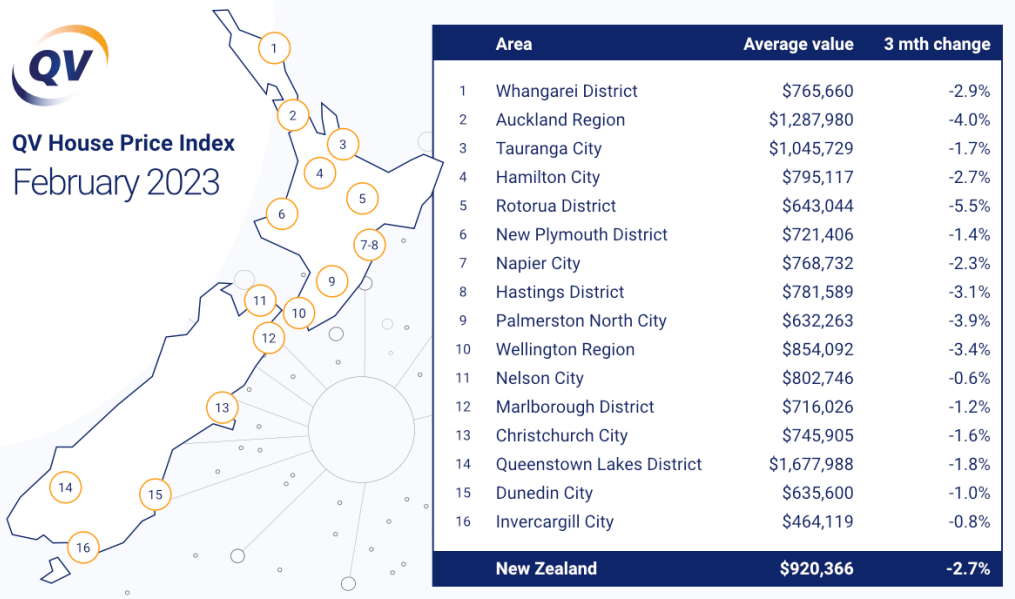

The rate at which residential property values are declining picked up speed in February, according to Quotable Value.

According to the QV House Price Index the national average residential property value declined by 2.7% over the three months to the end of February, compared to a 1.7% decline over the three months to the end of January.

The rate of decline more than doubled over that period in some regions, led by Rotorua where the rate of decline in average values went from 2.3% over the three months to January to 5.5% over the three months to February.

In the Auckland region the rate of decline went from 2.0% over the three months to January to 4.0% in the three months to February.

The decline in average housing values is now well established in all regions of the country. See the table below for the latest regional figures.

In dollar terms the average dwelling value fell $14,395 last month and has declined by $133,117 over the 12 months to February.

The fact that the rate at which housing values are falling is speeding up, suggests bigger falls may be coming and it could be some time before the market finds its floor.

"Clearly there's still some way to go if the residential property market's correction continues unabated," QV national spokesperson Simon Petersen said.

"That remains to be seen in the longer term, but the Reserve Bank's latest increase to the Official Cash Rate will almost certainly see it maintain its current downward trajectory for the time being," he said.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

151 Comments

If you were basing investing purely on what's the most popular topic on this site then housing wins hands down.

Because shelter (housing) is a basic human need. Printed debt and leverage has been used in a very exploitive way in the last ten plus years. People are pissed off about that exploitation.

Banks daily profits (topical this week) really highlights were NZs productive sweat is ending up. And for what...

There's some truth to what you say, but also a hype train a' running. If there was an out-rage-o-meter based on levels of exploitation and deprivation of "basic human needs", not being able to buy a house wouldn't be at the top.

You get exploited if someone owns you.

Some truth to that also. One notes that the banks own the speculative, and will exploit them as things unwind.

The bank owns the house (and therefore the homeowner) until the mortgage is discharged.

The bank has a caveat over the house when there is a mortgage, it doesn't own the house.

The legal owner on the title of the house is not the bank, it's the owner.

On the Sale & Purchase agreement the buyer and seller are not the banks, but the owners.

The owner can choose to renovate the house, add a room, sell it etc…

this is correct

Yes, but the bank has the option to recall it's mortgage loan at any time for any reason.

Technically correct but in practice until you make that last payment they have you over a barrel. They can raise your interest payments at any time.

The house is on borrowed money, and the lender has many ways to shaft you and take your money and the house. At least a landlord can only evict you.

Glad you agree that the banks doesn't own the house. I do hope your post makes you feel better about your situation though.

Depends on your definition of 'own'.

It can mean to have complete control over someone or to exert a great deal of power or influence.

If you have a big mortgage, then your property might not be 'owned', but you surely are.

Worst the bank could do is bankrupt you. Hardly a good old whipping followed by a slow death that accompanied human ownership back in the day. Conflating the two is stupid.

Rastus, what a cray comment to suggest that "I'm owned by the bank". There is no length you're not prepared to go to, to somehow try to make your biased point.

Ditto

The banks never loose..

History would say otherwise.....

Fortunately the taxpayer stands ready to support bank directors and shareholders.

It should be in exchange for equity, though.

