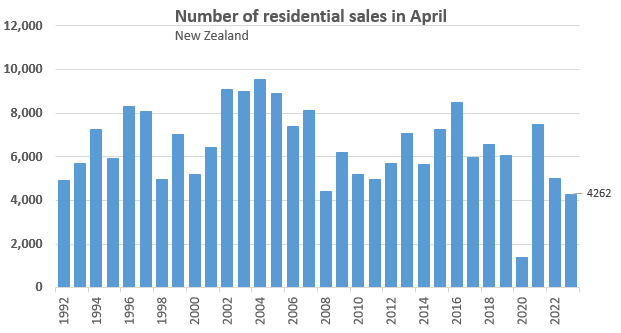

The housing market slump deepened in April with sales volumes dropping to a record low outside of the Covid lockdown period.

The Real Estate Institute of New Zealand (REINZ) recorded just 4262 residential property sales in April, down 15.3% compared to April last year. It's the lowest number of sales recorded in the month of April since the REINZ began reporting sales in their current format in 1992, apart from April 2020 when the market was in a near total lockdown due to pandemic restrictions (see the first graph below).

In April 1992, 4929 residential properties were sold, which means sales are currently running 13.5% lower than they were 31 years ago.

Prices are also continuing to slide with the REINZ House Price Index (HPI) , which adjusts for differences in the mix of properties sold each month, declining another 0.8% in April.

The HPI is now down 12% nationally compared to April last year and down 17.5% from its November 2021 peak.

The amount of time it's taking to sell properties also continues to stretch out, with the median days to sell rising to 47 in April, up by two days compared to March, and up by nine days compared to April last year.

The low level of sales is also having an effect on the amount of stock on the market, with the REINZ recording 28,643 residential properties for sale at the end of April. That's down just 2.19% compared to March even though new listings dropped by 22.7% over the same period.

The biggest declines in sales were in the upper North Island, with April sales in Northland down 24.7% compared to April last year, followed by Auckland -23.0%, Waikato -20.0% and Taranaki -20.7%.

All up, the figures the figures paint a disastrous picture of the state of the housing market.

"New Zealanders are waiting for the peak of inflation, a settling in interest rates and some clarity around the outcome of this year's election - this is what is keeping activity low," REINZ Chief Executive Jen Baird said.

"However for those looking to buy, lower prices and good stock levels means there are opportunities as we head into the cooler months," she said.

The second chart below shows the monthly sales volumes by region.

The comment stream on this story is now closed.

Volumes sold - REINZ

Select chart tabs

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

193 Comments

Chashamundo. If it walks like a duck and quacks like a duck........time the MSM started using the C word.

C you next Tuesday. Who are you referring too?

Let’s see Tony Alexander spin this one in his sponsored column! Didn’t he say 5% growth this year not that long ago???

Read his latest column on OneWoof. Something appears to have scared the bejeesus out of him.

Judging by the enthusiasm for property (as indicated by the bloggers here today) its long-term prospects are better than ever.

The only thing people want more than a property…….. is yet another property. But many of them will end up buying after the market has turned around - and prices are rising again.

Smarter folk often opt for a countercyclical approach - and, thus, are buying now.

TTP

Does it mean the stupid ones are taking a cyclical approach? You're not going to make a lot of friends.

He was also urging people to take a cyclical approach a little while ago.

No credibility

Yes - zero credibility.

"Smarter folk often opt for a countercyclical approach - and, thus, are buying now."

From the guy who also encouraged people to buy at the peak in 2021 and find themselves in negative equity.

Says a man who rents.... clown. Listen to those who trade well, we understand the market , not these one way spruiker fools.

The housing market is crashing if anybody took TTP advice last year the property purchased would be down around 20% the same will happen this year to next.

Like the people who followed your advice in late 2021 who bought investment properties in Auckland, Wellington or Palmerston North? They will now have lost around 25% of the value the property, and had debt servicing costs double.

Miguel - can you please post link of your updated graph - many thanks!

Team DGM

Stay away from the drinks man, and get some helps!

Within a few short years, the DGM will be wishing they’d bought property at the discounted prices of 2023.

Indeed, those who dismiss the wisdom of a countercyclical approach to investment display ignorance……..

Following the “lead” of the DGM is akin to following lemming rodents 🐀 as they jump off a cliff. ☹️

TTP

I'd suggest the people buying now hoping for a quick return to price growth read my comment further down. It's not going to happen.

As a CA with two accounting firms we get a lot of micro data across clients, we are seeing in the past month people entering Canterbury wide market that have been on the sidelines, the easing up recently on CCCFA making a real difference, don’t know if that will start to place a floor on the local market however a clear change is occurring with people securing finance in our client base that were not possible since December 21 when the credit contracted because of CCCFA. The demand never left just the credit..

Lads keep ya undies dry!!

Volume of sales have dropped but the idiot sureal estate spinners lead by that " theres sun in that downpour" REINZ CEO Jen Baird, still kèep pushing the high prices to the gulible sellers.

I suspect, at the persuasion of REINZ H/O, they are now ignoring "reducing" Homes.con algorithims and holding tough in a deseprate attempt to see if they cah hold out till summer.

Not a time to buy!!!

