The volume of unsold housing stock continues to weigh heavily on the housing market.

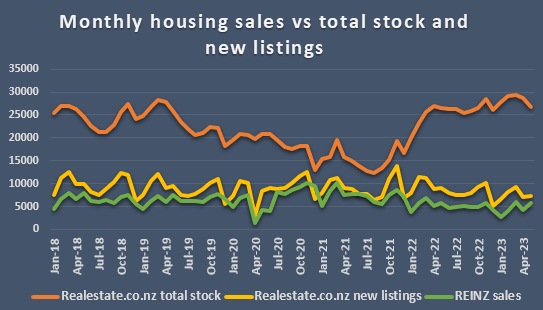

Property website Realestate.co.nz had a total 26,685 residential properties available for sale at the end of May 2023, while the Real Estate Institute of NZ reported just 5752 residential sales in the same month.

That means there were an average of about 4.6 properties available for sale for every property that sold last month.

The graph below shows the relationship between the end of month stock levels and monthly new listings on the Realestate.co.nz website, and compares them with the REINZ's monthly residential sales from January 2018 to May 2023.

It shows the gap between total stock and monthly sales steadily declined between May 2019 and mid-2021, hitting a record low in December 2020.

It then started to increase sharply from August 2021 and has remained at an elevated level since the beginning of last year.

Essentially this suggests the housing market currently has a bad case of indigestion and is struggling to convert properties that are on the market into sales.

That may not bring much joy to vendors, but for potential buyers it means there remains plenty of choice. For both groups there could be some hard bargaining involved to close a deal.

The comment stream in this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

95 Comments

And just like that, some finally found out houses are a horrendously illiquid store of value.

This is correct. And because property is relatively illiquid, the costs involved to free up capital from property can become onerous.

Good point. Especially if its leveraged, and the cost of that leverage is approaching a re sign at 3x the original cost. Are we finally at the point that risk of leverage is being exposed...?

Ha I wonder whether this belief in "storing value" is one of our ideological delusions limiting us from making significant changes in our collective behaviours. Ultimately it's a fear driven belief. It's like we no longer have any understanding of inherent, intrinsic or extrinsic values.

On top of that is the belief that homes are "assets" and "investments" rather than a basic cost of living. Yet we somehow believe this price increase is good but price increases in other necessities is bad.

I’ve been scrolling through this website for months now and cannot find any convincing reasons or plausible indications that house prices will begin to rise again in NZ anytime soon.

Anyone?

HW2 used to have lots of implausible indicators. TTP has gone on a well deserved holiday.

It must have been EXHAUSTING to be a spruiker over the last 18 months.

Buy this year guys...it's gonna go up

You're banging your head against a Wall there Harvey

Up to 10% Interest Rates This Year, Guaranteed !

Commercial and second or third tier lenders already there. Test rates must not be far off. I wouldn't count on a fixed rate north of 10% but stranger things have happened.

TTP has gone on a well deserved holiday. [starrider]

High time Starrider got real - instead of riding stars.

TTP's been coming here regularly for longer than most people can remember - and he's far from exhausted.

Let's hope Starrider's dinner goes down better than her BS.

TTP

According to one commenter named 'TTP' its called resilience.

Yep let's rejoice

Tony Alexander has suggested The Top is in for mortgage rates, and 3-5% rise in property prices is on the cards for this year, and 10% for each of the following years. (NB: personally, I reckon he's about right with the numbers, but it's the direction he's got wrong - again)

What T.A. never seems to factor in is that inflation has taken money from people's pockets that they'd otherwise have used to pay a mortgage. And worse? The fear of more inflation means they're keeping even more back.

T.A is actually correct when you ponder on the Teachings of The Prophet.

What the Vested Interest Brigade says - Believe The Opposite !

If T.A says Mortgage Rates have Toped - Then 10% Interest Rates This Year, Guaranteed, is what it will be.

T.A says prices will go North - Property Prices will go South.

It's just that Easy !

