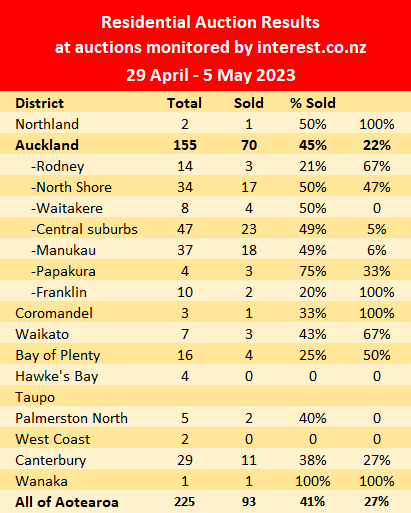

There was jump in the number of properties offered at auction and the number that sold under the hammer in the week from 29 April to 5 May.

Interest.co.nz monitored the auctions of 225 residential properties around the country at the latest auctions, up from 193 the previous week.

That was not particularly significant because the number of properties offered has been bouncing around the 200 or slightly above mark for several weeks.

However the increase in sales was more impressive, with 93 properties selling under the hammer at the latest auctions, giving an overall sales rate of 41%.

The sales rate had previously been stuck around a third for the last couple of months.

The increase in the sales rate was particularly noticeable at the Auckland auctions - see the table below for the full regional breakdown.

A clue as to the reason for the higher sales rate could be in the comparison of selling prices and rating valuations.

At the latest auctions just 27% of the properties that sold achieved prices above or equal to their rating valuations, down from 37% the previous week.

That suggests vendors may be being more realistic in the current market and adjusting their price expectations downwards to achieve a sale.

Individual details of all the properties offered at the auctions monitored by interest.co.nz, including the selling prices and rating valuations of those that sold, are available on our Residential Auction results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

179 Comments

As is reported on the other piece on here today:

None of today's data will be welcomed by the Fed. It does not indicate that inflationary pressures will be easing soon from a slowing economy.

It doesn't matter whether any of us think what the Central Banks are doing, or are about to do, is right or wrong. All that matters is what they are going to do. And along with the rest of them the RBNZ is going to raise interest rates further.

Buy into the property market knowing that; fine. But make sure you've factored in a large rise in financing costs. And maybe even that calculation will still be on the low side....

You assume the increased finance costs are permanent. Thats a big call, knowing that a fairly standard play when things slow down is that central banks and governments will throw money around.

Have a look at the historical nature of mortgage rates in New Zealand. We are STILL under the long term averages. So wherever rates go from here, they have plenty of upside just to get back to 'normal'.

Will we revisit the levels of 2007-8 and an OCR of over 8% again? Probably.

Can you point me towards this immutable law that says interest rates have to attain a certain historic average?

The law of averages.

That's a belief, not a law.

Possibly, but it also Math.

What's the average price of Kodak stock?

It had an average, unlikely it'll ever find it again.

It's literally there in the name... ;)

This message was sponsored by the law of sarcasm.

Should they be so low as to be over-stimulatory? especially when inflation is at risk of spiraling?

And can you do the same - that mortgage rates always fall over the duration of the loan? Or is this confirmation/recency bias because it is what you have experienced in your adult life?

Not saying either is a certainty but it does appear that we’ve just broken a 40 year trend of falling interest rates - anything could happen over the next 30 years for a FHB taking out a loan…who knows..mortgage rates could be 10-15% in 10 years time. Or they could be 2%!

All I know is that I wouldn’t want to be sitting on a mountain of debt right now given that the money supply is contracting for the first time in nearly 100 years. The outcome of this could be unrecognisable compared to anything we’ve experienced in our lifetimes.

I watch what underpins the low interest rates more than anything.

I feel they're a hallmark of late stage capitalism, and there's a certain level of confusion that the covid-derived high inflation, high OCR environment is a reversal of a longer term trend.

Now, it could be that there's a persistent level of global disruption that keeps inflation high for the next 20 years. But assuming stability returns, it would seem more likely for lower long term rates.

Note im not encouraging debt levels on this assumption, or even have much at stake on my end, it's just more useful to determine what sort of future we're likely looking at, instead of going down fantastical rabbit-holes.

The last 30 years of low inflation were an illusion. We continued to see steady domestic inflation, but it was masked by importing deflation through cheaper goods. Wages have been held low due to demographics (Baby boom during peak working years), but with falling birth rates and an aging population this will be harder to maintain. And deflationary impacts of cheap imported goods was the result bringing almost 1/5 of the worlds population (China) into the global workforce - and this won't be repeated. Both of these impacts are now in sharp reverse. Global population is peaking faster than many expected, and China is no longer driving down goods production costs due to rising wages and some crazy demographic shifts (thanks to the one child policies).

We will look back at this ultra low inflation/rate period as the anomaly, not the new "norm".

They were an observable trend, no illusion necessary.

And there's still a pretty healthy volume of cheap labour around the place outside of China.

The bigger question seems to be how those in the developed world retain their lifestyles.

I have a fairly strong suspicion many don't.

Bingo - and that is exactly what centra banks have been either hinting at or openly saying - we are going to be collectively poorer going forward and there is no escaping this (obviously there will be individual exceptions).

Weve drawn too much wealth from the future into today (by playing silly games with the cost of capital/QE etc) and now it loks like it’s time to pay to pay the price for that.

2020 might have been ‘peak wealth’ where people thought they got richer siting at home getting paid by the government to do less (while asset prices exploded much much higher) - but in reality all we did was create an IOU for the future.

