Discussions around housing affordability often focus on how difficult it is for first home buyers to get into a home, with how current conditions are affecting the ability of existing home owners to move on up into their next home often overlooked.

Interest.co.nz's latest data suggests the kiwi passion, or should that be obsession, with moving up the property ladder remains a surprisingly affordable option for many, in spite of the currently high mortgage interest rates.

The data takes the example of a working couple who bought their first home 10 years ago at what was then the lower quartile selling price, and are looking to sell and move up to the next rung on the property ladder by buying a home at the current median price.

According to interest.co.nz's calculations this should be well within reach, because the couple would be likely to have accumulated enough equity in their original home to put a 50% deposit on a home at the current median price, and the mortgage payments on the balance would only take up just over a quarter of their after-tax pay, assuming they are on average rates of pay.

Let's take a closer look at the numbers.

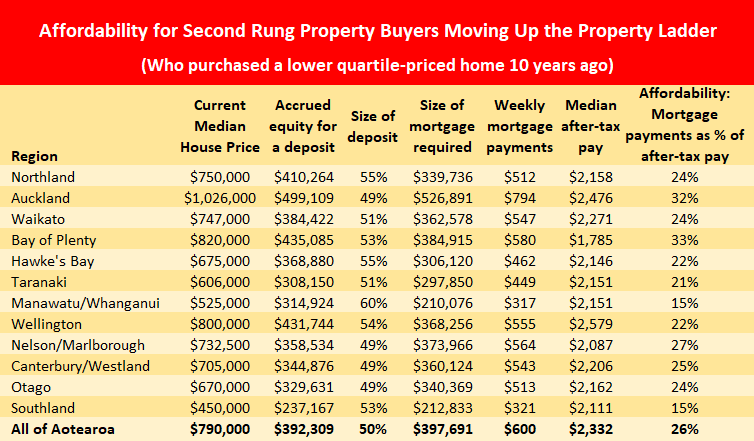

A home at the the Real Estate Institute of New Zealand's national lower quartile price 10 years ago (February 2014) would have cost $280,000.

If that same property was sold at the February 2024 lower quartile price it would fetch $595,000.

Interest.co.nz estimates after the owners had repaid the mortgage and paid their selling costs such as agent's fees, they would be left with net equity of $392,309 to put towards another home.

Those calculations assume the original mortgage was for a 30 year term, had remained on the prevailing two year fixed rate and the owners had not made any lump sum payments.

That would give them a 50% deposit (using rounded percentages) on a home home at the REINZ's February 2024 national median price of $790,000, meaning they'd also need to take out a mortgage for $397,691.

The mortgage payments on that would work out at about $600 a week.

Using median pay rate figures for people aged 34-39 would give the couple combined after-tax pay of $2332 a week.

That means the mortgage payments would take up 26% of their take home pay.

Essentially they would be able to move up the property with 50% equity on their new home and be paying about a quarter of their take home pay on the mortgage.

By almost any measure that makes moving up the property ladder an extremely affordable option, even for people on average wages.

Although there are regional variations on the above figures, they are not substantial.

For example, In Auckland, which is the second most expensive region for housing in the country (behind Queenstown), the same scenario as above would have given the home owners a 49% deposit on a median priced home, and while the mortgage payments would increase from a quarter to a third of take home pay, that's still well within affordable limits.

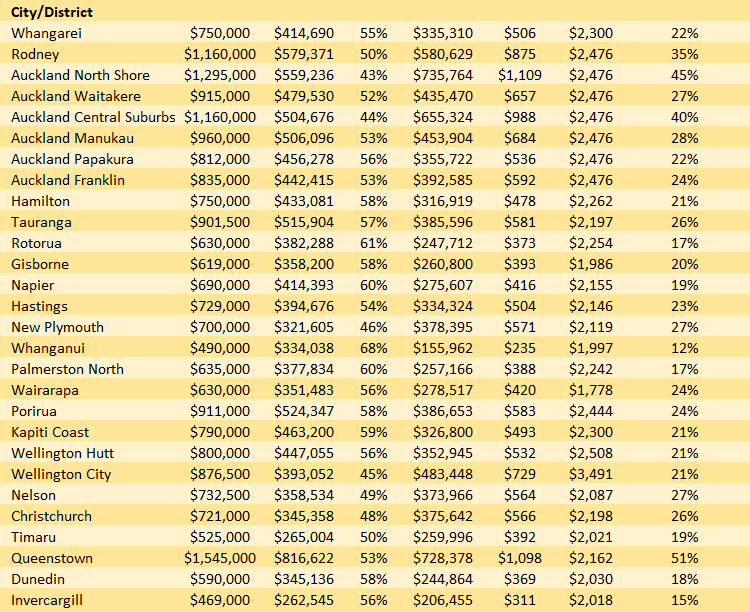

The table below shows the current affordability measures for the example given above, in all of the major urban centres around the country.