Reminds me that the deluded horncastle idiot predicted (and still has on his Instagram) that he reckoned average house price was going to increase from 810k sept 22 to 900k nov 23 . Comedy.

it's already very bad with the housing market, I'd say let it collapse, as many people were hoping for, and just leave it.

How is falling house prices "very bad"? I would have though that something being more affordable is a good thing. I don't understand baby boomer logic though.

I agree with you house prices falling is good thing, even while owning houses. But why do assume its baby boomer logic? Why did feel the need to insult a group of people, irrelevant of what their actual opinion is?

My in-laws are looking to buy and went to see a house, and apparently the owner is 89 years old, selling so that she can move to a retire home, but no one is offering even after she dropped the price about 200k below RV.

and I am not a boomer.

Many retirement homes want clients to have $1m in the bank before they'll lock in a spot for them, meaning there is more pressure on those needing care to hold out for high prices. Sad state of affairs in that basket even though the overall effect of lower prices (I say lower, but realistically we are still only correcting the last 2-3years worth) is the opportunity for people to make a life for themselves in their own home

Everyone loves a home vs a rental, and everyone loves one thats already 17% less then it was 18months ago.

Shame even with this many $$$ off so many hard working Kiwis cannot afford one.

More to come, FHBers are the base, without them there will be no 2nd home buyers in 10 years time..... Rental investors cannot take their place, they tend to want to live at the bottom in high yield locations....

This sucker is going down. Their is NO VOLUME ON THE BID

The lowest mortgage rate we saw at the peak of the market was 2.19% - at this rate, you could mortgage $1,000,000 over 30 years for $3,792/month

At today's best rate of 5.99%, to get the same repayment, you can mortgage $633,000. So prices need to fall 36.7% just to get back to the same level of affordability for the marginal buyer.

And in forced sales and FOOP and we will likely overshoot this number by a significant amount. 50%+ falls would be my pick.

On top of this the BMD (bank of mum and dad) will not be very eager to dole out $300k deposits to the kids. So we have shrinking deposits, 36% less buying power. Record low sales rates, ever extending time to sell and current sale prices already touching on 2018/2019 pricing, inflation adjusted.

Also the peak of the market was not what anyone would have called affordable. So it needs 36.7% fall just to get back to that unafforadable level. Add in leverage unravelling (property investment was always a leveraged capital gain play for most) and it could get quite messy.

"prices need to fall 36.7% just to get back to the same level of affordability for the marginal buyer."

As has been mentioned here many times, there has also been strong wage inflation over the last couple of years so that is not true.

Just add "in real terms" to the statement. The worth of the house still needs to fall that much "in real terms",

One can argue wage inflation but this statistic has been mainly due to the main centres such as AKL, WLG, CHCH. A large number of NZ'ers across the country won't have gotten very much of a pay rise.

Jfoe had a good comment regarding this in yesterday's afternoon thread.

Change in Real Wages - 2022Q1 to 2023Q1 (HLCPI Adjusted)

- Forestry and Mining: -4.4%

- Wholesale Trade: -2.7%

- Accommodation and Food Services: -2.2%

- Public Administration and Safety: -2.2%

- Education and Training: -1.3%

- Information Media and Telecommunications: -1.3%

- Electricity, Gas, Water and Waste Services: -0.8%

- Arts, Recreation and Other Services: -0.4%

- Retail Trade: -0.3%

- Manufacturing: -0.3%

- Professional, Scientific, Technical, Administrative and Support Services: -0.2%

- Total All Industries: -0.1%

- Financial and Insurance Services: 0.1%

- Rental, Hiring and Real Estate Services: 1.0%

- Transport, Postal and Warehousing: 1.0%

- Health Care and Social Assistance: 1.4%

- Construction: 2.1%

Let’s see how long it takes for the first time buyers who bought in the last 2 years and end up losing their shirt, to save for a deposit again.

I don't believe in a -50% scenario. First, incomes are catching up (+7 or 8% on average in the private sector in 2022). Just a couple of years following that trend and you get +15% of borrowing power. Second, people (buyers) will use peak values as a reference, -20% already looks to be a "good" deal. As time passes pre-covid times will be less an less relevant (we're already looking 4 years back). That said I reckon there's more fall to come, maybe an other -10% in 2023.

"Buyers will use peak as a reference" - that sounds like hopium.

Anecdotally, the few friends of mine who have bought in the last 6 months all offered 20% less than the asking price, not the peak price.

Just a REA notify me of a sale that was offered @ 40% off, but 'can't tell us the sale price' - even though we knew the asking price. I'm guessing it was lower.

My position (for many years) that it is quite possible that at some point in time we could see around a 50% fall in real (inflation adjusted) terms. Have been saying this since about 2017 - just wasn't sure of the timing/when it could happen.

So if wage inflation runs >5% for 2-3 years and prices fall around 30% in nominal terms, then we're pretty close to that.

It think it is quite possible over the next 12 - 24 months.

FYI based on REINZ HPI data, from peak prices, estimated inflation adjusted price changes:

1) Nationwide: -24.5%

2) Auckland: -29.4%

3) Wellington: -31.9%

Remember how the property promoters were telling people that house prices rise with inflation or houses are a hedge against inflation?

The percentage impact on a leveraged buyer's equity magnifies the above price changes considerably, as many are now in negative equity.

