The latest figures from property website Realestate.co.nz paint a dismal picture of the residential property market at what should be the industry's busiest time of the year.

The figures suggest the market is awash with properties for sale.

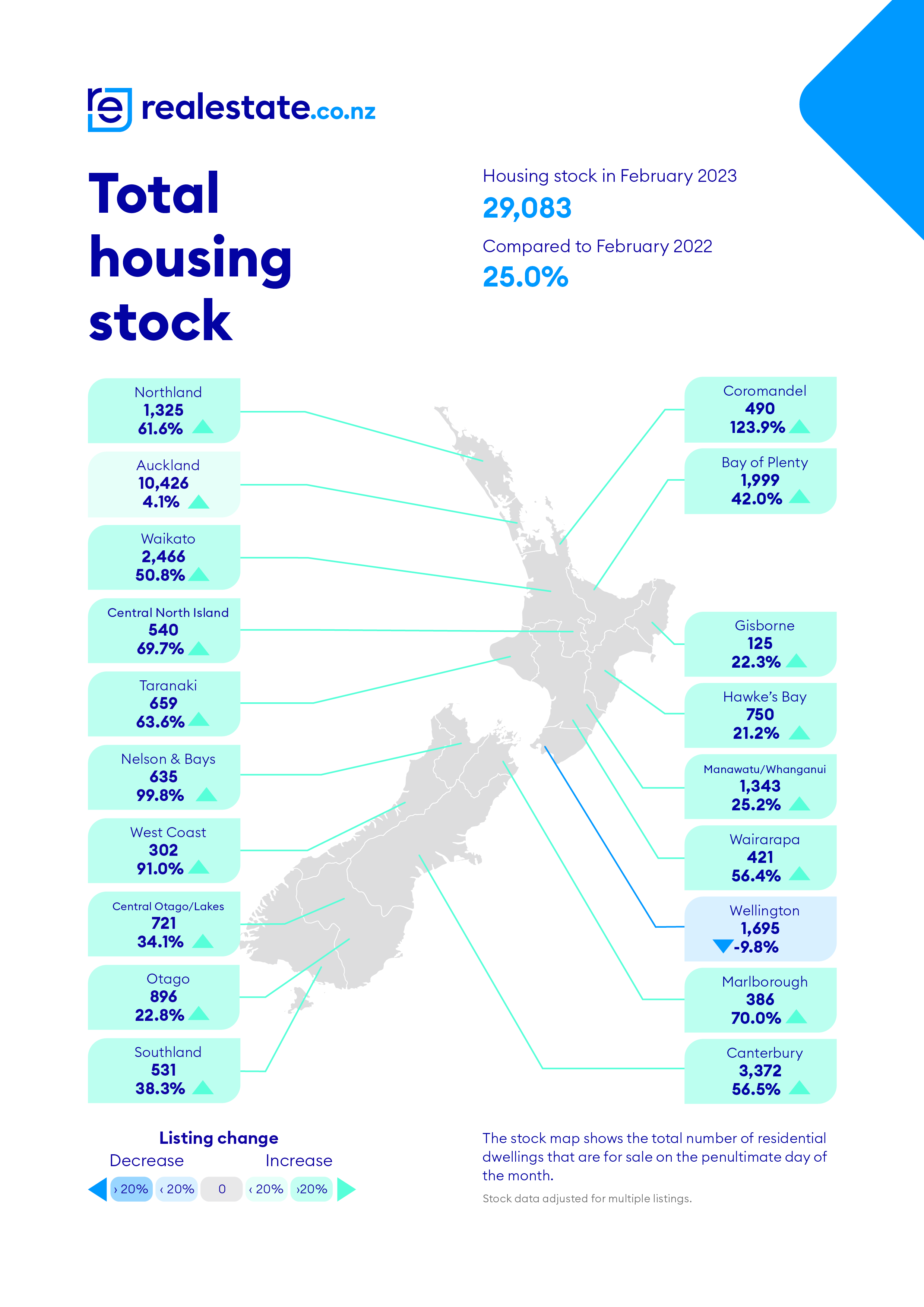

At the end of February, Realestate.co.nz had 29,083 residential properties throughout New Zealand available for sale, up 25% compared to February last year.

It was also the most residential properties the website has had available for sale in any month of the year since 2015.

The gravity of the situation is underlined by the fact that the build up of stock for sale has happened as the number of properties being newly listed for sale each month has fallen to a record low.

