The pending election did nothing to dampen activity in the auction rooms over the last week, in fact it seemed to have had the opposite effect, with the auction rooms having their busiest week so far this year.

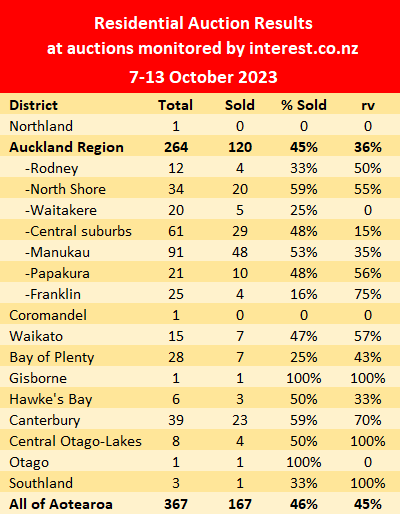

There were 367 properties offered at the residential property auctions monitored by interest.co.nz over the week of 7-13 October, the highest number in any week so far this year.

It was the first time in 2023 more than 300 properties have been offered at the auctions we monitor. The previous busiest week was at the height of the summer season in the last week of March when 294 properties were offered.

The latest auctions also had the highest number of sales achieved so far this year, with 167 properties selling under the hammer, giving an overall sales rate of 46%.

Although the sales rate was not a record, it compared very well with last summer's auctions when sales rates were typically around a third.

The higher level of activity over the last week was apparent across the country, with all of the areas where auctions are most common - Auckland, Waikato, Bay of Plenty and Canterbury, all showing a strong lift in activity.

The table below shows the regional results from the auctions monitored by interest.co.nz around the country.

Details of the individual properties offered at all of the auctions we monitor, including the selling prices and rating valuations of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

73 Comments

Could the buyers be returning in anticipation of a change in government?

Could just be spring, and that the dire catastrophizing that's been going on for what seems like years now hasn't been felt by many in reality.

I think it's simplistic expectations National will save the day and the myopic belief current cost of borrowing will only get cosier from here.

Higher for Longer. 2024 will be a year of confronting a stark reality that sustainable prosperity isn't owned by countries who's residents sell overpriced houses to each other.

The situation is still evolving.

When the article doesn't fit with what you would like to happen, just talk about the future. Then no one can tell you that you're wrong !

Either that or make some sort of soap box statement about people being greedy or yourself just wanting the best for your country

You don't hate kittens now, do you Yvil?

Adult conversations are hard ☹️

I hate kittens. But that’s probably a different conversation.

People seem to be getting used to higher for longer, hence sales are holding in there.

There hasn't been the oft promoted bubble pop. Apparently, there's a lot less people needing to ditch a house at any cost under this current environment than promised. Likely partially because since the GFC, the lending criteria changed, so there's far less marginal mortgages than previously, with most mortgages ahead of schedule than behind.

If things actually do come to a head, it's going to be far less about whether housing is sustainable, and more so about the global economy being incapable of navigating the rather substantial amount of large change agents of the past 4 years. Housing will be affected, and no doubt some will herald that as a prophecy ringing true (has to at some point, right?), but housing will only be collateral damage.

What's that other Buffet quote, "it's better to be precisely right than approximately wrong"?

I agree with Warren Buffett that it's better to be approximately right than precisely wrong, that would lead to a general judgement that debt and NZ residential property prices are still relatively high so that future returns are still likely to be relatively low. The prices have declined since 2021 so extreme pessimism is unwarranted.

Predicting a crash or a boom in anything is reckless, irresponsible and likely wrong/hard to guess.

We've not yet seen the RBNZ's low interest GFC-like "teaser" rates flow through in refinancing of residential debt so it's too soon to say how things will play out.

Yes they already know the government is changing. This is part 3 of a 4 point plan, part 4 is house price increases of 3-4% next year.

The markets been heating up for ages with lots of activity. It doesn’t fit the narrative for some on here, and probably defies logic, but that is what has been happening

"Higher for longer"...

😂

"Busiest week" and yet less than 200 sales..

Give a child a lolly and they'll be happy..

...out of the 367 Interest monitored. NZ wide there are many more sales.

Just watching the local market, for the last 2-3 months the number of listings has been static, i.e. the house sales have matched the new listings. In the last week there's been a massive upswing in listings, likely to make the most of spring and hope for a Xmas close.

Tricky to say what the sell through will be like, but then again I've never seen a rental market with such a lack of supply and high rental inflation. Successful housing policy at work.

42 rentals available in Rotorua. That's almost a 10% upswing on the last time I checked, when it was 39. They've all been hoovered up by social housing providers and AirBNB.

As usual, Yvil is competent, quick-witted and insightful.......

Compare his comments with those of the lazy, greedy DGM.