The problem with your logic is that 7-8% wage rises without commensurate productivity improvements simply fuels more inflation and therefore higher interest rates and downward pressure on house prices. There’s at least another 20% to come but I wouldn’t be surprised to see 50% fall from peak to 2025 trough. And that would be a good thing despite the pain

Saying a good thing suggests to me you have a narrow view and appreciation on how wide the pain would be…and the consequences of that for all within the economy. The loss of options in people lives..

Disastrous? This is great news! Asset bubbles are terrible.

Disastrous? This is great news! Asset bubbles are terrible.

No it's not great news. People think that crashing asset bubbles mean cheaper prices. It's a very simplistic outlook. You're looking at the destruction of the nation's savings that has influenced the sheeple's consumption behavior for the past 20+ years. If they stop buying the Raglan Coconut Yoghurt and taking the winter holiday to Queenie or Fiji because they feel less rich, these impacts are far more damaging in terms of the economy. Behaviors are self reinforcing and feeds back in to the bubble. Prices go lower and the exceptionalism attitude turn to seed.

The hapy median/ medum?... is to fall to 2018 levels.

This would allow the genuine buyers a go without screwing the wealth gained by most except the morons that brought during covid chaos.

Pre-covid prices coming? How about pre-2017?

168 Saint Andrews Road, Epsom, Auckland City, Auckland

Premo area, DGZ, big section, etc. etc.

Passed in at $2.8m yesterday.

Last sold $2.8m .... in May 2017 !!!

Your optimism is endearing ... ;-)

Yup, as I said yesterday, the house I'm in has already dropped below it's 2017 purchase price, and the houses in the area that are selling are at a ~12% discount currently. Had a property investor friend around for coffee a couple of days ago, and he thought it's 2017 price was about 40% higher than it should've been, even then.

I hope my landlord's are well capitalised :D

Yup. Too many "investors" banking on a capital gain. Dumb.

It's always been about yield. Yield is here and now.

Anyone who thinks they can see 20-30 years into the future and thinks their untaxed capital gain is assured is a fool.

I suspect your property investor friend is no fool. Prices need to come down by that amount to allow the typical "mum and dad" investor to make a buck. At 2017 levels only extremely clever (and hard working, hands on) property investors can make a decent yield.

How does a hands-on property investor differ to a hands-off property investor??

He uses his feet.

Hands-on property investors do all their own maintenance, inspections, advertising, tenant support, etc. etc. while improving the properties by adding rooms, bathroom / kitchen refits, additional house, etc. etc. Pretty much a full time job

Hands-off gives it to rental outfit and just checks their bank balance from time to time.

The bad news was the inflating of the bubble in the first place. Instead everyone gloated about unsustainable rises in price fuelled by stupidly cheap money. Can't have prices sustainaby rising 20% a year, what you are saying is this generation's house owners got theirs, should keep their gains, and screw the next generation.

Its not the destruction of savings at all, they had a house, they still have a house, nothing real is lost. All that changed is peoples perceptions of how rich they where, and the amount they are willing to spend on frivolous thing based on that perceptions. As a society we need to consume less not more.

The added advantage will be that perhaps construction prices will also go down, so if you need to get your house painted it won't cost you upwards of $20,000.

Great comment, spot on

It looks like the heady falls of 2022 are behind us now in Auckland, the 3m and 6m percentage falls are clearly starting to head lower - remember this is a second order differential, I'm not saying prices are rising. However, at this rate I cannot see house prices returning to the median multiples that many commenters here want them to be. We will basically need a complete meltdown to get there, so substantial job losses and mortgage defaults. It may still play out that way but I don't see it. If Nats get in and repeal interest deductibility then I think that will go a good way to arresting any further price falls.

If Nats get in and repeal interest deductibility then I think the electorate will expect Nats + Labour + Greens to work together to introduce a CGT.

I'd expect the Nats will implement a fairly weak CGT that will affect only a few. I don't care. Once it's in the statutes it - like all other taxes - can be tweaked. Good outcome all round. (Won't inspire me to vote for any of the major parties though.)

We already have a weak CGT that only affects a few, it's called the brightline test.

We already have a full CGT that says if you are investing in property or any other asset for capital gains you should pay tax on it, its just that a lot of people lie and say they are not. The brightline test is just a bad attempt to stop people lying.

I think you are forgetting the house of cards that we live in. Many SMEs are financially backed by these assets. In turn many jobs are provided by these businesses. The rubber hasnt hit the road yet.

Based on the contraction I am seeing in my own business (and its happening fast), in a month or two the pain will start setting in with gusto. For reference, I import and sell leisure based products (non essentials), compared to last year we are seeing a 30% plus drop in sales. April hit, and the cliff appeared. Fortunately I dont have debt to service, but SMEs that do will be feeling it.

I did point out that severe job losses would put this under pressure. At the moment there is just no volume in the market, both sides are holding out and waiting for more information. In 6 months if nothing else changes the market will be flat or near enough - however, we know there is a lot to happen in 6 months. We will have an election, and the economy will either deteriorate or not. Both of those events could go either way and support the market, or push it further down. All I'm saying is that unless things get markedly worse the market will not be dropping to the level some people are hoping for.

