A significant increase in the number of consented housing projects in Auckland that do not get built over the next couple of years is possible.

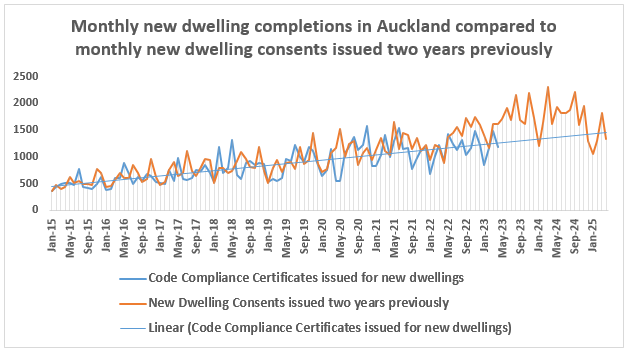

Most residential building projects take about two years to complete once a building consent is issued. Comparing the number of Code Compliance Certificates issued for new dwellings in Auckland with the number of new residential building consents issued two years previously, shows their numbers are very similar, suggesting very few projects are not completed.

That suggests building consents have been a very good indicator of future building activity.

Code Compliance Certificates are issued when a building is completed, making them a reliable indicator of new housing supply.

However the two sets of figures may be about to take divergent paths.

The graph below shows the number of Code Compliance Certificates (CCCs) issued by Auckland Council (the heavy blue line) every month between January 2015 and April 2023, compared to the number new residential dwelling consents issued two years previously.

The thin blue line is the trend for CCCs.

Both data sets are actual quantities, not estimates.

What the graph shows is the number of new homes built in Auckland has risen steadily over the last few years, in line with the steady increase in building consents, and it will need to keep increasing if completions are to keep pace with consents.

If that does happen, then Auckland's residential building boom is yet to peak, and it could increase by several hundred more homes a month to complete all of the projects that have been consented.

While that is a possibility, it seems unlikely because the overall housing market is in the doldrums and residential building consents have started trending down, indicating a weakening in developers' intentions.

The thin blue line in the graph shows the trend in new dwelling completions, projected forward from April 2023 to match up with dwelling consents issued over the previous two years.

What that suggests is even if the number of new homes being completed in Auckland continues to increase at the current rate, there will still be a substantial shortfall between consents and completions.

If the number of new dwelling completions declines or remains static, the shortfall will be even bigger.

Which suggests we are likely to start seeing a significant number of consented building projects in Auckland being put on hold.

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

68 Comments

Plenty of developers are going to loose their shirts. Two years ago they were paying two million for a 1000sqm property in Papatoetoe.

They where paying $4000 a sqm in Glendowie, they will lose their trousers as well....

Lots will say they saw it, but few pocked the 4k per sqm.....

This devalues about 50% of Auckland which is land plus 15-20% improvement, its all now worth ?

How much per sq m?

What about land in hicktown that was sold for under 500 per sqm. BARGAIN

There again, it was sold the previous time for under 150 per sqm. STEAL when no one else was buying.

I sold for $4000 a sq m and bought 157,000 sq m at $20 per s m

Don't get caught up in the number as much as the multiple

We luckily won an auction (being the 'crazy' person in the room) for 25000 squares at 26 each before covid. Since rezoned from rural to Golden ticket resi. Won't support intensive development but still a good 4 bagger. Pity no mortgage to amp up the gains. No intention or need to sell either.

Nice. I only got $1625/sqm when selling but picked up an additional 6Ha for just over $8/sqm.

FYI, the land here got purchased at NZ$9,149 per sq m.

https://www.oneroof.co.nz/news/auction-fight-for-best-view-in-auckland-…

Likely to see apartments be built here?

"I think we can say the market is back. It’s what we were used to prior to last year.” said the agent 🤣🤣

Lets get real here. The average (probably over priced) price of NZ farmland is $3.20 per square meter (not $32 as I first said, almost too large to believe a difference from the numbers being tossed around here ).

https://www.interest.co.nz/rural/resources/farm-sales

Sure there is the cost of development but even allowing for that there is a huge dollop of speculative value in these figures you are tossing around.

If we had a free market in land (as opposed to a corruptly rigged one), the cost of building sections would never get near these astronomical levels, we would have a secure stable market in which developers could safely operate confidently with a lot less risk of going broke and therefore develop land at smaller margins.

Yes, you're 100% correct of course but don't expect too many up ticks showing agreement as many are making good money under the present system as many of the comments are happy to say.

These extra costs are seen as wasteful to many but are the main source of revenue for others.

This inability to buy land without non-value added costs causes a multiplying effect right through the system from holding costs, consenting costs, and time delays, through to building costs, and even the risk value added to your mortgage rate by banks, and as you mention developer margins.