The banks are the last to lose.

No, the reason it is such a big topic on this site is because New Zealand is basically a property market with an economy tacked on the side.

We don't really have a petrochemical sector, a vibrant tech sector, a pharmaceutical or medical sector, a semi-conductor or automobile or consumer electronics sector, etc. This country doesn't really make 'things' apart from houses.

NZ is property, and of course farming, and not a lot else of note.

Xero..Rocket Lab..Lanza Tech..we have the smarts but the worldwide money tree just scoops them up.

NZ investment dollars in have been channelled by policy directly into rentier speculation (FIRE) sectors instead of productive industry. Even the agricultural sector has slowly become about productive land price appreciation and rentier carbon credits and it's productive endeavours are becoming just a side hustle to fill time.

We don't even make houses well in this country. It takes us 8-12 months to build an average pre-designed house on a flat block of land, as compared to 4-6 months in Australia, US and UK.

SMOKO

So the national average value declines are now topping $11k/month.

You’d want to make sure you’re getting a serious discount if buying in this market

There's not really a way to "make sure", because no one really has a reliable means to determine the width and breadth of the current economic conditions - of which house prices are just a passenger.

Until there's some decent stability it's even more of a roll of the dice than normal with any investing.

Are you telling me it’s not safe as houses?

Sometimes I forget there's a percentage of the population who don't know how to use a rotary phone and don't know that markets don't always go up.

A higher percentage of the population don’t know how to send telegraphs stop.

Time in the market beats timing the market stop.

It’s easy for some boomers to be self righteous when they’ve sent their lambs to the slaughter in order to enrich themselves, avoid self sacrifice and milk the system.

The majority of boomers recognise this is a self defeating enterprise resulting in an unequal society that’s less pleasant to participate in.

In some ways yes but they grew up post-war without a lot of 'stuff', therefore as with many who grow up poor, they are more motivated to pull themselves out of this and enrich themselves so their children don't have to go through the same experience. There was also less people and MUCH more resources such as native timber, for example simply look at most houses built before the 70's, they are all old hardwood that lasts the test of time. Less people and more resources = greater opportunity. The could get houses built for cheaper and there was ample land to use for this. Supply was high, demand not so much. While I will always agree that the boomers have a disproportionate level of wealth compared to other generations, I will also acknowledge that even if houses were pre-covid prices, and lockdowns never happened, we would still be in a higher demand and lower supply situation, and eventually the central banking systems would be doomed to fail given enough time given how they are designed.

The main issue I have with the multi-home owning baby boomer generation, for those that do, is the attitude that "I've worked hard and made it to the top". Buying a second house in favourable conditions, leveraging it to buy another and another when the rent pays them off in 10years due to the low cost of housing, does not make one having had worked hard, it is simply making decisions and waiting for the money to roll in as a relatively surefire thing of the time. Also the fact that said house gained 50% 'value' in 2020-2021 due to FOMO and ridiculous RBNZ decisions also doesn't indicate hard work pays off, it is a simply matter of luck. This is where the ego and the attitude of those struggle to have a valid point of rebuttle.

The market has already fallen much more than the figures reveal.

A neighbour in my street has had their house on the market for months. Similar houses were going for $3m in the peak and homes.co.nz is still giving it an estimate up to $2.7 and they think it’s worth that.

There has already been a failed auction where the highest bid was $2m and this was a couple of months ago. The agents put in vendor bids up to $2.5 before withdrawing it.

it’s a nice house, but the reality is that it was $2m pre pandemic.

I believe that once sellers accept the market (or are forced to) then the figures will reveal an uglier fall.

Yes. The algorithm used by homes.co is so wrong it isn't funny. Complete la-la land valuations.

One roof is more believable.

Indeed. The straight line rises where the listing agent has paid to increase the price while prending that is a statistical adjustment should be classified as fraud.

Give them a chance. For 10 years the algorithm was probably

thisyearsprice = lastyearsprice + 20%

Now they have to recode for the next 10 years:

Thisyearsprice = lastyearsprice - 20%

🤣

I understand that a lot of people are trying to talk to Homes to get prices sitting more correctly as many vendors are choosing the Homes estimate as the price they would like. Correct me if I am wrong, but I also understand that Homes.co.nz is owned by trademe.

Homes is yet another laughable Kiwi rort

I was sold my proprety in wellington privately on trademe in 2021 - The day before I listed the proprety, homes.co had my proprety valued at 925,000. It was in the top 1/3 of the estimated values in my street.

2 days after I listed my property with trademe, my property was valued at 860,000 making it the lowest valued proprety in my street.

That behaviour smells :-)

On a side note - Feb 2021 Sale price 855K - Vendor had to borrow from family to raise the deposit.

Today:

Homes.co estimate - 725K - 785K

Propertyvalue.co - estimate 650K - 700K

Real Estate.co - 682K - 789K

Oneroof - 600K-760K

I suspect that all of the deposit has evaporated, and he may be in negative equity as of now.

That is a powerful anecdote, a lot of pain for that family

If they purchased that property today at 700k it would lose 10% by end of year. The pace of falls are increasing once average wage couples can afford to buy a home we might see fall start to slow down.

