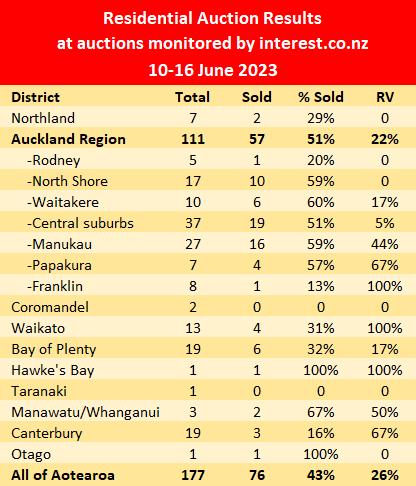

There was a pick up in activity at the latest auctions monitored by interest.co.nz, with more properties on offer and more selling under the hammer.

A total of 177 properties were offered at the auctions around the country monitored by interest.co.nz over the week of 10-16 June, up from 157 the previous week, but below the 185 on offer the week before that.

Of those, 76 sold under the hammer giving an overall sales rate of 43%, compared to 40% the previous week.

Similarly, the number of sales that achieved prices above or equal to their rating valuations increased slightly to 26%, up from 19% the previous week.

The biggest improvement in the sales rate at the latest auctions was in Auckland, which had an overall sales rate of 51%, with only two districts - Rodney and Franklin - where the number of sales under the hammer failed to pass the halfway mark.

Conversely, activity was unusually subdued in Canterbury where the sales rate was just 16%.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices and rating valuations of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

73 Comments

Sellers are now accepting inevitable...

I noticed the media have been driving the narrative hard that the market has bottomed. Even the banks have piled in. It makes you wonder if it's panic, or they are seeing something I'm not? I personally don't think we'll see a sustained rise in prices until investing stacks up and interest rates halve. Happy to hear views ??

Totally agree. I am starting to feel a collapse in equities is the next big test coming globally. For our struggling housing market, it would be bad timing.

edit

Yes a concerted campaign to deceive buyers into saving the collapsing housing market is truly afoot.

The REA vampire sucking industry, are especially working feverously in overtime to suck in the first and most important victim (the REAs pivotal: Usefull Idiot) - the first of the selling chain.......vulnerable FHBs.

Is the FMA asleep at the wheel....again????

The old saying applies here more than ever "when it's this bad, they have to lie"

Beware and be warned.

Even RNZ had a section yesterday with Opus - calling the bottom in 2 months! Smelt so bad of a paid spot and so cringe I had to turn it off.

As The Prophet would always say - What the Vested Interest Brigade says, Believe the Opposite !

Vested Interest Brigade Preaching - Interest Rates Will Not Go Up from Here sermon. ( taken from the book of deception ) chapter 666 verse 13.

I suggest we stay with the Teachings of The Prophet , ( taken from The Scrolls )

10% Interest Rates This Year, Guaranteed !

The Prophet's people are still here, awaiting Their return, tho we are not worthy.

Yip. Like supermarkets aye! They don't sell food anymore they just lease shelves space.

And Mc Donald's Corp don't sell burgers they sell licenses and property

"Panic of 1884 was an economic panic during the Depression of 1882–1885. It was unusual in that it struck at the end rather than the beginning of the recession. The panic created a credit shortage that led to a significant economic decline in the United States, turning a recession into a depression." Wikipedia

The beginning of the end or more likely,, the end of the beginning

Didn't expect this from you HW2.

Oh is that you 2022, hemi

No.

But this is from John Key. He must have his own copy of the Scrolls.

Recessionary spruiking 10 percent floating rate...

"Oh and I chair a bank so I need to justify to all you mortgage holders why you're feeling poor while the bank is in clover."

Suckers 🖕

by Flying high | 17th Jun 23, 10:36am 1686954972 - "Suck on this" 🖕

HW2, at this rate your "Flying High" account will shortly be banned too.

Thanks for the HEADS UP Hemi. You're not entirely mean

I see you removed the insult. Nice save.... 👍

I found it a flippant and unqualified "guess" from the Chairman. He was a casual and cool as a cucumber. A bit like the Chairman of the Board of the TAB giving us an inside tip on which pony to back. Totally weird.

Anyone have any idea why John Key is predicting the spread between Fixed (at 7.xxx) and Floating (at 10.xxx) would widen out to that degree?

