old Doom Goblins sit here, day after day, obsessing over their computer keyboards, cold breakfast coffee and foregone opportunities. 😢

TTP

You should be overflowing with gratitude for the "Doom Goblins" - and their efforts to bring down house prices - remember? With each passing day, that house in Ponsonby is becoming more within your reach - right? Real and fairer prices opportunities are getting nearer by the day.

Que the cherry picking.

Hi Crash Crusader (aka Retired-Poppy),

You vehemently discouraged first-home buyers (and others) from purchasing a home through the years leading up to the previous two market upswings..... Anyone who took your advice would have been badly burned. Your housing market predictions were an unqualified disaster. You could not even forecast the direction of house price changes - leave alone the magnitude.

But you, in a cowardly manner, disappeared from this forum when all that you said turned bitter. You were nowhere to be seen for 2-3 years - you were in hiding - as many people here are only too aware

Do you feel any remorse for your actions? Are you prepared to be accountable? How about an apology? Or are you still a lowly coward?

TTP

If I were a FBH, I would certainly be glad to have missed out on purchasing a lifetime of debt immediately before the removal of cheap debt.

And those who bought, and still own their own home with no intention of cashing out, how have they made any profit from the upswings they didn't miss out on?

The bubble was of benefit to investors, and retirees. Some others may have felt wealthy for a period of time, but that seems to be changing.

At the end of the day, people make their own decisions, and should not take serious life changing advice from a comments section online. It's pretty obvious what's happening to those who look. And you can't possibly think that 2021 was the best time for FHB to enter the market, there really has been no worse time in nearly half a century to enter the market than in 2021.

Tim, your lies mean little here now. Due to you're vested interests, you've only managed to self assassinate your own character and on numerous occasions too. You've only got yourself to blame. Its high time you considered some self reflection. Not only are you forgetting to thank the Doom Goblins for their dedication to your cause but you're now making up stuff in an attempt to hinder. This is not a good look for someone who is supposed to be above reproach in the eyes of the community.

Well said RP.

I am not sure who came up with the term 'Doom Goblin'... maybe the term should be replaced with 'Savvy Investors and moral NZ citizens'. These people simply provided sound investment advice that disagreed with the marketing messaging from what had become a greedy and self serving RE industry. They also faswaw correctly that the pumping of the residential property asset classes by RBNZ, RE Industry and Govt has led to poor home investment options for FHB's and poor savings return for retirees from bank deposits and poor return on shares in productive businesses.

Seems that the the 'Savvy Investors and moral NZ citizens' (DGM lol) are currently being proven correct in their advice - being that investing in non-housing asset classes or savings over the last 2-3 years, then waiting for the inevitable bust cycle (that always follows as night follows day) then investing in property at an optimum time (ideally to live in and leave plenty for others and keep pricing fair for society). Was the correct strategy for making money and for the optimum wellbeing of the investor and their fellow citizens (and thus a better lifestyle and society to live in with more wealth).

DGMs' lol.

Not only money, but time. I imagine there are a number of young people who are more interested in retiring early than anything, and it's clear that investing your life savings into housing right now is one step forward, two steps back.

House prices are falling very quickly and will easily fall back to 2018 levels and if rates keep climbing could go back to 2015 levels wait until downturn is complete before you ridicule people for what could be correct predictions.

Yip. All makes sense. An entry level house ending up at $350-450k? Sounds right to me. median wage is $60k before tax. So that would account for some overpricing of the residential property asset class due to excess demand leaving it at at 6 or 8 x income? NZ houses are pretty basic construction and whilst its a nice place to live the health/education/infrastructure here is hardly competitive to attract young and smart overseas workers.

After such a drop NZ property will be aligned with Tulips as an investment option for at least another 4-7 years. I think most smart people have been looking elsewhere to make money for a couple years already... stuff that does well in a downturn :)

"Astute property investors have a different mindset." They are sold up and enjoying the crash.

Printer8 and his kids managed to offload to less fortunate and (likely) more scrupulous Kiwis, as far as we heard.