I think theres plenty of wealth in the future and the value of the global economy will only increase this century.

What's occuring though is the dispersement of this wealth is shifting.

I was a bit shocked when I looked today and saw how many banks have their fixed one and two year mortgage rates above 7%. I thought most were around 6.5%. I clearly haven’t been keeping up.

At these rates property prices certainly have further falls to play out.

Unless people take a 3+ year rate under 6%.

Sure. The problem with that, of course, is that a lot can change in 3 years, and rates might be around 4% in one or two years.

I think you would only do 3 years if it meant the difference between getting a mortgage or not.

btw 6% is still high relative to the debt many will need to take on.

Buy housie on a 3+ year interest term.

Don't buy housie.

If it comes down to the two, most will take the former.

If you have 20% equity you won't be paying over 7% unless you're floating...

True. although even many of the ‘special’ one year rates are now above 6.7%, which again is higher than I realised.

Just locked in one mortgage with ANZ for a yr at 6.1 percent got one floating mortgage at 5.23 with ANZ both 100 percent tax deductible and way cheaper than 18 percent that I first paid way back 30 odd yrs ago

That's right, the advertised rate isn't typically what people are getting offered either... especially in this environment where banks are fighting over business.

Is it though?

Because 18% on a $250,000 mortgage is cheaper than 6.1% on a $800,000 mortgage.

Two examples I have done in last two and bit years brought 3brm house on a 1012 sqm section (when the market was going to crash remeber that ) brought for 325 000 rented the day I brought it for 400 aweek. Parked my caravan on the back as I live in my caravan. Built a 4brm house and subdivided the section on it for 235 000 rented that out for 550 aweek. Capital value 1.2 mill.

6 months ago brought another 3 brm house on a 1012 meter section again rented for 400 aweek. Got my caravan at the back just got plans I to council last week for a 4brm going to cost me cheaper in subdivision costs but a little more in build costs but that's my job for next year to 18 months why can I build for so cheap cause I do everything myself bar electrical and plumbing. So in your example I have gotten two houses for the price of one and pretty much the same yeild it's called thinking outside the box. The over educated ones can't or just have a job mentality

Brilliant example

Are you LBP

Qualified builder 38 yrs only need to be LBP if working for clients or selling your houese. All my houses I own and don't sell so come under a law called owner occupier most people don't know about. Haven't worked in a job and or own business for a few yrs now. Don't get me wrong when I build my own houses I do everything from obviously the building side to the roofing plastering painting tileing landscaping, 7 days aweek people call me a machine but a totally different experience than when you are working for someone or clients it's not work.

You sound very happy good on you. Long may it continue

Either you started with a tonne of cash or have a secret I dont know about.

You're earning gross yield 8.8 pct on the $560k before interest. You mentioned 32 pct debt loading @10pct ie 18k pa. Rates and insurance ain't cheap even in small townships. 5k pa of property management fees

32 percent is across my whole property group I have property from Taupo to Oamaru. That example was only on my last new build so there is still 100 percent mortgage tax deduction. Still cannot add the capital growth I have made on building on the back of existing house swinging a hammer for a boss. The years keep and pay for the asset and gives me an income which I don't need alot of.

Congrats for your achievements, I wish every kiwi was as hard-working as yourself.

But did you say it will take 18 months to complete the next new build

That's subdividing and depending on supply issues which you have to take into account. But I am the only one on the job apart from sparky and plumber so I did the pile holes I put up trusses I put the roof on I put the gib up ceilings as well I plaster paint tile lay lawn. Get the picture. That way I don't need to conform to the H and S bullshit that walks on 40 000 onto a build plus and I don't have these so called young know it alls that spend half the day looking at their ph. So 18 months is max.

PS no didn't have a ton of cash grew up in the most deprived area in NZ the Hokianga left school and home at 15 and half. But worked every hour there was. It's the 4 letter swear word of today wife and I would do our jobs during the day then at night and weekends. And owned rentals while still rented ourselves but made real money when we left Auckland 35 yrs ago. That's the key people have this huge asset that they work all their life for which hopefully goes up in value but dosent generate and income no legit tax right offs wether that's just insurance and rates. All the time trying to impress people my wife gets on my case when we go out that I always wear my work boots

Also, these high interest rate tales from years ago never account for inflation. 18% then and 6.1% now will be a similar real interest rate.

Yeah but back then hourly rate was 15 dollars an hour for a qualified carpenter. Not 40

Yeah but don't houses get built 3x faster now?

Only joking. So it's not just the hourly rate you have to factor in, but the productivity also. I actually think it now costs closer to $100 for what used to cost $15.

Good on ya Colin, you sound like a weapon.

They probably do but a so called qualified carpenter now only knows how to stand up frames. The last paying job I was on the company sends its apprentices to its competitors to learn how to fit windows as they leave that to the joinery company and the apprentices only spend a week so they get the paper work signed off. I got taught and did everything by my employer a tight hard Dutch builder. And NZ builders back then were in high demand cause they could prep a floor hang doors pitch a roof etc etc not anymore

Everyone's a specialist now.

But yeah, you're right. Building houses is now standing up pre build framing and bolting it into a pad. Im sure it's more expensive now having a dozen or so individual contractors doing individual tasks.

