First home buyer activity remained steady in October, with only small movements in buying behavior.

According to the latest Reserve Bank figures, new mortgages were approved for 2437 first home buyers in October. That's up from 2233 in September, but slightly less than the 2481 approved in August.

However in spite of those monthly variations, first home buyers share of the housing market has remained unchanged for the last five months.

If we exclude mortgage top ups from the lending figures and only include new mortgages issued for the purposes of buying a property, first home buyers' share of that market has been stuck on 37% since June.

However, they may be becoming just slightly more cautious in regard to the amounts they are prepared to pay for a home and the amounts they are borrowing.

The percentage of low equity loans approved to first home buyers with less than a 20% deposit, declined for the second month in a row in October. It went from 32% in August to 31% in September and 29% in October.

That helped to push the average amount borrowed by first home buyers in October down to $617,564, the lowest it has been since April.

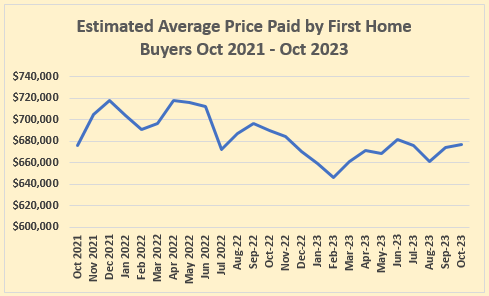

Interest.co.nz estimates the average amount first home buyers paid for a home in October was $677,347 - see the graph below for the monthly movements over the last two years.

Overall, the figures suggest first home buyers remain very active in the market and are prepared to commit to a purchase, but they are remaining cautious around price.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

55 Comments

I would suggest that actually - banks are remaining cautious around lending.......

Its incredibly encouraging to hear that at least FHB's are being cautious on price - they have every reason to be. The housing market remains fundamentally overvalued. I think encouraging low equity loans in vulnerable housing and labour markets are potential cannon fodder and not the wisest of moves anyway. It cannot be argued that bigger deposits up front are much better for reducing interest costs.

FHB's must be taking on board the regular posts made on this platform by realists. These are people that care.

re ... "It cannot be argued that bigger deposits up front are much better for reducing interest costs."

Care to explain that logic?

With respect, I know FHB's who took on board the regular posts made on this platform by the 'realists' between 2016-19 and are now needing to pay over 300k more for the same property.

Respect noted. There's been plenty of post's just like yours made before now. If the present to too hard to reconcile, why not bring up the past in order to undermine the credibility of saving for a bigger deposit to attain more equity up front now? Had unpredicted COVID not come along, house prices would likely have fallen anyway as they were overvalued then too.

These FHB's you speak of, I suppose inflation has completely eroded their deposits, all their money has gone on rent and they're dead broke?

More facts perhaps

Fair enough. I just find it a tad rich to offer such definitive comments as we care and take our advice, when this advice has been so wrong in the past.

BigBen, I just work on the basis of the risks associated with paying 8% interest on something that's still seriously overvalued, has soaring rates and insurance attached and the vested are promoting FOMO to the financially vulnerable just to protect their own interests.

I think this is when we should consult history to see what could possibly go wrong and promote some caution as this has the potential to ruin lives.

Let's not forget to pay tribute to the few on here that pushed the FOMO throughout 2021. Now that we're where we are, they've potentially created more emotional and financial distress than the advice you speak of has :)

edit

I think if FHB's are taking on advice from either side of the debate on this forum in order to commit to the single biggest financial commitment/risk of their lives, there are other issues at play! This site is interesting, thought provoking, informative and sometimes absolute BS, but not something to bet the house on.

dp

Thats the problem right there

commit to the single biggest financial commitment/risk of their lives

Its a house, a roof over your head. We have turned it into the only reason to get up in the morning and a sign of "great success" (borat).

There's not too many paying attention, most are talking at each other. Half are spruikers, the other half are bored old farts with rose tint glasses who say repeatedly that houses are overpriced. Houses are overpriced but just saying it does nothing.

I think the drop off in low equity loans is down to the high interest rates meaning that serviceability, rather than deposit, is the limiting factor for most FHBs, rather than any prudence on their part.

If that's the case then the market is more vulnerable (interest rate sensitive) than initially thought. Perhaps it's more a story of a commodity held aloft by a debt explosion.

Do you understand his point

Why are you asking me? It's the Baptist who's suggesting this article is misleading and you're foolish enough to go along with it.

