Residential property values continued to gently rise and fall through the first quarter of this year, with a glut of listings and dearth of sales in much of the country, according to Quotable Value (QV).

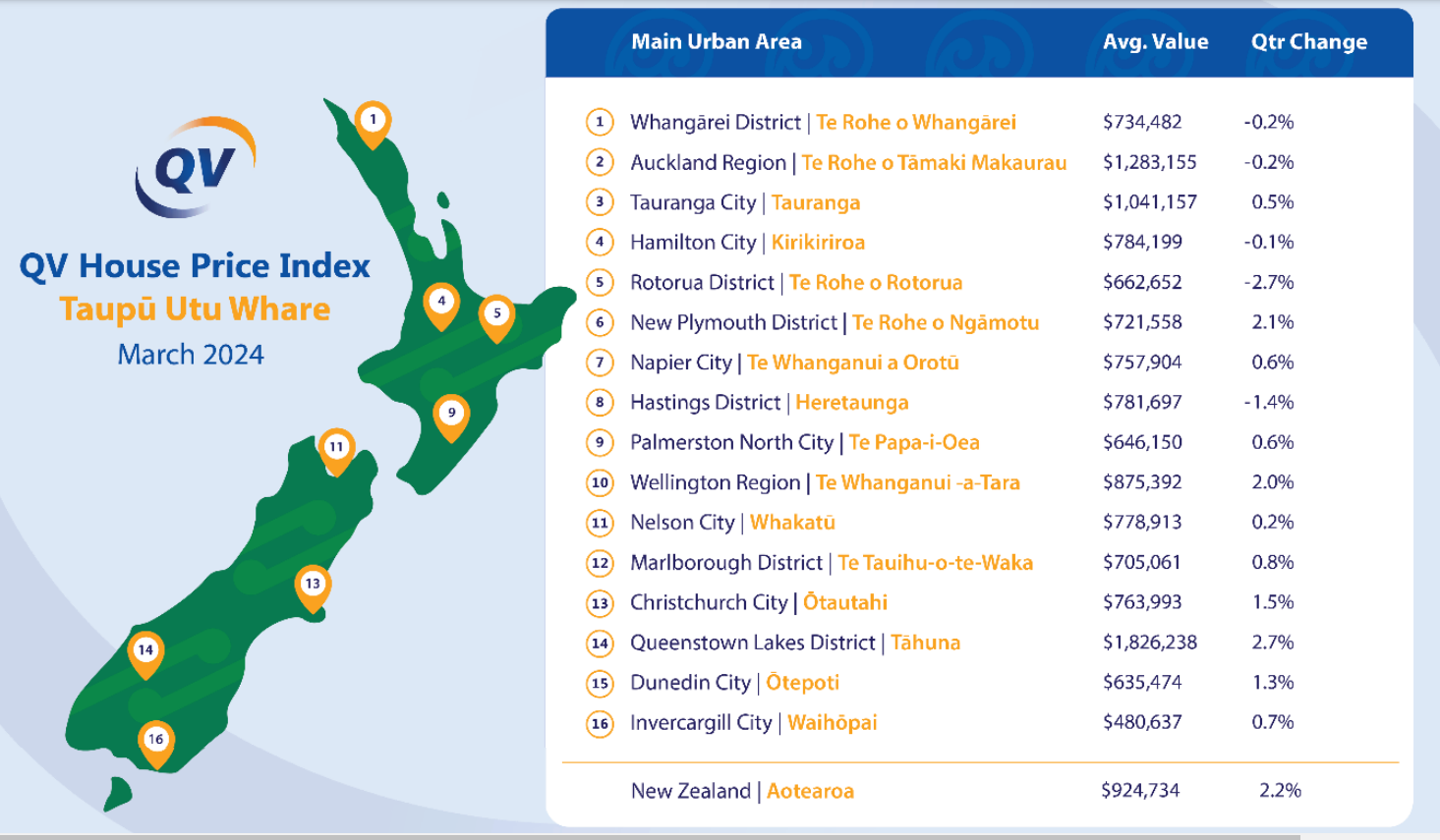

The average value of New Zealand homes increased by 2.2% to $924,734 over the three months to the end of March, according to QV's latest House Price Index figures.

