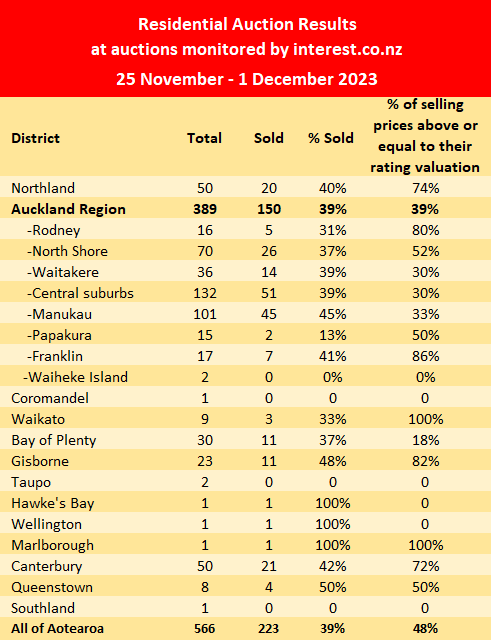

There was a big jump in the number of properties put to auction last week but the sales rate dipped back to under 40%.

Interest.co.nz monitored 566 residential property auctions last week (25 November- 1 December), up from 476 the previous week and the first time this year that the number has been above 500.

The number of properties that sold under the hammer was also up at 223 compared to 190 the previous week, but because the number of properties that sold didn't increase as much as the number on offer, the sales rate dripped slightly to 39% from 40% the previous week.

The sales rate had been above 40% for 26 of the previous 30 weeks.

However, the percentage of properties that sold at prices that were above or equal to their rating valuations crept up to 48%, which was the highest it has been so far this year.

So overall, the auction rooms were the busiest they have been this year, and there were plenty of buyers about but they are remaining cautious with their bidding, leading to some tough post auction negotiations on many properties.

The table below shows the district-by-district results for all of the auctions monitored by interest.co.nz last week.

Details of the individual properties offered, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

95 Comments

Busiest period and a sales rate of below 40%.. definition of a cold/we/damp/lethargic/ uninspired housing market

A damp letdown, just like Spring/ summer so far

the percentage of properties that sold at prices that were above or equal to their rating valuations crept up to 48%, which was the highest it has been so far this year

Some only see what they want to see.

Interest.co.nz monitored 566 residential property auctions last week up from 476 the previous week and the first time this year that the number has been above 500.

Hmmm

The number of properties that sold under the hammer was also up at 223 compared to 190 the previous week

More houses sold, it's quite simple really, more houses sold...

And so what? It’s not a bad result, it’s not good. It’s mediocre

Sure, if you say so!

Well if this is good volume and sales, then the bulk of 2023 must have been worse than most realized. Alternatively the lead up was abnormally high volume and success, so much so that those involved mistakeny thought that level was normal.

Well, it's the best volumes and sales and prices of 2023... that's what the numbers say! Maybe not the best week to call it a "cold/wet/damp/lethargic/ uninspired housing market" ?

Wasn't that always going to happen during spring? Isn't spring always the period with the highest number of sales? I smell seasonality (and its playing with my sinuses)

The housing market is busy enough.

Further, the downward trend in prices is abating markedly. Notably, more properties are selling at, or above, their rating value.

This blog is also pretty busy. Like it or not, that's an indicator of enthusiasm for housing.

When folk give up coming here, we'll have a clear sign that the market is really struggling....... But don't expect that to happen anytime soon.

TTP

Get in quick "Taking the Proverbial" .....this is the BOTTOM of the market !! .....fill ya boots mate !

I have, and where I've bought, the action's suddenly heating up - since the election.

Its Tip Top !

Do you have a life? I swear you’ve got alerts for whenever a new property related article is published for the purposes of adding your 2 cents. Step outside mate, get some fresh air. The market will continue to bounce around for a while until there is some certainty in rates. But just know one fact - the HPI (the indicator you DGMs use) has gone up every month since August I believe. Just don’t let all of this get to you too much!

HPI should at least be going up in line with inflation, if it isn't houses are losing $ value.

If that is the case my mortgage is also losing value.

That's correct.

"Put very simply, inflation helps borrowers because it reduces the real inflation-adjusted value of their mortgage. Thus in “real terms”, a £200,000 mortgage will have fallen in value during 2022 by about 10 per cent, or £20,000. In 2023, if inflation averages about 6 per cent, the figure will be £12,000. Thus, in the two-year period 2022-23, a mortgage worth £200,000 in 2021 will have fallen to £168,000 in 2021 prices just by inflation, even if not a penny had been repaid of the original capital by the borrower (on an interest only loan for example). Now of course, wages tend to lag behind inflation, but current wage inflation is not that far behind CPI inflation (the ONS has wage inflation averaging 7%) and in the longer run will almost certainly catch up. So, in the long term the outstanding mortgage will be lower in real terms relative to both prices and wages. In the long run, the mortgage borrower is certainly made better off by inflation."