All because of Govt. policy.

Glendowie is a nice place to be fair, I'd move back if it were value for money.

Really nice spot, lived there for quite awhile. Not great for work commuting (assuming you need to work in an office at least several days per week)

Their shirts are going to need to be loose because of all the champagne and caviar?

Fat f7564rs going to have to sell the Ranger.....

Well this came out of the blue.

No doubt someone will be along to tell us they predicted this.

Next will be, shock horror, Mortgagee sales....

The onslaught of mortgagee sales will break like a dam in Ukraine. RUN!!

Condolences and commiserations to those in Ukraine. Only evil bustards would do that

The Chinese blew up there own yellow river dam to stop japs advancing, estimates millions drowned but official numbers 500k..... its been done before.

It's interesting how quickly the rhetoric has gone from "Filthy Ruskies. Blowing up the dam and flooding defenceless Ukraine" to "The failure of the dam...."

This may be overstated. Firstly, the feasibility would be a couple of years ago - and based on house prices precovid - and the land purchase would be precovid. Construction costs have gone up but the house prices are still 10% above pre-covid. and while building costs have risen they only represent half to a third of the cost of delivering the property.

In addition, I am aware of developers continuing with a property development because that is the only way they can get their land purchase price back. The alternative is to sell the consented land at a loss. And that will happen - but it will sell at a price which would allow the development to be continued.

The challenge in turning consents into buildings is not the price changes it is the requirement to get pre-sales which have just evapourated. This is relevant for the larger developments rather than the occassional 4-home infill development.

Yes I have noticed that there is now work starting on a number of building sites that I assumed would never go ahead. For just that reason: the not insignificant land (plus wreck of a house) purchase price is a sunk cost. They either proceed and grin and bear it or sell at a discount to someone who may eventually proceed. Most developers are doing the only thing they know. Developing. What else would they do to earn a crust?

But. They may eventually go bust part way through...

The tax collection stats released by IRD is already painting quite a grim picture of our economy while the construction sector is still busy finishing up existing projects. The real pain begins when new starts take a nosedive and the sector scrambles for work.

Building construction and allied services together make up 9% of NZ's employed workforce, mostly paid above average wages. The ripple effect from job/income losses in these key sectors will be felt in real estate, finance & insurance, food services, retail, building products and so on.

Time to be counter cyclical then ... After all, it does take 2+ years to build, and by then the market will have turned.

Feel a tad sorry to those that started building 2+ years ago when it looked like they'd make a fortune.

2 years to turn.🤣🤣🤣🤣🤣🤣🤣🤣🙄

I do not. Anything that only stacked up at 2% based on the stupid price of leveraged debt was a one way ticket to bankruptcy. Simply a victim of their own greed.

Yeah now is a good time for well capitalised developers to be buying development sites. At least in theory.

National’s MDRS flip flop hasn’t helped. Prior to that developers could have proceeded with a good degree of confidence on rezoning.

The uncertainty and political risk Labour have introduced mean we are heading into the biggest housing shortage on record. You'd be mad throwing big money anywhere near the construction sector

How about the Nats and MDRS? Massive uncertainty caused by that

Yes, you can clearly see consents plummeted after Labour got into power. Oh wait....

https://www.interest.co.nz/charts/real-estate/building-consents-residen…

Wrong, there ARE PLENTY OF HOUSES, just not houses in the rightbplsces for the " jacinda be kind poverty Car sleeping bludgers" to take up.

The new "Ardern underclass" has created the demand but these people don't buy houses they get us to subsidize them via benefit.

As such, there will be new builds for the underclasslings but they will reject them and they will end up like every social housing shit hole in NZ.... ful of gangs and harley fucking Davidson at midnight!

Take Kerikeri new social housing for the losers.! Its already driving people out if town ( see listings on TM up 30%) as the retirement folks get their serenity ruined by the useless northland loosers!

You gave to be wary about buying near empty land tree days .. if the asshat at TPK own it your fecked!

Kainga Ora buy million dollar brand new builds and then turn them into transitional housing for meth addicts and ex-prisoners. Why wouldnt you want to get a drug habit or commit crimes when it comes with free fancy houses now?

ACC will play difficult now re storm water drains on street etc etc as they are at debt ceiling limits

The bigger residential builders have been raising the flag of liquidation since Xmas. Developers are sure to be the same.

Paid way to much for the land, now caught with rates moving up 3x and buyers cannot afford the stupidity of that speculation. Accordingly Devspeulator is caught naked. Banks should just start shooting those that still have something to recover. Lets face it, the other assets used as security are also dropping in value...every day.