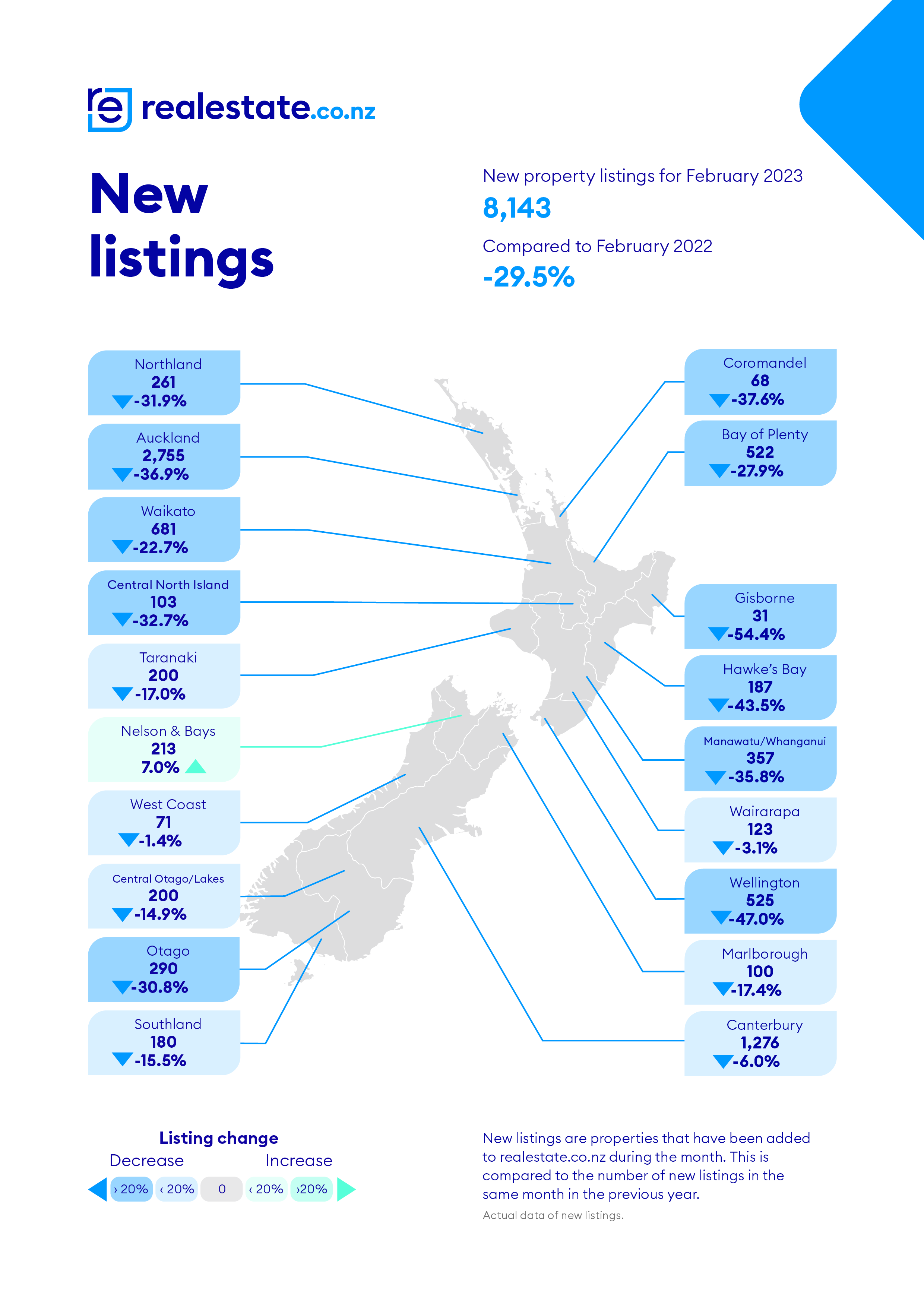

Realestate.co.nz received 8143 new listings nationwide in February, down 29% compared to February last year, and the lowest number of new listings received in any February since Realestate.co.nz began collating the figures in 2007.

It was also the first time ever that the number of new listings received in the month of February has been below 10,000.

The growing stockpile of properties for sale comes after the Real Estate Institute of NZ reported sales at the start of this year were at a record low.

All of that paints a picture of a market where fewer properties are selling and there is a build up of unsold properties, putting buyers in a very strong negotiating position.