Has anyone got an example of a good to premium house being sold at a loss, anywhere - Ak, QT, Coro???

I see discounts in high density townhouse and property development/land bank, but not elsewhere.

I have seen a couple on Auckland's North Shore, yeah. Only one listing still live, but I have seen a couple sales take place below the owners purchase price from a year or two ago.

Birkenhead - Bought in 2021 for $1.15m, been on the market for months and asking $1.098m, no takers

Thanks, there are just very few visible signs of market stress.

There was a guy on here a month ago tweeting every loss in AKL..... he got banned - there was and is pain, denying it is making you lose credibility in front of a lot of very imformed people....This site likes to talk rolled up figures they don't like personal examples published on here to much

What do you mean by loss.

Sold below asking?

Sold below GV and which year ( dudong covid or pre covid)?

Sold below last buy price ( plus inflation?)

Plenty sold below covid GV and a few below pre covid GV

7 in My areas below what they paid. All brought in covid period

Hi Te Kooti,

I'm tracking 250+ new builds that were one the market just before the peak in Oct 2021. Most are in the $1.75m plus range. When they don't publish a price you can use the price range features on most RE websites to see where they're going. Sure some got sold but the ones still there are going down and down. E.g. terraced house in up market area of Akl in Oct 21 was $2.75m+. Still on the market but now $1.9m+.

I'm also tracking auction sales of houses more than $1.75m. When they sell, I check the property history to see when they were bought and at what price, and whether they've been subject of a big reno or other substantial changes. Yesterday I posted a seller to took a 400k+ hit from a 2020 purchase. Believe me, they're coming thick and fast now. Even some bought way back in 2017 and even before are taking hits.

I don't remember post-GFC being quite so bad. And prices are still falling.

Thanks, very informative.

There is a weekly newsletter here .. copy n paste into your browser - then sign up

https://open.substack.com/pub/aucklandpropertyrealitycheck/p/auckland-w…

“However, For those looking to buy, lower prices and good stock levels means there are opportunities as we move into the cooler months”. I hate how Jen Baird can speak as though she advocates for buyers getting a good ‘opportunity’ when more sales and higher (or at least stabilised rather than dropping) prices are clearly what she would desire to increase income for her stakeholders.

How about the nonsense that the Aus immigration changes have so immediately affected FHB interest?

What’s affected FHB interest is unaffordability!

Not just unaffordability.

It's sentiment. The FOMO has gone. The spruiker narrative has taken a hammering. It's not completely dead in the water. We'll need to see the further price drops come through over the next few months and then stories of people being in dire financial straights, losing homes. It's still got a way to go yet.

There is a "pent up" wall of sellers praying for a lightening price recovery that, as predicted, is proving elusive.

In markets (FX) we call this overhang, and say there is a lot of wood to chop before things move higher..... Every day NZers get older and people want to sell or need to sell for health reasons, to release cash from equity due to job loss/health impact etc.

Also many have withdrawn there property as the vendor of the one they want to move to is still asking yesterdays prices.

Sales volume must increase before prices stabilise. This indicates that buyers and sellors agree on value.

For many sellors there house is all they have. Its their retirement lifestyle and they are very reluctant to sell lower as they are grieving the paper loss from the last 18months. Greif takes a while to process.

For many sellors there house is all they have. Its their retirement lifestyle and they are very reluctant to sell lower as they are grieving the paper loss from the last 18months. Greif takes a while to process.

If all the young people are more interested in Pepe than paying for overpriced houses, that also spells big problems.

Take it from me, the house youbhave at 50 will not be the house you have at 80.

There is a retirenent move then a aged care move.

Asset price - meet gravity, I mean interest rates, I mean risk adjusted target gross yield

Gone is the long-held boomer psychological advantage!

No fun when the rabbit has the gun.

See ya at the bottom ya dawgs

-SMG.

Bullshite, 🙄I'm a boomer (just). Cashed up ( 50% of my propertiies)and looking excitedly for the bottom. The lower the better!🖕

Ya Richard cranium!!

Very well then, fossil

-SMG.

Dollar each way. Up or down i cant lose.

50% spilit in cash v property assets was a smart move.

The ones i kept can drop 60% before i blink.

👌👌👌👌👌👌👌👌👌

"I'm alright Jack"

Oculos Pasco - you wear it well

Who knew that enforcing some degree of lending responsibility by the banks, shuttering the tax avoidance model, and being forced to have more normal interest rates by rampant inflation would deflate the ponzi of greed and stupidity.

It was obvious really. More to come.

The big question is when the herd of speculators really panic, how bad will the under shoot be...?

Labour has done well on this. Housing was our biggest issue and they have done well to address it.

You are correct on that point. Shame they are bonkers in others, and keep pushing uncampaigned agendas.

What is happening in our housing market has nothing to do with who is in government.

If they have no effect why are National so keen to reverse all of Labour's efforts to cool the market?

Because it's election year, and National are trying to win votes.

Well it hasn't won any vote from me. In fact it shows their true colours so much that I don't think I'll ever vote for them again (I haven't the last couple of times anyway)

Nats policies arent bad overall. IF they will drop their efforts to kickstart house prices in favor of building a proper productive economy - i am all in. If not - Winston gets a tick

Which ones oldskool?

