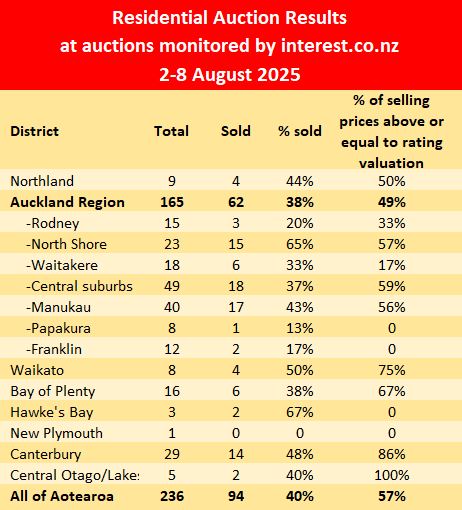

Things were a bit quieter at the latest auctions, with interest.co.nz monitoring the auctions of 236 residential properties around the country over the week of 2-8 August.

That was down from 282 the previous week and was the fourth lowest number of properties offered at the auctions we monitor so far this year.

However, although fewer properties were on offer, there was no change to the sales rate, with 94 properties selling under the hammer, giving an overall sales rate of 40%, which was unchanged from the previous week and within a percentage point or two of where it's been for the last two months.

So overall, things were quiet in the auction rooms, but about where you'd expect them to be for the time of year.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

29 Comments

40 percent. Does life begin at 40, some say it does, I say it is downhill from there

NZ ME say its set to take off, when is launch?

For Dr Yvil, the launch is already cruising and he's there with his party of one. For vendors, they’re just wanting to stay afloat so yes NZMEs right, its set to take off as vendors take off thousands off the listing price

Stuff / Herald is full of job and cost of living doom today, no doubt true for those impacted. Its turning to a winter of discontent for NAct, but looking at photos of Hippie surrounded by loser caucus, on an offsite, all hope disappears. They seems to be no one with viable alternative policy solutions.

Its easy to say that CG Tax or tax reform in general will turn us around, but these are slow burn solutions, we also need something to stimulate investment (outside housing) and job generation.

What will the Greens do after they've taken all of the other people's money ?

Oh they will be voted out after a single term as well,

no one has a viable plan which can replace the collapse of the Property Ponzi's credit creation engine. But people want to vote for hope, and NAct seem to have spent the entire term firing and cutting and saying a turn around is, just around the corner. They need to pump.... more.

It is traditional that the money flows just before an election, though I think for NAct it would be wise to start NOW. People want to see evidence of a plan, not proof its successful before the next election. If things are significantly worse by Xmas NAct are in real trouble.

"The entire term" haha is basically 20 months so far, and Nact have been busy and effective in my view. Its ridiculous that the first two months are for writing up the coalition agreement followed by another six weeks holiday if they want it

Off topic for housing but NZ govts need to have a 4 year first term to get underway, then 3 years after that.

Nact have been busy and effective in my view

I know many who have bailed from Wellington to Australia and more planning to currently. Jobs going everywhere with no end in sight for further rounds of job losses. With mounting pension and healthcare costs imminent, I see no economic plan from National to help address the longer term issues, and the immediate is woeful at best from observation. The current coalition are continuing the theatrical scale for politicians, and will likely be voted out as their voter base voted for hope and change, and are not seeing any improvement to justify their votes.

Letter to Mary Holm, how many assumptions can you spot:

Q: From Peter Lewis, vice president of New Zealand Property Investors Federation:

Owning residential property in retirement remains a smart and resilient strategy, especially in the face of inflation and uncertain financial markets, and the reality that retirement can now last for more than 30 years.

A 4% annual return on a substantial sum deposited back in 1995 won’t go very far in paying your council rates today.

Unlike term deposits, which offer fixed returns that lose value over time, rental property provides both income and capital growth. Property values in places like Auckland have consistently outpaced inflation, and rental income typically increases over the years, especially as housing demand will, in time, continue to rise.

While term deposits gradually deplete, property preserves capital. Selling may seem practical, but once the money is spent, it’s gone. Retaining the property provides a steady income stream while keeping your financial base intact, a crucial advantage for those concerned about longevity or wanting to leave an inheritance.

Property also offers flexibility. Retirees can sell when the market is favourable, downsize, or tap into equity if needed. In contrast, fixed-term investments lock up funds and offer little adaptability.

Importantly, owning property gives retirees control. It’s a tangible, familiar asset not subject to the same volatility or institutional risks as many financial products.

In summary, residential property delivers inflation protection, income growth, security and legacy value, all vital advantages that cash-based investments can’t reliably provide

Almost everything we do is based on assumptions.

Property Investment lacks the liquidity that other investments often provide to older peoples rapidly changing requirements. This is a harsh reality, things can turn on a dime at 72. Perhaps better to be in managed funds that offer easy entry/exit?

Sure things are different if you are 25. Even commercial real estate investments at fund level can turn off your ability to exit during financial crisis and Covid etc. A product disclosure statement is available on request.

IMHO Rentals stopped being great investments about 2012, since then its been a simple Ponzi based on capital gains. The yields are not there to cover maintenance etc, no more Negative gearing against other income etc etc, rates and insurance are going up, rents are flat to failing, not keeping up with rates and insurance. Without interest deductability its a busted flush.

The trouble is the values are now so far away from yield based investment viability , that repricing to that level would cause our banks considerable issues. Thus we slowly fall, very few investors are buying to hold at these levels, rather a few buying to develop, which is still likely to be viable IF you buy well, build cheap and manage to sell quickly.

Its a lost 2 decades just like Japan has had and China is entering, the alternative is not spoken as it will cause even more harm, a sudden price correction.