The Realestate.co.nz figures also contain a clue as to why sales might be so sluggish.

They show the only region in the country where the total number of homes for sale at the end of February was lower than it was at the same time last year was Wellington.

It may be coincidence, but the latest figures from property data company CoreLogic show that average dwelling values in Wellington have declined by $215,000 since March last year, down more than anywhere else in the country.

That suggests there could still be a significant gap in many regions between the price vendors are hoping to achieve and the price vendors are prepared to pay and as a result, more and more properties are sitting on the market unsold.

This website's Residential Auction Results page suggests a similar theme.

The results show whether or not a property sold at auction and compares the selling prices of those that did sell with their latest rating valuations.

This page is updated daily and shows that only around a third of properties are selling under the hammer and many that do sell are fetching prices that are well below their rating valuations.

If price is the main sticking point to achieving a sale at the moment, then it's likely that many vendors will be facing some hard choices if they want to achieve a sale in the current market and prices are likely to have further to fall.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

124 Comments

“Reports of more activity in the market are growing “Agents in many areas are reporting more attendance at open homes, more interest online and even more multi-offer situations. Inventory has increased 39.4% year-on year, now sitting at 27,732 properties which provides plenty of choice for buyers. Add to that prices that have eased over the last 12 months, and some less bad economic news coming out recently, it seems there are more buyers active in the market. February and March data will tell us if they choose to act” adds Baird.

“This is interesting data and does indicate a slowing of the decline. The coming months will be telling as the country braces for more activity both in the weather and the property market,” concludes Baird.

“Salespeople around the country say owner occupiers remain active, and that there has been increased interest in out-of-town buyers looking in different regions. Sellers are tending to be more realistic and will usually meet the market through negotiation — however, many remain cautious with properties taking longer to sell, and investors sparse.”

https://www.reinz.co.nz/Web/Web/News/News-Articles/Market-updates/reinz…

I guess buyers chose not to act. Be interesting to see how they spin February.

Near record increased supply (availability of houses on the market) and low demand. What's the sticky glue holding prices up? What might be signals of reaching equilibrium?

Inflation. House prices will remain high until interest rates rise above the inflation rate (halting speculators). Banks have no intention to stop inflation, the money creation scheme will continue.

Nothing will change, with influx of people coming to this country supporting rent, it is all happening very quickly.

Prices aren't holding up, they're dropping rapidly (for property, anyway).

NZ housing market is in a transitional stage so only history and human reaction to similar events is a guide. If inflation remains sticky, interest rates continue to rise and recession/unemployment increases the house price direction is down, how that plays out is impossible to even predict a likely level as unexpected shocks like the Russian invasion of Ukraine and how China's post covid recovery goes will be major determinants. I will update with an exact prediction once my Crystal Ball is repaired by the ardern robertson crystal repair shop.

Its still a Mexican standoff, buyers & sellers are waiting for the first to blink.

"Equilibrium" is only a point in time.

Indeed. Cashed up buyers can wait to save another 20% at least.

Fantastic long may it continue.

Let the natural correction processe take place.

Very good for first home buyers.

But the fact is that to buy a house in a popular area you need to borrow as much as humanly possible. Always has been like that.

To buy any house in any area, unless you have a substantial inheritance/gift or exceptional income.

Not so, historically the house price to house income ratio was around 3. Even in 2000 it was 6. Recently we got up over 11.

It was about 3 in 1986 but the absolute maximum the bank would let me borrow at 22.5 % interest was $60k, $20k deposit and $10k second mortgage from the vendor to meet $90k sale price. You could argue that house prices were suppressed on account of the very high interest rate and buyers ability to pay. Repayments were nearly $16k a year of a $24k after tax income. Say $2k for rates, insurance utilities left only $120 per week for food, transport Herald delivery and beer. We had to buy a TV licence then too.

Same, I was about the same age in 1986 too! We had 22% mortgage and there were rampant house price increases and huge inflation, so the advice we received was to get a big loan and inflation( with wage increases) and house price increases would deal to it overtime. At the time I thought the big house price increase were largely driven by a large cohort of young women who were now working in professions and other well paid work - and planning to continue working after they started a family. This meant suddenly there were two incomes to count towards a mortgage, we’re previously there had been one. We had to change bank to get a mortgage though as the bank we were with ( BNZ) refused to count my income towards mortgage repayments as I may get pregnant and have to give up work - this statement from a rather crusty bank officer prompted a very vigorous response from me.