Realistic (first) home buyers are aware that rents are climbing rapidly, while house prices are at a lower level than they were a couple of years ago (albeit starting to rise again in some regions). Further, mortgage interest rates are quite likely near their peak - and, inevitably, will fall.

Hence, there's meaty logic in buying at today's lower prices and, by doing so, eliminate paying (ever-increasing) rent. 😁 Additional benefits will accrue to homeowners from lower interest rates in the not-too-distant future - as well as, in the medium/longer term, capital appreciation and a sense of stability/security/satisfaction. 👍🍒

Nonetheless, if you're intent on being a life-long tenant - right through your retirement years until you shuffle off this mortal coil - then this site is a good place to hang about....... You can swallow the advice of those who believe the time is never right to buy a house, yet come here religiously - secretly yearning to own a home of their own. Make sense to you? Psst.... doesn't make sense to most other people either. 😉

TTP

OMG, now he's high....🌱

Are they being very active in the market or is it more that investors are being very inactive?

(AFR) Melbourne house prices on track to fall this month, Sydney close behind.

Melbourne home values are on track to post their first monthly decline since prices hit a trough in January, while Sydney is likely to slow to a crawl as listings rise faster than demand, CoreLogic says.

“I think it’s quite possible that we could be reporting a negative figure for Melbourne by the end of the month because stock levels are running ahead of demand

I suggest FHBers in NZ buy next year as prices fall and they have more bargaining power and rates are falling.....

The average first homebuyer loan amount $677,347 at 7.09% over 30 years works out at about $1050 per week. That's quite high but doable if you're keen and have two incomes.

For that reason, house prices won't fall much further.

It also doesn't leave much breathing room for higher prices to be paid.

The reintroduction of interest deductibility for landlords will delay the offloading of ex-rentals onto the market, with landlords still operating at a loss, just not as large as before.

With the ever rising costs of construction and no new $2M+ buyers, new builds will be limited to 2 or 3 bedroom townhouses stacked together in a row, unless you live in a provincial town where the cost of land is lower.

Net result: prices to remain flat for the foreseeable.

Good analysis which I generally agree with.

As I have said before there will be some regional variation though. I struggle to see how Wellington’s house prices won’t fall, given the slash and burn coming to the public sector in 2024.

My central view is while the economy will be weak in 2024, unemployment won’t get bad enough (outside Wellington) to hit property prices much.

4 to 5% gains next year in line with inflation is my pick, I guess most would still see this as "Flat".

You're a true soldier to your cause Zwifter!

Just wondering - would you like to see house prices drop further so to assist FHBs? Now that would be something worth celebrating - right?

If, like myself, you do own your house outright and it was bought to live in, then house price falls are inconsequential.

Oh well in that case buy buy buy!

4 to 5% gains next year in line with inflation is my pick,

Possibly. But this is the same water cooler train of thought that I have encountered. What does "in line with inflation" mean? It's almost like people believe that inflation is a natural phenomenon and that prices all magically rise more or less at a similar rate. This feeds into the dreadful urban myth that inflation destroys debt. This is completely wrong. Yes, the money supply is related to inflation and debt. But debt relative to GDP (a proxy for people's ability to produce) is increasing. Therefore, the idea that inflation destroys debt is fundamentally broken.

$1050/week doable how? That's $54600 a year of after tax money! You need a much higher than average income to afford that, that's not the image I have of FHBers. Or you mean doable by having an old car (10+ years), not eating out, no holidays, no kids, etc. How enjoyable is that kind of lifestyle?

There’s a reasonably significant number of youngish couples who earn at least 180-200k.

Assuming no kids, I think he’s not far off the mark.

Of course there are limits to how many young households earn that money, and therefore limits to the extent that FHBs can prop up the market.

It’s worth noting that while it wasn’t a runaway success, the previous government’s shared equity scheme also created a bit of demand from middle income FHB households. But I think that scheme has finished and hence that minor supporting influence on the market has gone…

There’s a reasonably significant number of youngish couples who earn at least 180-200k.

Huh?

Yes those are medians and averages. It doesn’t negate my point that a significant number of ‘youngish’ (25-35) couples earn at least 180-200k.

Yet my accompanying point also stands that there are limits to how many of those households exist.

You kind of contradicted yourself, either there's a significant amount or there's not.

Here's the chart I was struggling to find. If we work on $150k to $200k salary range, there's 67k earners. But that could be any age. 67k = 2% of income earners.