Both the buyer and family bank heading for negative equity perhaps? How many ma & pa's in that camp?

I'd be happy if sellers set their price according to the Homes estimate here in Hamilton. But nope, it's mostly CV from Sep 2021 and up.

I find Corelogic (propertyvalue.co.nz) and QV have both consistently valued my property lower than Homes and Oneroof, and IMO they are closer to the mark.

You get what you pay for or don’t pay for .

It's amazing how, due to the RBNZ-induced frenzy of 2020/2021, people forget houses were already massively over-priced in 2020 - and had been nationwide since ~2014, and in Auckland since 2006 at least.

There has been some wage growth over that time (minimum wage went from $8.50 hour in 2002 to $22.70 - but featured a lot of squish at the bottom end), but that fell far short of the increase in house prices.

The intentional introduction of an LVR over DTI in 2014 marked probably the worst of it, with those in power enacting legislation cornering the market for themselves. I still remember lying Simon saying "this will help FHBs", all the while anyone with a brain could see it would have the exact opposite effect - as history has shown. I guess the only way it helped was by reducing the number of FHBs exposed to what is about to unfold - though this didn't need to happen. The drop in interest rates wouldn't have had the disastrous effect they had if speculators had actually been required to pay for their purchases.

If something is overpriced for 14 years, that isn't overpriced anymore. That's just what the price is.

A traditional economic cycle used to be 7 years. If something lasts for 200% of the length of a standard cycle then it's not overpriced relative to anything, that's just a 'new normal'. I'd say no one has 'forgotten' - they just weren't prepared to wait around for 20 years waiting for a house to not be 'overpriced' anymore.

Where is it defined that a bubble can only last 7 years?

We've had inflated prices caused by reducing interest rates for 15 years currently - sure, there was the option for stabilitisation (as the 2017-2019 period showed), but the powers that be weren't happy with that, and kept dropping rates. But we were in a bubble in 2017, so what is one to expect?

Does the bubble crash back to the 2017 prices (which were already a bubble), or do they crash back further (to fundamental values, IF the fundamental values don't support the 2017 prices)?

How many of those who "couldn't wait" got in on their own equity vs how many leveraged their parent's gains in the bubble for a deposit? Bank of Mum and Dad was bigger than Kiwibank, and no one has been buying on fundamentals for quite some time.

Just because I don't know any personally, doesn't mean there doesn't exist FHBs without parental help - but I've known a fair few FHBs over the years, and the last ones to stump up their own deposit was in 2013 - and they were well above average income.

Yup - I agree a lot of people have forgotten that prices were well overpriced in 2019 and there were genuine fears of the bubble bursting then

That’s when Granny Herald with their property division Oneroof rolled in the market historian and expert Ashley to put everyones fears to rest

https://www.oneroof.co.nz/news/ashley-church-this-is-what-a-house-price…

A major reason we are where we are now, is the property industry (self proclaimed experts) built and perpetuated a narrative that the NZ property market was bulletproof

You’ve got to laugh at their 2019 market scenarios where they don’t even consider rising interest rates/increased cost of debt as a risk:

The good, the bad, the ugly: The market scenarios

5-10 percent rise:

Possible but unlikely. Would require a significant uptick in the economy and increased confidence in the lending sector.

0-5 percent rise:

Likely. In line with most bullish forecasts for the property market. Assumes continued surge in Dunedin and Wellington and increased demand in regional markets as well as improved performance in Christchurch and Auckland.

0-2 percent drop:

Likely. In line with most bearish forecasts. Assumes recently passed and planned legislation will have a drag effect on Auckland’s market and property investors.

2-5 percent drop:

Possible. Assumes the consequences of a capital gains tax, the removal of tax breaks for landlords and the foreign buyer ban are more severe than expected.

5-20 percent drop:

Unlikely. Would require major cataclysmic event, such as earthquake or massive failure in the banking system.

David Hiscoe thought they where overvalued in 2016

Yup - was he the original DGM'er / rational thinker ??

Shame that the ANZ board found a justifiable reason to sack him, as a logical and sensible voice in the lending market would have been beneficial for the country

"Salaries and wages have hardly changed whilst house prices have risen - this can't continue so it's a matter of when, not if, the market adjusts."

"New Zealand is a great country and we've come out of the Global Financial Crisis well compared with many. But logic tells me things cannot continue to run this hot."

"Low interest rates give borrowers the best chance to repay their debt and that is what they should do, not use them as a chance to borrow to the max."

It's hard to argue with anything he said in 2016

https://www.nzherald.co.nz/business/david-hisco-housing-and-nz-dollar-o…

Ditto Bernard Hickey and Shamabeel Eaqub if I recall correctly (Bernards legenadary 30% call)

Tell that to the Japanese

The last cycle length wasn’t typical ., a result continued QE following the GFC then accelerated via Covid. Perhaps taking the medicine due following the GFC would have been more prudent?

Agreed. We are back to pre pandemic levels and dropping. The graphs on Homes simply serve to show how great the stupidity of cheap debt was.

Debt ain't cheap anymore....