We mostly lived in poverty, but inflation did improve our wages over time.

Things corrected after the 1987 stockmarket crash and the many people who had used equity in their houses to purchase shares had to sell their homes.

Exactly

You didn't have to buy a TV license. Just like aspiring FHB today don't need to pay for Netflix (or an internet connection for that matter).

Thats not true, it hasnt always been like that. Check ponsonby/grey lynn/kingsland/western springs pre gentrification...

In the mid 90's I paid 123k for a 3 brm bungalow on 500m2 in Onehunga. Household income was over 60k at that time...

Ok, so some areas were priced low until they became "discovered". Exceptions like this would probably include Queenstown.

But back then there wouldn't have been the jobs that are there now.

And there are other places like Tauranga which have progressively been discovered to be a good place to retire to. Hence the higher than average price increases.

Essentially a different pool of customers than before.

I can still remember Queenstown in the 1980s. A really lovely place to be. Pretty much zero crime. Mostly NZ tourists there (from the South Island).

“40 years of falling rates were the engine of financialism - optimizing the real economy around leveraged finance and asset prices. Without the ever-falling rates, financialism is over. The next 40 years can't be like the last 40. Investors are yet to see it.”

Central Wellington certainly isn’t awash with quality listing. Sitting around 750. In 2008-2009 it was more like 1400.

Wellington isn't awash with talent in government either, look at the mess the country is in and it's going to get a lot worse.

There's more to Wellington than Government.

I mean there is and there isn't. The public sector roles will always be Wellington's biggest strength and weakness - that and surely being a candidate for total relocation in the event of a decent shake. The well-heeled consulting crowd and bits that hang off the government on good money move the costs of everything in the region up, while the coalface public sector workers and those below senior management face either wage freezes, sinking lids that increase workload and the general feeling that they're going to be on the hook for decades of deferred maintenance on really basic stuff.

I imagine if your hospo sector takes a pounding like it has in other regions post-Covid, it becomes a pretty miserable place to live when money is tight and you can't go out and enjoy yourself even if you wanted.

The average income in Wn is really quite high due to the public service jobs and a few head offices.

Most are steady jobs. Except some are lost each time Labour loses power. All those Ministries of wokeness...

There's a big tech sector outside of Government and public service. Sure, Government contracts help the sector to remain robust, but there's plenty going on that has nothing to do with Government.

Wrong. When Labour is in power they increase the public service numbers who are typically paid less than private. When National comes in they cut numbers and work gets done by consultants charging 3 or 4 times what a public sector worker gets paid.

I'm reviewing a project now where the cost of external PM is 450k full time for 1 year. If this were an internal role they would get in the region of 120-140K add organisational costs and you're looking at somewhere in the region of 250K. This sort of thing is way more prevalent under National governments from my experience working in both sectors.

IT work being done by inhouse specialists under Labour? Eh?

Without the Govt sector Wellington is just another windy ferry terminal.

I've lived there 50 years

Yip, its windy, on a fsult line that us ierdue

Yip, its windy, on a fault line that us overdue for a 7.5+ earthquake, full of gen y woke dummies, has a useless sewerage /water system, expensive rates, to name a few things

I feel a slow bleeding of wellington has occurred since covid 2020 as people realise they dont want to; fund the infrastructure that has been kicked down the road for 30+ years by council, bear the weather long term etc.

Nelson on the other hand has a LOT of 2 bedrooms for sale from investors bailing out, and many 3 bedrooms also the area seems to be filling up with folk from Auckland, Wellington and abroad, some places still selling for RV (gawk).

yes in nelson and they are still 100k overpriced

there is a build up of unsold properties, putting buyers in a very strong negotiating position.

Looking like a pretty decent time to buy if you can find the right property. Next to no competition from buyers, vendors willing to negotiate, banks fighting over themselves for your business offering loss leading rates..

Come on HW2 we know it’s really you posting ..,,,,

Still throwing around those false accusations in 2023 IT GUY...boring. If you're triggered, take a deep breath, step away from your computer and go for a walk...you'll feel better for it.

Agree. There is still some time to go before the absolute bottom though. However when everyone realizes it’s time to buy, it’s usually too late and has passed the mark.

This market won't recover in a spectacular way. People are now aware that prices can and do occasionally fall. The risk is not worth the return.

Hopefully I'll see you bidding on a couple of properties..

I suspect you won't DGM because you'll be on here scared & not making moves...