Well done Yvil. Always a pleasure to read your offerings.

TTP

It takes a fool to recognize another.. well done

Give Dgm a headline and he loses his marbles.

Frustrated with life mr. Ice? Just check if you're marbles are still intact..

It’s you lot who are frustrated because the writing is on the walls for all your BS wishful thinking. Depressing little man.

Take it easy my friend, your fragile heart will pop .. and then someone else will enjoy your riches, while you lay alone in the dark

Proving my point about depressing. See a councillor if you need mate and cheer up a wee bit. National will be in power tonight.

You seem nervous, National will ultimately govern, so what?

This is much less a political issue than it is a monetary issue.

You seem to really dislike economics and love the tales of yesteryear. The whole “ladder” mantra.

I’ve seen a noticeable increase in your level of spruiker panic…

Might be worth asking your tenants if you have any, to buy you out 👍

I’m not sure where you pull comments like that out from. My tenants are lovely, I treat them with respect and provide well above average places for them to live in and call home. They’ve been thankful that I’ve increased rent instead of selling too. I’m just looking forward to having my interest deductibility back.

It’s exactly that talk from people like you who always think prices are “expensive” and never buy. Can’t help you.

"They’ve been thankful that I’ve increased rent instead of selling too."

Thanks for the laughs. Iceman, you sure as hell hit the jackpot with that one!

I cringe at the thought of how you view yourself.

Do your tenants also massage his majesty’s feet during home invasion, whoops, errr…. inspection.

I suppose I’ve never really my asked, what actual businesses have you started Iceman?

Stating facts mate, that is exactly what they said because firstly I wasn’t even charging them market rent. like I said - not all landlords are AHoles or are trying to make a quick buck. I actually have a great relationship with my tenants. The truth is - you’re insecure or have tall poppy which probably is not healthy for you.

That is exactly what they said, it might surprise you that not all landlords are AHoles. Enjoy the laughs, you have much to learn.

Based on your comments, you don't seem a nice guy, so no surprises if you're one of those Aholes

Relationship with tenants is a good two way street. Now you on the other hand, I can’t deal with stupid.

Easy boy.. name calling now . How low will you stoop... you definitely suffer from hypertension..

I call a spade a spade mate. On that note, won’t be wasting another second today on you.

If you have any shame and brains left, restrain from commenting when it's not appropriate..

Just because you're a spruiker doesn't make you superior to others

How do you explain to an idiotic that they’re idiotic? I know what I’ve achieved in life and proud of it. You sound like a sour little man on the other hand. So you resort to being a daily keyboard warrior pretending to be knowledgeable but really you know nothing about the real world from the comfort of your arm chair. Perhaps less commenting and more experience at something else will educate you. Never ever think I’m superior to others, I’m always learning. The very face you perceive me as being superior speaks of your incredible insecurity and littleness.

Lol.. you're such a spineless loser... can't stick to your words..

You clearly are portraying a person you are not.. so name yourself Hotman.. or even better.. Madman

It's time to "be kind" to Iceman - he's anxious. Last night's victory is looking more bitter than sweet with each news headline!

Some of National's policies/promises are simply not affordable without additional borrowing. If Winnie has a say, implementation cannot be taken for granted.

Pro-property policies/promises might well end up being deferred or worse - down the gurgler.

Good to know you're still breathing..

We are happy to buy. But bank will only lend us so much. Four years ago, the amount the bank would lend will buy us a house worth over $1 million now. Drum roll, these same houses were selling at $600 to $800k @ 3%. So we are unable to buy same house selling at $1 mill @ 7% give or take. So not only are house prices higher, interest rates are higher. It's a double whammy.

Also more people are rolling off 3% interest and inflation is still high.

If banks don't lend and prices are out of reach. Other then selling a current house and then buying, not sure how people are buying houses.

We have noticed people have already moved, and buying a house, so need house sold. We need more of these.

If the bank doesn't lend, you don't have many options.

Interesting that a lot of rental owners still don't understand the interest deductibility rules on people who they might sell to one day. I was chatting with someone yesterday at kiddies tennis, they provide a small rental to an older friend. They want to sell and move closer to family and were shocked when I said that their friend would have to pay double market rent for the new owner to break even, if an investor were to buy it and keep their friend on as a tenant.

Double. That's a gap that will not close, so the logical endgame is the state houses everybody who rents. Social housing is the next meth testing cottage industry to boom.

And you can deduct the interest if you're renting to the government.

Amazing plan.

Next up, UBI.

Why would people buy now when the housing market could easily fall another 20% over next 18 month.

They might have sold now and want a place to live in?

Maybe people would buy now because the market could rise by 20%, over the next 18 months...

C'mon now Harvey - more than likely not :)

DTI, is a Property Speculators worst nightmare.....

Be a good argument, if bags of apples were 10 grand.

