Residential auction activity is definitely on the wane, as the housing market moves further away from the peak summer season and into the slower autumn/winter months.

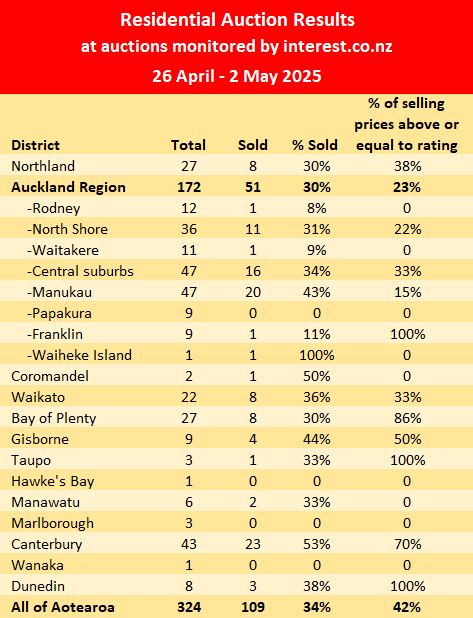

Over the week of 26 April to 2 May, interest.co.nz monitored the auctions of 324 residential properties around the country.

Although that was up from 196 the previous week, that week's results were particularly low because it was a three day week wedged in between the Easter and Anzac long weekends.

At the beginning of April, interest.co.nz was monitoring the auctions of more than 500 properties a week, so auction activity has declined by about 40% since then.

Of the 324 properties offered at the latest auctions, 109 sold under the hammer, giving an overall sales rate of 34%.

The sales rate has also been in a slow decline from about 37% in March.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The table below shows the latest regional results.

The comment stream on this story is now closed.

24 Comments

% sold looking incredibly dire......keep it going!

Almost as dire as comments here.

Musta been a rough Saturday morning for some, without unleashing a few capitals laden Ponzi diatribes

Interested in the mid month numbers auctions are a waste of time in winter

Yep. Though the ponzi protection squad is throwing smoke. Truth is increasing apparent.

🍿

Canterbury does look better than the rest, just over half sold.

Repeating my comment from a couple of days ago:

I follow the Christchurch residential market regularly, with a medium term interest in eventual relocation.

Last year I saw a definite listing pattern play out regularly over several months: Deadline sale/Closed Tender > Auction > Offers above > Fixed price

This year the big brand agencies (eg Harcourts, Bayleys) seem to increasingly be going straight to auctions.

Not sure what this really indicates: possibly resetting vendor reality early to avoid wasting agency time? ChCh prices started from a lower base in the 2021 inflation & haven't dropped back as AKL & WLG, my impression is that ChCh sale prices have also firmed up over this year (for standalone 3+brm 2 bath double garage in the NW, there remain multitudes of unsold apartments across town).

I'm interested in any comments from anyone knows the ChCh market well?

I've been following the ChCh market for almost a year, relocated in December and bought in April.

There seems to be a very keen understanding of value here. Value is made up of some variables that are stronger here than elsewhere - school zone, proximity to Hagley Park (or lower slopes), new build versus pre-quake concrete slab. You are unlikely to get a bargain.

People are ignoring the risk of natural hazards in areas such as Fendalton, Merivale and St Albans - while the same valid issues have killed the market towards the east coast (it's about maintaining the values). I would avoid the whole former swamp areas.

They're building a whole new city around Rolleston. The infrastructure isn't keeping up. This week the floods left only one road open to the southwest.

The macro numbers are misleading. Yes, there's a lot on the market, but much of it is junk (or it goes away and comes back again). Those monolithic clad leaky homes are an issue still. Places that are knackered but no-one's looking, as is where is still a thing.

Thanks very much for your comments.

What % of the for sale market is solid vs what you call junk/leaky/knackered/swampsville ?

You’d have to look area by area to be accurate - the worst locations are obvious because the old stock is either gone or nothing’s been done to maintain/ improve it. Having said that, there are many places in and around Merivale (all TC2 land) where big money has been spent to put things right because location location (but things will get smashed up again in just the same way if there’s another quake).

But overall … roughly 20% avoid (older places never fixed up/modernised or flood-prone) plus another 20% made up of cheaply constructed new build townhouses and units subdivided to an extreme and that won’t age well. It’s no longer the garden city in terms of private yards (public parks are great though).

Unlike say Wellington, there is a clear price differential between unimproved older places (eg. single glazing, old kitchens and bathrooms) and well-built new homes or well modernised older homes. A premium for peace of mind that you’re not buying a problem.

Relatively good value (less pricey) where the land gets more stable, out west from Burnside/ Bryndwyr onwards and also southwards around Sydenham. Esp if well zoned for schools.

WGTN has always got nuts money for shitty old wooden buildings, the typical restoration of a Ponsonby villa with a pool, decking etc, is rarely found in WGTN. Its no surprise to me that it has been hit hard with CV changes.

Even here in AKL there is a huge pool of old shitter houses that are only land value. The right to build three townhouses on any site was/is a way out I guess, but if they open more land up as seems to be happening, they are stuck at land value only.

Auckland landlords seem reluctant to spend any $$ on maintenance.

Wayne Brown & National nimbys now getting cold feet on infill development

https://www.stuff.co.nz/nz-news/360675153/wayne-brown-doing-deal-chris-…

so not even land value (assuming rebuild options)

oh dear

I agree. Unreasonable for a home owner who maintained or upgraded a home for many years in a stable suburban suburb to be suddenly expected to accept 3 story properties all around.

One reason (not the major) I sold in town was the likelihood my home would suffer such a fate. Made improving such as a double glaze, new heat systems, roof etc to much of a risk. Would have been dead money.

Its obvious the market is going to keep tanking

Well yeah, overall economic outlook doesn't look great, and real estate is tied to that.

Its obvious the market should keep tanking....whether it does or not depenends upon how much how many have to risk and whether they (and the banks) are prepared to accept that risk....ultimately however reality will prevail

Keynes had something to say about irrational markets

If FLP is not renewed as mortgages role off that heap cany crack, banks will be taking more risk. Their model is min risk for max profit and profit do they make.

So expect more specu mortgagee sales.

Isn't expecting specuvestor fire sales your default position?

Well yeah, overall economic outlook doesn't look great, and real estate is tied to that.

Hasent stacked up for years, except for specu exploitation gamble. Reading above, you support that position.

I think the market outlook doesn't support big upswings anytime soon

You've thought there's this cadre of close to the wire specuvestors who are about to buckle for years, that hasn't materialized

So clearly, the market stacks up different to your expectations

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.”

Lets check some Trademe numbers... Mortgagee x 62, Must sell x 895 (bank threatening not unlikely), Moving Overseas x 40, Overseas owner x 207. Lets say they all sell for -25% cv or there about's, not unlikely in the current market. More than enough to shift the Banks and valuation portal algorithms.

Those that bought years ago and have little to no debt will yawn. But they are not the leverage monkey market.

Well the banks may just lower what they are prepared to lend to the next specu buyer....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.