If Tony Alexander is one side of extreme, you are definitely the other side of extreme. even house prices dropped to 10k, you would still wish it drops even further.

Not saying house price will not drop further but to say there'll be a limit that house price can drop just so much.

Prices are a direct reflection of what people can borrow. We still haven't reached the equilibrium (prices haven't dropped as much as borrowing capacity). For now I don't see any possible improvement on the rates side, only wages increase will compensate a bit. At the current pace it will probably take an other 2 years for things to stabilise. Unless there's an other pandemic...

Some think a change of government will rebalance the market (with interest deductibility reintroduced), I'm skeptical about it as I doubt it will be enough to make the investment worth it.

The only unknown is the cashed-up buyer from offshore via Singapore, Australia permanent residence or for new builds. There, demand is potentially unlimited and based on a lower threshold, in terms of rational value. e.g compared to Shanghai it is still cheap and even if I lose a bit keeps my money away from the CCP.

The way life works, they'll flee to NZ to escape the ccp, then be caught in a web of greens and broke socialists.

The proposed wealth tax has killed off those cashed up buyers from wanting to move here.

Restoring interest deductibility wont change anything, as its high interest rates that are killing landlords not lack of interest deductions (currently landlords are unaffected by the changes as 100% deductibility of 3% mortgage interest is exactly the same as 50% deductibility of 6% mortgage interest). About the only benefit is that it might stave off some of the flood of listings that will hit the market next year when interest deductibility goes to 25% and interest rates go to 7%. However, the market will by then be into the second year of Brightline roll offs (2018 and 2019 buyers) so that tidal wave of sellers will be pretty much unstoppable.

In Australia over 50% of new listings in the major capitals are landlords selling up. And Australia has lower mortgage rates, full interest deductibility, higher rents, and negative gearing AND rising house prices - and they're still selling! Its only the promise of waiting out the Brightline and pocketing tax free capital gains that is currently keeping landlords from cashing in. That will only last for a year or so longer as after that 2020 buyers will be in negative equity and the Brightline Tax will be irrelevant.

https://www.afr.com/property/residential/property-investors-sell-up-as-…

"Sydney city and the inner south posted the largest share of ex-rental listings in the country, accounting for 57 per cent of all new listings during May, a large increase from the 38 per cent decade average. Across Parramatta, 47.6 per cent of all new listings were investor-owned. That figure was 43 per cent in the eastern suburbs and the inner west. In inner Melbourne, nearly half of all new listings were landlord-owned. In inner Perth, 47.5 per cent were ex-rentals."

I disagree - as interest rates rise, the investor is caught by the increased cost AND having to pay tax on what can't be claimed as a deduction. The result is it makes a bog-standard residential investment uneconomic. The result is writ large in the data - investors aren't buying and the consequential reduction in demand is having a depressing effect on property values.

As I said, the increased tax only kicks in next year because currently the doubling of the interest bill is making up for the loss of being able to only deduct half of it. ie. the $ amount claimed as a deduction is still the same as in 2020/21. Most investors have a cashflow problem because of high interest rates, not because they are paying more tax.

currently landlords are unaffected by the changes as 100% deductibility of 3% mortgage interest is exactly the same as 50% deductibility of 6% mortgage interest

That's for existing investments. But any new investments get hit with 0% deductibility so I disagree that restoring interest deductibility wont change anything. Where I do agree though is that high interest rates are the main factor.

But those investors already knew that when they bought the property, so they knew that the amount of tax they pay won't change over time regardless of what happens to interest rates. For them restoring interest deductibility is nice, but its not something they ever factored in to their financial return at the time of purchase. Unlike existing investors who bought houses based on the financial return of being able to deduct interest, and then had the rug pulled out from under them.

The point is that some of those investors will hold off making new investments because with 0% deductibility the numbers don't stack up.

So in that respect restoring interest deductibility will change things because some of those previously unviable investments would again make sense.

"The point is that some of those investors will hold off making new investments because with 0% deductibility the numbers don't stack up."