I don't recall it being that wide a spread in recent memory - I'd be keen to understand what global (or local) financial environment would cause that?

I noticed that too, and concluded he was thinking on his feet and we heard "floating almost 10" and "mortgages (fixed) with a 7 in front" at different points in the thought stream with subtly different time scales in mind.

But should the Chairman of the ANZ be "thinking on his feet" aloud (LOL)? The RBG has said no more OCR increases for the foreseeable future, but the head of the biggest residential mortgage lender in NZ tells us "you ain't seen nothin yet".

I tend to think JK did make that prediction (i.e., slip-up) based on inside knowledge. It would be actually worse if he was intentionally talking up his book - but I don't think that the case.

In 2016, then ANZ Chief David Hisco's conscience got the better of him and he publicly stated that he thought NZ property was overcooked while wages hard hardly moved and the coming adjustment could get messy.

https://www.nzherald.co.nz/business/david-hisco-housing-and-nz-dollar-o…

Might just be an ANZ thing to do....LOL!

Back in Spain my brother worked for one of the biggest banks in Europe (La Caixa). He was a young graduate of economics and got a bit of shock. The banks (and business around them) are the biggest mafia outside Calabria (Italy). Back then, fifteen years ago, they would get a memo with the product that they had to sell (normally poor performing products) and all the terminology that they had to use. I can see that the mafiosi are still using the same methods. Have you wonder why they are suddenly all pushing the same narrative at the same time with no evidence all in sync (banks, media, real states...) using the same words? (bottoming out being the preferred)

Yes simply:

"Tell a lie big enough and repeatedly and it will be believed"

Its happening now in plain view.

They all know the market confidence is shattered and sunk without trace........SO THEY JUST HAVE TO LIE!

They are doing it in open collusion and on an industrial scale!!!!

Q

WHERE WILL THY LIEING BANKS BEEEEE WHEN THOUSANDS ARE FORCED INTO MORTGAGEE SALE ??

A.

THATS YOUR PROBLEM!!

Not just banks bro .

Government

REINZ

Booking. Con

Most technology manufacturers like Sony apple ...

They all spin a line. But what's worse is the price controls they force on us.

No bargains.

Take samsung... I've want a S23ultra 1tb phone. Search the world and the price is the same everywhere. From the smallest high cost retailer to the largest bulk buyer retailer... the same fixed price dictated by the supplier

The whole world is dictated too by the manufacturer. The retailer cannot discount like the old day's.

Then there is the " same product 2 retailer variants" scam...

Makita make two identical skill saws ( one actually) with different part numbers.,one for burnings one for mitre 10. They do this so bunningd does have to give you the 15% " we will beat any competition pricing" deal.

We are being screwed and the retailers have had thier point of difference MOJO removed...

In australia they a have the Oppo find 5 pro for $799 ( nz $1400) but while its not locked you can only use it in Aussie,.WTF?... the same spec as NZ but tweaked and half price for the Aussies.

Com com should be over this stuff

If they talked the same way about shares I'm sure the FMA would be all over their asses

Paraphrasing what I heard yesterday on RNZ primetime: "the market is very likely to bottom out in the next few months. I'm hearing there's more activity in the auction rooms"

If they used the same language with shares: "the NZX had been taking a tumbling, but hodl for 2 more months, as I've seen more people logging into Sharesies"

It's interesting how liberally everyone in the media can speculate to drive sentiment about an asset that's currently 10x the value of a yearly household income, without any repercussions or at least disclaimers

prices will double if interest rates halve, precisely what Orr is trying to avoid.

Correct. If you look at the data it's the cheap houses In the cheaper areas selling and a few rich oldies spending up before they die 🤣

Are apartments sales for the immigrants in this set of data.?

While they still have their marbles

The hubby of a family friend wanted to retire but the wife made him stay at the grindstone. Until he almost croaked. Then they went on a cruise with him as a paraplegic. 🥳

My impression is prices have probable bottomed in Wellington and Auckland. But, further downside likely in the rest of the country (Queenstown and affluent nearby areas excepted).