I totally agree but also it has to be said that the market is also very volatile. I've been observing low new listings at the same time as a small relative bump in auction sales, followed by very low auction sales, and over the same period some houses selling over CV and others up to 30% down. Some new listings are coming in with very high expectations but increasingly it looks like many houses settling in around 20% below CV when they first come online (and many/most still not selling). Some very good houses with reasonable vendors are getting almost no interest while other houses are getting good attention. It's all over the place.

We were about to buy, so watching things very closely, but we decided to pause and watch a little longer. It's too risky to buy for us at the moment. We also think if we wait we might be able to get a better house at our price point. Given that we (as far as I can tell) are one of the few cash buyers out there in the bracket and area, and we are keen to buy, makes me think that there are a tonne of people taking the same course...I want a good deal but also I have to say, I feel sorry for some of the folks trying to sell a house right now. Some will do well but I think there is an increasing amount of uncertainty and pain out there for many folks trying to sell.

A few months ago I stated we had no intention of buying here in NZ. Since then, my wife's contract has been extended and it makes good career sense for her to complete it.

As long as it remains cheaper to rent than to buy, we'll keep renting - but we're watching the suburb she works in. It'll take a significant fall to tempt us to buy, but at the current rate of falls, that might be sooner than we thought.

With the healthcare system having been in decline for a decade-plus it'll be interesting to see whether house prices decline quickly enough to make NZ a more attractive proposition for healthcare workers to stay/come.

Very similar boat here :) Ready to go, just watching to see what happens

Ditto

Not me - owning residential property is too popular. Paying the huge competitive premium makes no sense for me.

Amusing article quoting QV today mentioned that if house prices continue their current rates of decline then we'll be back to 2020 levels in 2 years. No mention that the rate of decline would be characterised as a crash in other places.

The property love story is history.... pity all those with broken hearts

The peak selling period of the year is upon us. The lack of sales is telling.

Someone posted earlier this week about and OCR model tracked by one of the Uni's. It indicated the OCR should be over 8% to control inflation. Imagine the blast radius of that on the speculative, but note also they are by far the minority of the population....

That models the Taylor rule.... which for a long time was close to what central banks used to do....

Central banks have been clinging to the idea that inflation is simply transitory - that once the covid pandemic calms down and supply chains revert to normal, that inflation will too. Consequently they thought they could slowly raise interest rates because eventually there would be a cross over where the interest rate becomes higher than the inflation rate (~5%) and the Taylor rule will be restored. The problem is that inflation is not coming down fast enough to meet the slow rise in interest rates, which is why the US Fed is now talking about increasing interest rates at a faster pace https://www.wsj.com/amp/articles/jerome-powell-to-testify-to-congress-o…

What central banks have done is merely create the space for inflation to become structural and not simply a response to the covid supply chain crisis (which is well and truly over). Markets were betting on a pivot from the Fed, then a pause, and soon the market will face the reality of "higher, faster, for longer" and asset prices will start the real leg down.

Fantastic long may it continue.

Very good for the younger generation.

Higher interest rates are making it harder for FHBs to get approval in the first place. We have the worst of both worlds atm - a high deposit requirement and high interest rates, and one is not functionally offsetting the other.

The problem is the rest of the economy is now set up under the assumption that you can extract blood money for housing, and decades of future earnings have been pegged against this by new market entrants. So for millennials et al to even be able to retire mortgage free, let alone with a nest-egg, we're looking at a severe contraction in spending in areas that will hurt young workers the hardest (hospo and other discretionary spend industries).

"Higher interest rates are making it harder for FHBs to get approval in the first place."

This is fantastic news. It protects them from buying due to FOMO on assets that are still massively overpriced and falling. This will cause even bigger falls in house prices which will help FHBers in the long run.

Assuming that actually happens. But the political and institutional failures that got us into this situation in the first place haven't been addressed and there's no logical reason to assume that someone won't find a way to jumpstart things again, or that the resulting fall-out won't adversely affect them, in a country that has shown little interest in actively addressing the issues they face.

"there's no logical reason to assume that someone won't find a way to jumpstart things"

It's precisely because the political and institutional deficiencies have not been addressed that it's unlikely that locally anyone will be able to jumpstart things.

At a global level the broader structural changes to the economy driven by global factors (access to credit, de-globalisation, resource scarcity, increased number and frequency of extreme weather events, insurance risk, etc...) will mean this mythical someone will need god-like powers to jumpstart things again

I wouldn't be sure about that. NZ has long been a high cost, low wage country, but that didn't stop us flinging the doors open to import more tenants and there'll always be someone somewhere who thinks life in NZ is better than life where they are now.

I mean it sucks but based on our form to date, I would say it's definitely the most likely outcome. We've given up on the 'high value tourism' approach pretty quickly, even in the face of carbon accounting and the kind of response we need to meet our targets for emissions.

"House prices remain nearly 25% higher than pre-pandemic" we're told by QV.

And that's the problem.

We didn't do anything productive during the Covid monetary expansion to justify price rises. In fact, quite the opposite. We all sat at home and watched time pass by. And at that same time all Central Banks continued lowering the cost of Debt and make more of it available, and Governments shovelled copious amount of liquidity from the Public to the Private Balance sheets to replace lost productive income.