TTP I bought at 846 sold at 3.25 mil did nothing..... sold nov 21, I am an investor but the time to buy is so not yet, there is no pain yet

We’re witnessing shifts in interest rate policy and the fundamental price of living that could likely put pressure on property for many years to come. Astute investors don’t fixate on property and will be looking at other investments that have already been hit hard by interest rate rises and forward projections - price movements in property lag in comparison so yeah best not check the rates and auctions every week - enjoy the summer and keep your cash out of the nz property market for the time being.

HouseMouse, the numbers would seem to indicate that the forced sales will come from overleveraged landlords, not homeowners.

As you say, many households can tighten their belts and find the extra money... but when you have 3 or 4 or more mortgages, then things get spicy.

100% agree

Banks will try not to roll a homeowner if possible, its a bad look.

But they will roll an investor, especially if he owns many in a Heart Beat. In fact the banks will already be planning who they will be speaking to first.

The public don't feel sorry for these people, and the banks need to readjust for their own safety and personal agendas. So its an easy and effective move. Banks call in loans.

Banks have been telling some to sell for 6 months but there are no buyers

If we had a wave of forced sales from landlords, and not from homeowners, this would be the best scenario for NZ as an economy and as a society overall.

where's the 160 from? is that each person? Are you referring to 800k outstanding debt?

2% of 800k is 16k, or $~308/week. A pretty decent grocery budget for 2 people.

Never mind their other increasing costs eating into their excess cashflow as well.

Yeah. Although if it’s a couple they could be up $200 per week collectively after tax from pay rises. But as you say groceries etc have risen too.

Having said that, many if not most people can cut back on things.

the calculation starts looks pretty dire at 7% rates, which are likely within 4-5 months.

Banks are already selling 7% loans.

And if you have low equity and belong to the Kiwi Bank its an Average of 7% right now. Imagine what next Month will look like ???

Where is the 160 from, on an 800k mortgage the difference between 2.99% and 5.99% is $325pw over 30 years.

A couple with an 800k mortgage are each almost certainly in the 33% or even 39% tax bracket.

Extra gross income needed to cover $325pw = $488pw/$25k annually (@33%) to $533px/$28k annually (@39%).

Would be a great pay increase, I'd suggest they could bargain for that EASILY.

Edit: had fortnightly amounts in, not weekly - I now see where $160 comes from. $325 between two incomes.

I think you mean $650 per fortnight.

You're right I did!

An excess supply of housing, who would have thought. It wasn't that long ago we were being told by every spruiker and his dog that this could never happen?

Don't really recall that ever being said let alone in concert.

The cost to produce new houses doesn't look like it'll decline anytime soon (you have half a dozen or so inputs that'd need to change).

The housing market is slowing.

Both are related to supply, the former is fairly baked in, the latter could increase in intensity and duration.

Housing prices are dropping mainly due to a drop in demand (number of mortgages and value of said mortgage dropping), that is credit growth is declining and thus supply catching up.

The cost to produce houses might no decline but the cost of land can fall, which makes up the lion's share of quite a few houses. It can fall quite a bit.

It makes up the lion's share of some older houses' values but far less of new. Unless you're talking outlier high end suburbs, the build and fees is usually higher than the land value.

Not sure in what world you're living in? Land is extremely expensive in cities.

The one below started at $1,050,000

https://www.realestate.co.nz/42168320/residential/sale/15-riverside-lan…

Now "only" $899k. Still plenty of room to go down, and definitely not a marginal cost.

Stock up. Interest rates up. Unsold for rent up. Inflation everything up. Auction failure up. Spruiker gloating down.

Sales down. Prices down. Immigration down.

The speculative are holding on thinking it will return to last year.

Good. Luck.

And 60,000 surplus houses, thats up.

The property market will always trend upwards in the long term. Over the next few months we'll see growth return to about 15% for the year. There simply aren't enough houses to meet demand. Buyers need to be quick; avocado prices are only going up from here and will become unaffordable so fhbs need to use that money to get on the housing ladder as soon as possible or their lives will be miserable, and their finances may never recover.

