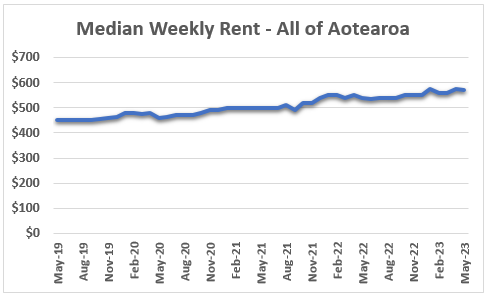

The national median rent declined by $5 a week in May but remained up by $30 a week (+5.6%) compared to May last year, according to the latest residential bond data.

Tenancy Services received 11,688 rental bonds from throughout New Zealand in May this year, up by 5.0% compared to May last year.

The median rent was $570 a week, compared to $575 April and $540 in May last year.

The dip in rents in May was not unusual, because rents usually peak over the busy summer months and then ease slightly in winter.

Most regions showed a similar trend with a drop of about $5 a week in May.

The dip was bigger in Auckland where the median rent declined by $20, from $640 in April to $620 in May.

However in spite of slight easing over May, rents in most places remain close to their record highs set over the previous few months.

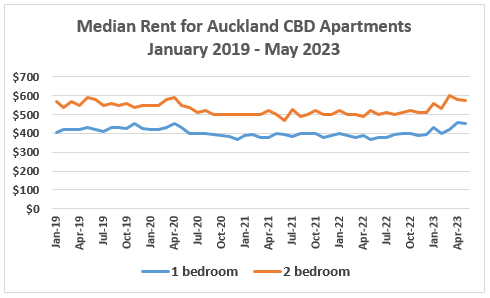

Rents for apartments in Auckland's CBD, which is the country's largest apartment market, also showed a slight decline in May. The median rent for one bedroom apartments declined from $460 in April to $450 in May, while the median rent for two bedroom apartments fell from $580 to $575 over the same period.

Auckland CBD apartment rents have recovered strongly since the easing of pandemic restrictions, which has seen the return of international students to the city.

Even after the slight drop in rents in May, the median rent for one bedroom apartments in Auckland's CBD was up by $85 a week (+23.3%) compared to May last year. The median rent for two bedroom apartments rose by $55 a week (+10.6%) over the same period.

The charts below show the median rent trends for all of Aotearoa, all property types, and for Auckland CBD apartments over the last four years.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

92 Comments

Government should roll out residential rent controls as a matter of urgency.

Regulating rent hikes makes complete sense in the current tough economic climate.

TTP

And right on track, as the first news of rents falling is announced, the spruikers are out calling for rent controls

A friend told her landlord how we all thought she has it good. Nek minute the mail arrived with a bigger rent increase than she expected.

Silly sod

I emailed my insurer and asked them to limit their increases to be inline with inflation and eagerly look forward to their reply.

Let me take a guess at their response.. I'll summarize: "LOL, no!"

What response?

If their risk remained static they might consider it.

Same as if the landlord's cost remained static they may consider it.

by tothepoint | 18th Jul 23, 9:16pm

The DGM consistently forget or ignore the glaring fact that property investment is NOT just about capital appreciation....... It's also about rental return - the "liquid" part of ROI. In fact, for many property investors the rental return is much more important than capital appreciation.

Oooooooops! When adjusting for inflation, things are looking a little like double trouble especially now that Spruikers appear to be lobbying for rent controls!

Good typing retired-poppy

Its shite grammar day today - lol!

Rent controls are for socialists. What's next, price controls like in the mess Piggy Muldoon made of the NZ economy?

But National and their supporters keep saying the Labour's property policies are causing rents to rocket. You see it daily in various media comment sections. What gives?

Complete BS as is the nonsense Luxon has been trying to sell that reinstating interest deductibility on investment properties is purely for the benefit of renters.

On a different note, I saw Simplicity announce more BTR developments a few weeks ago. Sad to think the number of dwellings they add to rental stock in 2-3 years will be gobbled up by current net migration levels in less than 3 weeks.