Housemouse and Pythagorus are talking about household incomes, not individual salaries. A 180k-200k household income means each spouse is earning an average of 90k-100k each, which is hardly outlandish. The number of couples who earn this is significant enough to put a floor on house prices falling significantly more. I would even hazard a guess that this is the average salary of working homeowners in NZ.

I am not as hawkish as Zwifter but I would pick that the price floor is about now we will have flat prices for the next two to three years while rents catch up.

A couple composed of two primary school teachers with teaching degrees who have both been teaching for 8 years (so are both 29) would fit in the 180k-200k household income bracket. Primary school teacher is a pretty 'normal' thing to be - so agreed, that kind of salary is not oullandish for a household composed of a young-ish couple.

That chart shows ~450k people earning 90k+. And the higher they are in that bracket, the lower their partner's income needs to be to make combined 180k.

There's some bad statistics going on here.

First, you want to measure the household income, cos it could have 1-N people all contributing. Not necessarily however that all of those want to buy a house together (flatmates all together count as household income, for instance). Then you would need to remove all of the people who already own one or more houses in this cohort. From the remainder you would need to figure out the housing intentions of the remainder and project it to account for regional disparities etc. Its all guesses and reckons, would require a fairly extensive study, but you could probably get a round about figure by studying this stats release: https://www.stats.govt.nz/information-releases/household-income-and-hou…

my point was simply that that data provides no useful evidence one way or the other :)

When Chaos posts data, people tell him they don't like his interpretation.

No I didn’t.

Something can be significant but also have its limits.

The word ‘significant’ seems to be widely misunderstood.

Pretty much the same lifestyle as I had SND, cannot complain. Its pretty hard for 10 years but the payback comes later so it depends on whether you are a "I want it all and I want it now" type or not. Its all pretty simple really you make your choices and you live with it.

And if unemployment picks up pace even faster and people are forced to sell?

Yes but how much does current price reflect Expectations for future capital gains?

More falls are very possible

LOVE IT!!! The last thing a young family should have is the burden of high debt, while navigating the other challenges life has to throw at them

you don't have to buy properties, young or old, but you must start building your wealth, especially when still young.

I bet RE agents are pulling their hair out in anger over the foreign buyers band remaining.

Looks like that juicy market segment will stay stuck in mud for the foreseeable future. At least they can collect the crumbs from the FHB 600-700k bracket.

Looks like that juicy market segment will stay stuck in mud for the foreseeable future. At least they can collect the crumbs from the FHB 600-700k bracket.

Reminds me of Blake's brilliant dialogue from Glengarry Glen Ross:

"F*** you! That's my name! You know why, mister? 'Cause you drove a Hyundai to get here tonight. I drove an $80,000 BMW.

"And your name is: you're wanting and you can't play in a man's game. You can't close them? Then go home and tell your wife your troubles. Because only one thing counts in this life! Get them to sign on the line which is dotted!"

Reminds me of Blake's brilliant dialogue from Glengarry Glen Ross:

"F*** you! That's my name! You know why, mister? 'Cause you drove a Hyundai to get here tonight. I drove an $80,000 BMW.

"And your name is: you're wanting and you can't play in a man's game. You can't close them? Then go home and tell your wife your troubles. Because only one thing counts in this life! Get them to sign on the line which is dotted!"

Noticing the FBs are now back in Australia market, namely Sydney, MLB and Gold Coast.

A gigantic house on my way to work has a For Sale sign put up last friday, except for the company name, the entire wordings content is in Mandarin!

can you share a photo? or the address at least?

use imgur for the photo - super fast and easy

My heart bleeds for the RE agents. The poor little lambs. <cue violin>

Know I have been a broken record on the imminent construction slump, but you know when the media aren’t covering it much I have felt duty-bound to do so:

https://www.nzherald.co.nz/business/ryman-healthcare-cites-challenging-…

Property investors with cash flows funded from rest homes. A model based on never ending growth in property prices.

Battening down the hatches as they re-assess their modelling.

Rastus, you make a very good point. Share prices of such companies that promote these products are lousy performers. They're ones for dumping as opposed to leaving them in the sock draw. Much like a few posters here, this business model is groaning.

never ending growth in oldies at least ... for a decade or two ...

Less construction of Retirement Village units means less supply and more old people staying in their family houses, just when there is higher population. Perfect storm

The site of the takapuna fire station is a great spot, units there won't be cheap

House prices will remain stable for now, once mortgage rate start to drop, we'll see a big jump, especially in Auckland

Good. Better for them in the long run if they have a bigger deposit.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.