I didn't say that I was going to be bidding, did I? So don't be a goose and jump to conclusions

So do you attend auctions for fun DGM - with no intention of buying? Kind of like window shopping - nice to dream I guess...

It's fun watching some clowns fight each other to pay more for absolute rubbish..

But hardly anyone's buying or fighting for properties at auctions...unless you're suggesting it's different out there?

Nifty - attending auctions is called due diligence .

That’s a lot of overhang on the ask in a low liquidity market.

Liquidity is drying up and Banks appetite to lend on all but absolute certainties.

Looks like Wellington region is finally see the bottom.

😂😂😂😂😂

As rates continue to increase? I doubt that very much.

Be quick then, buy now or you'll miss out. oh no wait, isn't there an abundance of stock and tight monetary conditions?

Unsold stock, record low new listing, cost of debt rising, more new builds underway. Looks like it's sale time.

What's left to push into a fire sale..?

Forced sales would add some lubricant to the slide no doubt

Orr has stated he wants to see unemployment rise. That will add some dry wood to the fire.

Coupled with no real movement on inflation of course. We have a way to go yet. Mortgagee sales will be the start. So far we have only seen a reversal of the covid period increases..not the real fall from the prices that were way too high before then.

Albert - Orr has the oil can fully charged and ready for action.

Personally it doesn't make sense to buy at current inflated prices on high interest rates. I personally prefer to wait on the sidelines until sellers are ready to agree around 2017 RV (no matter the suburb or property).

And before the perma bulls pounce, yes I would be happy to miss out rather then get caught up in the frenzy like those who bought at the peak of 2021 and are losing hard earned deposit money. I would think more than a few times before spending my hard earned money on something that is priced way higher than its value.

Why hang your hat on the RV number? It’s a useless measure of a property’s value in any market. Get to know your target suburbs in-depth, do your research and then you’ll know when a good value property comes up and can pounce! RVs are a joke

Agreed. If it isn't at 2017 CV or better, then it makes no sense.

And yes, CV is just a guide. We all know that there is more to valuation than CV, but it is useful general guide.

Also the recent disasters made CV mostly meaningless for many properties.

”Never flooded” will be a selling point in the future.

The high number of houses for sale and the low number of rental properties is due to government and RBNZ policy. Policy that would be fine, if current renters could save up a deposit and afford a mortgage. In the mean time, more emergency housing will be required.

With inflation at 7%, we should see house prices going up to compensate. With Auckland at $940,000 and down -21.7%, this is -28.7% in inflation adjusted dollars.

Short term pain for long term gain. If everyone sells their rentals then house prices will go down lots and then rental yield will make sense again.

And sell they will. Not even 7houseLuxon can stop this house pice declide now its gained momentum.

History teaches us that there are a few years left of the downturn and a few interest rate hikes to come.

Coming soon: the polar opposite of frantic FOMO auctions. Ones where someone makes a cheeky low opening bid, the auctioneer accepts it, everyone is stunned and then nobody else bids.

If you know you HAVE to sell its better to market that way and open bidding very low.... gives agents the ability to get bidders to your auction.

Sounds unlikely. Not the low bid bit, but that it necessarily stops there.

Already happening. Not a lot but increasing.

I have been trying to buy a property in nelson tasman area and they are way overpriced and they dont negotiate much at all and i am cash at 1mill. Luckily I have at least till september till I have to buy and I have a caravan which I will live in if I have too.About 30 on my watchlist and 3 have disappeared off it .Go figure.

I think sellers haven't quite realised what has happened yet. You just need to what for a year or two.

Houses were overpriced in 2020, so you'll end up being ahead eventually, even if you sold everything in early 2020.

I feel you. The sense of vendor entitlement is unnaturally strong in Nelson Tasman. “Oh but nelson isn't like the rest of the country, we have so many people coming here from AKL and WGT cashed up who are willing to pay”

Yeah right REA and vendors, the place has been on the market 6months and you still wont budge? They’ll be in tears in another 6months when that 1.3m house barely gets an offer over 800k. It makes no sense why people wouldn't take the money now as opposed to hang onto unrealistic hope and spruiking from REA where every day, every week they lose value. Their loss i guess, literally 😂

100% this. I am hearing the exact same attitude in Blenheim "oh house prices won't fall, we're still cheaper than Auckland so the Auckland buyers moving here still have money".

We are still in denial phase. The boom lasted about 10 years this time. So far the down has been about 6 months? Long time for it to play out.... people still think they can defy gravity.