Investors in the long term rental market are given tax incentives in the following areas:

1) new builds - the country needs more new builds

2) existing houses rented out for social housing - there are long waiting lists for social housing, so there is a shortage of social housing

These are the areas of housing needs for the country and hence where tax deductibility of interest remains.

If interest deductibility is reinstated for existing houses purchased after March 2021, will this stop investors buying new builds and hence builders / developers stop building new builds? And the underlying housing shortage will continue?

I agree, there's a correlation between house prices and access to credit, but that's not the only factor. Immigration and cost to build (i.e. increase supply) also have some bearing. Of course cost of credit is also an issue, residential investors have pulled back not because of credit access barriers but because the cost of credit is much higher due to the effect of interest deductibility limitations.

I meant to add - the move to income to debt ratios is another tool that restricts access to credit. This could affect the FHB segment the hardest.

Agree DTi will have an inpact. I believe that will mainly be targeting investors with different threshold for home buyer/occupiers vs investors.

Generally, a DTI would favour FHB. However, when you read the RBNZ discussion document, you see they are doing all they can to put in as many loopholes as possible for other groups - particularly developers and renovate-to-flip'rs. Even with that though, the example DTI was high enough to be meaningless above ~3.5% interest, and control of the ratios was given to the banks.

Hopefully you don't take all your research from just this website...

Of course not. The sheep’s entrails too have been indicating poor omens ahead.

Pull the year slider all the way back as far as it goes....

Median price - REINZ | interest.co.nz

But I still wouldn't put money on it happening any time soon

Pull the year slider all the way back as far as it goes....

Is that a euphemism?!

Tony Alexander thinks prices will rise 3-5% this year. You can find his article on OneWoof a day or two ago.

Whether he has convincing reasoning for that is a matter of opinion. I would say ‘Hell, no!’

In my opinion, before prices bottom out, let alone start rising, one of the three following things need to occur:

1. Prices fall further (perhaps another 5%); or

2. Retail interest rates fall, by at least 1%; or

3. A combination of 1 and 2 eg. Prices fall a further 3-5% and interest rates fall at least 0.5-0.75%

All 3 scenarios are at least 6-9 months from playing out, all things being equal.

As SND says, prices are a direct reflection of what people can borrow. Unless prices come down further, interest rates start dropping, or a combination, realisable demand will remain pretty dead and prices won’t start moving higher.

Edit- of course it depends what measure you use to measure price movements. I have said before that it is plausible for the median value to increase while the HPI continues to decline. So if using median value it’s quite possible The Comb could be right.

You don't mention the effects of the MDRS or the NPS-UD.

Nobody ever does! And they are - quite frankly - the major reason house prices will stagnate in real terms for a very long time.

I tend to agree, however there’s every chance the MDRS will disappear if it’s a National / Act government.

Anyone is entitled to an opinion and they have as much chance of being right as the so called "Experts". If we see no more OCR hikes then we are near the bottom of the cycle, then National/ACT get elected in October and then we have summer. I can see house prices then remaining flat for all of 2024. The war in Ukraine ends and we get back on track and house prices begin to rise again in line with inflation in 2025. Each part requires the previous part and any number of things can throw a spanner in the works.

Replacement cost is horrendous. Land owners generally don't need to sell and construction cost will not drop fast enough.

Had that chat yesterday with an agent. No real acknowledgement that the cost of capital and construction continue to rise, and that this will have a negative pull on the value of land. Especially ially in a declining market. The glow of several years if simply order taking at 2% rates and panic fueled prices has agents still enjoying a europhic stake of how great they are...

There is alot of over priced rubbish but little in the way of quality. The market will start to seperate as the old truths of quality builds in good locations maintain value. whilst others continue to fall away.

I sold up too early, 3 years ago and am cashed up but i see two opposing tensions:

1. overhang of stock. increasing mortgage rates. possibility of capitulation panic selling in some sub-markets. loooooong period of flat prices.