Now, the RBNZ is correcting its actions.

If we get just another 25% fall to return us to pre-COVID levels, I'll be surprised. We are staring at far more than 25% to rebalance the unsustainable in our economy.

If we get just another 25% fall to return us to pre-COVID levels, I'll be surprised. We are staring at far more than 25% to rebalance the unsustainable in our economy.

Prices always overshoot - to be affordable prices need to be at a level that matches where they were when interest rates were lsimilar.

One thing which is not being talked about is people who have a house and nothing else and have retired. When interest rates were 2%, a reverse mortgage was attractive - Now people on that train have are heading over the cliff and may wind up homeless.

Sadly, you're right.

8.5% and rising. It won't take long to eat up equity at that rate. Especially as the value of the asset backing it falls.

Leading to forced sales as the owners have to cash out with enough money to buy into Chateau du Rymans !

Reverse mortgages always sounded too good to be true to me.

Chickens coming home to roost on them now.

And it will get worse.

The headline should be that property values are still 25% higher than the pre pandemic levels.

The interest rates were a lower pre pandemic and they become a crazy low during the pandemic years which caused the piranha scramble for properties.

The house prices were stretched even before the pandemic and now with higher interest rates, the property prices are just too high to service a mortgage. Anyone buying now at these prices is just too rich and do not care how much they spend.

Eitgrr Prices will have to come down a lot or if interest rates go to crazy low levels and we can fix them for 30 years, then it makes sense.

The banks borrow money from international markets and they know we are not a stable economy like US, so they do not commit money to our banks at low fixed rates for longer durations and that passes in to end consumer.

Anyone buying now at these prices is just too rich and do not care how much they spend.

...or doesn't want to put their lives on hold waiting for the kind of correction that our political and financial institutions have spent decades bending over backwards to stop happening.

Seriously, how long do you expect people to sit on the sidelines? You say house prices before the pandemic were nuts... if you spent four years waiting and saving, all that's happened is your savings have been monstered by inflation and won't have kept up with increases in your deposit requirements.

Ridiculous comment nobody needs to put their life on hold just because they haven't bought a house.

They can rent and buy once the prices fall sufficiently. Buying an overpriced depreciating house is more of a risk to you having to put your life on hold. It risks locking you into staying put, unable to move for employment or life experience opportunities, you can't sell due to negative equity (or if you do you lose all your life savings) and you have to sacrifice everything else in life to meet mortgage payments.

Oh yeah and you don't really actually own the house until you make the final payment in 30 years time. Sounds like buying a house in this situation is more akin to putting your life on hold.

Nah, I'm calling this out. I had friends who moved 12 times in ten years because landlords sold out from under them and took the money and ran. Try doing that with kids, staying in school zones, close to work etc. No thanks. You have to have a pretty demented adherence to your own desire to be right about something to endure that over and over again, and to watch yourself slide backwards as houses increase in prices faster than you can earn money and saving for a deposit and paying rent gets harder and harder.

And there's that 'overpriced' argument again. It's stopped-clock logic and inherrently flawed. See previous comments about this supercycle of house prices lasting for more than two times the length of an ordinary econmic cycle.

But sure, the comments I'm making are 'ridiculous' while people say things like "anyone buying a house now is just rich and doesn't care what they spend" like it isn't insane.

Oh yeah and you don't really actually own the house until you make the final payment in 30 years time.

This is also insane. That's never been a valid point against owning a home, and it isn't how mortgages work in the first place.

You have to have a pretty demented adherence to your own desire to be right about something to endure that over and over again, and to watch yourself slide backwards as houses increase in prices faster than you can earn money and saving for a deposit and paying rent gets harder and harder.

I'll take that. And I've done what you said beforehand too, as a result. And I've really enjoyed the flexibility of being able to move when I want as well.

"Stopped clock logic" - you're wrong about that. No one is saying prices are overpriced because they are higher than when the clock stopped. Prices are overpriced because they have sat persistently above fundamental values, and in the past decade of crazy interest rates, the amount they are above fundamentals has increased - I think at peak houses in NZ were almost 28x the average persons income!

I don't think you're ridiculous, btw. But I do think you have skin in the game for prices to not drop further and for interest rates to not rise further, and this gives you a blind spot.

From an investment p.o.v, if you cannot afford to buy a house with cash and hold for a very long term (and willing to take the risk), it would be insanity to buy right now - you're much better off even in a TD and waiting for prices to stabilise. Which at the current rate of falls is probably a fair way off, even without considering the wider market dynamics.

You're talking about what has happened over the last 12 years and applying that scenario to today's situation. 12 years ago it might have made sense to buy.

Not now, for the reasons I've given above. If you bought 12 years ago we'll done. If you bought in the last 5 years you might get away with it. If you bought in the last 2 years it was the wrong decision. Unless you have money to spare, money is no object and you don't really care about the value of your house declining as the original commentator said.

With all due respect dude, that's just your opinion man. You can't generally decide someone who bought in the last two years made the 'wrong decision' unless you are getting something out of assigning personal levels of responsibility after decades of political, institutional failure that got us to that point. And the last 12 years is relevant in that regard because the argument is house prices have been well ahead of wages for literally decades now.