34 rentals available in Rotorua today. Pop 70,000+

That's fewer than there are employees of newly created social housing providers in the town.

"Complete BS as is the nonsense Luxon has been trying to sell that reinstating interest deductibility on investment properties is purely for the benefit of renters."

Strange thing to say. I mean obviously both landlords and renters would benefit here. Reinstate interest deductibility = more rental supply = lower rents.

The interest deductibility thing was never about improving things for renters though, it was always about improving things for first home buyers by encouraging landlords to sell existing properties. Of course the bit left unsaid is that this reduces the housing stock of existing rental properties...

I think it was more to discourage landlords from speculating on more property (outbidding FHBs) and encourage them to build new.

The equation seems to be more like: Reinstate interest deductibility = more speculation = higher house prices = higher rents.

I doubt these statistics mean much. They don't allow for number of bedrooms, so if we were coming out of a building boom where a lot of small units were completing and being rented then the numbers would skew lower. I don't know if that's the case, but suspect it is. I own a property management business and rents are definitely not flat or falling anywhere, except perhaps in Wellington, and that is slowly trending back towards a supply equilibrium.

Its Fri-yay for another reason now

Hello Greg - doesn't Stats NZ report Auckland rents for the year to June up 7.3% with a rising trend?

TradeMe Data shows Auckland up 10%

Benjamin Disraeli had something to say about stats.

Tenancy Services data is based on bonds received, so only captures new tenancies.

TradeMe data is based on rental prices advertised, and therefore expectations.

Neither capture increased rents charged to existing tenants.

Well my rents have all been rocketing up nicely, so I'll trust my own stats. Cheers!

Who needs stats departments when our ol' mate Cote can tell us the state of the nation.

Tenancy Services data includes social housing rentals. TradeMe data is only private sector rentals. So rents are rising or falling depending on whether the Govt is paying for your rent or you are.

Social rentals are at a set 25 percent of incomes, usually a benefit

It stands to reason that rents on these houses increased 7 percent when the benefits did. The buzz-words are stock and flow rentals

Good points that the Tenancy Services rent data may be skewed by whatever is happening with social rentals

I wouldnt assume that increased rent was automatically passed on by the Be Kind Govt. Especially since rents can only be increased once a year, most of them wouldnt even be up for a rent review.

Well said

This is what Tenancy Services says about the data: "The data shown is for non-government owned properties that we have information on. It should not be used for any purpose other than as an indication of the non-government rental market based on bonds lodged."

Non government?

CHPs community housing providers are non government

Correct. Kainga Ora housing is not represented in the Tenancy Services data because the Govt no longer requires KO tenants to put up a bond. No bond, no bond lodgement with TS.

3.x% according to this link. I haven't done any detailed digging into it tho.

https://www.stats.govt.nz/information-releases/rental-price-indexes-jun…

We regard the rent data collected with bonds to be the most accurate measure of market movements because it is so comprehensive and also because it reflects the actual rents agreed between landlords and tenants rather than advertised or asking rents. It is also a leading indicator because new rents are generally settled at what the market will bear, so landlords will use these figures as a market indicator when the rents for existing tenancies come up for review. As well as reporting monthly movements in rents, interest.co.nz also produces a more comprehensive quarterly report. The Q1 report is available here.

It is distorted by social housing rentals. The Govt pays a CHP a subsidy, but the tenant pays below market rent which is reflected in the actual bond lodgement for the lease. Nowhere is the actual rent paid by the CHP to the owner of the property reflected because these leases are outside the RTA. And increasing numbers of owners are choosing to rent to CHPs because they get interest deductibility restored.

That distortion existed last time the data was collated too, so it's presence is irrelevant (bar change in makeup - feel free to provide some data to support your assertions that the rental market has shifted so heavily and so quickly to CHP that it's skewing year-on-year data).