The comment stream on this article is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

65 Comments

It would help to put current most-common context for FHBs into this article. The average age for becoming a FHB is 34 - so that person may have had a 30-year mortgage as is assumed. Then ten years of gained equity for this archetype would put them at 44 - so the median earnings used would be for an older age group (and so would likely be higher than the 34-39 age bracket used). This older age might affect the term available on the mortgage they would acquire on the second property and so the repayment amounts and affordability against the income used.

Also - what isn't discussed is the relative risk to future capital gains (with respect to inflation) - yes they might have a house at a higher price, but might they be better off waiting and paying down smaller debt, faster to increase disposable income and/or savings.

Valid points. Just regarding your last sentence, yes if someone were to wait a couple of years for a lower house price then they'll borrow less for sure. Even if higher interest rates result in similar repayment amounts, a smaller principle amount is much easier to pay back with increased repayments/lump sums.

- $800k mortgage @ 3% = $3300 per month. Increase repayments by $500 per month, it's now a 25 year loan

- $500k mortgage @ 7% = $3300 per month. Increase repayments by $500 per month, it's now a 21 year loan

But what if the gamble doesn't pay off?

"$800k mortgage @ 3% = $3300 per month."

What a highly leveraged buyer in 2020 - 2022 period is potentially facing as mortgage interest rates increase

$800k mortgage @ 7% = $5,372 per month

Increase of $2,072 per month (63% increase in mortgage payments)

Increase of $2,072 per month = $24,864 per year in net income

This is $37,110 gross income (at 33% marginal tax rate)

Don’t worry, this website is stuck 25 plus years in the past, when it was realistic for people to buy in their mid to late 20s.

Their affordability reports always assume this. It’s ridiculous, and has been pointed out several times

some serious thought needs to be given to a number of things here, including readers’s opinions, how people who make contributions are treated etc.

We're putting all we can afford into the Kiwisavers of our 7, 9 and 11 year olds in the hope that when they're less than 30 they can get a deposit together. It's not much, but we're hoping compound returns will work some magic. That's what we're reduced to - hoping for magic so our kids can own their own home.

We're also starting now on how principles behind finding a life partner so their houses don't get lost/halved through a break-up.

The master of the long game, I like your style.

John Key sure tried his best to undermine Kiwisaver. Taxing employer contributions had to be the most cynical move ever. Gotta love our TTE retirement system!

One must also subtract the purchases made in order to keep up with the Joneses and impress mates, financed by drawing down those capital gains. The Ranger, the boat, the big TV and home theatre, the "treat yoself" trip to Fiji with the lads...and then there's more mundane stuff like childcare costs associated with both parents heading out to work.

It takes great restraint to leave those paper gains untouched when one feels one has finally "made it onto the ladder."

That's the thing, they are imaginary numbers until realised therefore the wealth effect of this is completely foolish. Why spend more on the basis that the supposed value has increased when that value could be false, and the true value is only realised based on what others offer you.

Or with "great restraint" you can buy a rental property instead ... That's working really well I hear. /sarc

Buying renters has always worked for me. Selling them was the not so smart bit.

There's also the feature of our current housing market that yes you can upgrade, but on the backs of those who want to get on the ladder. Selling our first house 4 years ago after 7 years ownership netted us ridiculous capital gains, even after all the hard work we did, so we easily upgraded by shifting areas, knowing we'd never be able to go back.

But at least $200,000 of our capital gains was the result of a broken market and we sold to FHB. Yay, they're on (and promptly gained, then lost $200,000 over the next 2 years).

We paid $200k in 2017 for a basic 3 bedroom 80's Keith Hay home on 1/5 acre (Masterton). Sold for shy of $600k in 2021, also to FHB. Gave us a very nice deposit for our central located 4 bed, 2 bath on 1/4 acre near all the good schools. As you say, all off the back of FHB paying greater sums.

According to OneWoof it's now estimated worth $150k less but then so is our place.

Sounds like what we did. It's all about when you bought, not much else. We transformed the worst house on the street to one of the best, but it still doesn't account for the extra $200k that allowed us to double our section, double our garage, double our footprint and keep the same mortgage payments.