And everyone passes the buck so where as a small problem say a wall out by 5 mills becomes a major 60 mills wall out on the 2nd story and when found out the person shrugs the shoulders well it isn't my fault and nobody has the nouce to sought it out because the pretty picture on the PC screen don't show that. All the apprentices want to do is get qualified then sit there site management course so the can sit in the office container and tell everybody else how to do it. You think leaky building was a major issue you ain't seen nothing yet. I give it 10 yrs

Data by credit bureau Centrix found 19,300 households are behind on their mortgage repayments, up 26 per cent on the same time last year.

Be prepared for more falls as buyer sell up.

And the be kind government says,-

Finance Minister Grant Robertson recently told the Herald on Sunday support for homeowners battling high mortgages was not in plans for the upcoming cost-of-living-focused Budget.

Hence why I don't live in a house you see these fools spend big money to impress the Jones. On average people up grade their house ever 7 yrs. So they are just working to keep the roof over their heads and once they get the mortgage under control and house has gone up turn around sell and buy a more exspensive one. What I did was buy a 20k caravan self contained and rent the houses out and build new. Carry about 32 percent debt on 10 percent less than what the banks value my properties at. Don't work for the man haven't for several yrs so if the shit really hits the fan just go find a job.

You sound like you love your work. As well as building do you manage your rentals yourself? Are there enough hours in the day?

No I spend my time building and finding houses I know I can add value and get a reasonable return on but get good capital gain. I am not good at dealing with people I know my knitting get good professional property managers who make certain the rent comes in means I focus on what I am good at the management fees in the grand scheme of things is chicken feed

You sound like one of the few people who can make money from property in the current environment.

That's right but I drive a 96 landcrusier which I have had 22 yrs done 900 000ks have no debt apart from property debt that is all getting paid for by rents and I don't need to keep up with the jones

Read all your posts! All strength to your arm.

Wrong. It's what they WANT us to THINK. Doesnt mean theyll do it.

Reality is sinking in. Houses are not made of gold

It's good that claim, made by no one, has been refuted.

People are flowing into the country at a greater rate than they're leaving.

The country is about to go into another 2-3 year period (or more) of under building.

The long term view of house pricing doesn't look like it's heading for coal level valuations.

But who is flowing in and who is flowing out?

The fruit pickers are coming in, and the brain surgeons are going out. It's as much about capacity to borrow (to buy) as it is raw migration numbers.

Brain surgeons are usually pretty well off, and are less likely to relocate.

The outflows are over represented by the underhoused with intermediate levels of experience.

Many of these new New Zealanders come with their own money.

And that's what makes a market - difference of opinion.

And as we all know, it's being able to afford to be wrong that matters. A lot of heavily indebted New Zealanders; the ones that set marginal price levels, can't afford to be wrong.

In the end what you think doesn't matter. Neither does my opinion. All that matters is what Adrian Orr thinks.

It doesn't really matter what he thinks either. The market is more than one entity, so the trick is trying to spot actual trends, from singular pieces of news.

Which is why I posted the original quote.

None of today's data will be welcomed by the Fed. It does not indicate that inflationary pressures will be easing soon from a slowing economy.

It doesn’t matter what Orr thinks either.

what matters now is in the hands of tens of thousands of businesses who will each individually decide what they will do with their price book this year, and next

Yeah, nah.

The current profile of most immigrants is not one that suggests high levels of wealth to throw at house buying.

It doesn't need to be high. Our market is so small it gets over manipulated by small movements.

Gets a bit tiring the people on here that think all the immigrants are coming into NZ broke. There are countries with over a Billion people and no shortage of millionaires wanting to leave for a better lifestyle.

Yes. But correct me if I'm wrong, they can't buy here until they have the right status? And that takes time.

The days when you could walk down the gangplank at Queenstown airport, go into the estate agents and buy whatever you wanted came to an end sometime back.

Do you think everyone else is talking about things happening in 15 minute intervals?

No, but many spruikers are talking as if the recent immigrant surge will have a very near term impact on house prices.

How about the 164 000 new NZers this govt gave a passport too who have been here for several yrs working hard saving which they are better at than most average NZers and all of a sudden they can buy a very high percentage will be looking if not already buying. Oh and that's another figure the over educated got wrong its was only going to be approx 60 000 then low and behold a 164 000 man if I got those figures wrong in my business I would be broke luckily I am not educated

Okay. So those people are already here, presumably living in rentals. They buy a house and free up a rental. Hopefully their former landlords don't have mortgages to service. Maybe they could take a solo mum living in a motel, since all landlords do the work of Jesus.

The reverse is also quite boring - but everyone has narrative they want to form or create.

I never said they are all broke. But if you look at the jobs that make up most of the immigrant profiles, and their country of origin, it’s not suggestive of individuals with much in the way of wealth.

Of course I could be totally wrong and perhaps many nurses from the Phillipines, many tradies from South Africa, and many cooks from India are coming here with 200k+ In savings.

Why would one leave a place where they have done very well for themselves to come to somewhere like NZ where their hard work would be immediately eroded simply but the cost of buying a house?

You could be top 10% in wealth in many nations and yet deploy 100% of your wealth just to buy an average house in NZ with nothing left to show for it…it would be a drop in living standards to move here for them in many cases as you then become like us and have all of your net worth tied up in your house and nothing left over the do anything you want to do/enjoy to do.

Good point. Why go from the mid-upper echelons of your own society to the lower- mid echelons of one you don’t know?

I guess things like safety play a part, especially for South Africans.

Most of the migrants coming from those places are the more well off people from their societies.

That doesn’t mean anything if they are coming from a third world country!

Their upper middle class are often a lot wealthier than our upper middle class.

There's just an awful lot more poorer people.