Well, older Auckland owners might still have money - if they can find a buyer.

What is Nelson - the retirement capital of the retirement capital of the world?

Lifestyle for families due to geographical variety and retirement mecca also yes. Even someone I know is trying to shed an investment property in Picton and the REA reckons they’ll make a little profit on it, I haven’t the heart to tell them it is very unlikely to make profit if they want it to sell sooner rather than later at a greater loss

Hearing the same thing from reqional REs.

What regional RE don't seem to grasp is that an actual buyer in Awk and Welly is essential to create a cashed up regional buyer. Little to no one is buying in Awk and Welly right now. Investors now have to increasingly pay tax, FHB'rs cant access debt, immigration is low, there is lots of new stock in mid development or arriving at market, and any marginal speculator buyer can see that a full on market crash is underway. Add in anyone investing five minutes reading knows a very large chunk of NZ mortgage debt rolling over to 2-3x what it was last fixed at, you can easily see further price drops yielding an immediate and growing capital loss v.s. the "Im so great" BBQ capital gain stories off the last ten years.

Now is the time to... Be Slow.

WAIT A MINUTE!

Are you telling me no one's on the way to pay $2M to live cheek-by-jowl with other ex-Aucklanders in Havelock North any more?

https://www.trademe.co.nz/a/property/new-homes/new-house/hawkes-bay/has…

https://www.trademe.co.nz/a/property/new-homes/new-house/hawkes-bay/has…

What about $1.5M for something more modest?

https://www.trademe.co.nz/a/property/new-homes/house-land/hawkes-bay/ha…

The horror.

Indeed. The stupidity of almost free cash is well and truely over. The fallout will be widely felt.

Around the BBQ in my circles is like looking at deer in the headlights. Those who were putting their head in the sand are finally starting to realise their mistake and the enormity of cost increases to come this year. Those renting don't really care as they are banking more with better paid jobs, considering moving cities, or living more remotely with a predominantly work from home role. Oh the opportunities

Auction results for Auckland from yesterday.

- 84 offered at Auction

- 29 sold (35% success rate)

When sold, the average price achieved was -9% below CV.

65% unwilling to sell at market prices. What is the point of an auction of you aren’t going to meet the market.

jim many do not get any bids, well any above the "wasting everyones time" level

Because the people who can buy at auction (unconditional offer / cashed-financed buyers) aren't the entire market. Plenty chance their arm at auction hoping for a quick sale knowing that if it doesn't sell they can then go to negotiation with a larger market.

Because the people who can buy at auction (unconditional offer / cashed-financed buyers) aren't the entire market. Plenty chance their arm at auction hoping for a quick sale knowing that if it doesn't sell they can then go to negotiation with a larger market.

At a cost in terms of money, time, and convenience. At the end of the day, the agent is working in their own self interest. And any sale is better than no sale. Glengarry Glen Ross.

Leading upto the auction the agent is able to get some idea of market expectations from visitors at open homes.

There are a few things which artificially create the scenario our housing market is in.

1. Media publishing Average price of properties in regions aggressively. Gives vendors a false sense on what they should expect. 80% of properties in NZ are well below average conditions but they expect to be paid average prices.

2. RE agents manipulate a lot of data which is available in the online world and this again gives false sense of value. Cartel system needs to go.

3. Private banks have vested interests to artificially keep prices up by giving as much credit to individuals who can afford it if only by a single strand of thread. So gullible can spend and fall into that trap of FOMO if they didn't pay the big bucks.

4. Central and local government policies which have been working in opposition to ensure well balanced housing market in the country.

80% of properties in NZ are well below average conditions

That makes no sense

Yeah it does. Average is not the median.

I think you'll find all the poor quality houses pull the average down, not up

Not if they're all clustered around the same entry-level price point. If the market is heavily skewed one way, the average can be well above the 80% mark.

Housing quality in this country would probably be better modeled via a pareto, or more likely school, distribution.

Simple example:

10 houses. 1 2-star, 9 1-star.

Average is 1.1-star, 90% houses below average.

I think “average” is being used to describe a standard. Excellent, Average, Below Average. Maybe terms like Excellent, Satisfactory, Poor are better descriptors.

Anyway have spent quite a lot of time with ourselves and our family looking at houses and can verify that most houses are below “average” or the “satisfactory” level. Many have weathertighness issues, even the older houses. A lot of houses we have seen have had no maintainance undertaken for many years. Currently we are seeing a lot of houses with single glazing and little insulation.