LOL, how many edits do such simple posts need.....

If you can't stand the message - attack the poster....yawn.

It's not that I can't stand it, it's that the message is jumping all over the place like a Jack Russel Terrier.

Poor poppy, you used to be so sure of yourself.

I rest my case.

Haha, the old "Fein interest by sounding bored, yet continue to read and reply" act.

DTIs off the table by lunch time Monday.

I have seen people wait and there is a commentator above who tells you of trying to buy 4 years ago and the story is similar. I read yesterday I think it was reserve bank now forecasting 7.7% rise in 2024. If you want or need a home long term then being out of the market is your biggest risk

That's still nuts yes you can buy if you have money. But banks are stress testing at higher then 8% and are currently loaning on 5 times income. You cannot get around this. Sure if you have invested before and know 2nd tier lenders and can handle the risk, knock your socks off. But that is not joe average, and that doesn't help now or future generations.

You need to have money to buy the house. Just saying buy, doesn't make it so.

why would people buy now when the housing market could easily fall another 20% over next 18 month.

Simple, selling up and relocating to somewhere else for lifestyle, job, or any other reason, then buying in the new location where housing is cheaper than where they sold up.

From my area only 4 sold out of 25 with 75% above RV, last week nothing sold. Think our area is being stubborn on price.

Listings are low as well. We can see some prices being reduced now, but not much. Quite hard though, when you see people have bought at peak prices on 3% now want $200k more, plus people who have bought 2016 for example @ 3% want $400k more, really old and ugly house. They want $900k. Not much you can do when banks not allowing you to borrow anyway. Which is cool, as the debt levels are to scary, when you have a family and cost of living is so high.

Our combined income is OK, not sure how people on less money are surviving. Luxon said he spends $60 on groceries so all is easy for everyone.

A house where I'm trying to buy was last sold October 2020 for $800k, now has an asking price of $1.26m

I put an offer in on a house this week that sold for $430k 2015. It went from Auction to deadline to price by negotiation to asking $1.2m

Cost to build has skyrocketed. Why would anyone sell their house for X when the replacement value is Y. A decent house in a decent location (Thats now been taken by the existing house) is always comparable to the new build price of the identical house you have to build elsewhere.

I get cost to build, but you can't buy if you don't have the money or bank won't lend. I had same issue with my business. I had to take a hit on some of my products, as the products were not selling at price I wanted, even though I differentiated and added more value. Customers were just not buying, so I had to cut price, so I didn't lose to much.

That kind of makes no sense, if people can't afford to buy, how do they buy something. Banks are stress testing at 8 to 9%. You can sell for whatever you want, but if people don't have money, you will end up with nothing or a mortgagee sale. Some common sense needs to apply.

I learned a few years ago now that common sense doesn't apply to the housing market. A house is not really something you can take a pass on and most people want one. There are plenty of "Products" in life you can take a pass on or just buy a cheaper product. Homes invoke emotions and rationality quickly goes out the door, just visit an auction when the market is running hot, its madness.

My Daughter tells me Gucci bags are emotional and my son says apple watches are as well. Houses are products just like anything else. Yes I like some more then others, but a lot of our houses in the boon docks of NZ are 100 years old and tired yet bringing in premium prices.

But for arguments sake pretend your right. Thats all true when house prices were within affordable levels at 5 to 7 times income which was doable and banks were willing to lend at 3% and stress tested at 5%. Banks lend based on income and deposit. Unless I am missing something that other people know.

Anyway the Bank says approximately 8% or more stress test and 5 times income, thats as emotional as I can get.

Ouch, wonder where they are getting loans. Be interesting to see their numbers.

Rising house prices should be looked upon like rising petrol prices and all the rest.

They should be mourned in heartfelt sorrow.

CM and look at petrol prices now, last time it was this high the media were going to every man and his dog who had some story how their life was being impacted yet this time around not a whimper so fuel dropped and then slowly climbs and is expected to climb higher. Reminds you of anything else mmmmmm. What's dropped the last 18mths from an extremely high price and is now bumping along

Nothing to get excited about in these results, for either spruikers or DGMs.

The market has steadied a bit, strengthening slightly. But only slightly.

I think the jury is still out. The retrial is coming in 2024.

I've just sold my late mother's house at auction in West Harbour, which was required to be sold under the terms of her Will.

It sold for $1.296m. About exactly what we thought it would get. It requires some renovation, but is quite liveable. There were 8 registered bidders, quite a crowd turned up and we were extremely pleased with the result.

I kind of get that price in Auckland. It's not out of whack for me. But towns miles away from Auckland over 1hour drive with no traffic, which is never now, with little in terms of work and smaller market want Auckland prices. It's quite risky. Least 1.2 in Auckland has a little more logic, lower risk.