Reasoning is wages are rising and we do have high inflation. So nominal wages are quite strong. People will be getting 10 years of wage rises, in 4 years. This suits those with high incomes, as they actually spend a lower percentage of their income. If you gross 140K per annum and net 100K per annum, but only spend 60K per annum (may be one of a two income household). And you get a 5% pay rise matching inflation, you earn an extra 7K, $4666 after tax. But your expenses of 60K went up 5%, ie $3000, so you have an extra $1666 to service a mortgage, save or invest. So high inflation, matched by wage rises, benefits those who earn enough to save and invest.

The other reason is the reality we will likely have a National/ ACT government. Improving the after tax economics of owning rental properties.

The one caveat with this outlook, is marked unemployment in the context of a deep recession.

Auck and Wgtn still have outrageously overpriced house prices of 7 to 10x DTI!!! We are just off (and downslope skiing) where they maxed out at 12x DTI. Never before have we seen such high, bubble multiples!

3 or 4x DTI are considered affordable. So we have a long way down to run, in this early, initial stage, of this massive housing price reset.

REMEMBER: the average NZ household income is 117k!!

CHECK the Irish correlation and DTI from the bubble to the bottom. This is the closest correlative example of what is occurring live in NZ right now.

We will never see a DTI of 3-4 in desirable areas to live (though possibly a debt to household income ratio for property owners of 3-4 is doable). The DTI of 3-4 was a metric of a bygone time, when Dad worked and Mum was at home with the kids. This was also a metric when many were happy with an 80sqm Keith Hay home. We now have large double glazed, ensuited homes with a scullery. And people are prepared to work longer hours with more incomes per household to service the mortgage on these modern homes.

The other thing to keep in mind the average income per household in an age of wealth disparity is less relevant. You need to look at the median household income of property owners.

I purchased at a DTI of 4x. I'm not yet fossilised either!

With normalised Ddddebt costs of 6 to 10%, so it shall be again.

Sales in Auckland are running 38% below pcm average of 2008-22. In last 5 months sales are well below 2008.

As sales in Sept 20 to May 21 were 65% above the pcm average ref above, the market will remain overbought for minimum of 2 years, to be balanced by reversion to the mean of 3300 sales pcm. That two years will expire roughly 2 years after price peak which was about Dec 21.

But until rates fall back to at least 4%, little life will be seen

Courtesy of Granny H; "A Chinese businessman’s decision to buy Sir John Key’s former mansion for $23.5 million has proved to be the worst house purchase made in New Zealand in recent years, because the businessman suffered a $7.2m loss when he resold the former prime minister’s glamorous home in November, having never even lived in it.

For all those similarly minded Ghost House owners the words now out. I doubt these houses were bought with the mindset "its good fortune if I lose millions"

https://www.nzherald.co.nz/nz/sir-john-keys-former-parnell-home-resale-…

The old lucky 7 mil loss... very expensive wash cycle

Wouldn't it be ironic if he lost with an 8 in front........lucky for some.....

A 30% loss. I'm sure that "Chinese businessman" has made big money in the past so it's probably not such a big deal. You win some, you lose some.

To have bought, but never lived in the house. Yes, some would say a 30% loss is still a 100% gain when money laundering.

Is it still a 100% gain if the money he lost belonged to someone else?

Wondering if that's entirely on the housing market? I mean, can we discount the businessman overpaid in the first place? I mean, overpaid for the house, but evened out overall? Is JK a saint? Could this have been just a settlement for who-knows-what other favour?

The 7.2 mill loss is tax deductible right ?

Was he a nz citizen? I think these laundry Asians need to be cleaned out.

But the washing in NZ went sooooo well and they could even make lots of money doing it too, it dried the notes sooooo well in the bright NZ sunshine......until 2021.

Our property market collapse has stopped the Chinese money washing machine game.

- Better to sell in NZ now and take the washing load to Aussie market? YEP.

The thing that made me laugh out loud about this article was this quote:

“One homeowner’s pain is another’s gain and shows that timing is everything in the market — although it’s not always easy to spot when you’re in the moment,” OneRoof editor Owen Vaughan said about the huge loss on Key’s former home

....this is a reversal from one roofs usual 'it's time in the market not timing the market' mantra!

I'm still not seeing much in the way of bargains out there. Very few mortgagee sales. If you bought speculatively two or three years ago and now have to sell you are likely looking at a 25% loss. If you bought a nice home that appeals to boomers you'll probably get what you paid for it.

"I'm still not seeing much in the way of bargains out there" My sentiments exactly, its still early days.

Is it early days, the peak was November 2021...