The reduced ability of landlords to claim interest deductibility combined with the increased interest costs this year, has resulted in a shift to renting to social housing providers. Its about the only way that owners can afford to retain their properties. It is openly being touted on property forums as a means of improving cashflow for owners who are struggling with the increased mortgage payments. Prior to the loss of interest deductibility and in a low interest rate environment most landlords wouldnt have dreamt of leasing to social housing. Times have changed.

Has it? I don't see a massive "shift" in community group housing.

- Community Group Housing Managed Stock

- March 2023 = 1516 out of 70k KO managed.

- December 2022 = 1508

- September 2022 = 1509

- June 2022 = 1498 out of 69k KO managed

- https://kaingaora.govt.nz/assets/Publications/Managed-stock/Managed-Sto…

- https://kaingaora.govt.nz/assets/Publications/Archive-Managed-and-Vacan…

- https://kaingaora.govt.nz/assets/Publications/Archive-Managed-and-Vacan…

- https://kaingaora.govt.nz/assets/Publications/Archive-Managed-and-Vacan…

That's just the houses KO owns that are managed by CHPs.

Most of the CHP housing is owned by landlords, leased by various charitable trusts. Eg Monte Cecilia trust in Auckland has 627 on it books as of its last annual report, up from 594 in the previous report. No doubt that number will have increased when it latest annual report is released soon.

Rents will never fall in this country ....as even if NZ went into a economic depression, the government would "top them up" with the accommodation supplement, from "printed money" pushing NZ further into debt and exacerbating the current account deficit.

As long as the landlords are all OK .....screw the rest.

About time to drop the accommodation supplement and let renters pay what that can "afford" - and if they can't afford it, look somewhere else.

The landlords talk about doing "so much good for the community with housing folks", well if you are that generous, instead of taking taxpayer dollars to prop up your rents for that cold, damp sh*tbox" in South Auckland, play the game and let the "true" free market decide, with what your property is worth for rent vs. current incomes - whether earned or from welfare.

It's totally time to look at housing as a national asset to create homes and security for families, nurture new businesses and that good ol' backyard kiwi innovation, so we can create careers and businesses for people ....not just more uber drivers and short order cooks !

Bring in a "one house policy" per family (with no capital gains tax) so you are not penalised for improving your home ....while any second and subsequent property will be run just like any other business, with no assistance at all from the government ie taxpayer !

If the economy can afford to dish out money to landlords, they can use this money for infrastructure, roading, community facilities etc etc etc

This would bring down property prices down to where the "true" market would put them and opening up more houses for more FHB's to buy, while in the meantime rents would be at a market rate for that "cold, damp sh*tbox" ! While the tenant would be paying for "what you get" not what the landlord "WANTS", while the landlord themselves would never live in, in its current state !

Time for a real change .....wonder which political party would have the guts to implement the above ???

It certainly won't be National or Labour, that's for sure ! ....too weak and afraid !

Both parties only do what the swing voters or donors want. they already have the votes from their base so they will keep all the relavent policies so they wont lose those (which is very unlikely anyway) and so all their new policies are designed to please swing voters or donors (or their personal needs).

Until the population realise that and stops habitually voting for the same party - it will continue this way.

Banks, political parties, supermarkets, insurers, streaming service providers, accountants.. etc all work that way.. they arent interested in their core customer bases other than not changing too much that they might leave.. lol

Completely agree Crazy Horse - as I've said on this site for 5+ years that if we were to remove accommodation supplements, it would be the entitled landlords who would whinge more than the struggling renters - end of the day they are the ones holding the bad debt against the property market, not the renter.

The power trip the rent seeking class have been on in recent times needs to end (and supported by successive governments, under the guise of socialism/caring for the poor - but while actually increasing inequality and giving to the rich).

Sounds like you'd fit in well in North Korea, Crazy Horse.

I suspect this is being pushed down the high number of 2 bedroom townhouses coming online. Is it possible to break down by # of bedrooms?