Tell that to the Irish.

Sarc?

Curses, Busted.

It is amazing to me that there is not more panic yet.

If people were rational, they would be trying to get out now, before the rush.

Seems pretty clear now that people will try to hold on... and hold on... and then all be forced to try and sell at once.

There must be thousands and thousands of people that cannot afford the new mortgage rates but are still standing around with their head in the sand.

The longer that people delay, the bigger the crush at the exits will be. The price falls will be brutal. Knowing how stupid we all are, we will probably vote a National govt in, just in.time to hawk off our houses to foreign interests for cents on the dollar.

There's no widespread panic, because working careers and mortgages are usually measured in decades, and economic downturns usually only in years and months.

If it's your first time to the party you'll get lulled into thinking this is end of days stuff. Anyone following your thinking in previous downturns usually came out worse off.

It is amazing to me that there is not more panic yet.

"As down-spruikers wakeup to the harsh morning sunlight, many will realise they've been listening to the wrong prophesies."

From the Scrolls: 1HW2 v2

You will own nothing, and you will be....

Kept

Or alternatively, its not a nice position being kept by your bank either. Your "portfolio" is their asset. When equity is rapidly eroding or even lost, you are merely a caretaker of their asset that can, in hard times, be moved on. There's nothing worse than being sent a letter requesting you refinance to another bank. I saw this happen in the 80s. Being up to date with mortgage repayments doesn't nessasarily shield you.

Savings can provide security in tough times💪

From the same stable: "It's not so bad for many in society to rent for life. We don't need to lower house prices."

Careers and Mortgages are certainly measured in decades.

Also mortgages need to be paid every fortnightly and if they become too expensive to service, then they need to be to repriced.

Repricing will be when property changes hands at a lower price so the new owner can service it better.

A million dollars is still a big amount for a human being to save in a life time. Not everyone is a Musk or a Hart.

People are stunned by the Rapid Increases in the Interest Rates. Fastest Ever.

Its like a Possum starring into the Headlights before certain death. Frozen in Fear. This cant be real, surely not, its just a dream, deny deny deny.

But the Interest Rates and the OCR forecast goalposts keep getting moved higher and higher just like The Prophet said in the Scroll. Banks are selling 7% Interest Rates like it was Prophesied, North Shore is touching on -30% crash in home prices by December just like The Prophet said, deny deny deny.

Will the Sheep believe Price Fixer talk like "small correction" "Interest Rates heading South" " "Property only goes Up" ??

Or will they Believe The Prophet.

10% Interest Rates Next Year, Guaranteed !

What about the next few years after next year, oh exalted one?

High for good? Or does the prophecy only deal in day trades?

Property prices will go low for many years to come.

100% agree this deflating will continue well into '23 .. and beyond (as no one believes it's happening - as mentioned above there is no mad rush for the exit yet ) ... once all the wind is out of the market and after the economic s storm that coming ... it'll quite rightly just lie limp for years to come.

Most people are fine because most people either don't have a mortgage, or don't have a ridiculous mortgage. Which should be a warning as to how high interest rates may yet go.

Though, I know people who need to re-fix in the next 6 months, and are hoping something will change, as they know they can't afford the higher rates and haven't been able to sell (no one turned up to their auction). One of these was gloating to me a couple of years ago about 'now being able to afford a Ferrari but no longer want one' - but are now working 3 jobs just to keep their property empire afloat. And another was lamenting not breaking and re-fixing 6 months ago, and is now waiting for next year to solve their problem - and has no plan B if interest rates don't fall back down.

Interest Rates are Not falling back next year. But I can tell you where they are going.

!0% Interest Rates Next Year, Guaranteed !

!0% Interest Rates Next Year, Guaranteed !

...and the programmers amongst us read "Not-zero interest rates", and we completely agree.

We knew 0% was falsy all along... no need to bang on about it...

I'll see myself out...