If you have difficulty paying the increased monthly mortage payments, that's a seperate issue of liquidity or "cashflow".

I'm not interested in your mortgage. We're talking about house values and whether they are going up or going down. They are still falling in real terms.

Just like what unfolded in stealth fashion in the 70s, when adjusted for inflation, house prices are now still falling.

I suspect the root cause of Sp - - - - - rs naivety is most weren't even alive in the 70s. That's hardly the fault of the resident realists now is it?

...... when adjusted for inflation, house prices are now still falling. [Retired-Poppy - above}

However, when earnings (rental income) are (rightly) factored into the equation, the vast majority of home owners/investors are well ahead of the eight ball.

Remember, we seldom hear complaints from them. Indeed, the housing market is a great place to be for long-term gain - both financial and non-financial.

TTP

TTP, it's very rarely I pay you a compliment, so I'll try not to become too emotional😭. It would now seem you're a reliable barometer of the health of the NZ market. Each time you up the rhetoric, the market tumbles shortly afterwards. I wouldn't be at all surprised if the well documented FHB apprehension is in part thanks to you.

A job well done!😊

Hi Retired-Poppy,

When you remove your blindfold - and start seeing the big picture - then first-home buyers might stop baying for your blood.

Right now, having been burned by your crook advice, they aren't convinced of anything you splutter.

TTP

Even while strung up on a FHB's wall you're not a particularly attractive barometer, it's the reliability and consistency that matters most.

BTW, it was you that recommended that they buy in Nov-21....

Edit!

by tothepoint | 24th Sep 21, 12:40pm

Unfortunately, "feeling rich" can make people spend more, especially when they're mesmerised by the thought of cheap money - in the form of low interest rate loans......

See you outside the Audi dealership first thing tomorrow morning, old chap.

TTP

The above quote is the sort of thing I was saying in late-2021, Retired-Poppy.......

It speaks for itself. I saw the housing market correction coming and made my views well-known about the imminent downturn - sometimes using humour for added emphasis

TTP

You guys too busy quoting each other

the facts are the market is tepid in sales, too many listings, asking too much , too high interest rates, too high test rates for FHBers, to HIGH everything.....

too long to wait if you NEED TO SELL

The best day to sell is TODAY!

Talking around the fringes seems to be an argument for the over leveraged these days.

The only thing matters is the overall direction, not the noise in between.

2024 isn’t going to be kind to the market propagandists.

TTP, this is the sort of trash you were posting in late 2021, by tothepoint | 3rd Sep 21, 8:39pm - "NZ house prices are increasing - on a sustainable long-term trajectory"

LOL! - you've been caught out yet again! Note you used that key word sustainable too!

(edit) Its glaringly obvious you didn't see the correction coming.

Hi Retired-Poppy,

You're back with your old tricks of misrepresenting what people write here.

Not only do you keep changing your own posts, but you change the posts of other contributors as well. Unscrupulous.

You never play honestly, so go shame yourself somewhere else,

TTP

No tricks, just plain facts. Your Sept 21 post reminds me of this one from the same month in 1929, "Stocks have reached what looks like a permanently high plateau"

Priceless!

With that you win the, Most Excellent Post of the Year award for 2023. It must have been a tough time for you after 1929

I jest about the last sentence 🤣 but here's a question, what were the interest rates doing from 1929 to 1940

I suppose you want me to research house price/inflation rate from 1930 too? Don't be lazy.

"I'm not interested in your mortgage" = I'm not interested in any good news for you. I'm only interested in what makes you suffer and I will cheer on any news that I think could hurt people that believe in different things than I do"

Very few people here wish pain on others..... we watch people inflict pain on themselves, sometimes cheered on by others.... but most of us who believe the price floor is not yet in do not wish harm on others.... we do not profit from others pain.

Amen.

For those of us that own homes with mortgages, inflation is a good thing so long as we can service the interest. Even when houses are falling in real terms.

Example: a house is bought in 2023 from $1m with a 800k mortgage. The owner owns 1/5 of the house if you will.

Lets say in 2024 there is 10% inflation and hose prices are stagnant. The house is now worth $900k in "2023 dollars". The owners equity is still 200k but he now owns 2/9 of the same house. Nevermind the nominal house price rise that you have dismissed. Inflation has made the man wealthier in real terms.

Inflation is a good thing for leveraged asset owners, even if the high interest rate to counter it is not. That is why most home owners care about nominal rather than real house price rises. I would rather make a nominal gain in an inflationary environment than a real gain in a deflationary environment.