That Wellington's prices have gone down as well as their number of listings suggests that Wellington's vendors accepting lower prices is a factor in the reduction in listings. Wellington home sellers are more realistic?

Wellington as a bellwether city at last?

As a Wellingtonian who now lives in Auckland, I've always found Wellingtonians to be more conservative when it comes to property. In Auckland there has always been more of a "keeping up with the Jones's" mentality - I have several friends that are up to their eyeballs in debt because they must have the Ponsonby villa with a new Audi parked in front of it. As such I'm surprised to see such a sharp drop in Wellington, as you would assume it would be driven by forced sellers?

Probably reflects their fear that a change of govt will see them redundant, unemployable and unable to pay mortgage so better get out now while they can.

Larger cities will usually have larger volume of movement in the market, hence the downturn hits hardest as one house selling at below RV then effects all the surrounding houses and the area somewhat, more movement, faster reaction to the market.

Every month for the last year this data comes out, The spruikers line up and tell you now is a great time to buy... and every month so far, 30 odd days later new data comes out to tell us that the market is LOWER. Perhaps the best indicator of a stablisation will be a flat 3 month moving average.....But right now we have not seen a rising month since when HW2?.. thats right its falling and it will continue to keep falling as there are more sellors then buyers (read article above).

Overpaying is dead money. Recession is coming. Be Slow.

The RE industry has plenty of time to do marketing these days....

ikimpaul used to do a survey of houses in the Hutt which had time on market. I haven't seen this for a while. Could we have an update?

I keep an eye on Wairarapa. Very similar to comments about Nelson, vendors have their heads in the clouds. Often homes with huge price tags have no formed drive ( just a little gravel down), poor quality fit out- sometimes DIY, no garaging or sheds ( I look primarily at lifestyle) yet they are asking the very high prices - north of $2million - that you would expect to pay for a very high quality high spec’ed property. There is a large amount of greed that has come about over the two or three years of sustained rapid price increase here.

In the height of the sales frenzy, listings of Realestate.co.nz dropped to around 180 properties for all of Wairarapa, currently there are 585 listings with very few sales each month.

I recall when we were looking to buy our first home in 2017 Masterton, total Trademe listings for Property (All property types) were around the 100 to 120ish mark. Just now I look there are 276 listings.

Also, when we sold in late 2021 we had very little interest. Only 2 offers at Deadline sale, and viewings were dead. A few other properties that were listed for sale nearby ended up delisting after a few months.

Listings are updating to fixed price, price drops are becoming more frequent, or withdrawn by seller. Nothing is moving in my area. Hold fast.

There doesn’t seem to be that many for sale signs around that I’ve seen. Definitely not a crazy number. Some are taking ages to sell but I suspect that’s because they are still asking peak prices.

I have monitored trademe listings in Chch, Nelson and Dunedin for the last three years. There are now more listings in all of those locations than in the last three years

The housing market is falling apart and will continue until average wage couples can afford to purchase a home at 3.5 x DTI. Sure some people who cash out at top of the market are sitting waiting as far as people coming here to live I know more who have left for Australia.

suburb snap shot: Remuera, 3+ beds, houses only -

83 listings on Trademe, Similar to same time last year

Feb 23 auction clearance rate 13%, Feb 22: 27%

Feb asking prices (where given) 116% over 2017 CV on average, Feb 22: 27% 136%

Most family homes in Remuera are owned by people that don't need to sell. They likely bought them many years ago and can sit until the right buyer comes along. What I read in the low clearance rate is the market coming to a grinding halt - i.e. the cashed up boomer won't let go of their Remuera family home for less than what they think its worth, which then stops the Meadowbank townhouse owner upgrading, which then stops said townhouse come on line for a FHB.

I think the big drops will be in areas where people need to sell - anywhere with a huge amount of new development and anywhere that is usual investor hot spots

In otherwords - specuvestor locations.

What if the boomer has declining heath and needs to go into a home, or god forbid kicks the bucket?

While what you say about most boomer-owned family homes in Remuera is correct, there have certainly been big drops in Remuera already, and I still expect further drops to come.

It also has a significant cohort of the Silent Generation. When they pass on, or finally need to down-size or moved to age care, they are price takers, and prices are set at the margin.