That puts the national average dwelling value 1.9% higher than it was a year earlier, but still 13.1% below the market peak in late 2021.

Of the main urban areas, Queenstown had the greatest quarterly value growth at 2.7%, followed by Wellington at 2% and Christchurch at 1.5%. However, all three centres recorded less growth in the three months to March than they did in the three months to February, suggesting the rate of growth in those centres is slowing.

Auckland's average dwelling value is already in decline, dropping by a modest -0.2% over the three months to March, following a -0.1% decline in the three months to February.

Also posting declines in average values over the three months to March were Whangarei -0.2%, Hamilton -0.1%, Rotorua -2.7% and Hastings -1.4%, with all other districts posting increases in average values - see the chart below for the regional figures.

QV Operations Manager James Wilson described the housing market so far this year as "flat."

"We're seeing only modest movement across the nation, mostly up but some down, which is a fair reflection of a housing market that is continuing to find its footing again amidst some pretty strong economic headwinds," Wilson said.

"Although the pendulum has clearly swung in favour of prospective purchasers, with a relatively large number of properties on the market today giving them plenty of choice and helping to maintain downward pressure on prices overall, interest rates and credit constraints are continuing to make life difficult for everyone," he said.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

90 Comments

Flat...with a touch of flatulence like noise as air escapes the bubble.

For evidence of hot air, read the comments thread...

For evidence of hot air read your comments? It's a mix of hot air and laughing gas

I own three houses in a stagnant market. If I don't laugh I'd cry.

Ummm, don't you mean the bank owns them?

Wellington doing well in the face of public sector job cuts. I'm surprised by that.

That's because the public service has actually expanded over the past 6 months despite the culling. There's a paywalled article on the Herald site about it if you're a subscriber.

I've seen this happen time and again in Wellington. Under National the PS cut permanent staff but hire contractors and consultants, while under Labour they take on FTE. That's why the Wellington rental market has always been seen as a steady earner.

that's because Wellington has gone through a bigger drop in past 2 years, and Wellington household incomes are still in good shape.

It’s never going to turn around, is it? NZ property is done.

A lengthy recession with 7%+ unemployment will put paid to that.

Not 'never' just a prolonged period of price falls but cyclical nature of economies and human nature means in 3 - 10 years this will be forgotten and fomo will be back with 10%+ annual gains.

In the meantime positive immigration and lack of new builds will keep rents up...

Better to invest elsewhere for a while.. but looks like property investment in the long term will be OK.

LOL ... Sorry. I can't be bothered listing all the reasons that I have already listed to say how wrong you'll be. If you'd said 20+ years I may have nodded in agreement. And for Akl? Maybe 30+

It would be a good outcome if it is 20 years.. 30 even better.

The prob in nz seems to be noone in power has any better ideas for the economy and investment than property... so as soon as people forget the bust and the number of new houses starts to drop... off we go again.

I live in hope that someone (7houseluxon? Seymour?) actually drives a change and finds a way to grow other parts of the economy.

Yes, even the so-called party of business is only a party for property speculation. 'Tis a dismal state of affairs.

Seems extremely unlikely. NZ has nothing of especially high value to offer. Just a rule of law and a few pretty views. But many places have that now.

With populations flattening out or collapsing around the world, it’s hard to see property prices outrunning incomes any longer.

So in other words it's going backwards, considering all the costs involved..

Pain is yet to come..

Great news for those saving to buy their first homes. Those boomers out there who cannot cope with this kind of news. Get over it. Think about your children and grandchildren and their need for housing. Some good news for you. Maybe you might not need to give them so much money to help them build up their deposits.

Grandchildren???

The children are too busy, both working to pay the mortgage, to have grandchildren.

Those that already own. But that's their error.

The smart ones are in Aus or UK earning real money... ready to come back and buy houses when prices are low... and the NZD falls a bit further.

Always winners and losers.

Who's earning real money in the UK? Wages there have been going backwards for a decade

Yes that is not ideal. My wife never worked full tim as she did not need to. My worst loan was 3 times my income. Paid off in three years before the children arrived. We were the lucky generation.