Baptist, since you've already declared on here you bought your house to live in as opposed to speculate on, it hardly matters what happens to the market - right? I'm becoming more puzzled on each occasion you feel the need to repost the same reinforcements on how, as an individual, you're a winner in investment / money terms. Your argument is that somehow you will always gain wealth by using others money no matter what. I think taking wage increases for granted in an inflationary environment is dangerous thinking. For starters, not everybody gets them.

Do you think it is a good thing if house prices continue falling so to give more FHB's a sustainable entry point? Houses are for living and not speculating on.

I recently bought a home to live in but I have also been a landlord for 14 years. I have two rentals and a plan to build two more in the next five years.

Whether I view house prices falling/rising as a good thing is inconsequential. My "feelings" towards a price movement has no bearing on what actually will occur. I only comment on what I think might happen and not on whether I think it is a good thing or not. It would be wise for all of us to have the humility to know we can't influence the market direction in a meaningful way, and rather make financial decisions based on where we believe the current is moving, regardless of whether we see the direction as beneficial for society.

On a personal investment level, I don't care about house price rises/falls in the medium term. Capital gains/losses are only realized when you sell and I am not planning to sell for at least 10 years if at all.

Stop it, the DGM's will LTS

You're up early... have you run out of ICE?

You just can't stand the facts.. hide behind your thin veil..

I’m always up early. Facts are HPI has increased since August, are you alright in your head? I’m coming to think you’re just an attention seeker on here who gets a kicks out of all the likes you get from your fellow DGMs. Whatever helps you sleep at night mate.

You definitely sound angry and frustrated.. the pathetic housing market is taking a toll on your mental stability

Aren't you a lovely person.

Thanks for noticing.. and glad I'm not like you

You don't like having a wonderful family, being married for 30 years and still in love? Having lots of awesome friends and having multiple international holidays per annum? You don't like paying others wages so they can support their families whilst having a great relationship with your staff?

Check yourself mate, your phrasing is weird.. just like your attitude

Is it inappropriate to admit that I just thew up in my mouth? The Hall Monitor can be anything he wants on this anonymous forum....

I apologise DGM if my phrasing is weird, english is my 3rd language

Hi Yvil,

You've contributed superb analysis and wisdom today. Excellent thinking and accuracy. 😇

BUT PLEASE, when you address the DGM, have mercy and stick with one-syllable words.

TTP 🤭

Two fools don't make a right

Spoken like a sore loser. Did you rent go up $50 a week? Sorry about that.

Lol..I'm mortgage free..

You are the scum of the earth, so you should be the last to call anyone a loser

by Dgm | 4th Dec 23, 6:59pm

You are the scum of the earth

Do we really need this language on Interest's comment section?

So you have ignored your mate's name calling? Typical you

Stop deflecting, don't you think calling someone "the scum of the earth" is extremely rude and low?

I call a spade a spade..

If it's not you, it's him having a go at me..

And you call others "the scum of the earth". Are you happy to be known for that kind of language?

If you deserve to be called it, you will be

OK, that's your choice of course. But be careful, being rude to someone says more about the person being rude, than the person you speak about.

Have a good evening.

Wow, you're definitely such a narcissist, that you choose to ignore the initial perpetrator..

by Dgm 4th Dec 23, 8:40pm. Two fools don't make a right

You said it yourself above...

We are witnessing “Teacher's Pet Syndrome”

Record houses for sale, more houses sold and at record prices? Can't be, many Interest commenters told us so on Saturday's "auction results delayed" article.

It is interesting to see where houses are selling at or above their rates valuation. Only 18% in BoP; i wonder if that is to do with flood damage etc.

Pretty grim in south Auckland at 30% or so.

To correct the sole Hawkes Bay auction result, the property was a 1,000sqm bare piece of land in a new subdivision and went for $820K, against an initial (2023) RV of $790K. I can only guess the RV in the results page was for the previously undivided section.

How on earth is a quarter acre of bare land in hawkes bay worth that much? Hard to see how we fix our economy and society without addressing the exclusionary cost of access to land. If that means heavy land tax, fewer regulations or weakening of property rights then so be it - the alternative is the slow south africanisation of our society which is no good for anyone, rich or poor.

It's in a small, "exclusive" subdivision in Havelock North. I'm surprised it went for that much but it appears smaller parcels of land are going for similar or higher $/sqm in the area.

Nah BoP got way overvalued

Interesting to compare this to same time 2 years ago when numbers had been declining for 6 weeks.

https://www.interest.co.nz/property/113656/overall-sales-rate-barfoot-t…

Will sales rate increase to 68% over next 6 weeks?

agnostium ....you may miss this post, but I had a look at the article in your link above and found this beauty from our resident "spr .....ker" TTP .....

by tothepoint | 7th Dec 21, 12:27pm

Hi Chebbo,

When inventory goes up, prices go up.