2. houses are a good investment in times of inflation which i believe is with is for some years at least. houses can generate an income and there is limited supply.

so, maybe buy quality houses in the coming dip??

On 2, how do you figure this?

During periods of high inflation, central banks tend to hike interest rates which reduces the amount people can borrow - the price of the underlying asset tends to take a beating, not ideal if you want to cash out.

On the cash flows, there's no inherent reason why rents must rise in line with inflation - if people aren't experiencing enough wage growth to keep up with other aspects of the cost of living, that leaves less money left over to pay the rent, inhibiting landlords' ability to ask for more - rents have been going backwards in real terms over this last inflationary period.

"2. houses are a good investment in times of inflation which i believe is with is for some years at least. houses can generate an income and there is limited supply. "

"houses are a good investment in times of inflation" - that is a extremely pervasive belief by many people.

Here is the reality that people may have overlooked.

Since Nov 2021 peak for house prices:

A) Nationwide

1) REINZ house price index for NZ has fallen 18.0%

2) With inflation at 7.0% per annum, the REINZ house price index for NZ has fallen 25.0% (i.e has fallen in real inflation adjusted terms and not kept up with inflation)

B) Auckland

1) REINZ house price index for Auckland has fallen 23.2%

2) With inflation at 7.0% per annum, the REINZ house price index for NZ has fallen 29.6% (i.e has fallen in real inflation adjusted terms and not kept up with inflation)

C) Wellington

1) REINZ house price index for Wellington has fallen 26.7%

2) With inflation at 7.0% per annum, the REINZ house price index for NZ has fallen 32.9% (i.e has fallen in real inflation adjusted terms and not kept up with inflation)

Depends on when you buy and how long you hold, but generally (but not always) over a long term houses do better than inflation. An international comparison of house price movement.

The last 40 years isn't a good example of long term though.

The cost of building new houses is still rising and will continue to do so.

Govt is bringing in a completely new raft of carbon calculations. So the developer or builder will have extra cost to calculate these. Councils will need a new dept to check them - so guess who is going to have to pay for them?

The 1st of possible 3 tranches of increased energy efficiency regs are now in. But the others will follow.

The replacement for RMA? 3/5/10 waters?

I agree that people may not be able to afford them.

The only place to cut costs is government. In the UK, new homes are zero GST. That would bring a nice 15% off the cost.

A new build should cost more than an existing home. What the past few years has encouraged is spending large on existing property. Renting a 3br home has recently cost the same regardless of whether the house is 5 years old or 105 years old.

This may start to shift, anecdotally in this comment section there was a comment from a REA about renters in Auckland choosing newly built townhouses over old rentals as the additional cost of living in a newly built home is marginal.

Unfortunately algorithms used by Homes and co cannot accurately depict the value of a home between these, and "market rent" does not account for quality of home. Currently the only determining factors are the urgency to sell against the depth of the buyers pockets.

We already have a tax incentive on new builds for investment purposes.

Renting a 3br home will cost the same regardless of whether the house is 5 years old or 105 years old.

Not always true. As the old crapbox 1930's uninsulated home with floors so low there can't be underfloor insulation in, may go for a bit cheaper than the neighbouring 10yr old home for rent, FHB's are waiting and watching as they know it isn't worth paying top dollar for an old dunger when it is only ____ amount more for a relatively modern house with good insulation. The days of a fixer upper are gone as it just can't be justified to buy one in todays market unless you are leveraging another house and banking on capital gains and rental profit long term

As preferences shift and older houses don't sell, the market will find it's equilibrium.

Edited previous comment. Otherwise, yea that's the same observation I'm making/hearing about. Those I know who are renting are moving to nicer places or new build townhouses and they're happy with price vs the cold house they're moving from.

Investor friend I know is looking to buy a doer upper, needs 10% yield to "make it work" at a 50% discount on current prices.

I wouldn't judge a book by its cover.