Or is this going to be the new way we assign blame to young people for not being born earlier? Millennials are now hitting 40. They got told that there was no housing affordability issue and it was all down to their spending when house prices were rocketing, but if you did actually manage to save and buy then that's now your fault too? Come off it. If you wait around any longer you're not going to have a working life to cover the length of the mortgage you need.

That's the problem with this country. There's always someone trying to lord over something as simple as 'having a stable family home' over you to tell you that you're doing it wrong, and how much smarter they are than you, when the market goes up, when the market goes down, you're always wrong somehow. No wonder so many young people leave.

It's just the usual narrative from Boomers, everything with them is one-upmanship. They were the last generation to play outside and drink from a garden hose. Your problems are not problems because they had much bigger problems in their day, but they pulled themselves up bootstraps and all.

Unfortunately there were not enough counsellors out there to treat a whole generation of narcissists.

When I say it was the wrong decision I'm talking objectively speaking from a financial point if view. I'm not blaming anyone for making the calls they made.

The system was rigged and it was/is shit. But no-one forced anyone to take out a massive mortgage. There were plenty of warning signs that the housing market was overvalued and in a bubble.

People choose to borrow big and buy a house because they thought it would provide more security than renting or moving abroad or something else. What is playing out now is showing that it was the wrong decision (financially speaking) if you made that decision within the last 2 years and it would be the wrong decision to make now.

Financial considerations are only one aspect to consider though, so if you value all the other things home ownership provides then could still be worth buying, but as the original comment stated you have to put aside financial considerations.

To probably offer a more constructive response; the financial 'considerations' are only relevant as much as you can influence them or can expect them to change in your favour - and like I say, there was every indication RBNZ and the Government would keep this party going and bend over backwards to make sure it kept happening.

I've said it previously here but it bears repeating: if you'd taken the PM, Finance Minister and RBNZ Governor - the three most senior and relevant officials - at their word about house prices, tax intervention and negative interest rates, a completely informed decision would have been... well... like you say, a bad one (with the benefit of hindsight).

Again, that should be seen as a failure for them to justify, not individual borrowers, who get stuck with the fallout either way.

Well since you have opened the anecdotal example as the basis of your position, I will respond in kind: I know half a dozen people that have rented 2 houses over 10 years. And they decided to move, not the landlord.

The vast majority of rental properties are not being sold from under people. In my anecdotal experience, bad tenants get booted much more often than good tenants.

That's not to say I don't know people who broke their own leases or indeed, bought properties off landlords. But I absolutely in good conscience could not put a young family through the worst case scenario over and over again and people who want to pretend that kind of thing doesn't come at an enormous cost give me the shits :)

Obviously it sucks when you are forced to move, but it's been pretty uncommon for myself.

We rent and have been in our current place for 8 years (Central Auckland suburbs).

Since I left home (almost 30 years ago) I've flatted or rented in 6 other houses in Auckland. Only twice have I ever needed to move at the landlords request. Once they sold, and the other time they wanted to move back in.

Sounds really like 1st world problems to me. Moved 10 times in 10 years (and have owned a house for 2.5 years during that period), never was an issue for us to stay in the same school zone. Even if not, so what? I went to 3 different primary schools myself. Some people really have an aversion to change! Close minded?

Oh good, because it wasn't an issue for you, it's not a problem at all? Feel free to keep normalising adverse outcomes of broken markets dude, but I'm going to keep talking about them as 'adverse' outcomes because they're not going to stop happening if you just expect everyone else to "suck it up", nor do they come at any less of a cost.

Time to put the spade down and grab a coffee.

I'm pretty sure there is a link between kids who move a bunch and adverse health outcomes - I kind of feel pretty strongly about stuff like that.

But to be safe I had about six coffees and now I'm coasting a serene high so trying to be a bit more constructive :)

Yes, it's bad out there, real bad. The lack of parenting is far worse than the covid epidemic. It only we had invested the covid budget in trying to sort this!

Right, can you post evidence of the link please or is it just your reckons? I mean if you feel strongly about it it must be more than an I reckon?

There's plenty of reckons about this on Google.

Agree, I don't want to put chasing an extra dollar ahead of stability for my child growing up.

"Sorry you had to change schools, but look, daddy has an extra $50k saved for his retirement. Thanks for your sacrifice!".

Stability vs flexibility and resilience ... just saying.

If you have evidence moving houses impacts educational outcomes or health outcomes then please share, otherwise it is personal bias rather than evidence.

I mean there has been plenty of research done on it which suggests it's the case. I'm not saying it is indeed the case, but that I just don't know for sure and would rather err on the side of caution. Some children might do alright, others not so well, it's all very subjective. As a parent you won't really know until after the fact.