Great news - not quite as house prices are still to high c.f. incomes. When house prices in pissy little provincial towns in NZ still exceed $1 million we have a way to go yet. The price shock and decline needs to continue for some time yet before people understand that house prices can go down

Rents need to be next - I for one am tired of giving employees pay rises only to hear that their rent has gone up and they are no better off

Luxon owns 7 houses and now he controls tax and accommodation allowances.. can't see rents dropping anytime soon.

Rents will rise above the inflation rate for the next few years.

You forgot to up vote yourself.

Thanks averageman - that made me chuckle :)

Why are rising house prices "great news for those saving to buy their first homes" Ex agent ?

The average value of New Zealand homes increased by 2.2% to $924,734 over the three months to the end of March, according to QV's latest House Price Index figures.

Including +2.2% in Jan. Draw your own conclusions.

Interesting to see house prices trajectory vs inflation for last couple years

The real story is in what hasn’t sold. Around me there are a lot starting to back up… some have been to market 3 times with a different agent and are still sitting there.

Examples of vendors being stuck in the mud.. their ability for lateral thinking is inhibited

Yes, I know of similar houses re-listing multiple times too. It's just surprising that this hasn't resulted in overall price drops. (Perhaps not yet, but then again, how long have we now said the drop is imminent?)

Same here (The Tron). Even the agents are telling us there's a lot to chose from at the moment. I'm about to throw an offer on a house, I've done the maths, there's not much for us to gain if the market remains stagnant. At the same time thinking it could be even more favorable for us in 3 or 4 months if prices drop again.

Just waiting for wingman to chirp in any second now...

No doubt he will be thinking of something to polish up the news with. Otherwise his whole world will collapse.

Get real Ex agent. Just above you have "polished the news" as you say, in a way that suits you. You made it sound as if house values were dropping when the article actually states that: "The average value of New Zealand homes increased by 2.2% to $924,734 over the three months to the end of March"

See my comment above: +2.2% in Jan, 0% in Feb, -0.1% in Mar (error due to rounding, changes are expressed with a single digit after the decimal point).

QV does not publish monthly figures, but quarterly data. So the 2.2% you're referring to for the Jan data is for Nov, Dec & Jan.

Anyway, my point stands, why is it good news(as Ex agent says) when the latest quarterly prices are UP?

They absolutely publish monthly figures:

Scroll down and place the cursor on the graph for the desired month.

Feb 24 quarterly change was 1.3% = -1.0 (Dec 23) + 2.2 (Jan 24) + 0.0 (Feb 24)

(Again rounding error)

Comprendo?

You really don't know what you're talking about to post such comment.

Maybe you want to look at yourself first, before accusing others of not understanding. You write yourself:

Feb 24 quarterly change....

Quarterly, meaning not a monthly figure, which is precisely my point.

You have issues.

They publish both quarterly and monthly data and my example clearly shows that: Feb 24 quaterly change is calculated from Dec 23, Jan 24 and Feb 24 monthly changes (again, available on the graph).

The report says the market is flat Yvil. That is great news for those entering the market as prices are not running away from them as it did in the past. I suspect it might turn downwards over winter as the listings have certainly increased. I suggest since you are a boomer you have that blanky handy during winter as I suspect you will need it.

The average value of New Zealand homes increased by 2.2% to $924,734 over the three months to the end of March

That's what the latest numbers say Ex, but you believe what you want, ok.

QV’s operation manager describes the market as being flat so far this year. In Auckland our biggest market it is down. Probably because the listings have increased a lot. Winter will be tough for vendors especially those who need to sell and at a price greater than the market is willing to pay.

Is that in line with inflation, above or below?

I'm still here, been very busy with my new build. You know what they say, buy in gloom, sell in boom.

Winger is bound to chip in soon, sure as Eggs. He will opine how his backwoods area of Auckland is only going up like a rocketship and "what crash" are we all seeing in the official stats??

Fact: Auckland back 40% and WellingTank is back 48% in REAL TERMs. Real crashectomyland there!

As the confidence in the property market is now torn to pieces and people see their deposits disappear into negative equityland, another suckerpunch is coming down the pipe, of another -10 to -15% set to peel off the nearly spooled housing reel, in the next year ....