This thread has deteriorated in quality. I work in the medical arena. The latest appointment from overseas in my city is early 50’s, a surgeon, with a large private practice in the RSA. He sold up and came here to escape concerns about the safety of his family. Top salary step specialist who is still renting a year on and now has a wife who needs to work to be able to afford a house in the city for 3 kids.

The immigration flow will put more demand in the property market. However, let’s divorce what suits our narrative from the reality of where we are in NZ. Housing stock is still over valued compared to incomes. If you have paper wealth from surfing the asset value wave all the way to the beach you are sitting pretty. If you rely on some modest savings and a good job (as with this example) to buy a family home in the city suburbs it still doesn’t cut it.

I don’t have any skin in the game except my family home but it’s tedious listening to comments here that are based on bias.

It's the Saturday morning auction thread. It's not where you come for deep thoughts.

Hold on, I thought you were in the camp talking up the impact of immigration.

‘Caught’ just showed through anecdote how even high skilled, highly paid immigrants are here and struggling to afford to buy a house. Let alone those much further down the food chain.

Fruit pickers are deflationary and add to export earnings

Yeah I'm not sure why the fruit pickers cop so much grief.

Or do people not want fruit anymore? Its all very confusing.

Nothing wrong with fruit pickers, they are willing to work and pay tax rather than sit around doing nothing and complain.

“ But who is flowing in and who is flowing out?

The fruit pickers are coming in, and the brain surgeons are going out. It's as much about capacity to borrow (to buy) as it is raw migration numbers. “

No need to buy, we won’t have enough houses to rent. $400 per room per week, Wi-Fi included.

The looming underbuilding will be a big factor, but as a factor that supports house prices it’s probably at least 1.5-2 years away from having any significance.

Note to other posters: I rarely care what's happening in 6-24 month periods.

You are aware the new regs that came in on 1st of May. Triple glazing 6 by 2 exterior walls as thicker wall insulation and R 6 ceiling insulation. Oh how this govt and the greens scream we need cheaper housing yet bring in more costs. Example men cannot lift triple glazing in so you will need a hi-ab to lift all joinery in now all more costs on new build keeping the older existing house prices up

Yes of course I am aware of that. It’s just the icing on the cake in terms of house building slumping in the near future.

But in the mean time, there’s a stack load of houses to be completed in the next six months.

Not disputing that this is a real issue, for myself that cost isn't so bad as the house will have better thermal performance. My issue is I don't see any effects of increased productivity and technology. Staff these days are required to be trained, certified, and continually recertified for everything and that cost is passed on to the consumer. Why are health and safety persons paid multiples of tradespersons?

They are if you can add value

I would love to see your house.. is it 22 or 24 carat?

Nope I live in a caravan but own alot of houses which I buy but then build on the back basic 3 to 4 brm warm dry new houses but all these new regs coming in are for all new houses just got my next house plans in last week. Before these came in

Land is. Better then gold.

The more paper wealth we stack away in land prices the more tempted broke govts will be to tax it. Wage and salary earners are now tapped out, inflation has buggered up money printing, realised capital gains have turned to losses. That leaves unrealized gains. The past is no longer a great predictor of the future because the system that rewards land speculation is collapsing.

As a old tight Dutchman told me 40 odd yrs ago. They ain't making anymore. Land that is but I wish NZ would follow Singapore, Netherlands and China and re claim land I.e the hauraki gulf imagine if all that good rich soil that got washed out every year thru the rivers was dug up transported and filled and to say from Howick to Waiheke or drege the firth of Thames imagine the gold they would fine as they dredge it. So accomplishing several things more land for Aucklanders to build on Waiheke connected to Auckland so reliable transport and cheaper and people closer to the cities. Oh that's right we live in NZ so nothing gets done

The green lobby groups dont want to protect the land we already have from dropping in the sea. By use of sea walls. They say let nature take its course. I recall seeing the Coromandel surf club building being undermined before there was a last ditch overnight effort to save it being washed away. Conservationists had stood in their way to block their consent, how utterly idiotic. I sure hope that the Gnats turn the tables and "break some walls down"

Never listen to a Dutchman!

They are making new land all the time.

New land to build on is being developed every day.

Reclaimed land is new land as well. All of wellington waterfront us new land. Half of Dubai's waterfront is too.

Every house I have ever been thru that is owned by a Dutchman has been a cluster fark of home handyman unconsented ugly wooden disasters.

I never buy if dutch guy has owned it!

Shaft, although I am not Dutch, these are very racist undertones. I expect that if you are the old Hemi account but he got cancelled and you have already been warned by the editors.

Oh piss off HW2 your a gas lighter!

And you told everybody here I would be gone by lunchtime Friday,🙄🙄🙄 soo.... Get out of lala land compare my likes 👍 to yours, and feck off to Sharna land a have a "Anti everything cry 😭 together.

Facts are not racist undertones!

So stop tagging my comments like a kerekere cry baby!

Sales rate increased - yes. Prices stopped falling -no. Once prices stop falling and sales rate/volume remain healthy, then prices have hit the floor. Are we there yet? - not by a long shot. The big question is, the distressed selling phase, how long will it last?

Yeah, well 6 months ago you were shrieking that no one will want to move to NZ because it's so poopie-doopie bad, and that's already been shown to be well wrong.

You could power a car off your negative energy.

Morning Pa1nter :)🚙

Always good to catch up in the Saturday morning toilet thread.

I take it you’re pro immigration painter?