Anecdotal I know, but there are now three nice townhouses for sale in my little subdivision here in Christchurch.

Two private sale, one with an estate agent company I've never heard of before (name escapes me). These aren't rubbish Williams/Wolfbrook style houses - all three are well-appointed, three bedroom, double garage and nice spec and in a central location.

The two private sale ones have been listed for a couple of months now, with no signs of any interest. Prior to the slowdown, anything in this area was shifting within a week or two of listing.

I think all three vendors are doing themselves a disservice by not having an actual asking price listed.

Agreed, my observations for Nelson are top end places done up to sell are still selling at or above 2021 RV, likely cashed up folk from Auckland moving in which has always been the case, and boomers. Middle ground is dropping and the bottom end more so.

Got a ring from a RE agent the other day saying a couple of places I'd casually viewed are going up for auction early December and their observation is that this is becoming a little more common with vendors wanting sales locked in by xmas.

Nelson is a wonderful little city but struth it rains a lot

What? I thought Nelson had the record for sunshine hours in NZ?

Yep, tied in second place with Blenheim...

https://www.newzealand-all-over.com/2021/06/sunniest-places-in-new-zeal…

On average it has the highest sunshine hours, but when it rains it pours

Having spent a weekend in Nelson just before Covid (2020). My impression of Nelson is the same as Hervey Bay in QLD - Just a waiting room city; newly wed and nearly death!

Some amazing old mentalities down there too: https://www.stuff.co.nz/national/crime/128744672/identities-of-the-arti…

Waikato is second in terms of stock with 142%. Clearly reflects the absence of sales, sellers sticking to CV+ prices (from Sep 2021, more or less peak of the market), and buyers being limited on the size of the mortgage they can take due to rising interest rates.

We need a new metric - withdrawn without sale - to really understand the stock/market situation. The only place I can find this data is to check homes.co.nz after a listing I've watch-listed is withdrawn from realestate.co.nz.

Surely there must be a better way. Zillow (US) notes this information in all its listings under a price and tax history tab. The more information buyers have in a slow market - the better for everyone.

I agree, but the vested interests would not want the depth of stale properties getting out there.

Talk about being economical with the truth! The whole industry needs a re-think with a focus on transparency (free of charge). This industry has no trouble sniffing out where the money might be but where's the trust in return?

Yes, I have to do the same for non sales, have taken to checking everyday for new sales in our area (they are very low at present). I also notice that data such as sale price and even previous sales info is harder to find on the “affiliated” info/valuation sites, unlike the few years prior when it was trumpeted from every forum to help boost even higher prices.

Harcourts in Kāpiti have taken to withdrawing a property - then re-listing to get a new listing date. A way to coverup the length of time a property has been on the market. Spotted four of them done that way today.

I'm guessing realestate.co.nz will stop noting the listing date on their website soon.

I should set up a sweep on how many days 'til that happens.

Jump in new residential property listings in October but will it be matched by a jump in sales?

No.

The speculative (debt without clear supporting income) took the risk to do so by themselves. They should also be allowed to accumulate any losses by themselves. Any banks needing to recapitalise from speculative can lean of the profits of their parents. Their recent profits should be helpful.

If the Govt has to bail out a bank, then they take it over as the majority shareholder.

Is this properties being put in the market by people getting a bit freaked out by the rising interest rates, falling prices and slow sales - and they want to shift the houses before their mortgage comes off the low fixed rate it's been on for the last couple of years?

Yes most likely. Most of the new listings in our area are 3 bedroom 1 bathroom… investment properties I think

The biggest arseholes in NZ are the developers, who take millions from the country while ruining roads, creating dust storms/ noise/vibration damage,... From 7am to 7pm.. and then crowd people into small sections.

But!!! It's not the developers that take the hit! They pre sell the sections to building companies like generation, signature, GJ gardener... These are the guys that will take the fall.

Meanwhile the biggest scum on earth ,the "real estate liars" will cream it thru listing fees and bullshit "marketing packages " but sales will crash and burn . As we👉 are already seeing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.