Not to mention no one earns that kind of money where we live, except farmers. So banks will not lend if you can't afford repayments.

Friends 17yr old daughter just left school started job in dairy factory starting at 70k a year average house price in local Town 370 000 and dairy factory freezing works,are screaming out for workers. Beats sitting in traffic 1 to 1 and half morning and night and paying exorbitant rents etc

Not actually sure what your getting at with that rents etc. Thats great for her. And a good price for where ever she is, but its not relevant for over a million people who live near Auckland and all the other cities around NZ. Not everyone can pick up and leave and there are only so many jobs in those towns where shes from. Not to mention, if all 2 million moved to those towns, house prices would rise.

Thats if I'm getting your gyst and your saying move. Just tell my wife who comes from overseas and has made a life for herself here with friends work etc, to get my kids out of school and leave their friends, and me leave my current job which is an awesome job where I don't sit in traffic. I live in the country. I think your assuming a bit there.

But apart from me alone, which its not, we are on a good combined income, house prices have gone past joe average, that is most people, houses are $800K or more at greater then 7% and stress tested at 8-9% and banks are lending 5 times income. Which means its more then just me.

But hey we will see how prices trend, based on banks lending criteria. Your just arguing against the bank and its risk profile, not me. If I were the bank I would have a high criteria of lending in this climate.

This is interesting as well - https://www.interest.co.nz/banking/124685/switching-banks-mortgage-borr…

"After a long period of increases, since this data series began in 2017 but probably well before that, borrowers are restraining their appetite for taking on larger housing loan obligations. Perhaps they reached the limit of their financial capability, and were looking forward to much higher rates and therefore higher repayment obligations, with concern. They have certainly acted like that."

The points being one that you don't have to be in Auckland or Wellington to make the big money (like alot think) two that again there are great careers outside of Auckland and Wellington for young people with opportunities to progress. Three that those young people are able to buy a house in those local areas again alot of people say they can't. Fourthly my wife also came from overseas many years ago when you didn't have video calls and or cheap ph calls home never went to her parents and sisters funerals as airfairs were to exspensive and only had a echo ph call from family members to tell her of family passing. Yet England did something in the 70s that NZ needs to do they had an issue of London being to exspensive for,workers and or businesses so she up satellite cities like Bracknell Peterborough were by industries shifted out and created a city and took their workers. But first the UK govt had to create the infrastructure like good roads etc. Hence the 2 million people you talk about which in essence might be 200k people as alot have homes and jobs in Auckland could if we had good roading be shifted around the country. Obviously not all into one town but spread out throughout the country. In summary my point is that alot on here think of only Auckland and anything else is some hicktown maybe they should look at San Francisco and in a greater sense California as people abandon that state cause of the cost of living. Again that is alot of people who are on minimum wage etc.

they should look at San Francisco and in a greater sense California as people abandon that state cause of the cost of living. Again that is alot of people who are on minimum wage etc.

Those are significant factors, however there is also the stark realisation of those in southern California that they may not have any water security in a few years time, as well as increasing large-scale wildfires and large hikes in insurance premiums as a result.

Nice of you to take an interest in my life Colin gives me warm fuzzies, not sure why you care though, maybe a bbq and beers at yours, just been having a few after rugby so lucky for you, Im done till next week.

My point is which you conveniently overlook is banks will lend to people based on salaries & interest rates RBNZ dictates to them, the banks will then make a margin with as little risk as possible (theoretically). Unless there is mass migration changes which somehow I feel is highly unlikely (not sure why I feel that) then we are dealing with cards we are dealt, as a nation. People will borrow whatever the banks lend them.

I will borrow based on what my goals are, which you do not know, because I have not told you.You are just making assumptions.

IMHO we need property prices to drop, which could be fairly likely if banks lending criteria is strictly adhered to. We will see. I think banks lending and basing it on 5 times income and stress testing at 8-9% is more likely because thats what they are doing. While borrowers are reducing their debt risk profile, which I showed in that article. Today I read that if CPI has increased or is still hovering around 6% plus other factors, then interest rates could increase. Then we have DTI coming in next year. I heard emotions rule, but even for gucci bags you need cash.

Also we don't need to setup satellite cities, we have to many people in NZ as it is. Thats just your opinion for property growth more likely.

NZ should be looking at increasing productivity and investing in international scalable businesses that proportionally run on the smell of an oily rag like Xero. We should be looking globally and not locally to bring in our income, keeping NZers rich per person, and bringing in more money to make us even richer. Your way sends more money to shareholders offshore, from NZers getting poorer by holding more debt. Doesn't sound great to me.

My main point is we are dictated to by the banks. I still don't get what your point was, was it for me to move. If it is, I'm just telling my wife and the kids, Colin on interest.co.nz has told us to move, so we need to start packing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.