If so, what do you think is a healthy/manageable/sustainable level of migration? (ie one that our infrastructure and services can handle going forward)

We're a country of migrants, so it'd be hypocritical of me to want the door shut after me.

Whether it's migration or natural increase infrastructure should be maintained and improved.

I think we should have a level of migration that satisfies our job market requirements and pay as you go tax base. I couldn't tell you what that number should be, off the top of my head.

Well I’m asking you what you think this would be because it’s important. You appear to want more people (for business and to support house prices - correct me if I’m wrong?) but do you want the associated drop in living standards as we become more congested and have less public service/s per capita as a result?

Or are you willing to have an overall drop in living standards for everyone so that we can support business and high house prices, with no limit or control on how many migrants we bring in?

Were the numbers pre-covid appropriate in your view?

Even then house prices were going flat around the country and it was only the emergency interest rate drops that pushed prives higher (while we had no migration at all!)

He doesn’t care.

by Pa1nter | 5th May 23, 11:57am

I agree it is another pathetic attempt to kick the can down the road

Isn't all life just kicking the can down the road.

Some people sound like they expected to be bequeathed a perpetual comfort environment.

I don't know how you got that I don't care from the comment of mine you quoted.

It was more a response to the notion that life and society is somehow a game you can fix for perpetuity, rather than an ongoing process.

It's about trying to leave the world a better place than we found it.

I know that's idealistic but if everyone just gives up and pursues everything out of ruthless self-interest with little concern for negative externalities we are even more screwed than we already are.

The choice is either to deal with problems upfront or kick the can down the road. We have been kicking way too many cans down the road. It will be an ongoing process but we do have a choice to at least try and solve some of our long-term problems before they get even worse.

It seems to be a lot more about talking about things than doing anything.

Case in point, it's extremely cheap to start a business, and embark on all the productivity gains and forward thinking sustainable business models one can devise. Off you go, no more talkie talkie.

How is it extremely cheap to start a business? I feel like most business owners would disagree with that.

What I have been advocating for is restructuring the tax system so it's less dependent on a growing tax base and having asset holders start to pay for some of the services they benefit from which I have talked about at length as a potential option. You disagree with my views and that's fine but it's not like my opinion is worth any less than yours.

Off you go, no more talkie talkie

Rude lol.

It costs about $50 or there abouts to register a company.

asset holders start to pay for some of the services they benefit from

Assets usually don't have a high service requirement.

Aspiring business owners just need to lower their expectations. They can't expect to have the same type of business as their parent's generation. Maybe try cutting back on the avocado on toast and coffees, and start with a basic wrench.

That's pretty much the size of it. People starting a company these days seem to think the first order of business is a new sign written vehicle, and a bunch of self promoting social media posts.

In all seriousness there actually seems more opportunity out there than ever. Cultivate a product or service people want, get really good at delivering it, and go deliver it.

All that's needed is tenacious graft.

What a stupid comment, so registration covers your development, infrastructure and acquisition costs now does it?

Based on that logic you must be spinning up new entities with the companies office everyday.

I guess you run a business and your only outlay is your rugged determination.....

Im saying the act of starting a company is really cheap.

It's a response to many cries of people waiting for a government to somehow foster all these highly productive, high paying businesses for them to go and benefit from.

I've started and run many businesses. I generally find it really hard. But also, way easier than waiting for someone else to do it.

A piece of paper is hardly starting a company Pa1nter and you well know this.

If anything that piece of paper is an immediate administration liability.

I'm glad we agree, running and scaling a business (though rewarding) is hard, far from "simple"

Companies are varied.

-Some have longer paths to profit (many are a terrible idea for all time)

-Some have higher initial capital requirements

-Some grow from one dude and accidentally end up with thousands of employees.

-Some require very little input but still make money

There's so many ways it can go down. The biggest problem is people go into things blind, and biased. If you know your business and market well, it can be harder to fail.

E46 you are Idealistic and naive.

You know the theory of everything and the practicality of nothing.

You want oil gone but want the medical benefits that oil produces (plastics /chemicals)

You want the poor to not have what the rich should give up!

You want NZ to pay the price of being a climate change warrior yet let the big 4 pollute more in an hour than we do in ten years .

You want electric cars for a rich minority but no, or expensive Petrol for the poor.

You want more houses but no ," ultra polluting" concrete, steel roofs, treated timber, tip filling gib board....

Mate, you should join labour green confused double talk spin the spin wankery parties.

You could save NZ from all it's issues utilizing talk fests, conversations, Hui's, PowerPoint presentations, meetings on your specialist subject...

," I KNOW WHAT IS BEST FOR YOU,!"

JEEZ, DUDE, ARE YOU THe GUY that will tell the poor kiwis they can't have X because X is banned here because X was determined by those that loved using X to be bad.. however X is still being used by billions in China, India, Asia...

X could be electricity powered by fossil fuel burning generators like all Maylaysia use (( because it's cheap there) to keep their power costs affordable so the poor can live!

X could be concrete that certain poor countries need to build houses and hospitals that can withstand hurricanes... Nah ban it !!!

X could be many things that the NZ and CC morons deem bad but are essential in poorer nations

Will. You give up you phone, car, tv, heat pump, concrete driveway for some one in Ngaru?

I doub't it. And until you do you are just a fffing virtue signaler

And when you say "we" this and " we that... How about changing that to " I" and walking the walk!... Or just STFU,!

Hi, Shaft nice to see you as well.

All of the above that you have said I apparently want isn't at all what I have been saying. You have listed a bunch of stuff that I have never even talked about, I don't know where any of that has come from.