Education also looks terrible. Which ones do you like the sound of? I'm open to being persuaded but all I saw was recycled populist junk that has proven to be innefective.

When your political party's number 1 mandate is to present a point of difference and shout down anything the opposition does, then all you end up with is recycled ineffective populist junk.

This is the point that irks me the most.

Historic, enduring cheap money and inflation is what counts here, the knuckle draggers in Wellington are irrelevant.

But, but, but...... iNteReST DeDucTiBiLiTY!

What exactly did Labour do??

Interest rates where lowered, They spent a whole lot of money, causing inflation meaning interest rates had to come up accelerating the crash which should of happened a long time ago.

CCCFA... that's what lit the match to this housing inferno. Interest rate rises are just the fuel...

Nah, the CCCFA is a scapegoat. The banks already knew what was coming, and they were already starting to batten down the hatches before this went into law. The timing was just conveniently used to pin the immediate blame on the government.

There was a wave on inflation rising all around the world, that had been labelled 'transitory', well before CCCFA happened.

At best, CCCFA just saved some people from themselves.

they lent the banks a ton of money virtually interest free to lend to speculators - which drove a 30%+ surge in prices during a Pandemic -- instead of investing it on infrastructure and productive go forward technology

Removed tax deductibility on mortgage interest and underwrote bank financing for business loans during COVID

The rest was Reserve Bank of NZ which removed LVRs and lowered interest rates, which were the most impactful IMHO

Yip, us cashed up boomers love a looney labour house price fall.

Speculaters dont panic when their asset v property holdings v cash balance is groovy baby

You appear extremely proud of yourself.

And looming over the horizon we get 'news' that's softening us up for what coming.

Mills said wealthy people should be paying more than they were. He would be in favour of both a capital gains tax and wealth tax. “Those who can afford it should be paying significantly more taxes.” He says it is “bad for the economy to be tax-advantaging asset classes like residential property”.

https://www.stuff.co.nz/business/132001093/wealthy-new-zealanders-say-t…

Has anyone checked how many of these 96 people make donations to either Act or National?

I'm prepared for that with my Aussie account set up and ready to receive.

We are still very early stage into this mere 18 month crash........these housing crashes take on average 6 years to play out, to bottom.

Japan being the outlier of over 20 years!!

Early days and will require bundles of popcorn, as the specuvestors will writhe and gnash teeth.....as the promised Onewoof Spruiker lies of doubling every 10yrs, crack and collapse towards a DTI of 4 - 5.

Japan being the outlier of over 20 years!!

The team around the water cooler reckon that we are far different to Japan. When I pointed out that the NZ bubble compared to the Japan bubble is 50%+ as big (measured by total housing / land stock value to GDP), I got looks of disbelief, confusion, and even contempt.

Trust me. The denial is strong but the faith is still there. Like watching the ABs down 10 points heading into the final 15 mins. Nervousness but everyone feels that we're going to pull through.

Plenty of cheap houses in Japan - maybe we could pay NZ super to Kiwi's who retire and go live in Japan - good for both countries

Plenty of cheap houses in Japan - maybe we could pay NZ super to Kiwi's who retire and go live in Japan - good for both countries

Kiwis are not very culturally adaptable and generally not good at foreign languages, particularly the Anglo Saxon-Celt stock. Better option would be an agreement between NZ and Vietnam where the oldies can be shipped off to places like Da Nang - wonderful environment with all the amenities.

I also got looks of disbelief, confusion, and contempt 2+ years ago when I used to say to people I know (including professionals in the property space) "... but what happens when property prices start coming down again?".

It's an emotional thing for some. For example, most people don't seem to have an issue understanding that a property is worth what someone is prepared to pay for it when the market is on an upward trend, but for most that same understanding somehow disappears in the downward (at the start anyway) portion of the trajectory. Though emotions provide little comfort against increasing living costs and vanishing low-interest loans (although we knew it was unprecedented) - I hope most people knew that when they decided to take the dive near and during the peak of the market, but I'm also nervous that a lot of people didn't.

https://figure.nz/chart/bOXOzYWW8RyIotwx

1992 there were total 1322800 dwellings ,2022 there were 1944300,

So comparitively to the total number of dwellings ,the actual percentage of dwellings sold is significantly worse, Right?

Compared to Greg's 1992 in the article, the number of dwellings sold is 40% less ,than the worst April in the last 3 decades , April 1992,is actually 50% better than April 2023, IN % OF TOTAL EXISTING STOCK SOLD, so can Greg Update it to worst April since WW2?

Correct.

Prices will be rising by the end of the year. Buy soon. Ironically the more it crashes right now the sooner it rises, and to a greater degree. Rising population, new builds stopping, it will have to equalise- just like it had to over the last 18months because prices got too high, now it's because they're too low.

🤣🤣🤣🤣

End of this year sounds a bit early, but night is always darkest before the dawn. Problem with most reporting are 3 month late.

Role up role up. $1m in Turangi. Be quick....

As a fly fisherman, I spend quite a bit of time in Turangi, I love the place. Sure it has a rough side to it but there is a great community feel as well. I have never felt intimidated by the boys in red.

But the prices that where being obtained for complete shitebox uninsulated ex-hydro workers huts was NUTS.