If you scroll up there is a graph already for akl CBD broken down by bedroom

Yep definitely likely to be a factor

Perspective surrounding the cost of property habitation is interesting - whether that's paying rent or paying down a loan. In this article for the US a mortgage loan officer is staggered that someone sees paying $7,000 a month in loan repayment as acceptable. But we see that as 'normal' here, and yet the example couple has a gross income of $270k. I doubt the same would apply here. And we still think there isn't a significant rebalancing coming? Of course there is.

In December 2021, when the 30-year fixed mortgage rate still averaged 3.1%, a borrower could get $700,000 mortgage that required monthly payments of principal and interest of just $2,989. Fast-forward to Wednesday, and a $700,000 mortgage taken out at the current average mortgage rate of 6.90% would equal a $4,610 per month payment, which is $583,000 more over 30 years than that mortgage issued at a 3.1% rate. When adding on insurance and taxes, that monthly payment could easily top $6,000. Not to mention, that calculation doesn't account for the fact that U.S. home prices in June 2022 were 12% above December 2021 levels and 39% above June 2020 levels.... these borrowers (have) already concluded that these high mortgage payments will be "short-lived," and they'll simply refinance to a lower payment once mortgage rates come down.

https://finance.yahoo.com/news/loan-officer-m-seeing-middle-000641114.h…

@bw .... Welcome to the "craziness" of the NZ residential property market and what it has become ...... the chickens are well and truly coming home to roost .... yeehaa says the Crazy Horse, as he gallops over the dusty hill and away from the madness ....

Good, we really want to see a big pull back in non-tradable inflation of which rent is an element.

All the posts about how mean and money-grubbing landlords are. Well if being a landlord is that profitable why aren't all the whingers here buying a rental or two?

Rentals are under regulated... wait a minute.

Commercial rentals still allow deductibility

@wingman .....that's the whole point, as right now being a landlord doesn't stack up financially (no more "go on forever" capital gains) and the "sheeple" have finally woken up to, just how few people it actually benefits financially throughout the country........maybe just you, Luxon and just a few other multiple property owners.

Welcome to the "real world" mate, get off your XXX and do something productive for yourself and the country ....and get your hand out of the taxpayers pocket !

NZ Gecko?

Heartening to see you all missed me.......

The BW and Horse (that is far from crazy) are saying all that needs to be said.

Love that rents are declining for the poor sops that need to endure the crappy rent seeker boxes on offer.

Talk of *rents to the moon", by the Govt sponsored landlords.......hahaha!!!! falling flat into the mud of the thousands of newbuilds being completed all around me.

Equally as good, is the plummeting prices of entry level, first homes for families to buy at ever cheaper prices.

Another 4 years of good housing prices dropping will be warmly greeted by New Zealanders.

Love the bathing, in the ample tears, of the ever more squirming Lords of the lands

Being a landlord "doesn't stack up"? You sell property when interest rates are down and buy when interest rates are up. There....now you don't have to go and buy a book on property investment. I've just spent well over a million buying land, getting ready to build my next property.

You guys are like goldbugs, sitting on their tiny 'stacks' waiting for their ship to come in, but it never happens.

When will the AK City Council let you build in that floodzone?

You may need to wait for the next Tectonic/Geologic uplift epoch.......Thats one ballsy bet there! - Winging it, I see :)

Gooooood Luuuck.

We don't think they're mean and money-grubbing, just that they're an unproductive waste of capital, and most provide zero value to society as they clamber over all and sundry to outbid FHB on existing entry level homes using 100% loans while expecting the taxpayer to underwrite.

Why are you worried about my 'unproductive, waste of capital'? I've made a fortune out of renters. And I'm a damned good landlord too, I give my tenants the best treatment.

I suppose you want the government to build all the houses so we become another North Korea? Isn't it amazing, all these posters criticising landlords making a 'killing', but not doing it themselves. Because you're not up to the job - taking on mountains of debt, repairing trashed houses, and dealing with some problematic people, just not you, is it?

I suppose you guys are just too moral to be multi-millionaires, I mean who wants to drive a good car, have no debt, do a bit of travel, live a nice life and have a million or two in the bank?