You can think what you want about me but it's whatever I am allowed to have an opinion and comment here and so are you. I don't know everything but neither do you.

I work in the manufacturing sector, I don't want to get rid of oil, kill the economy and businesses and add more consultants to the government or whatever. I don't like labour or the greens they're useless and have made the country worse off. I don't think we can be a climate leader only China, the USA and the EU can lead in that space. I have another comment on the electric cars and stuff but it isn't at all what you think.

My above comment isn't about the immediate term maybe in another 50 years or so stuff is going to break but I don't actually know what to do about that so it's whatever. I do think we need to at least give some thought to the future and the world we are leaving our kids behind though I think that's fair enough.

Go back and read some more of my comments on other things and you would see that, I don't want to ban anything. I don't even want to halt all immigration I just want it to be done at a rate that doesn't put too much pressure on our infrastructure.

The main thing I have been arguing for is shifting tax burdens off of incomes and taxing land as in my view it would be more economically efficient. People should get to keep what they earn, I don't see how it's "fair" that someone earning $200,000 a year has to pay 39 percent and someone who inherited a bit of land pays nothing. The superannuation system isn't sustainable that's just what it is. We need a better way of paying for it if we want to keep it as it is.

E56. I didn't read your comment as it would only be excuses and more clap trap two faced diarrhea.

When you venture beyond your office, city , country and see and experience what I have you will realize how small NZ is and how much the world needs what you , the greens, and the industry that profits from CC say it can't have and all because of ego centric twats like James Shaw and Jacinda Ardern and their positional posturing

IO, is this what its like debating with a toilet brush? 🤣

Spending too much time on the sh*tter IO & Retired Poppy?

by Nifty1 | 6th May 23, 10:41am 1683326463

Spending too much time on the sh*tter IO & Retired Poppy?

On the topic of excrement - does this comment add to discussion at all?

Ad Hom on a finance news comments section is quite bizarre. Someone says something one disagrees with and it irks them enough that they feel compelled to create some whitty insult for what purpose exactly? To impress the wife and kids?

"Hun, where are you? Come here a minute!? Check out what I called this bozo"

"Yes, okay that's nice dear....".

Projection!

He actually provides a very well reasoned response to a comment further up so don’t completely agree

What I want is something different entirely. But that exists in a realm very far from what's likely, or possible.

But there's a deficit of taxpayers and workers, and it costs hundreds of thousands of dollars, and takes decades, to make new ones. We are facing a rather large amount of reduced services per capita by continuing to decrease our worker and tax base.

So the most tolerable scenario, is introduce already grown workers. That would improve the overall burden on existing workers, I'm not sure how anyone could even argue that.

I don't know what that amount of people is though, sorry. If I could get a clearer understanding of how bad the future liability shortfall is, that'd give me some understanding.

Pa1nter, do you think our cost of living is an upfront concern or a drawcard for immigrants? I get the feeling many will now view us as a stepping stone to Australian citizenship....

Your default mode of thinking is that anyone should leave for Australia, so that's not really news.

I dont think cost of living factors very highly for most migrants, no. I think they're drawn to the environment, higher wages (than where they're from), and vastly better political and societal landscape.

"higher wages (than where they're from), and vastly better political and societal landscape"

Oh-okay then so just so we understand each other, which countries have these Doctors, Nurses, Teachers and alike - come from to cover our skill shortage that are attracted by our higher wages and vastly better political and societal landscape?

South Africa has been mentioned quite a bit. The UK, we get some Aussies move here, decent parts of Asia. Those are our most likely candidates, through a combination of geography and alignment.

Most countries have nurses, doctors and firefighters.

You added teachers after (actually looks like you ended up editing your post multiple times, hard to track). Im less concerned about teachers, as our birth rate says we're going to have 25% less students soon.

So, in the light of changes to Australian citizenship criteria, you're implying the Brain Drain as its referred to is fake news? Why do you think Australia changed the criteria? Answer - to attract our brightest and finest....

BTW, correct me if I'm wrong but I understand that South Africans that you hear mentioned a lot cannot transfer their entire wealth to New Zealand...

edit

Every aging nation wants migrants.

The brain drain has been discussed ad nauseum since the 90s. NZ still experiences net increases in migration. Australia is a richer country (via luck), so will continue to be a draw from NZ.

"Every aging nation wants migrants" Yes, and 3-1/2 hours away many young perceive higher wages and overall superior cost of living is for them. In light of the recent changes to citizenship rules, their parents/retirees will likely follow them.

I'm not sure what your point is. NZs a migrant nation, with a population free to leave. So we will have people coming and going.

We have a very close neighbour, who are wealthier per head of capita. That's the most desirable place for people to migrate to, in the area.

Most people though, generally stay put.

The good news is, when you're right and NZ is in terminal population decline to the benefit of Australia, you can say you told me so. Assuming we're both not already dead.

Pa1nter, I think I've made my point :)

"You whipper-schnappers don't like it here? W-w-w-w-well just leave why dontcha?"

"W-w-w-w-wait, where are you going?"

Ha-ha-ha :) Nzdan, it might be you left switching off the lights!

Have you seen the cost of a rental in Aus that's if you can find one that is. Have talked too several on the ground over there and it ain't how it is made out in the media and or govt. Things ain't as Rosie over there as one thinks.

But then the exact problem we have now will be a problem for future taxpayers will it not? And mass immigration at the rate we have been going clearly hasn't actually been improving services, has it? What you are basically describing as a solution is basically a pyramid scheme.