...be patient Nifty1

i thought that villa at 1.3 mil vs last sale 2 mil was ok , could it get cheaper yes... but villas have limited numbers and perhaps not so much stress... showed me that demand had a firm upper bid limit

There is COVID froth being burnt off however there is also development property mania froth that is going to be burned off as well.

We are totally setting ourselves up for the next boom, but the bust has to run its course.

I reckon there will be a meaningful lift in prices from late 2024 IT Guy, but it will be far from a boom.

"I'm still not seeing much in the way of bargains out there" My sentiments exactly, its still early days."

As The Prophet would always say - There is NO such thing as a bargain in a falling market !

Where you looking bro.

I'm seeing 200k drops in the last 3 weeks. Five so far.

ONE TREE POINT IS IN FREE FALL AS THEY ARE OVER STOCKED, IN A OVER RATED DIRT BOWL, FULL OF EMPTY SECTIONS AND POOR SHOPPING OPTIONS.

The amout of people who brought " new" 2 years ago and are selling shows the area is not a good place due to all the continual earth works and Commercial traffic volumes ruining a nice seaside area. The oldies are leaving?

NEW BUILDS DROPPING FROM1,000,000 TO 800K AS WE SPEAK AND STILL STRUGGLING

100s of sections being drip fed, no buyers, builder crying in their Ford rangers, and building Co's laying off the Ute laden reps.

New builds drop from over 1milion bucks to high 8s

ONE TREE HILL 100b?

The calapse of HP and capitalism is just around the other side

"Drip fed" so named after those buying them

Papakura. 4 sold and 67 percent of those were at/ above CV.

So how many sold at/above CV??? Well 2.68 homes of course. Amazing

Waikato. All sales were at/above CV. Its winter and buyers are lining up for it in the Waikato,,,

Houston we have a problem

Waikato is the centre of the galaxy and we all the scientists told us what that is. The big big black hole. It sucks everything not even let light out💡😂😂😂😂

Waikato is the centre of the galaxy and we all the scientists told us what that is. The big big black hole. It sucks everything not even let light out💡😂😂😂😂

Waikato is the centre of the galaxy and all the scientists told us what that is "The big big black hole" . It sucks everything not even let light out💡😂😂😂😂

Waikato- Yes, it appears 9 vendors were foolishly expecting RV and never got it 😂↘️

Late arrivals to the party. Houston, Waikato certainly has a problem.

Probably not enough data to really read too much into it, but it is interesting that more affordable locations in Auckland are seeing much higher proportions of sales going at or above RV.

More buyers, FHBs?

Immigrants buying apartments?

Developers being rentals for immigrants

Developers buying land to sub divide and build 5x 3 story shit boxes

What year is the CV?

Pre covid or post 2020 makes a huĝĝĝĝggĝgge difference

Haven't seen a sales rate like that in Auckland for a long time...

"Green shoots" "Rates have peaked" "Market has bottomed" "Bbbbeee Quick"

- These REAs well worn narratives, pervade the media, sucking is the novice gumby buyer, like octopus tentacles........

"Remember, when it's this bad, THEY HAVE to LIE"

The market confidence is kaput, gone.

Where's the lie, the sales rate is clearly higher than it's been?

NZGecko, Which spruiker will be wheeled out today on the won woof radio shoe ↗️↗️🖕

I wait with baited breath expecting the OneRougfhie "paid for lies" to be trotted out, ad nauseum......

I listen, but know its primetime spruikerland!!

The hosts are good enough people, likable guys, otherwise very smart, but for this one hour unfortunately, they appear to be completely beholden, they are "bought and paid for" by the OneRoughie slimeballs. It’s a known quantity.

If they say it enough....... the LIES can become reality and believable, it will be, it will be, it will be, it will be .........

"Green shoots" "Rates have peaked" "Market has bottomed" "Bbbbeee Quick"

Warning to the uninitiated...... the last line in the above: are Utter LIES, BS and very dangerous to take at face value!

OneRoofie....

Sadly that is close to the truth with the sector tricking people to inject themselves with endless debt enslavement.

The next colluded spruikerfest is booked! 4pm Newstalk ZB.

OneWolf Packleader: the Church of Ashley - is booked in with his "million-and-one" reasons the property market has turned and "Bbbbee quick - buy now"

It will be a spruikerhoot for sure.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.