Broken.

Lucky for some, not for most

It is not luck. It is focus and sacrifice.

That joke prompts a smile with a little bit of sick in the mouth

You realise the "sick in your mouth" comes from within yourself.

It is both of those things, given that house prices have changed both very rapidly and very unpredictably in the last 4 years. For example, in my city from March 2020 to March 2021 house prices increased by about $150-200k on average. They have now gone down, but it means for example that someone who bought in March 2020 has generally made about $100k over the purchase price, someone who bought six months later is sitting pretty much even, and someone who bought six months later again has lost a substantial amount. When six months either way makes such a massive difference to your relative positions, luck is definitely a factor. Of course it takes focus and sacrifice to be in a position to buy a house in the first place, but there are all sorts of reasons that have nothing to do with focus and sacrifice why one person might be ready to buy a house 1 year earlier than another (like being born a year later, and thus having graduated from their qualification and entered the workforce a year later, for example). So two people, who have exactly the same level of focus, who have sacrificed the exact same amount in terms of saving and living frugally, could be in very different financial positions simply due to a one year difference in graduation year. If that's not luck playing a role I don't know what would be.

You said that the FHB buyers "gained, then lost" 200k.

Isn't every homeowner in the same boat of disappearing paper gains. Im not talking about the supertraders that sold at the top and did not repurchase

That's the thing, the rises and falls are talked about in percentages, so the higher the base the bigger the swings. Theoretically one of our properties has "lost" about $500K so it's actually moved the house closer in pure dollar terms to someone further down the ladder looking to move up who has "lost" $200K. Ignoring those pesky interest rates, of course.

Then again, paper gains (and losses) are worth exactly $0.00 until they're cashed out.

"One of our properties"

Lucky guy and good on you, how many have you got now. Very well deserved, its probably why I always enjoy reading your comments

Thanks, but no luck involved, just time and timing. We bought that one as our first home when we were newly married DINKs.

We only have one other property, which is our "forever home" and has enough land and facilities to provide a decent income when I eventually retire. Diversity is key in my mind.

"Then again, paper gains (and losses) are worth exactly $0.00 until they're cashed out."

Really? My banks don't think that way.

According to most commenters on this site, only paper losses are real, paper gain aren't, lol.

It's a bit disingenuous to generalise that moving up the housing ladder is affordable when cherry picking time points for a FHB from like 10 years ago, with a huge amount of capital gains occuring, and looking at what they could afford now in a gloomy market.

If you'd pick an FHB from 2-3 years ago their next home at current prices would be grossly unaffordable as they'd likely face a loss in equity (assuming they're buying houses in an comparable area).

In order to generalise the housing upgrade affordability, one would need to do the 10 years comparison over a number of years/decades.

"It's a bit disingenuous to generalise that moving up the housing ladder is affordable when cherry picking time points for a FHB from like 10 years ago. If you'd pick an FHB from 2-3 years ago"

Greg could have chosen 20, 15, 10 or 5 years ago and the outcomes would be similar. The cherry picking part, is choosing the specific time of the market peak of 2-3 years ago.

the average hold time for owner occupier is around 6 -7 years, if someone bought 2-3 years ago, we need to wait another 5 years to see how affordable for them to move up.

"the average hold time for owner occupier is around 6 -7 years"

It used to be. Hasn't it got longer?

That said, the length shifts up and down depending on the market cycle. And the age of the owners has a considerable bearing. As does the location.

Interesting. I was thinking id sell after about 7 years. I'm so predictable.

This is almost my exact situation. As a GenYer now in my second home having bought my first home in 2010, I'd be the first to acknowledge it was way easier for me than today's FHBs.

"it was way easier for me" - With house prices largely going sideways, yet still falling when adjusted for inflation, how easy is it for you to leverage up even further right now? Costs of home ownership are expected to escalate for years to come due to heavily indebted Councils and climate change through insurance. Going forward, have you given any thought as to how leveraged owners will be compensated for these additional and unavoidable costs? Can any capital gains be easily banked by those needing cash flow to put food on the table? The investor/flipper of yesteryear has hit the wall....

What is your advice to prospective FHB's again? "There is no hurry to buy?"

R-P the system is broken. Start a political movement

....it certainly is. From your perspective, what is the purpose of this forum? To provide others with useful insight?

@ Flying high

Eat a prune?