Auckland back 40% and WellingTank is back 48% in REAL TERMs

...since the bubble peak. Cherry picking for effect is fun but context is important for constructive discussion. I have genuine sympathy for OOs who bought during the bubble. They were well and truly sucked in by the narrative and its going to be years before they are back where they started.

Yep fair call all round. Yes from 2021/22 peak.

Its still an epic, sickening Real decline, not matched since the 1970's.

By any measure, its not done yet.

Now that the market is going nowhere at the moment, it would be a good time to have more real in-depth analysis and what that could mean going forward.

For example how about looking at housing cost inputs as weighted averages?

On one hand, we have non-valued added inputs like speculative rentier capital gain, and some council and supplier costs, which while not increasing at the moment (and may not again) still make up to 1/3 the cost of inputs, and thus is available for removal with the right policies.

The counter to that are the value-added costs, like building code improvements, housing typology, and size to a point, that add real cost but also real value.

These two types of inputs (and there are many of them) give us a plus & minus add to get a total value.

Add to that a general rate of inflation, plus wage growth, lending policies etc, then we can start having a more intelligent conversation about what the value vs price of a house is and whether it is truly 'affordable.'

I'm still sticking to my 3 to 4% gains this year. The rest of the world is turning to shit and I'm awaiting the first ever migrant ship to arrive here and that will be a lightbulb moment for most punters on here.

Hoping for the worst to preserve your self interests? What a mentality!

The world is what it is, adapt or die.

Or choose your parents wisely.

I’m predicting the same but only for the South Island as more and more families in the North Island relocate to the south.

Has been happening since the great price hikes of 2020. More are realising there's more to life than traffic and restaurant choices, it;s been good to get some fresh perspectives in the south to mix things up.

I'm seeing a lot of listings with, 'owners moving to Oz' in the headline..

They would need a very stout ship and good seaman ship, as sailing down here is far easier said than done due to the sea state and distance.

But good luck.

It amuses me when people say its hard to sail to NZ, when both the Maori's and the original British traders and settlers got here without any problems. If you can sail from Hawaii or England, you can sail here from Indonesia.

Most people only listen to msms messaging on housing. So many people I know still believe property is racing away.

It's when the bbq/taxi driver/shoe shine boy narrative sifts to the negative that things will really unwind.

We are not there yet.

so.. what will see when get to the Capitulation phase? a few guesses:

1. Mainstream media (despite their Advertisers) with multiple horror stories with quotes like "buying a house is a stupid idea - I don't know what we were thinking!"

2. multiple "advisors" telling people that the best place for people to put their money is the bank, term deposits, crypto, gold, classic cars, art, foreign currencies, equities.. basically anything but housing.

3. multiple more builders / developers going horribly broke

4. multiple stories showing "analysis" of how much money people really lost (eg -35% on the house, -$100k on the reno, -$30k on agents' fees and -$120k on inflation)

5. multiple headlines of house prices "crashing", a la early 2023 but bigger / worse.

I'm only see a little bit of 1 and 2 so far. Maybe I just need to be more patient. I try to take the opposing view - i really do - but the arithmetic is always too compelling.

People who align the property market directly with speculative investment assets/commodities miss the biggest single factor which makes them different.

80% of the property market, buyers and sellers, are NOT investors/speculators. They are mostly people who own a house to live in and are "upgrading" so buying in the same market, this churn doesn't stop. The others are first home buyers, a fairly small % of total sales. This is what underwrites the market and makes property "safe".

Now, in real bubbles seen in stocks you get to the worse phase "capitulation" and owners of the stocks dump them (they never needed them as they do a roof over their heads), they all sell up at once and buyers run scared, so they all sell into an empty buyers pool making for a crash.

Do you really think the 80% of home owners are going to sell up and go renting instead, when theirs nothing to rent and rents are climbing fast? The market is too heavily dominated by actual home owners living in their own homes, so we will never see capitulation in NZ property as seen in bubbles of other asset classes.

Ireland property was close, but their house prices are already back past old pre GFC peeks - theirs was caused by Polish immigrants imported to over build houses, so too much property already, then they all left so a decline in population, and GFC killing lending, fairly rare situation and one NZ can't be compared to as we already have too few houses, and rapidly growing population.