We have a fully renovated 109 year old rental property in Wellington that is far warmer, drier and healthier than the 2016 build we rented in a supposedly desirable part of Havelock North. That HN house was cold all year round with endless condensation issues, underwhelming insulation, and terrible finishing, while our Wellington property has none of these problems because it was our first home and we made sure all the work was completed with care and attention.

I'd never buy a property that was built during the recent boom years.

Old houses were properly oriented to the sun on a section, whereas new houses simply get oriented to the street or driveway. My old 1950's house was super warm and dry and did not require heating during daytime in winter, because it got all day sun starting in the kitchen, and moving through the living areas, and ending up in the main bedroom. I feel sorry for people living in townhouses with only 2 windows at each end of the house, one of which will never receive sunlight.

Increasing the cost of construction materials further is going to decimate the industry. It is uneconomic to build now.

wait till the coming March to June. Spring may be late, but will come.

Mortgagee sales - and bank "suggested" sales - should start mounting up over winter as the slow sales rate combined with mortgage rate roll-overs and recessionary effects start to really bite.

Winter has arrived for the housing market. Autumn wasn't much fun (and it lasted for 12 months!) but the winter will be long and harsh. (The RBNZ has much to answer for!)

Google "nz immigration v house prices" as an image search.

Then check latest immigration numbers. 60k to year end March nearer 80k to year end may. Will be over 100k for calender year 2023.

Correlation is not causation. In fact, the housing market saw its biggest price gain in the nation's history when borders were shut tight during Covid. Extending your logic out to interest rates, a higher for longer OCR will keep house prices low.

The net figure is an assumption based on people immigrating with intention to stay, and people emigrating with intention to leave. We do not know the latter, hence they use a 12/16 month rule to determine when somebody has truly left the country. That means we do not know emigrants for 12-16months after they have gone. Notice that the major emigrant reaction to lockdowns occurs a year after the first one? Whereas the immigrant reaction was immediate? And how the charted 100k leaving now far outweighs the 50k arriving a year ago?

We are net losing ~20k people per month since Feb. Which is seasonal, and usually ticks up with the ski season. So we won't know until next year.

Important to look at actual arrivals and departures to determine how many people in the country at present.

Not sure where those numbers come from, when we've had a net loss since march. -23k from 1/Jan to 31/May.

All it will take is vendors to meet the market, and that total stock will start to move. It will be interesting to see if we will hit 35k or 40k this spring.

Obviously, no shortage of housing in NZ. Just a shortage of realistic vendors.

I wonder how many vendors refuse to meet the bid due to their equity position?

Or the Vendors' lenders not letting them.

Someone I worked with previously bought an overpriced unkept house in central Hutt Valley in late 2021 to get onto the first rung of the property ladder. The plan was to build up equity (pay down loan and cream ever-increasing prices) to move into a better school zone by 2024.

The plan change now includes staying put in the cold, damp house and coughing up 10k+ a year to send his kid to a private school.

No absence of greed.

It appears to be a cycle, as one vendor will over-offer on another house thinking they will get a good price on their own, then it drags on and on until they either accept the lower selling point and stump up more mortgage for the new house, or they pull the pin and try another offer on another place. Meanwhile the place they offered on is making another offer elsewhere which is too much as they think they've locked in a good price on their own house.

The number of mortgagee sales is slowly climbing. And I'm hearing many are in tough discussions with their banks.

Forced sellers are very realistic vendors - the have no choice. The impasse is about to be broken.

Remember this is with near record low unemployment at 3.4%.

What happens when the unemployment rate rises?

Key question: How many house owners will be unable to hold on?

I wonder how many Mum and Dad Landlords have actually worked out what happens when those tasty Tax advantages come to an end soon ?

Add that to the list of reasons to sell.

"Mortgagee" search on Trade me October 2022 result returned 26.

Today 44.

From memory it was steady in the 20 - 30 range through March and maybe April and bumped up to mid 30s in May. I'd need to do a search on my interest.co.nz comment history to verify that.

Its called overhang, and its the reason why there will be no rapid recovery.....