Banks are clinging on to hope of a recovery as much as any speculator. They know full well that the market is on an absolute knife edge right now, and that once they start shooting, the whole thing will fall over. I wonder which of them will fire first.

No developer is going bust!

They are alĺ protected by trusts etc.

The workers suffer

The people that financed development suffer. Eg people who brought of the plan, the government who maybe subsidized tthe project for losèr housing

Someone get this specimen a Grammarly subscription

I finished my build during covid period as the cost price of the new build increased about 50% on my type of property since I signed the contract so didn't want to throw that away on land I was never going to sell anyway. Rented out at 18% yield based on cost. That collapses to 10% or less if I paid todays building prices. Never thought of selling, I built to rent before the interest deduction was announced, just had to pace my build to ensure the CCC wasn't issued before the random date where labour have decided a new build is a "new build" for tax purposes. Would have been pissed off had luck not been on my side and the random date labour choose (March 2021 I think?) was after my CCC issued. Big $$$ to have labour throwing spanners in the works 24/7 I'm surprised any developers are left in NZ.

Enjoy the looming housing shortage 2.0 everybody.

"Property prices aren't going to fall any further. They've already fallen a lot" But that's just it - they haven't. They are still way above Covid inspired prices, that even then were at lunacy levels compared to any metric you want to look at, except the eternal hope of capital gains.

There's a lot further to go with the property sector of our economy than most anticipate - no matter who 'wins' in October.

"that even then were at lunacy levels compared to any metric you want to look at, except the eternal hope of capital gains"

Based on historical house price analysis, many believed that:

1) house prices don't go down by much - after all, the worst was during the GFC where they fell 10%

2) house prices double every 10 years

Many high profile property promoters with their vested self serving financial interest repeated this message frequently and many in the general public believed it.

"Enjoy the looming housing shortage 2.0 everybody"

If there is a housing shortage, can you please explain:

1) why are there 6,489 new properties still listed for sale and unsold? (that is about 20% of all properties listed for sale in NZ, and in Auckland that ratio is about 28%)

2) why are there reports that developers / builders have been unable sell their current inventory for sale?

3) why are developers unable to achieve minimum pre-sales levels in order to get financing from their lenders?

If there was a housing shortage, wouldn't these newly built properties be selling like "hot cakes" and there would be little to no inventory on hand to sell?

He's more interested in slagging off Labour for ideological reasons than having a reasoned discussion based on facts.

The reality is that Labour have done well on housing. No comment on other policies but housing is going in the right direction. House prices are crashing like they had to eventually.

I think the housing outcomes are much more to do with RBNZ decisions than anything Labour has done.

ie. Low OCR pumped up housing development and supply, much higher OCR is key factor in house price falls

"I think the housing outcomes are much more to do with RBNZ decisions than anything Labour has done.

ie. Low OCR pumped up housing development and supply, much higher OCR is key factor in house price falls"

Monetary policy is not the tool to address macro-prudential risks (monetary policy tools are tools to address the RBNZ's inflation and employment remit)

The extreme house price risks were preventable back in 2016 when the then Finance Minister did not give the RBNZ the tools they requested to address macroprudential risks.

RBNZ's DTI plans hit by Government changes | interest.co.nz

If a debt to income ratio of 5 was imposed back in 2017, then a significant amount of lending would not have been made (and house prices would have been less likely to have reached their record levels).

Based on RBNZ data, the lending commitments made by banks in 2021, that were on a debt to income of 5 or above were NZ$58.8bn (about 59% of total lending commitments made in 2021). For the period of 2019-2022, total loan commitments on a debt to income of 5 or above totalled NZ$99.8bn (about 32% of the total loan commitments for that period)

https://www.rbnz.govt.nz/.../residential-mortgage-lending...

The higher the debt to income ratio for a borrower, then the higher the probability of default.

Now how many of these borrowers will experience significant cashflow stress, or default?

YAY! By printing lots of money, triggering massive inflation and then completely pile-driving the economy into the ground we have ever so slightly cheaper houses! Woohoo, why didn't I think of that?!?!

How have they done well exactly? I'm curious. Was it the massive rise in prices? Or the meddling in local government decisions that's lead to disjointed communities? Or is it the now largely unaffordability of housing? Or hugely underwhelming delivery of kiwibuild? Again, just curious. What they have "achieved" is not what any political plod party could have.

The inflated margins need to come out of construction materials before people are going to want to build.

A few builders are advertising on Facebook saying they have space… have not seen that in years.

Next year is going to be tough for builders!

Generational greed in this country is literally astounding. Uneducated people call Bitcoin a ponzi scheme yet are happy to make idiotic investments in housing (a basic human right) and based on speculation that some poor first home buyer will always come into the market to keep the NZ housing ponzi going. Well guess what, that's over now until either 1. house prices come rapidly down 2. wages go massively up or 3. interest rates tumble. Which do we think is most likely. At least investment in Bitcoin is not depriving anyone else of a basic human right.