Not you guys obviously. Hasn't been all plain sailing, that's for sure, but it's been worth the risk.

I've made a fortune out of renters. And I'm a damned good landlord too, I give my tenants the best treatment.

Sssshhhh! Nzdan is a member of Greens and keeping notes for Marama and Julie Anne

Far from it.

It's because unproductive capital has steadily eroded our standard of living to the point where houses are barely affordable for normal people. Compared to our peers, we have relentlessly moved backwards for decades.

Other countries encourage starting and investing in businesses, improving productivity. Here people think that buying a house that already exists and renting it out is a gift to the economy.

The pollies are to blame especially Clarke.

Sir Geoffrey Palmer with Clarke in cahoots brought in the RMA. David Parker's new resource management acts x 3 will be a major stuff up

At least Key would have got rid of it if he weren't un-dunne by Peter Dunne

Yes, politicians have been cowardly and short sighted, and many still are.

I'm not having a go at individual investors here, I can't really blame them for following incentives although they may lack a little imagination. But, as a whole rental property investment is way out of whack in NZ and it has made the country worse.

So what if a few investors made dosh out of rentals. Do you yourself invest in retirement villages

Its up to the pollies to set conditions.

And the latest builds are warm and cosy, in the outer suburbs and overpriced

Yes, I have shares in some of the retirement village owners. The difference is, they are constantly building new homes. I have no problem with property investors who are going out and building new homes for people to live in - that's useful. Buying up existing property and renting it out creates nothing.

Agreed. That's the crux of my comment. Allowing people to leverage 100% of the purchase price to outbid FHB on entry level properties is what I mean by unproductive waste of capital and damaging to society. Certainly not something we want to direct tax incentives too either.

Then you get the likes of Wingman coming in panties in a knot because he built a house 30 years ago, and has since rented it out which is not a waste of productive capital in my view. I think he just looks for ways to humble brag to be quite honest.

I built a house 30 years ago? I've built 4, I've owned about 15 properties over the years. It's just so easy, you go too the bank ask them to lend you at least a million dollars and off you go and get rich. Be my guest.

Do you know you cannot build unless council gives consent.

Bottle neck

Hang on… if you’re so busy driving your nice car, travelling, and living a nice life then why are you on here trolling less-fortunate people?

Someone’s feeling a bit guilty and trying to justify their position (to themselves and others) I think…

I can't speak for Wingman but the anti landlord, all landlords are bad, crap, wears a bit thin after a couple of years. Good on Wingman for posting what is obviously going to be shot down in flames by the majority of sad individuals on here.

Yes the truth does start to wear a bit thin if heard enough times.

But Wingman is right in many ways, we all should have taken advantage and snatched up “easy” capital when we had the chance. Unfortunately some didn’t have the equity or income to back it.

Be careful which bridges you burn Wingman, the gravy train has broken down at the station and you might need to hitch a ride (good luck building your next house for $140k…).

I'm not trolling anyone. I started with nothing, my father gave me $50 when I left the country for a few years. When I got back I saw an opportunity in the property market.

I'm retired, I do whatever I like, and that includes travelling, but I'm also starting to build another house because this is the ideal time to get a terrific deal on bare land. And the bare land is where there's going to be a lot happening.

Don't socialists just hate free enterprise? Don't ya just love the people that say they could have been rich, but just didn't want to be.......

wingman, there is a reason why few people get wealthy and the majority doesn't, that reason can clearly be seen in the posts on Interest.

Agree, “most” people have a conscience.

Wrong......most people don't have what it takes to borrow huge sums of money and take the risk.

You've Made a fortune rorting an underclass for every cent and the NZ taxpayer.

International Hero of the year award, comming your way!

Really glad you still sleep like baby every night.

I sleep extremely well every night.

I haven't rorted an underclass at all. In fact a tenant who's leaving shortly has rented from me for 5 years. I've never increased his rent because he's a great tenant and a handyman who's done a bit of paid work for me. I'm going to sell that house in a while, it cost me $140k to build and it's now worth $1.4m. That's how you make money, you could have done it yourself, but you're just too much of a bleeding heart socialist who wants da gubbermint to do everything for everyone.