Its a real mess, any experienced property investor with decent portfolio is being blocked by DTI. Its a sticking slowly decaying (due to lack of maintenance, mess. The only hope is FHBers but they are leaving for Aussie.

For sure. I wouldn't recommend property for retirees if they don't have other, more liquid, investments as well. I've just been thinking about assumptions lately, more in relation to PDK's statements. We assume a lot but we have to really. We assume we will find a way we don't currently have, like an act of faith, but it is human, and has proven to be fairly reliable.

You are somewhat correct, its clear on any metric that the S&P500 is at stretched valued against current forecast EPS, it can stay that way a long time before it corrects.

NZ property continued from 2012 to 2021 helped by QE after the GFC and then Covid low interest rates, but sooner or later all markets face their Minsky moment.

A Minsky Moment is a sudden collapse of the market following a long period of unsustainable speculative activity involving high debt amounts taken by investors.

We are well past the moment in end 2021 where buyers simply lost faith that they could buy and sell for more soon after.

We are back to yield based hard spreadsheets. And the numbers simply do not add up.

Sure you may have the religion that its worth "topping" up a losing rental investment now so you can ride capital gains later (Classic Property apprentice religion). But what happens if we have a lost decade or 2 from here? prices will only be where they are now and all you have done is enrich the bank and debt markets.

Buying at these price levels and these high inflation expenses and low rents with no real path higher, is actually gambling on house price increases later.

You may as well buy the ASX, at 24% banks allocation they win if its a lost decade (thankyou gormless top em uppers, win if capital gains occur... ) You could trade on margin if you wished.

You may as well buy the ASX, at 24% banks allocation they win if its a lost decade

You would have been better of buying only CBA. Nothing else. It's a shining beacon of what the Aussie Ponzi has achieved.

Yes and when it turns the shorts are going to pay big time.... but you need big kahoolies

will it get past 185 again?

Letter to Mary Holm, how many assumptions can you spot:

Reasonable argument on the surface. But what the VP fails to point out is the mechanism by what inflation exists. He talks about inflation as it's some kind of independent entity, however what he doesn't do is illustrate how the Ponzi is the single biggest driver of inflation - money supply expansion through mortgage issuance. It's ridiculous to suggest that the Ponzi, money supply, and the inflation construct are all independent of each other - they're interdependent. Unfortunately you're unlikely to hear this at the BBQs, water coolers, classrooms, lecture theaters of Aotearoa.

So while the VP of New Zealand Property Investors Federation is not wrong, he needs to realize that without inflation (in how it's been generated since the mid-90s in particular), the Ponzi is not necessarily the gift that keeps giving. And realistically, if his vision is so simple, Aotearoa would likely just be one big property investment fund and we all live happily ever after with our magical capital gains and inflation-protected rents. For that to happen, essentially we need neo-feudalism where the serf population keeps expanding. We've done a good job at that but what Peter and Mary need to understand is that they can't keep selling the dream of 'freedom from slavery' through the Ponzi. It doesn't make sense. But like many Aotearoan thought leaders who we turn to for advice, these people are very one-dimensional and really only capable of drawing imaginary lines from the near past into the future.

Maybe the smartest thing to realize is that the next Ponzi is just starting up, Gold has a long long way to run and some very big backers.

Come back to Property once its finished falling.

Mary Holm is very much a puppet of mainstream institutional economic and financial thought. Unfortunately, the institutions rely on people behaving uniformly for their livelihood. The hard questions are never really addressed. Now, that is not to say Mary's ideas and advice are wrong - she could very well be right - however what she has said in the past about ETFs and index funds has been potentially quite damaging IMO. And part of that is related to the whole idea of what inflation is. We see greater evidence that indexes like the SPX showing returns that are quite possibly the product of monetary expansion, so people are fed the illusion that they're 'getting ahead' on these investments when in reality they're treading water or worse.

I find it amusing how property investors have increasingly become fixated on bashing term deposits as an investment - and its happened simultaneously these past few years as term deposits have outperformed housing returns (surprise...surprise...). Its almost as if investors might be threatened by the idea that at certain points in history, saving is actually superior to investment (and one drives the other).

The fear is that if people chose to hold cash in term deposits instead of investing in rentals, there will be less demand to push capital values up on the property portfolios of the members of the Property Investers Association - hence the letters like the above. Its all self-centered, vested interest, BS and propaganda.

I find it amusing how property investors have increasingly become fixated on bashing term deposits as an investment - and its happened simultaneously these past few years as term deposits have outperformed housing returns (surprise...surprise...).

The benefit of low-yielding term deposits is liquidity. To be honest, I think that 'housing as an ATM' instrument has developed quite slowly. We have all the technology to be able to handle this. But the banks probably don't want to let other solutions emerge where they don't get a piece of the action.

Banks do what makes them the most return on equity that the regulatory environment in which they operate allows.

As far as I can see, banks have a monopoly on 'housing as an ATM' - reverse mortgages, adding a cost or debt to your existing mortgage loan, etc

Over in other article it states Labour have decided on a CGT vs a wealth tax.

Just 30 years too late

Final nail in coffin of the Ponzi

cgt doesn't phase aussies, nsw nearly $2m median

If chippie brings in a cgt he will personally become the biggest promoter of house price gains and investor house flipping. As he will want his policy to be a winner and bring home the bacon so to speak. Labour will pump the ponzi

The other concern being if it is not backdated then what good will it do if there is not much in the way of capital gains to access?

Exactly. Also if you don't sell, you don't pay. Lots of issues and work around. Lets face it, Prop Investors are very focused tax avoidance and minimisation so they will find a way in mass to sidestep any tax.

All highlights why a land tax paid annually is the way forward.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.