- https://www.apa.org/news/press/releases/2010/06/moving-well-being

- https://www.washingtonpost.com/news/wonk/wp/2016/06/13/moving-as-a-chil…

- https://www.uktherapyguide.com/news-and-blog/can-moving-repeatedly-in-c…

- https://www.psychologytoday.com/us/blog/thinking-about-kids/201007/movi…

From a study

Moving house ≥2 times before 2 years of age was associated with an increased internalizing behaviour score at age 9 years. This association remained after adjustment for sociodemographic and household factors. There was no association between increased residential mobility in other time periods and internalizing behaviour, or mobility in any period and externalizing behaviour. There was no effect of lifetime number of moves, or of an upwardly or downwardly mobile housing trajectory. However, a housing trajectory characterized by continuous rental occupancy was associated with an increased externalizing behaviour score

In other words we as a country caused the ram raids. Well done. Could have encouraged investment in shares but no.

Isn't that exactly what you're doing by assuming everyone "sitting on the side line" is "putting their life on hold"? Because it is a problem for you it has to be for everyone? You've probably been spoilt by life and don't realise what real life problems are.

Because it is a problem for you it has to be for everyone? You've probably been spoilt by life and don't realise what real life problems are.

You had a point to respond to here, but because of the baseless personal attack that you couldn't help but throw in there, I'm not going to waste my time or energy on it.

So suggesting someone is change averse is a personal attack now? People in the parliament call the other side way worse than that. You definitely have a filter in front of yours eyes making things appear a lot different than they really are.

To develop my point, you realise there are people in this country suffering from terminal illness, sleeping in their car or having only one meal a day if they are lucky? I believe we should be more grateful for what we have and less envious of what others have.

Seriously, is house buying in NZ is the only thing in life?

From your comment, it looks like we really are probably a housing obsessed country. And who's fault is it?

Hence the ridiculous prices of houses and we expect them to keep increasing

You sound like you've never owned a house?

by Yvil | 9th Mar 23, 9:57am - You sound like you've never owned a house?

Yvil, you're making uneducated assumptions about others. In this instance, why does house ownership status even have to matter? I'm a house owner and I also think we are a house obsessed country. Some are so obsessed they feel/felt the need to build portfolios and load up on debt. Right now that's probably not a great predicament to be in....

We are a housing obsessed country. We kind of had to be. That's not really my fault, I'm just dealing with the fall out.

I do agree though, keeping your family in warm, dry accommodation that doesn't suck a huge portion of your after-tax wages should far far easier than it is. But what would we talk about instead? The weather? People will be wanting you do something about that next, that's a much harder nut to crack.

We should be talking about destroying the current system as it stands and the narrative that housing is an investment class, you can't lose with housing, house prices double every 10 years, safe as houses, etc...

That means we will need to accept massive price house falls and many people going through a lot of pain. With any luck it will be painful enough that it completely reverses current attitudes and a new better system emerges from the ashes. The horrible system that fucked us all over is never allowed to rise again.

It also means vehemently opposing any political party that tries to jumpstart things back to what they were again - looking at you National.

Inflation is running so hot that I would argue prices don't even need to fall anymore to get that outcome. But we should be doing everything in our power to stop them rising again, agreed.

Lots of people do not understand real price losses and only understand nominal price drops. Maybe this time will be different but I expect we will need to see significant nominal price drops to below pre-covid prices before the spell is properly broken at a national level.

Blocking Singapore buyers from NZ market would also help.

So a lot of people’s discretionary wealth is destroyed and we are more equal. Then what? Houses are much cheaper, interest rates are high enough to stop speculation. Everyone lives in a house, few rentals. And we put our extra money into the bank at a 6pc. Or maybe renovating our house. And the wealthy few become wealthy through hard work and innovation and farming. It’s the 1950s all over again.

We as a society can choose to organise ourselves any way we want. The global changes that are coming means the current system is no longer fit for purpose. Climate change, resource and energy depletion, demographic shifts are beginning to reshape things and we can either front foot it or bury our heads in the sand.

We've all been eating apple pie. The pie is only so big, and a tiny minority hoard nearly all the apples. Over the last few decades we've managed to make the pie slightly bigger by growing more apples so even though this tiny minority have increased their overall share of the pie everyone else has been reasonably quiet because they got a tiny bit more.

Unfortunately we've maxed out the orchard and now the pie can't get any bigger, in fact we push the land so hard it's actually losing nutrients and it's producing less now than before and will continue to decline into the future.

Unless that is, those who sit at the top stop hoarding all the fucking apples.

Define "discretionary wealth". Hint: it has nothing to do with home values.

Dp

How many new builds coming on the market, with the builders finding themselves with no equity or negative equity on the completed house, be a few I suspect. Watch out for the investment (too good to be true 12.5% return and your unsecured investment), start to show up.

is there a simple list of price change per Month pls? per Quarter is just obfuscation.. i know it’s simple arithmetic but ..

So what will the February NZ Median price be? Make a guess.... Over or under $730K?

https://www.interest.co.nz/charts/real-estate/median-price-reinz

Under

Th big kicker is TD are back (5% plus return). ALK house prices need to drop 40% plus to get close to a 5% return. Until that day, NZ property (esp. AKL) will remain toxic (low yield, no capital growth, no tax incentives, depreciating value).

You are 100% right here. We are looking at buying our future family home and have just recently sold our city fringe town house in Auckland. We are in a fortunate position where we could have held and leveraged through, however the return on renting the property was 2% per annum vs. paying +6% on interest.