Now I look at the river side and sure there are nice houses, I worry re a 1:100 year flood, that riverbank may not hold next time.

I saw 300k bid to 800k in 5 years.

There is much pain to come in that market yet.

To an outsider it looks bizarre. How about 1.4M for a non-shitbox like https://homes.co.nz/address/turangi/turangi/213-taupahi-road/xq72G

There are not many places where you can step out the front door, and be at a world class trout pool without having to cross a road, the riverside properties by the judges pool etc price like coastal and are quite sought after by the ex stock broker brigade. Fly fishing is a passion, many will live there for the winter season and also holiday in summer. I have never seen the appeal of Port Waikato.... so there is a place for everyone. Some of these Turangi houses are owned by people whose wealth you can only imagine, they are mainly holiday fishing lodges for the family.... the other side of the highway is a different story.

No one wants a Crash. That's socially and economically destructive. But we could halve property prices today, and still be at the overinflated prices of 7 years ago.

What the economy needs is a rebalancing away from asset speculation and towards productivity. If that's new dwelling construction, fine. But recycling what we've already created at ever-increasing prices? No.

It will take a lot longer to achieve a smooth correction (as is written above) and what we see today is just the start of what hopefully will be an orderly process.

But if not....then...we get The Crash.

Actually that's exactly what we need.

The social fabric damage of NZ is the greatest its ever been, because of the over allocation of debt in property. This seeking of rent enslavement of other has been driving price to the simy stupid levels we see today.

Try borrowing for a succcessful business. First question.."how much is your house worth"...

Haha - yeah its a total mess, with no party cottoning on yet that they have to completely wipe the slate with policies and come up with a vision and strategy to dig us out of the mess.. into a better place. Wait a few months and its gonna get quite depressing in NZ.

Add one year.

And the uptick will not be rampant.

In Spruikerville they are snorting hopium and smoking the greenshoots.

Sorry, this is early days and much more required to reset, to get to 4 or 5 DTI. Then its legislated, Spruiker then staked, done.

TA and AC are then egged by the masses.

Spruikerville they are snorting hopium". Haha - classic. Will reuse this phrase from time to time.

There will ALWAYS be someone telling people that now is the best time to buy.

Why?

Because these people need to earn income to put food on the table to feed their families, pay for the roof over their heads (either rent or mortgage). More property transaction volume and transaction values financially benefit the following groups of people:

1) real estate agents

2) mortgage brokers

3) property mentors

4) property developers

There are others.

Positive spin leads to increased confidence to persuade people to buy.

Always remember the vested financial self interests involved.

There will ALWAYS be someone telling people that now is the best time to buy.

Yes, they are all over on the Property Investors FB group that I just joined. Apparently interest rates have peaked, the interest deductibility rules are getting rolled back, and we are headed back to the moon later this year!

HW2 must be absolutely punishing his keyboard, firing questions at ChatGP to try and come up with his usual spruiker spin.

Thanks but no

You guys can have the floor and vent

I have visions of a snake oil salesman, hurridly sweeping the bottles of oil into a suitcase, and high taling it out of Dodge City.

Who was that?;

Based on…..?

Prices will be rising by the end of the year. Buy soon. Ironically the more it crashes right now the sooner it rises, and to a greater degree. Rising population, new builds stopping, it will have to equalise- just like it had to over the last 18months because prices got too high, now it's because they're too low.

This fits in the consensus around my water cooler and neighborhood BBQs.

Investor friends of mine (I'm not a house owner myself) are of the firm belief that the election and increasing immigration will stabilise the market by ears end also. Said friends don't tend to listen to data and logic when it comes to predictable human behaviour, ability for borrowers to borrow etc, they will tell themselves whatever it is they need to in order to sooth the troubled minds and self-reinforce that prices will keep rising in the medium term. In the meantime they think they'll get peak prices because some investor will come and snap up one of their properties seeing the opportunity. Wahp waaaaaahp

You’re mistaken. In fact they are still too high, by some margin. Check out longer term average prices, not just the last 10 mad years, then adjust for actual inflation and you’ll see why. And if still in doubt check out prices in other similar western countries. NZ still way overpriced

CGT will be coming for the greedy landlord's profits, and your Kiwi Saver as well!

Summary

- Every year, billions of dollars of capital gains are made, but almost none of it is taxed. This is because New Zealand does not have a capital gains tax (unlike most other countries).

- This means you can buy assets (homes, art, shares, classic cars, crypto and even racehorses etc.), sell them later at a profit and keep 100% of the money you make. This is very different from how income tax operates.

Once again: its still the same asset with the same market value. This is not the same as price which simply reflects money as the medium of exchange, re/devalued by monetary and fiscal policies outside the control of the asset owners.

There is no real "profit" in such asset CGs (note this not the same argueable case in business goodwill CGs).

The house might be the same asset but in reality the land changes. The land absorbs all the good (and bad) work by the community and government in the area that surrounds it. The zoning changes, the bus stops and shops, playgrounds and schools...

...funded by the homeowner ratepayers.

Wrong.

Funded by society through work, private investment, general taxation and government spending.

Ratepayers pay rates which only funds the council's spend which is only responsible for a small amount of that uptick.

If we were to have a capital gains tax, would it be on nominal or real capital gains? How would you measure a real capital gain? If I suffer a capital loss, would the IRD grant me a tax credit or a refund?