Agree there are a good size number of retired people sitting in large Remuera houses on decent sized sections but with outdated, slightly shabby decor. They are not ready for retirement villages but are wanting to sell to make the transition to one of the bazillion new multi million dollar apartments being finished. The houses need work to make them suitable for current family living - without speculators to snap them up and apparently buyers at the top end only wanted finished houses not ‘ do ups’ it will be interesting to see if the prices drop.

For sure. A couple of years back potential buyers would have looked past the decades of deferred maintenance, with rose tinted glasses and some dream of 'adding value'

These days all the buyers see is the mountain of work to be done, and then think about the sky-high building costs, inevitable delays, dealing with the council etc etc

All those tiny little wooden windows.......

In the areas that I track, around 95% of unsold homes in Christchurch are those tiny 2 bedroom townhouse new builds. Hundreds of them. Since FHB don't want to live in them, and investors are gone from the market due to interest rates making property severely unprofitable, these properties just sit there now unless the developer can convince Kainga Ora to buy them.

A very interesting moment in the market. Things are pretty slow where we are.

I know of 3 people trying to sell. Two are selling their parents family homes & the third is a breakup. All 3 read similarly - 3 beds, 2 bath, double garage etc. & all three were built in the late 80's-2000 period (leaky homes?).

One is now approaching 9 months on the market (crunch) while the other two have been listed for 3-4 months. The dearer one is looking at minus $200,000+ from peak with the other two in the minus $100-150,000 range. These corrections do not represent a loss, as two were owned for 20+ years with the other one 6 years (so still a profit hopefully).

The Wellington market surprises me. I would have thought that with an extra 15,000 govt administrators employed (mostly in Wellington) since Labour have been in office (6 years) that this would have kept things strong. However, having been born & bred in Wellington I know full well all the other stuff that makes it a hard place to love (live) - ie: the weather.

As for the rest of 2023 I see a low point in early winter followed by polls showing Nat/Act potentially taking power later in the year, which along with the election sweeties spread around by Robbo, plus continued immigration, should see things level out in H2.

At that point my guess is minus 20% (NZ average) across the board, with the big towns down a bit more.

"The Wellington market surprises me. I would have thought that with an extra 15,000 govt administrators employed (mostly in Wellington) since Labour have been in office (6 years)"

1 - See my point above, the number of govt administrators aren't new, previously they were doing the same work for the government but were hired by private firms as consultants. It's a myth that cutting public sector jobs saves money, you end up paying more for consultants to do the same work.

2 - Government agencies have become very flexible about where staff have to be based, more so than private consultancies. Many of these government employees do not need to live in Wellington anymore, they can work from another regional office and visit Wellington now and again. Covid and WFH changed things dramatically.

This is exactly why the crash will keep going, and still has a long, long, long way to go. There's a long way down until people who bought years ago make a loss. Those who have purchased in the last 2, maybe 3-5 years will be stuck in negative equity and unable to sell. But those who purchased 5 years ago and prior will be forced to sell at a much lower price to meet the market.

Parnell Mansions, 30% off 2017 purchase price sale now on

Remuera Development sites - 30% off 2021 purchase price sale now on

www.trademe.co.nz/a/property/residential/sale/auckland/auckland-city/re…

Look for those mansions on a cliff, maybe <50% off, and that's just the half the section that is in the ocean now, then there's the price LOL

Oooh must be time to buy.

Quick check on mortgage calculator. Oh - would be paying 2.6x more on mortgage than current rent on similar place.

Plus insurance, rates and maintenance.

Plus ongoing capital loss.

= New found respect for property HODLers. You can have mine. Enjoy.

When will we see all properties advertised for sale (excluding auctions) with asking prices again? It would be great for an analysis showing proportion of properties with an asking price vs average days to sell. Watching from abroad and thinking I might like to move to NZ but I don’t have time to talk to spiv RE agents to get such key information

Agents tell vendors to not be greedy

some don’t listen

But but it's been 20 years of nothing but greed, fueled by agents. Oh the humanity....

Cycle still in denial phase not desperate phase

Denial in 2023 however is worse than archetypal one because of 20 years of Fed put and eternal drop in cost of borrowing. Era ended. Diabetics get no more sweeties. 19 year cycle for housing market should have peaked with the plateau of 2017-19. Then banks pumped it again. The 2 year super blow off top now reversing. Logic dictated prices have to drop to 2018 level at least when rates double what were then. 35-40% off peak at least

At current tax settings that will not be enough to attract new investors, numbers will not add up unless rents go way up and I do not see that happening.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.