Yeah nah

Property valuations aren’t set by the 80% of households or houses that are not listed - they are set by the 2% that are selling, or trying to sell.

The same happens in any market. Recent sales set prices and expectations. Up and down.

If that doesn’t make sense ask yourself why valuations have fallen 10-25%+ in nominal terms (depending on your area etc) over the last couple of years when only around 2% of total housing stock is for sale at any one time.

Re: Ireland - I agree - hard to compare as always differing factors but a couple of interesting insights:

Their crash was over a six-year period from 2006-2012. It never happens overnight like stocks. Houses are ‘safe' from overnight falls simply because they are hard to liquidate.

Their falls started when rates rose from around circa 3% to 6% from 2006-2009.

See Figure 2 chart:

https://www.centralbank.ie/news/article/blog-monetary-policy-and-intere…

Rates were slashed back to circa 3% in 2009 and for a 6-month period property started rising again, but then resumed the falls.

See Ireland HPI Chart:

https://www.macrobusiness.com.au/2013/04/ireland-the-greatest-property-…

As is the case with most housing bubbles, Ireland’s was fuelled by a number of inter-related drivers: easy credit, speculation, and unresponsive supply.

Sounds familiar?

Always hard to compare house price crashes in different countries, but if the world's biggest economy (the US) can have one, this tin pot nation that is so dependent on its housing market (and wealth/credit creation) certainly can.

Don’t be fooled that because you’re not reading about it in the vested MSM it’s not happening here.

Mortgage borrowers have different expiry dates for their expiry of their fixed interest rate. They become cashflow stressed at different times.

Mortgage borrowers will also draw on additional cash resources to maintain mortgage payments such as cash balances, existing lines of credit, other assets which can be sold - holiday home, assets not used, Kiwisaver

Mortgage borrowers will get some hardship relief from lenders which can buy time.

At some point the cashflow stress can become unsustainable.

What will the lenders do?

80% of the property market, buyers and sellers, are NOT investors/speculators

This overlooks the fact that the housing market has made speculators out of just about all recent (~20 years) buyers.

Ask yourself this: who would have paid these prices if not for the expectation of capital gains (aka the magical retirement fund)? Of those that can honestly say they bought without any expectation of gains, I would just say two things. They are probably financially secure enough not to need them, and/or they probably resent paying speculative prices for something they only value for it's utility and as a store of wealth.

Watch this space. If the 'speculative premium' priced into houses is removed by changing expectations around capital gains the next step in this crash will get underway. It could get much uglier than many expect.

good points. but there is SO much new stock.. I ask the agents.. why? downsizing, moving to Australia (a lot). they all seem to think they can get last year’s price.. or even 2021’s… soon they’ll be wishing they had taken 2017’s…

Ireland property ... can't be compared to as we already have too few houses

That's what they thought before stuff hit the fan.

I am confused how the average increase for the country is 2.2%, yet the only region that exceeded 2.1% was Queenstown, whereas the bulk of locations were well below this, including Auckland at -0.2% which has the majority of homes and sales. Is QV really saying that Queenstown has that much of an impact on the national average?

The QV website it shows the 1 month drop as -0.1% to $924,734 on 1 Mar 2024.

But for 3 months it went from $905,070 to $924,734 which is 2.2%

Can we stop blaming Boomers now?

"Gone are the days of millennials opting for avocado toast over homeownership, with new research revealing younger Australians are investing in residential property at higher rates than their baby boomer parents.

Millennials and Gen Z made up more than half (53 per cent) of all new property investment purchases last year, according to Commonwealth Bank data, taking advantage of rising property prices and strong rental yields.

The typical property investor is now 43 years old and looking to spend just over $500,000 and, interestingly, a significant proportion of millennial property investors are choosing to buy property alone.

“We can see almost one-third of all millennial property investors actually purchased their investment property on their own,” Commonwealth Bank executive general manager of home buying Michael Baumann said.

https://www.theaustralian.com.au/business/property/millennials-have-bec…

Yeah but remember, apparently all the "Smart ones" have already left New Zealand for Australia. All we are left with in NZ are the DGM group therapy sessions here every day.