So the most tolerable scenario, is introduce already grown workers. That would improve the overall burden on existing workers, I'm not sure how anyone could even argue that.

This is entirely dependent on what the workers are actually doing though. You are absolutely correct if the people coming in are doing jobs that either pay enough tax to offset the services they use or are directly working in jobs that are required to maintain those services. But it would appear that importing more people hasn't helped our services cope with aging demographics. Infrastrucutre has not kept up with the intake, service quality has been declining.

Most are not saying we need to stop immigration, but wanting the intake reduced to a sustainable level.

And mass immigration at the rate we have been going clearly hasn't actually been improving services, has it?

Our largest issue is the huge financial burden of over 65s.

So it's less a question of services improving, it's whether the rate of deterioration has halted.

I feel like you are ignoring the first point, is this not just deferring the problem to later? We will still have the exact same financial burden when immigrants age, especially if they bring their parents and grandparents along with them. It just doesn't strike me as a sustainable solution.

Sorry which problem?

A society needs a certain volume of new entrants. This goes for whether it's a tribe, a village, or a country.

Developed societies produce less children. This is mainly because females are more educated, have kids later and have a smaller pool of suitable males to select from.

So, our options are, find a way to grow people outside the womb, bring in labour, or slowly die, with the descendents having an every decreasing range of opportunities and services.

The buck has to stop somewhere though. The carrying capacity of the earth cannot hold an infinite amount of people. Unless we become a multi-planetary society or discover some kind of miraculous new form of energy the growth will have to stop at some point before we kill the host.

Does society need new entrants? Or does our current financial model need new entrants, they aren't necessarily the same thing. We probably long term need to have a more sustainable relationship with the environment around us. Or do you believe infinite growth in a finite world is possible?

Now you're talking across many areas at once.

- we don't actually know what the 'holding capacity' of the earth is. Is it 3 billion people living like us in the West, or 20 billion of the great unwashed?

- the global population is on a downward trend, without any intervention.

- our financial model and society are intrinsically interlinked.

- if humans ultimately can't work out how to live here then nature will have the last say and ultimately the planet will keep going.

This is supposed to be a financial site, not personal philosophy. Our current societal model is deeply broken on an interpersonal level. Will it improve? Hard to say, but I think the sorts of mechanism and measures being discussed are a million miles away.

The biggest problem our kids will have is a dramatically *declining* population. The demographic collapse is evident in *every* civilised society. Japan and most of Europe are a bit ahead of us, but it's still going to be a massive problem here.

China's is aging faster than any society in the history of the planet and will cease to exist in the next couple of decades.

I think you hit the nail on the head with "discover some kind of miraculous new form of energy". That has been, and will always be, the event that giant leaps in living standards will require. And it will happen.

AI is coming on pretty quickly and hasn't got the downside of strings attached like family and kids to put more burden on the country that new immigrants do.

The allowance for parents and grandparents is pure insanity.

So is the continued payment of super to those 65+ who are still working or sitting on income-producing assets. Want a retirement benefit? Actually be retired!

The big question is, the distressed selling phase, how long will it last?

Adrian Orr has made it quite clear with the Funding for Lending Program.

The only thing that counts is how his banking mates are getting on. Once their profits fall ... Adrian will do whatever is necessary to ensure they keep making money. (It's about 'financial stability', don't you know.)

Second tier lending, what could go wrong? https://www.oneroof.co.nz/news/43513

Resimac has cheaper rates than all the 4 big banks use them quiet often there is a cost thou in setting it up but that's the cost of doing business still beats 18 percent interest I have paid in the past yet stillmaking 9 to 10 percent return on property plus 100 percent tax deductions on my new builds.

You could have pushed me over with a feather... more sell if the vendor drops their price.... who would have thunk.. this is the start of the behaviour that will form the bottom. Too many people wont sell at "THAT" price as the vendor of the next house won't accept "THAT" offer. A good 12-24 months of this will form the base. I think we will have a tough summer market as those clinging on finally accept reality, the base may form next winter. If we see loads of forced sales then all bets are off (market will not base until forced sales stop). Sit tight this summer is going to be very interesting as stock floods the market, expect DTIs. A base can only be found on returning sales volumes, as this illustrates buyers and sellers have finally started to agree on value. And it needs FHBers to be able to afford to drive the buying chain. People look to past sales of the same house and sales relative to cv at the time of sale, I think we may settle about 30-35% off the peaks, the dev sites lower as they are just land value. New builds of quality will fall less, but shitboxs are history as those buyers can now allows less-shitboxes

Well said!

Dti have the potential to be nuclear. It enforces debt to be supported by income. Paper equity stacking would be more or less irrelevant.

Imagine needing 70-80% equity

The DTI does have the potential to be highly effective and efficient if chosen at the right level (<5). But the Government would never allow that as it would affect too many MP housing portfolios.

Government signs off on DTI measures here: https://www.interest.co.nz/property/111579/govt-signs-dti-measures-whic…

Its not so much an "if" its more a when.

2 years ago though. RB are now easing LVRs and Govt has amended the application of CCCFA

HW2, can you clarify what this has to do with the core intention of DTI?

I know you misread your early retirement. You aren't dumb enough to also misread the signals above are you?

The article from interest.co which you linked was from two years ago. Its hardly recent but I guess you are arguing that it is still relevant. On the other hand the recent moves by both Govt and RB to ease up restrictions is intentional and will help lift the market. Or do you think they will then about face and start adding DTI shackles.