Retired-Poppy: Clearly you lack the intellectual bandwidth to understand that property ownership/investment is not just about capital appreciation. Just as important is rental return - including the saving in rent made through buying one's first home. In fact, rental income is a key driver of capital appreciation over time.

Also, Retired-Poppy, you fail to understand/acknowledge that property markets are cyclical - that there are downswings and upswings over time. You are fixated with downswings. You always believe that the market is about to plunge - even as it starts to soar. You have never acknowledged/predicted an upswing (and rising house prices) in all the years that you've been coming here. Thus, your comments here invariably come across as being biased/unbalanced and your predictions constantly miss the mark. More often than not, what you say is misleading and deceptive.

You ought to have noticed by now that FHB's and other property owners are very seldom malcontent. Very few people regret having bought property - even those who bought at a market peak. Notably, this blog contains few (if any) actual property owners who report feeling negative about their property purchase(s). Such people/comments are scarce - almost impossible to find.

To Everyone: Enjoy the Easter break.

TTP

Seriously, if any of this were true, investors would be already biting at the bit to be ahead of the curve, unsold inventory would be dropping, sales volumes soaring along with prices.

Your posts are rich with luxury the novice investor/flipper of yesteryear enjoyed and can no longer be taken for granted. Your advice is based on backward focused assumptions and is dangerous.

Again, as the leading Property Spruiker on this forum you have a proven well documented undesirable history. You lack empathy and somehow remain heavily vested in the industry.

From your perspective, what is the purpose of this forum?

It gives you and I something to do in between "hay-making"

Good grief, Tall Poppy. Many of us are scouring the mortgagee sales, analysing auction day results, generally keeping a sharp eye on the market, so we can dive in at something approaching the appropriate time. It doesn't have to be exact, but the more equity we have, the less perfect our entry into the market has to be. I have 4 kids. They own 10 bits of land, with 8 units/houses on them. The only help they got from their parents was example and encouragement. their buying ranges from 20 years ago while at university, using money saved from part time work, to 2 years ago, post Covid. Property buying is doable at any time in the cycle, with focus and sacrifice.

"but the more equity we have, the less perfect our entry into the market has to be" - Perhaps that's a viewpoint of someone who's parents gifted them a deposit?

Time taken to accumulate a decent deposit @ 6% plus pa during a flat market affords one the position of having more equity up front and less dead money (interest) paid out. TTP has finally acknowledged this with the one true stipulation that TD's won't make you rich. Buying in the worst of economic times is prudent. Banks will be more willing lend to those with large deposits and you can cut a better deal. Downturns come often after times of loose credit and we're just at the beginnings of one that could be very prolonged.

There need be no hurry to buy. Be suspicious of anyone who suggests there is. Value that hard saved deposit that took focus and sacrifice to attain.

Property buying is doable at any time in the cycle

...

20 years ago while at university, using money saved from part time work

Not like that it ain't.

"They own 10 bits of land, with 8 units/houses on them"

Is any one of them specialists in residential property or professionals in the property business? e.g property trader, Airbnb, property developer, builder, real estate agent, etc

Property specialists are very different from owner occupier buyers who have full time careers elsewhere and have no inclination to become property specialists or get involved in the property business.

Some careers where people want them to be focused full time on their career rather than spending spare time in the property business.

1) Medical professionals, - nurse, doctor, surgeon, physio

2) Teacher

3) Social workers

4) Police

5) Fire service

Some careers where people want them to be focused full time on their career rather than spending spare time in the property business.

1) Medical professionals, - nurse, doctor, surgeon, physio

CN please apologise for that bs lie. How do you this these professional people invest their money.

Ive seen it lots of times

"How do you this these professional people invest their money.

Ive seen it lots of times "

Let me clarify my comment.

Yes, they can be passive investors, financiers. Anyone with capital can be a PASSIVE investor in any type of business enterprise.

However most of these health professionals are NOT ACTIVELY INVOLVED in the DAY TO DAY operation / management / decision making in the property business such as property development projects (e.g buy a piece of land, get the necessary consents, discuss building design plans, discuss materials, and build 4-6 residential townhouses on it). This is what I mean by being involved - ACTIVE participation in the day to day decision making at the property project level, or property development business.

Most of these health professionals do not have the inclination to be ACTIVELY involved in day to day decision making of a development project - it is way too time consuming, and most may not have any interest in spending their time in those activities.