You seem a little upset, has Australia already refused you entry?

Most people got off the boat in 1974 in Australia, not too may continued to sail for New Zealand. I do wonder how life would have been if we had stayed in the UK or got off in Australia, I suspect it would have worked out okay regardless.

Australia = higher wages, locations not requiring so much insulation hence less materials, and bigger economies of scale for building materials. They have had their own FOMO going on with the FHB market and the rents aren't great in the major centres right now either. Get in quick, you can't lose! LOL

Because facts speak louder than words ...

- Gross house prices are still declining in inflation adjusted terms,

- And falling further as inflation adjusted maintenance costs are included,

- And falling further when inflation driven rates, insurance, etc. are factored in

So no crash then...as predicted here hundreds of times?

Surprised you are still here mate, you must be a sucker for punishment.

Its dryer here then his flood plane? see head of insurance council already said you will not get insirance in a floodplane

There he is

How would you define this thing that hasn't and isn't happening?

"So no crash then...as predicted here hundreds of times?"

Not sure what data you're looking at.

FYI,

1) median sale price was $1,707,010 in July 2022

2) current median sale price $1,252,358

That is a 26.6% FALL in the median sale price from the peak. (before the impact of leverage. Those who had a 20% deposit and purchased at the peak are now likely to be in negative equity with over 100% loss of their savings used as their deposit)

Riverhead market insights for the last 12 months - realestate.co.nz

Even more for those that could flood

Have a look at the suburb trend graph. Yellow line, May 2023. Pretty sure that's when Wingman bought.

Then August/September and November/December 2023 must be when he started his bleating on Interest.co.

Poor old Winger, the facts show the Asking Price out there.....they expect moonbeams for some soggy, thistle patch out in the wops.

But the reality of the Selling Price, is a REAL Expanding crash, worse than what Auckland proper is seeing atm in this biggest overall crash since the 1970s.

No matter how much he flaps his wings and chops......he and the other selfish vested interest spruikers, just cannot reanimate this Staggering Rhino - dying Ponzi.

My neighbour just sold for $300k over CV, you guys are dreaming. Crash...hahaha.

Charts are showing property prices starting to tick back up, so anyone who bought recently is in clover. I've broken ground on my next project in Riverhead, where everything's selling.

Too bad you guys aren't in on the fun, but I guess risk isn't for everyone. Lots of immigration, less building, more red tape, less subdivision......what's that mean folks?

"I've broken ground on my next project in Riverhead, where everything's selling.

Too bad you guys aren't in on the fun, but I guess risk isn't for everyone. "

The assumption being made is that everyone wants to become property developers, or should become property developers to become financially independent. Those assumptions are untrue. If everyone became a property developer, there wouldn’t be doctors, nurses, social workers, police, ambulance workers, super market employees, truck drivers, wharf workers, gas station attendants, teachers (i.e. essential workers). Society wouldn't be functioning. Think of the 2020 period and the essential workers who kept the country going.

Good for you that you're building housing, which is entirely motivated by profit. If the project was not financially viable, developers wouldn't be going ahead with the project.

As a property developer, you're in a very different position to that of an owner occupier buyer. The economics are very different. Most people are speaking from the perspective of an owner occupier buyer whose main objective is buying residential property for shelter and buying at the median house price, whilst you're a property developer who is in the business of making profits from selling residential property with an entirely different cost basis.

I couldn't call myself a developer, a tinkerer more like it. It's a hobby.

I like property, it's interesting, fun and mostly profitable if it's done right. I build houses for myself every now and then, and I've renovated many. There's not many people going to buy property if there's the prospect of losing money. And sometimes it can be substantial amounts.

"There's not many people going to buy property if there's the prospect of losing money"

Yes, that is how the current system works in NZ.

That's how capitalism works. Some people make bad mistakes, some people are so disorganised and incompetent that there's always going to be casualties, it's just a fact of life.

There's lots of people out there that make life hard for themselves.

I saw a guy whining the other day about how hard life is. He's a lower order sharemilker aged 21 with 4 kids......HELLO!!!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.