When inventory goes down, prices go up.

In short, house prices are not beholden to anything.

TTP

I eagerly await the "increases" in house prices, when more properties are listed early next year ......hahahahahahahahaha ...it doesn't work that way, as there will be a "glut" of property on the market, that will be asking crazy prices .....with hardly any buyers at those prices.

Pure entertainment our TTP is, pure entertainment!

You are so right R-P .....that's all his comments deserve and anyone that agrees with him, is playing the same old "spr....ker" game.

I like ACTUAL FIGURES, not cherry picked stats !

A shame the 'house falling off a cliff .jpeg' couldn't make an appearance on this article after the steady auction sales... not quite what the DGM were hoping for after Saturdays article featuring the 'house collapsing .jpeg'...

Good to see at the most busy time of the year 39% sold. December and January will be quite hard to believe some people are happy buying overvalued houses not sure at what point this stops as average income earners have no chance of buying in many areas.

Well under half the properties going to auction are selling and under half of those are achieving prices above their 2021 CV's. Great News.

Meanwhile parts of Auckland have mortgage arrears above 5% of borrowers. Maybe that 3 bed 1 bath 1950's weatherboard on 650 m2 in Otara for $1 million wasn't such a great buy after all.

I'm sorry you're second guessing your Otara house buy Westie. I hope you will be able to deal with the cashflow until interest rates drop a bit.

70-80% of mortgages already changed to the current rate of 7% and guess what, not a big change in number of houses for sale. What's the conclusion then?

The Sep '23 yield on fixed residential mortgages is 5.29% (RBNZ B6). Up from 2.79% Sep '21. Current special fixed is 7.01%, standard fixed 7.6%.

Assuming a flat distribution, that does indicates approx. 59% have refixed - if all managed to refix at special rates - which would be the best case scenario. 52% worst case (no one getting special rates). The truth will be somewhere in between, but it's nowhere near 70-80%.

Intriguing to see some spin this as a good result, and others a bad result!

Really? You must be new to the Interest comments section HM.

It's like when you're bottom of the table in the relegation zone and you eek out a draw with a mid-table team. Average result for the mid-table team (those hoping that housing will become affordable for average New Zealanders), nothing has changed. Good result for the bottom of the table (spruikers) but you're still going down. Only team really happy are the top of the table who bent the financial rules in their favour and are pretty much romping home (banks).

I live in a city fringe suburb in Auckland. There are (and have been) several houses for sale in my street, and those directly connected, this includes 4-5 bedrooms, smaller houses, and 'units'. They've all been moving very quickly - particularly the houses.

Let's all pop open a chilled bottle of Moet and celebrate !!

In Auckland anyway, 39% actually sold - and 39% of those sales were actually above CV !!

Absolutely positive stats everyone - so just on 15% made a profit on sale - even better !!

Where's that second bottle - the party has only just started.

Oh WTF let's just get out the case ! ....we ALL have to celebrate !!

How about popcorn, Crazy Horse?

I hear that's what really pops your cork.

Anyway, learn to live within your means. You're still not on the property ladder, old chap.

TTP

Classic example of "broad brush" banal statements from "Taking The Proverbial" .....do you have a periscope down there in Palmy and know what everyone's property situation is ?

"But don't worry. It'll all happen in Jan/Feb/Mar"

Yeah. Right.

I given up with the "sprinklers" .......they just sprinkle "advertorial anecdotes" around for their businesses - that is all they are.

But what makes me laugh is they come on a financial website and make such "broad brushed" statements - with no actual examples to back it up.

Because if they did give actual examples, they could be researched to find out the truth - but part of their game is to NEVER release the "actual" truth.

Why would they - it all comes back to THEIR VESTED INTEREST in the game.

"It'll all happen in Jan/Feb/Mar"

What will happen Chris?

I've been tracking the sales prices of properties that actually sold against the values they last sold at.

And from there calculating the annual percentage increase over the number of year between last purchase and the current sale ...

And guess what?

LOL.

I'm intrigued now. Do tell!

Doubling in price every 7 - 10 years !!!

You know the Rule of 72? No?

https://en.wikipedia.org/wiki/Rule_of_72

Thus to double in price over 10 years you'd need an annual return of 7.2% per annum.

How many people are getting close to 7.2% appreciation per annum?

But for the more mathematically inclined the formula is: ROI = (Ending value / Starting value) ^ (1 / Number of years) -1

I've been doing this for hundreds of auction sales for a while now using some excel code I threw together to pull numbers from various web sites using the HTML DOM. (It only confirmed what I already knew.)

Man, Kiwis are dumb. LOL.

The house is no longer an ATM?

.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.