Hahahahah! For the past 2 years I’ve seen many malcontent people on here blaming the reserve bank or Mr Orr for being incompetent. Furious that they’re being ‘ripped off’ by banks. Even the government is talking about inquiry into banking oligopoly, BAFFLED that banks are making so much profit now. Gee why is that?

Yeah nah they love their homes, and don’t have to pay rent anymore. So why do they have to pay so much interest, preventing them from building a nest egg of savings? Paying off their home? The property ladder promises freedom and wealth, so why is the opposite happening? Durr why are savers doing OK now and recent homeowners suffering from ‘cost of living crisis’?

people will believe anything to protect our precious property ladder. Generate money without working, yeah that’s sustainable! That will last for ever!

To answer your questions in order. 1) Pretty easy. 2) Yes my compensation will come through increased rents. All of the extra costs of housing you list will be shouldered by all housing consumers, whether they are leasing or buying. 3) capital gains can put food on the table only when you sell up. This is a concept called liquidity. Only invest to the degree that your cashflow can continue to meet your outgoing expenses and debts. 4) Without going into an individuals unique circumstances, I would generally advice a FHB who is able to buy now. As you have already alluded to, we have a high inflation environment that will reduce their mortgage in real terms at the same rate it reduces their deposit. By the time they wait for their monthly rent to be more than their interest payment, house prices will be on the up. If I had taken the advice to wait 8 months ago when I bought, my net wealth would be more than 50k lower than it is today.

having bought my first home in 2010, I'd be the first to acknowledge it was way easier for me than today's FHBs.

Well I'll be darned as my boomer g-mother used to say.

Or, they could not move up the ladder, but still increase their mortgage payment to $600/week and be mortgage free in no time.

That only works on a floating rate. My bank only allows 5% extra of the capital over the minimum payments to be paid off every year on a fixed term.

Change banks ASB allows overpayments

Yeah we are with ASB and I'm currently maxing out on both loans (as mortgage is split into two) what they will let me pay off per fortnight.

We are contemplating upgrading house (I need more space for home office, and would like another child in the near future) and I figure smashing down the mortgage would be beneficial whether we decide to keep the existing home and rent it out, or more likely sell it to fund a new purchase.

Then stockpile the cash in an interest-earning account, pour it into the loan once the fixed rate expires, then refix with the higher payments in place. Not quite as efficient but still makes a huge difference.

At the moment my on call savings account pays more interest than my mortgage charges, so it's actually more efficient to stockpile cash than to pay off the mortgage.

change your repayments the next time your 2 year re-fixes.

Or as this above scenario has the couple breaking their fix to payback the mortgage after selling the house, do that, break, refix with increase d repayments immediately.

Yes additional voluntary payments during a fixed term does depend on the bank. Westpac i know allow you to increase payments up to 20% extra at your whim. https://www.westpac.co.nz/help/how-do-i-change-my-loan-repayments-onlin…

That's a really good, practical analysis, Greg. Well done!

Agreed. Clearly identifies iow much better the property owning class have it,

Pre-2020 property mind.

The term "property ladder" is simply real estate industry propaganda. Journalists should not be proliferating it. Immediately when seeing "property ladder" it's clear that the article will not be entirely rational.

Far too much common sense 😉

Seriously and vehemently disagree!

Your first dwelling purchase will never be your 'forever home' (unless mum and dad are helping out with huge sums!)

Far better to limit what you buy so that the mortgage is less than 15 years. And then rinse and repeat. Long mortgages are wealth killers!

I don't have much time for the RE industry either. But when the market is really slow they earn their money. When the market is frothy, or normal, I've sold privately and skipped enriching them. More work, and you need to learn how it works (especially the legal side), but I doubt an agent would have done better, and agents I know have confirmed this.

Agree. The first rung is ok. Paying a mortgage sucks so if you can make do with your first house and pay the mortgage off then you have a few decades to invest somewhere else, or spend and enjoy life a bit more.

So what you're saying is that ...

1) current RBNZ policy (DTIs, LVT, etc.) and,

2) government policy (mainly tax) and,

3) local government policy (restricting densities)

... combine to screw the younger generations into years of enriching landlords before they can experience this wonderfully affordable world of "moving up the property ladder"?

Shouldn't we collectively hang our heads in shame?

95% of FHB can only afford townhouse or apartment,

so let's say they bought one, how do they move to a real house with land if the difference between them might reach .5 or 1 million, ah?!

People who want to share their religious views with you almost never want you to share yours with them.

~ Dave Barry

Great quote that one Interest team. Just what you need after traversing the comments 🙏

Agreed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.