Interesting that listings are almost never below sales. i.e. there must be a constant flow of non-sale de-listings

I know plenty

I am sorry spruikers this is not the bottom, even the light at the end of the tunnel has been turned off due to the cost of living crisis

When you contrast to interest.co.nz articles with the ones in the Herald (Tony Alexander) and Oneroof, it does make you wonder if they're trying to talk the market back up?!

All you have to ask yourself is, "who's paying the bills?"

Unfortunately some here who still subscribe to the likes of the Granny Herald.

Can someone let me know what's funny about saying 'One Woof' instead of 'One Roof'? Does this make anti spruikers feel better about themselves for being One Roofs most regular readers?

A reflection of the view that One Roof is barking mad if it thinks people can't see through its attempts to attract attention?

The first sentence of this article about sums it up. Any other market and this would be illegal. Yet, here we are. Actively telling people false information in order to promote business activity and speculation.

Is anybody able to provide logical statistical evidence that proves right now is the bottom of the housing market? Not that it "might go up" or "could go either way" or "we hope it goes up". That the HPI, median and average tomorrow will be higher than today and will continue in a positive trend for the next 6-12 months minimum.

It's not supposed to be funny. It's just a way of ensuring we're not giving them any free advertising.

I don't see anyone referring to One Roof more than in the interest.co.nz comments section

It really should be changed to One Spoof. Because it should not be taken seriously !

Looking at the current stock of houses on the market, it's looks like vendors are trying to get rid of their crap at exaggerated prices.

No wonder there is indigestion.

House price’s were push up with super low interest rates now rates and inflation are so much higher the million dollar 3 bedder is well out of reach for average wage earners, for many this is hard to take but house prices will continue to fall until more of the population can afford to buy. Smart speculators would have sold 20 months ago but there are a few who missed the memo trying to talk up a dead market everyone is now aware and can smell the BS.

Agreed.

Housing market just needs some Metamucil and Adrian Orr has a big jar in his desk draw.. or is it Kool Aid?

A.Orr got a 400k payrise and a 5year contract extension. He'll be racking his regular morning publicly-funded line of blow and washing it down with a shot of 2021 FHB's tears which he relishes so.

Or he can line himself up for the new RBA Governor to replace Philip Lowe!

Time series doesn't go back far enough unfortunately, to a time when the housing market wasn't nuts.

I have a slight issue with that graph: whilst there were consistently higher 'new' listings than sold, the number of houses available dropped? That would tend to indicate the houses were'nt 'new'listings - or were many simply removed from the market? This could be explained if we're talking Auckland 2017-2019 I suppose - where prices stagnated until interest rates were dropped further?

The trend was your friend, until the bend.

Tailwinds will overpower the headwinds facing the housing market and push prices up, ANZ's economists say

https://www.interest.co.nz/property/122721/tailwinds-will-overpower-hea…

So we were told that interest rates had to go up so that inflation would get between RBNZ's target rate of between 2-3%. They were nowhere near achieving this yet said no more rate rises. It was at a staggering 6.7%. Oh but don't worry because it has come down from 7.2%.

Furthermore, petrol prices have been subsidised by 10% for over a year and that is coming off now. That's about $20 for each full tank. A lot more inflation to come. So for all the pain they are trying to inflict for over 18 months we are still in the same position. Madness if anyone thinks houses will stabilise.

Our contents insurance went up 40%, yes 40% (we rent). All because their risk analyst has finally become aware of climate change and the cost to them. Every district council are sending out huge raises in rates.

We are waiting at least 12 months to buy.

Things can't get much worse in this country, the place is a shambles. A pretty good time to buy, when you finally do buy you'll be looking in the rear vision mirror and everyone will be out there doing the same thing.

A new government will hopefully straighten the place out, inject some optimism and get the show on the road again. NZD taking a hit means all imported building materials will be more expensive shortly.

I've just purchased some land on the outskirts of Auckland - got a huge discount.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.