Do you know there's 40,000 empty houses in Auckland? Fact! Owned by people who can't be bothered renting, and the socialists here want to make it harder for landlords. Good luck with that one.

There'll be one page full of mortgagee sales in today's Herald. Go and buy one, you might make some money. I did. I bought a house so disgustingly filthy and loaded with fleas, animals wouldn't live like that. I eventually managed to evict the tenants, renovate, clean up the rubbish on the section and rent it out. I cut some land off the back and built another house. Anyone can do it, you just need the gonads to borrow the money and have a go. Be my guest.

The locals in that street told me how glad they were to see me buy the property and clean it up.

Kudos. You actually built a house and rented it out, that's exactly what we expect of investors.

My comments are directed at people who leverage up 100% of the purchase price, outbid a FHB and then claim they're doing the work of Jesus and need all the tax breaks real businesses enjoy. They're not doing anything wrong, it's perfectly legal, but they don't deserve any respect for doing it.

I had the option of buying/keeping my first home as a rental when I traded up in 2021 using the huge capital gains I realized, but I don't agree with that. We sold to a FHB who now have a home of their own.

It's not all about you wingman.

No, I don't want the Government to build all the houses. I want the Government to even the playing field between FHB and Landlords battling for entry level properties. Personally, I would have rather seen mortgage interest deductibility extended to owner occupiers rather than removed from Landlords, but removing it from existing properties to encourage landlords to invest in new builds is okay by me.

Have you ever once in your life thought about younger generations?

You've convinced yourself that you've done something amazing by borrowing debt and buying shelter, a basic human right and holding it over people that don't have the same access to credit as you.

Please, explain to me how you doing this has helped society and hasn't contributed to the inequality?

If people like me don't provide accommodation who's going to do it?

I don't think I've done anything particularly amazing at all, just takes a bit of determination and nous. Why haven't you done it and got rich?

I've renovated and built a lot of houses, think how much money that's put into the economy and how many people I've employed over the decades.

Just imagine how much socialists must hate lotto winners who don't do anything for their money at all.

Nzdan, that's a very broad generalisation, I don't know any landlords that fit that criteria. Oh, and you missed out "boomers".

So you think Landlords were not buying up entry level homes (low entry price, upside potential on yield)? RBNZ C31 contains lending data that show up until 2017 mortgages for investors were outnumbering FHB 3:1 and the average value of those mortgages even when factoring in any LVR requirements was on par, sometimes a smidge higher than the average FHB loan.

Wingman; "if being a landlord is that profitable why aren't all the whingers here buying a rental or two?"

Whingeing is a lot easier!

struth, we've driven around and seen the median rental.. everyone enjoying immigration policies? keeps a lid on wages at least if you're hiring eh

The median rent was $570 a week, compared to $575 April and $540 in May last year.

Which equates to a $100,000 household income required for the median rent to be considered affordable (if the affordability benchmark is at the high end, ie. 30% of gross income on spent rent);

https://calculate.co.nz/rent-affordability-calculator.php

Roughly, 2.5 FTEs working on the minimum wage per household.

By the time you guys have crunched all the numbers and come to the conclusion property's a lousy bet, the next property boom will have come and gone.

The cost of building new houses is becoming astronomically expensive thanks to the gubbermint and their 'expert' advisors. Just recently the healthy home compliance has added another layer of costs to new builds. From 2021 to 2022, the cost of a new build increased 12%.

I thought the Building Code already covered the minimum standards for healthy homes. Unless there was a recent amendment to the relevant clauses?

Is market still tanking ? will wait another year or so do we think ? cash buyer but 3 bdrm apartments pretty hard to find - any central city ideas or just ride out for a few more years do we think with rates trending up for forseeable - watching with interest but blood bath for developers it seems

By the time you read in the newspapers that the real estate market's recovering, it'll be too late, everyone and his dog will be out there bidding up prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.