All those fiddly questions simply underline why a flat land tax is superior. Keep em coming.

All other OECD countries have a CGT and they're all sorted out those fiddly questions to varying degrees. To suggest lil' ol' NZ can't too is a fallacy of epic proportions.

That said, if I can't have comprehensive CGT I'd settle for a Land Tax ... For now ...

And particularly with shares, aren't the shares already taxed before they're issued to the shareholders? Company posts profit -> pays tax -> gives shareholders dividends.

My wife has a share in my income, if I give her $100 should she then be taxed?

Your Kiwisaver is already subject to a wealth tax called FIF. You pay tax as if you make a 5% gain each year. A higher rate taxpayer (28% under PIE) pays 5% * 28% = 1.4% of the portfolio value every year as tax.

Capital gains applies to crypto. Or if it doesn't I'm a schmuck and the money I saved doing my own taxes was false economy.

Capital gains applies anything you are trading in, shares, crypto, houses, sock puppets, whatever. What an account can do is tell you how to structure your trading in such a way that its not defined as trading.

From the horse's mouth regards to property: (https://www.ird.govt.nz/property/buying-and-selling-residential-property)

As a general rule, if you're purchasing property with the intention of selling it, you will probably have tax to pay on any profit you make.

I really don't know why people here and in the media keep saying we don't, we clearly do. Its just that people lie about their intent.

2. is partially incorrect, crypto gains are taxable at your applicable marginal income tax rate.

Will the median price data be added to this article soon?

It's always available. See top menu. Go to Charts, select Real Estate. (This is a great site.)

The vendors and their handlers lying through the nose RE agents are still not learning their lessons.

The buyers should just quietly quit the market and not go to any open homes. The prices really have to come down a lot to be making sense to buy a house.

I have only one life to live, so why live like a slave of the bank just to own a house.

It's a house with walls and roof and a carpet. I shouldn't have so put myself in a situation where after buying I have to make myself and my family sleep on a half empty stomach just so that I can afford the monthly mortgage payments.

Remember me saying that Auckland's flat-line in the REINZ HPI between 2016 and 2020 was caused by the introduction of the Auckland's new Unitary plan that allowed far higher densities?

And me saying that the fact the government - with cross-party support - has now legislated higher densities with the MDRS and NPS-UD that affect the whole country and this would assure no return to house price gains above inflation for 20-30 years?

Well - it is pleasing to note that this is now being picked up across many financial forums. It was even quoted to me by a real estate agent at the Akl Home show. I asked him where he got that view from. He got it from comments seen on a news site and a financial forum.

Those predicting a quick return to house price growth above inflation have no answer to my observation. If you think you do - by all means - post them here. I've seen no answer yet that refutes my hypothesis.

I'm not saying your wrong - but Auckland priced itself out of the market. Properties had hit north of a million, and interest rates were not yet at ridiculously low levels, so there was mass migration into the Waikato (for workers) and Far North (for retirees). It was cheaper to own an hour south and commute than it was to live there, so people stopped buying.

Helping this was Hamilton CC's ridiculous policy of restrictive zoning to push house prices up [Hardtaker is on record as stating they wanted Hamilton to have the same house prices as Auckland] - which worked, and also helped push people out into the surrounding Waipa district.

As a Waikato local at the time, it was extremely frustrating, as nearly everything was simply being snapped up by Aucklanders either downselling or leveraging their Auckland property.

(Note, this is a myopic view, I'll own that).

Yup. But now Waikato is just the same as every other major center thanks to the MDRS and the NPS-UD. House prices there will behave no differently to Auckland's did in 2016. (And Wellington - poor Welli - they've a long, long way to go.)

I think the unitary plan was a factor, but so was lack of affordability, after the mini boom from 2014-2016.

I think you are quite right that the massive recent planning changes will result in much less land value inflation (and therefore house price value inflation). Hugely abundant development rights over many more properties takes away the scarcity factor of development sites that saw a lot of bidding up from 2020-2021.

I don’t think we will ever again see aggressive house price inflation. Good riddance.

Falling house price is good so people can afford to buy, high inflation is also great because people will stop spending when things get too expensive. So let house price crash and inflation run wild…

Except inflation causes increases in prices that will not come back down. As the inflation comes back under control, the rate of price increases will slow until prices stabilise. Your wage will not always keep up with this, and you and everyone else will have purchasing power eroded away minute by minute, day by day like right now, until you too cry foul. Rampant inflation has decimated countries before, rendering currencies not worth the paper they are written on. Investors pull out of said countries, people starve and work to the bone for literally peanuts. Inflation is not something to allow or be passive in, it effects us all.

Inflation roaring. Can see at least another .5 OCR increase, possibly more. This is now less than 2 weeks away.

May the 24th be with you..

Just watching the Harcourts Grenadier auction online .

About a 3rd of properties sold so far ("des-res" in the $1.2M - 1.8M range) but everything else has been dead. No bids from floor, leaving the hapless auctioneer to place a couple of vendor bids before passing back to the agent.....

Where I live house sales down 20pc from March and prices still dropping. Multiples chains of sales cannot proceed until the first one is sold unconditionally. Winter started here today so the market will get even worse. This is the time not to buy as prices will get lower as more and more people struggle to cope with inflation. This is our new reality.