Property investment provides the masses of kiwis that can not buy not due to price but due to them all living pay to pay with most income from benefits.

You assume the whinging fhb's with law degrees on 100k who can't save who are the vocal 5% are all that matter.

Regressive planning laws, perverse tax incentives and construction bottlenecks in materials and labour supply have contributed to a chronic shortage in affordable housing. To make things worse, policymakers jacked up demand for housing further with cheap money and high net migration over the last decade.

There is a place for property investors and the good ones holding long-term rental properties do a better job at it than our public housing agency. A change is needed in policy settings to favour longer term renting more viable over short-term flipping for tax-free gains.

"chronic shortage in affordable housing"

That is the one word that is frequently omitted in the media and commentators. Many people misunderstand the nature of the issue.

There is a huge difference between:

1) shortage of housing and

2) shortage of affordable housing

Investment also denies many people the "privilege" of owning a home. It's not one of the other. Please...

Housing is not a basic human right. Baisc shelter is, but an insulated, heated 4 beddy in a middling suburb is not.

Housing is not a basic human right. You get the right to get an education and then get a job where you work to buy a house. We hare getting close with Labour but we don't yet live in a communist state. Bitcoin has really capitalised on peoples desperation in the modern generation to get rich quick. Nobody wants to work now they want to tap away on a keyboard or make YouTube video's to try and become an influencer. Even a Gen X like myself is just left scratching their heads as society as we knew it slowly goes down the drain. Its all going to end badly and the Boomers will get the blame, even though they will probably all be long gone.

Jezz, the DGM end of the world narrative is strong with this one.

Not really try watching some YouTube videos that state that 70% of the current worlds population will be gone by 2025, that's real DGM for you. I would give us another 20 to 30 years at least.

Our system relies on a small % of the population being unemployed to prevent inflation. Where are they supposed to live? Are we running a society or a game of musical chairs?

"Where are they supposed to live?"

1) If they are owner occupiers and not heavily mortgaged - potentially in their own house

2) If they are owner occupiers and heavily mortgaged:

- sell and downsize their house, relocate to a cheaper area and buy

- live with family, friends

- rent in private market

- social housing

- government subsidized housing with housing supplements in the private market

This is how the demand for social housing increases more than there is available supply of social housing

live with family, friends

I know what couch surfing is like, I did it for over a year and its not the greatest.... it beats living on the street

Saved by Lotto 🍻🍻

" it beats living on the street"

For some people, unfortunately living on the streets, or living in their car is their only option.

Had a family member sleeping in their car when they lost their business and home. Other members of that same family were living in temporary social housing whilst they were on the waiting list for long term social housing.

You speak of Bitcoin as if it has a conscience. It has done nothing. Like any market it is the humans that create the issues. It's like saying houses are at fault for how much they cost.

Waikato and Hamilton are forecast for 43 and 33 pct popn growth over the next 25 years. Auckland and Western BOP 23 and 21 percent.

This is good for developers with demand in overdrive. And good for land bankers as Hamilton has the least amount of land per person of all nz cities.

Constrained between waikato district and waipa, the 3 councils are poor at making land deals. Talk fests with no results. It means the dairy farmers can sleep soundly a bit longer without annoying townies up close

Forecast, hate this bloody word.

I believe in magic more these days then the forecast of forecasting agencies in this country now.

Exactly

The actuals are usually higher

Higher immigration pre covid, and now post covid

Don't give up your day job

Market conditions have changed and many of these projects are no longer commercially and financially viable.

Refer this article and comments:

https://www.interest.co.nz/property/121782/timothy-welch-says-national%…

Dont worry, the Govt has already stepped up to bail out the developers. Any development that cant stand on its own two feet will be underwritten by the Govt, at whatever "market price" the developer puts on it. Once built, if they don't sell, the Govt buys them. What developer isnt going to go ahead with building when you have a Govt guaranteed get out of jail free card?

https://www.nzherald.co.nz/business/govt-to-backstop-more-stalled-housi…

"The Crown underwriting homes makes it easier for the developer to secure finance because they can assure their bank or other financier they have a buyer of last resort.

Developers can apply for assistance via the Build Ready Development Pathway between May 29 and June 16."

$159 million doesn’t cover much development

They will assume in their model that they wont have to underwrite all of it, so $159M can be used to guarantee $1.59B of development. And thats just the first round. There will be more. They'll just redirect Kiwibuild and Kainga Ora funds towards it, and they have a budget of billions.

I thought KO’s budget was under big stress

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.