For the simple reason above, I think the lower end of the market has a lot further to fall..

Spot on. And the rest of the regions will follow Auckland on the way down as they followed on the way up.

Agreed. Without the tax rinse this should be a real blow for speculation. More new stock coming on line everyday to give renters better options as well.

If the housing market trends towards prices that can be supported by the rental of a property:

i.e. something like price ~ (100 x weekly rent x 52)/(mortgage interest rate)

then in a lot of areas the prices probably need to fall by 40 - 50% more.

If that starts to happen, does the government and RBNZ decide that inflation is the lesser evil when compared to a massive housing crash?

Sound like you are promoting a New Zimbabzealand ?

You know a bag of hyperinflated, worthless Kiwi$ to buy a loaf of bread?

Not for me.

Bonfire the specuvestors and lower housing cost all round please!

No, I just hope the government/RBNZ is far more frightened of New Zimbabzealand compared to a massive property crash (that they helped create)

Agreed. Let the specuversors catch fire, with their own greed acting as petrol.

Will the 'Bank of Mum & Dad' be part of the review? Wonder how they are feeling. Pretty awful how some people have been sucked into the market last year. I suspect a number of people are in negative equity and the 'Bank of Mum & Dad' have lost thier deposits. Mate of mine works for the ASB and said to me, watch the s*&t hit the fan later this year. Too many houses are and have been built, with a filing cabinet look to them. I suspect buyers will try and leave these in droves as they see they are rental investments that will be neglected . With in a couple of years they will not be desirable. I still remember many people/politicians/business people screaming we need to build more. We now see the problems of hiding facts and only addressing supply, not demand. They will now scream we need more workers, so they can get immigration to support house prices through increasing debt.

Anyone know if the banks are getting worried? Will they get caught with mortgagee sales where the market has dropped enough so that they don't recover all their $?

RBNZ maintains its stress test and says everything is ok. Banks are also exporting record profits to their Aussie masters so they have some buffer. That said in the last couple of years banks are reducing overhead left and right via less staff and closing branches.

What do they think is coming....?

Yep everything is tickety boo .....untill one day it isn't!!!!

I recall the US Feds Ben Bernanke and GW Bush saying the US economy is strong and solid in 2005 -2007.

Then the shiz got sprayed floor to ceiling!!! as the GFC crash contagion spread .......

Agreed. The play made to isolate the failures, bury rates and not mark the market are why we are where we are now.

And that’s the problem coming down the line that no one seems to think about.

if unemployment raises above seven percent then why the need to import workers?

No need for the workers, no need for the rentals to house them... correct it does not degrade in a linear way.

The construction industry crashing should create enough unemployment to keep the RBNZ happy?, so they just need to keep increasing the OCR

It will be really interesting to see whether any housing supply is 'unlocked' by reversing house prices, as owners realise it doesn't make sense to hold empty places for capital gain.

It only becomes truely available if its reasonably priced..... much is just filling the books.

There is literally tonnes of fruit and veg at the countdown I'm at. Supply good and prices not bad. Inflation will drop and then int rates and then HPI UP

by HW2 | 9th Mar 23, 12:51pm 1678319506 - Inflation will drop and then int rates and then HPI UP

HW2, when is this happening? Will the wheels need to fall off the economy first before the RBNZ 1-3% target achieved? Are you forecasting this on the basis "it always has, so it always will"?

You're right RP it is the old formula I am using

IF the economy stays up AND IF inflation continues, then the ballgame has changed

With those 2 ifs you will be champing at the bit for property to fall without stopping

by HW2 | 9th Mar 23, 4:19pm 1678331967; You're right RP it is the old formula I am using. IF the economy stays up AND IF inflation continues, then the ballgame has changed.

HW2, your comment tells me that you've not considered the real possibility of the economy falling into a stagflation stage. One can take comfort in knowing that, while property prices may be falling on an accelerated basis, eventually it will stop falling :) I think its known as the "dismay" point of the Boom/Bust cycle.

With NZD tanking and rates climbing all over world. Inflation and rates will stay high for a number of years, HW2 again you show how naive you are with financial matters.

Or maybe like Japan in 1989

Property values half every 5 years.

Then quadruples over the next 5 to 10 years which keeps the 'ponzi' going. Inflation assisted of course.

Doubling every 10 to 15 years is only 4.5 to 7 percent compound. That is probably slow compared to what happened last time when inflation was last running.

Houseworks you cheeky little spruiker monkey you. It's soooo impressive how you manage to defend a Ponzi scheme by banking on an unsustainable level of inflation. Keep up the good work!

AFR

Australia faces “significant pain” in the residential construction sector as rising interest rates and uncertainty “play havoc” and push down building starts, Macquarie has warned.

Analysts at the investment bank told clients a backlog of work “will likely erode soon” and forecast that home renovation activity will fall

Today I watched a 2 bedroom unit in a block of flats sell for $425k. A year ago the one next door sold for $510k. Both units were in a similar condition. Another place sold last year for $980k, and was passed in today on a post-negotiation bid of $870k. This is Christchurch - so we are catching up to those Nth Island price falls now.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.