It can take a year to make a chain work in a market like this.....

13.5 % lower than they were 31 years ago -- how does that translate when adjusted for population and dwelling numbers growth - 50% down maybe ?

Someone has crunched the numbers higher up the thread

See my numbers in the earlier posts

Wake me up when residential rental yields and mortgage rates are above 8%, and average NZ house prices are 3 times average household income. Why fund a losing proposition.

For investment indeed, otherwise leave the money in the bank for a safe 5-6% return and enjoy popcorn as the mess unfolds.

The key number for me is the median value of the lower quartile house for each area individual area. When that number drops to 3 times the median salary of the local nurse/teacher/labourer for that area I will be happy. The local workers can then choose to buy a house rather than rent. Happy days suddenly.

Seeing some medians prices coming back up in April from March across Auckland... Rodney up 8.0%, Manukau up 3.7%, Northshore up 0.9%... Keep an eye on this...

Link please - thanks

Nifty1, keep an eye on what the HPI is doing here; https://www.reinz.co.nz/Web/Data-and-Products/REINZ-HPI-Report.aspx

Can’t trust median prices at the moment. Median price is not the best tool in a good market, it’s next to useless with the very low volumes at the moment. Median prices are soaring up and down in my area, based on whether the 10 houses sold in the month were large/small, old/new, rundown/pristine properties. Use the RENZ House Price Index… it gives a much clearer picture of the market.

Exactly.

Each house in it's merits.

The date of its last valuation is just as critical. 2021 shows no COVID HUMP! , 2022 BOOM YOUR OVER PRICED.

I COULD PAY over the top for a desirable local and win.

I could by a cheap house Moerewa and lose.

Timing is key but local is key too... But it depends how long you've got.

well... if you are a boomer you don't have much time left in this dimension :D

talk about long terms?

That's a lofty cherry picker you've climbed aboard to pick those numbers out of that report.

I'd say many here haven't even looked at the report... good to get a full overview of what's actually happening in each area of Auckland and/or city that you're interested in.

I am waiting for the 50% drop on this one.

https://www.trademe.co.nz/a/property/residential/sale/auckland/auckland…

Last Sold on 20 Oct 2014 for $3,600,000

They want $5.5m plus. They may be waiting a while but they'll most likely get it. It sits firmly in the "trophy house" category. They may not even get much motorway noise there either. As the Dutch say, lekka.

It's reasonable to assume that Chairman Moa wants to purchase it - or that someone in his family does.

CM's cunningness is undiluted.

TTP

Govt now propping up developers https://www.newstalkzb.co.nz/on-air/heather-du-plessis-allan-drive/audi…

How do they choose which developers to bail out?

Ones that are involved in large scale "affordable" housing projects.

Yes interested to know what qualifies as ‘affordable’

Perhaps the ones that agree to do a blanket sale to KO.

This sold for $2,785,000 last week and previously sold March 2021 for $3,205,000 a loss of $420,000 plus agents fees $70k https://www.barfoot.co.nz/property/residential/north-shore-city/devonpo… Highest genuine bid was $2.6m and negotiated up to $2.785 then no further bids when it came back to the floor

Where is HW2? Is this data too hard to polish?

He does not post on days like this, there are more and more of them recently.

If he does he risks the virtual lynch mob...

Then one day he will just disappear and reinvent himself at the bottom under a different userid, then one day the market will turn and he can claim to have called the bottom... not that he will have an equity to invest as he has been buying all the way down...

Why would I need to do that other than getting cancelled. HW3

$2.7M? I was expecting some sort of mansion, but it's just a little cottage with a push out the back to 4 beds on 500sqm of land.

Prices have a long way to fall yet. I can't believe how slowly prices have dropped, i thought we'd be back to pre-covid pricing by now.

by The Person | 11th May 23, 4:07pm

...Prices have a long way to fall yet. I can't believe how slowly prices have dropped, i thought we'd be back to pre-covid pricing by now.

Quote of the year/month/day so far. Thanks The Person I look forward to some more

What's astonishing is that sales are down to 1992 levels which we experienced when NZ only had 3.5 million people. Something's got to give. The only people selling now are those who have no choice, but I suspect the trickle will turn into a tidal wave if interest rates stay at current levels (heaven forbid they go up). I'm early 30s with a 430k mortgage, supposedly ;affordable', and our monthly interest repayments will go from $980 a month (at 2.33%) to around $2500. I struggle to imagine what it is like for people who bought million dollar homes.

1992 there were total 1322800 dwellings ,2022 there were 1944300,

So comparitively to the total number of dwellings ,the actual percentage of dwellings sold is 50% higher in April 1992,compared to April 2023,... Might be worst APRIL sales month since WW2?

Add on food, power, rates , insurance premiums, travel costs etc etc and it is very hard for some. We are in times many of the younger ones have never experienced before.

Agents seem to be putting a lot of pressure for these sellers to reduce their prices so they can get their commission.Even though agents are supposed to work in the best interests of their vendor, it is one of the risks when using an agent as discussed at https://www.cab.org.nz/article/KB00000928

Some new homes in my area are so cheap that you could never buy the land and build them for the price they are selling them for.

China has the answer:

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.