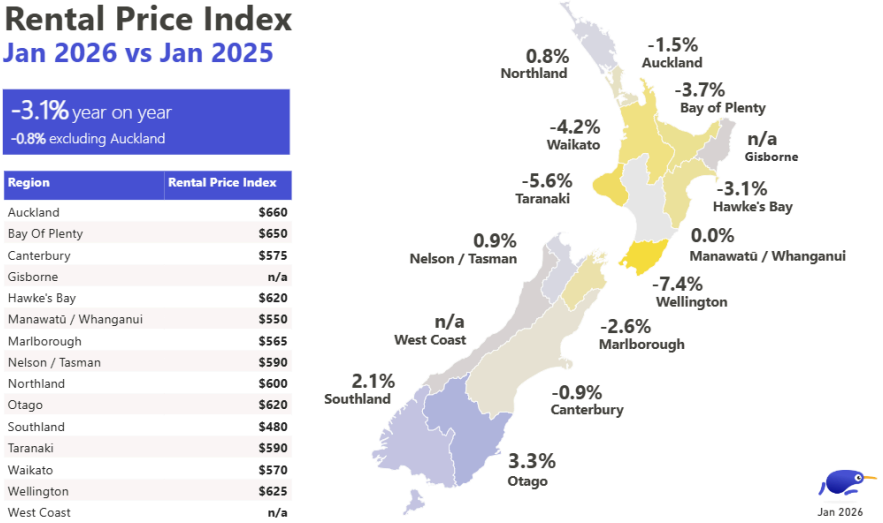

Advertised housing rents were down 3.1% overall in January compared to a year earlier, according to Trade Me Property.

The national median asking rent for residential rental properties advertised on the website was $620 a week in January, unchanged from December last year, but down $20 a week (-3.1%) compared to January last year.

The five main urban regions - Auckland, Waikato, Bay of Plenty, Wellington and Canterbury, plus Hawke's Bay, Taranaki and Marlborough, all posted annual declines in their median rents. Northland, Nelson/Tasman and Otago, posted annual declines. See the chart below for the full regional figures.

The biggest annual decline was in the Wellington region, where the median advertised rent was down $50 a week (-7.4%) in January compared to a year earlier.

"Nationally we saw tenant demand spike by 41% compared with December, but this was met with a 45% surge in the number of properties for rent," Trade Me property spokesperson Casey Wylde said.

"This balance between supply and demand is a major contributor to the current pricing stability," she said.

The comment stream on this article is now closed.

22 Comments

Ohhhhh dear.

Landlorders will be loving this.

Falling rents, as all costs increase markedly. Winning.

Now also the spectre of higher embedded inflation and the higher mortgage rates, that then must be applied, in the near future.

The next 10 years of aging boomers selling up, will bring lower and lower profits, as the pressure cooker selling pressure increases.

Leveraged landlorders will need very long snorkels, as many thousands will be further underwater and needing many hundreds a week to topup, the worst timed speculative bets in NZs economic history, thats gone very lemon sour.......

Actually interest costs have dropped over the last couple of years. Significantly.

And they're still on the way down as a large proportion of investors have interest rates locked in, not yet at the bottom of the market. I'm looking forward to next fixed term renewal later this year, likely bringing another 0.5-0.7% drop. For us, that's literally thousands of extra dollars in the pocket from 2 properties.

These huge drops in interest rates over the last years have more than offset any other related cost rises, to the extent that the last couple of years have been the most profitable in our long term holding of our (quite highly leveraged) portfolio.

All this talk of doom and gloom, is, well, a bit overly doomy and gloomy in my view.

The recent lows in mortgage rates got nowhere near the required 2.5 to 3% mortgages rates, that are needed to support the currently still far too high, valuations.

The market knows this, hence the multiyear, lower and lower pricing resets.

Oh and thanks. At least now I understand the term 'D&G merchant' which I've seen in these comments sections before and was wondering about ;)

Landlords in total have about 80% equity in their properties. I'm guessing they'll be OK.

Sure include the mass of boomers, who purchased on the 1980s and 1990s.....