Cue some poppy ad-hominem

HW2, I can tell you're rattled and can't answer the question. Here's another question for you. Can you guarantee the RBNZ won't impose DTI?

edit

by Retired-Poppy | 7th May 23, 8:51am

HW2, so you can't answer the question?

No you'll have to put up an easier question. Anyway good come back, enjoy your day.

If only you would learn to swim in more shallow waters....

Hahaha 🤏

Did you stay up late with a cup of ovaltine to watch the new king read his vows.

Dirty Harry will hopefully be back on American soil and out of Charlies hair

OCR down at 3.5% and we'll have a new Governor at the RBNZ in 12 months. Lots of new regulations and controls on residential lending by 24 months. May you live in interesting times ....

Buyer demand under pressure elsewhere as well - rising Debt rates?. In fact, buyer settlement is as well!

Australia-China trade specialist went on a property buying spree in recent years, splurging on a handful of properties from Point Piper to Vaucluse, but more than a year later he is yet to settle on $80 million worth of the prime harbourside real estate. As vendor patience runs out at least two of those properties have already been returned to the market, and Wang is facing hefty losses in forfeit deposits on all four houses.

https://www.smh.com.au/property/news/what-could-go-wrong-an-80-million-…

But are his losses in forfeit as hefty as the vendor's losses in potential sale price? Bet they're not happy either.

I'm guessing a lot of AUS' recent price increases is due to more external buyers taking advantage of their lower-than-everyone-else interest rates (what is the ratio of sales going to investment vehicles rather than OO?). What happens as those increase?

Just a guess, and not an educated one either, at that. Perhaps someone else knows better to correct me?

The B&T Auckland auctions certainly sold a few more house than usual this week. Vendors appear to be a bit more realistic in their price expectations. I noticed at least two selling for a significant loss.

Some vendors managed to get some really good prices as well. I added a couple more houses to my watch list of houses that got what I think was a good bid yet were passed in. I am now watching 20 such houses and as of this morning none have subsequently sold. A couple have list prices below the best bid.

Anyone of the patrons here writing a lot of comments have been to open homes or auctions recently.

Don't they all look highly staged by the agencies to rope in the dumb buyer's?

Yea but that’s always the case. Rain or shine, bull or bear market. People will stage things as best as they can.

Still reckon there are more motivated sellers to come. A lot of mortgages to roll to a higher rate, more rate increases to come, and inflation on spending still roaring. As seller capitulate via $1 reserves etc, the valuation software the banks look at will ratchet downwards putting more pressure when refixing.

Add in election year and talk of a CGT or a land tax and RBNZ promising Dti in early 2024. Also wonder how many more US banks need to fold before another 2008 like credit shock reoccurs?

Make your call, jump in, hold em, or fold em.

DTI regulation will be the dagger, to slay the previously eye watering reinvigoration of the housing market ponzi.

Once we reach the depths of this once in a lifetime property collapse......the reset will be done and the DTI will set future housing price inflation at the "average longterm" wage rise of just a fraction over 2%.

Good.

Or……..everything will be just fine 😀

Yep property usually just bounces back time and time again, that's pretty much why every man and his dog pile into property.

Agreed!

We'll see a whole swath of recent get-rich-quick land lords who are just now discovering the pain of even a 50% hit to their mortgage interest deductibility. Next year, just 25% and then zero.

Unless of course the Land Lord Parties get in and then it's all back to normal with zero capital gain ... Or will it be?

I think we'll see many economists and politicians come to the inevitable realisation that the OCR is an extremely flawed tool to control house price affordability and supply. (It's use created a boom and the bust will be felt by many for a long, long time.)

Consequently, I expect regulation, with novel banking, investment and taxation solutions, will return to residential lending. The laissez faire approach inherited from the neo-liberal era clearly isn't working.

I hope you’re right, on both counts - that the OCR-as-universal-tool is dropped, and that other more targeted measures are introduced to manage periods of insanity such as the last ten years have been.

The OCR is not used as a tool to control house price affordability and supply.

Glad you pointed this out. Ocr has never been for purpose of controlling house prices.

No. But it can.

"..with hindsight, we should have locked in a five-year term when interest rates were closer to record lows, that wasn’t the advice given him by his mortgage broker and bank. “They all said a [one-year fixed term] was the right thing to do,” he said. They said, ‘You know, the rates might go up a little bit, but they’ve never skyrocketed’.”

Guess what? They are about to skyrocket.

https://www.nzherald.co.nz/nz/nelson-mortgage-pain-2400-interest-rate-r…

Stupid advice. With rates that low you have to ask yourself what of the chances of it going even lower, which was pretty much impossible or if it fell the end results would have been negligible or the chances of it suddenly going up significantly ie double or even triple back to the historic average. That drop was always an emergency setting due to Covid, it simply had to go up.

Guess what? They are about to skyrocket.

https://www.nzherald.co.nz/nz/nelson-mortgage-pain-2400-interest-rate-r…

bw how did you draw that conclusion from the article. The homeowner, an expat American is campaigning for 30 year fixed rates as well as no early break penalties. The red herring is that he is planning to throw in the towel of home-ownership.

I agree, I cannot see interest rates skyrocketing from this point either. Its understandable if he and many other disillusioned individuals are planning to throw in the towel of home-ownership. Like many tenants, they're simply tapped out. If only they'd heeded the warnings.

KRAAAAAAAAAKKKKK

*Bubble popping sounds continue*

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.