Whats the leverage like on those that purchsed in the last 6 to 8× years ago?? I smell major mortgage topup land!

Oh the humanity.

I can smell the schadenfreude on your breath from here.......

Buying property in NZ is no longer a good investment decision. The fundamentals which did make it a good decision for the last 50 years have now dissipated and I can not see them coming back

1. Capital gain is no longer a factor.

2 Some form of Tax on Capital gain is a given down the track.

3. Rents are falling.

4. Costs are rising.

5. Supply is exceeding demand.

6. The Quality of the new builds and materials used are low.

7. Unpleasant aesthetics around of new subdivisions, appear cheap, nasty and crammed.

8. The price paid for the end product is not compatible.

9. Declining population.

10. Low wage economy.

11. Lack of infrastructure in moving people to centre's of work.

12. Increasing congestion.

13. New developments are well away from the transport hubs.

All good points. Would add...

14. Prince of Ponzinomics Tony A agrees with many of your points.

If capital gains are gone then yield has to be in the picture. Yield stopped making sense ten years ago as specuvestors went mental on ever lower debt chasing tax avoider capital gain.

To much debt without supporting income is just like to much 🌶 ....it creats a burning sensation at the other end.

Slightly off topic but for the record

Update on my non-scientific tracking of trademe mortgagee listings

October 2022 = 26

March 2023 = 37

February 2024 = 44

March 2025 = 65

October 2025 = 104

February 2026 = 92

Remember banks are doing their best to suppress mortgagee sales. Try searching for Must Sell as well.

some of those banks are a bit iffy offshore

The brutal sell-off was sparked from news across the Atlantic, where a UK mortgage provider called Market Financial Solutions collapsed into insolvency amid allegations that it pledged its collateral twice to secure £2 billion ($3.8 billion) of financing from a string of traditional lenders, reportedly including Jefferies, Barclays and Atlas SP Partners, which is owned by private capital giant Apollo Global Management.

This helped add further to the growing concerns around the health of the private credit sector, which have intensified in recent weeks as investors have probed the heavy exposure of both private credit and private equity firms to software companies themselves under pressure from the threat of AI disruption. About a third of private credit loans and private equity investments are thought to be in the software sector.

As the extent of the collapse in London became clearer, investors also got more information about what’s actually going on under the bonnet in private credit. On Thursday night, one of KKR’s publicly traded vehicles that owns private credit loans, called FS KKR Capital, plunged 15 per cent after it said it would slash its dividend and write down the value of assets in its portfolio.

Private capital stocks were smashed again on Friday night. KKR fell 6 per cent, Blackstone dropped 4 per cent, Ares Management fell 5 per cent and Apollo Global Management slumped 8.5 per cent. Poor old Blue Owl, which has become the poster child for this private credit drama, slumped another 6 per cent, taking its fall since the start of the year to more than 30 per cent.

As more of the finance gamblers, tech and property etc, are exposed offshore, the faith in credit markets will start to wane. Just like GFC banks stop lending to each other and failures start to rack up.

Bring on the margin calls!

The contortions will continue until they can no more

Isn't rent quoted as a key input to inflation? Something doesn't match up here.

Can New Zealand's economy thrive without a housing bubble? Liam Dunn

THE FACTS

- ANZ forecasts a 2% rise in national house prices for 2026, below the 3.1% inflation rate.

- Auckland and Wellington house prices remain significantly below their peaks, with real value declines of 33% and 39%.

- A cultural shift in housing investment attitudes is emerging, with a focus on stable growth and affordability.

The overhang suggests more Despair then Acceptance, but we maybe closer to clearance , another good fall over winter will sharpen the mind.

The continuing exodus from NZ will continue in 2026 and prices will be lower in years ahead......

Why NZ Homeowners are Moving to Australia in Record Numbers

If rents rise against rising property values, then the opposite must be true.

https://www.afr.com/policy/tax-and-super/unions-super-complex-s-conflic…

oh now i understand what professional investor means

Great news that rent costs continue to fall, especially in our cities!

Who knows, one day some of our young workers may actually choose to return to New Zealand...

No a single comment from Cote D'ivoire after spruiking those Auckland rents XD

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.