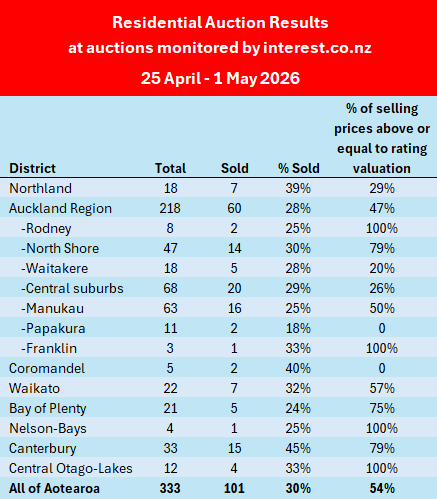

The overall sales rate at the latest residential property auctions has dropped below a third for the first time this year.

Interest.co.nz monitored the auctions of 333 residential properties around the country over the week of 25 April to 1 May. Of those, 101 sold under the hammer giving a sales rate of 30%.

That's the lowest sales rate achieved at the auctions monitored by interest.co.nz, and also the first time it has been below a third, in just over a year.

The national sales rate started this year above 40% but has been in a slow decline since the second half of February.

Just over half (54%) of the properties that sold under the hammer achieved prices at least equal to or above their respective rating valuations, with the rest fetching prices below valuation.

The latest results may have been slightly dampened by the fact it was a short week following the ANZAC long weekend, but even allowing for that, auction activity appears to be slowing significantly as the market heads towards the quieter winter months.

The table below shows the latest results by region, and details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

31 Comments

Unsurprising, given the international uncertainty and the prospect of interest rates rising

The market is dependent on sentiment and on credit inflow

Seems that the last interest rates rise of a few years ago taught NZers basic arithmetic. Belatedly, but the lesson finally stuck as it was learnt through their wallets

This rapidly retreating Home Auction market, is a harbinger for the rest of this year and the next, in a market of ratcheting mortgage rates and buyers retreating week after week.

2019 priced sales all only hold onto that cascading ledge, for so long, before the crevice locks give out.

With the Energy costs spiking into an already high inflation read and corresponding week upon week of higher mortgage interest rates, these clearance rares will be lucky to hold into the comming 20% range.

Clearance rates will only uptick once the sales prices drop another -10 to -20%, but like the now 5 year long, water torture crashing market, the slomo decline of managed retreat, is the menu.

Banks are still "managing" the tens of thousand delinquent borrowers and not as yet booked the roadtrain to the "mortgagee fire sale" abbotiour.

Meanwhile, had notifications of many petrochemical derived plastic products, about to rise in price betweet 30 and 40%.

Probably nothing......

Money going from too tight to mention, to nauseatingly stomach churning, for the financially stressed 65% of the country.......

INTERESTING times ahead.

Wow. thats an impressive number of metaphors for a post with almost no data

Ratcheting mortgage rates - where?

Buyers retreating week after week - based on what series?

Tens of thousands of delinquent borrowers - got a link?

Mortgagee fire sale abattoir - fantasy channel?

One soft auction week after ANZAC headin into winter and suddenly its economic Armageddon again lol.

You do this every time a weak weekly number appears, then disappear when turnover improves or prices stabilise.

Auctions are one sales method, not the housing market. If the collapse story was real, we’d already be seeing widespread forced sales, surging arrears, inventory blowouts, and broad price capitulation.

Instead we get another sunrise sermon built on adjectives from a sticky-footed lizard.

When facts arrive, let us know.

Cheers.

LATEST DATA !!!!

https://fred.stlouisfed.org/series/QNZR628BIS

Nice chart.

Now which part of that quarterly long-run index shows:

1. buyers retreating week after week

2. ratcheting mortgage rates now

3. tens of thousands delinquent borrowers

4. mortgagee fire sale abattoir

Because that was the question.

The first three are real. The forth is being held back buy the banks to supress the truth. This cant last forever.

Focus on the things that suck up money. Stagflation, Oil shock, Higher interest rates, AI destroying white collar work to name a few. Also all real.

They all manifest as lower available cash for rent and or mortgage payments though a greater supply of new houses. The reality that the debt stacker tax avoider model has run it course. The disciples of which have well overshot the system with their greed. This also stops them seeing the truth.

🍿 +⛽️ = 🔥

Some of those risks are real in isolation.

The leap is assuming they all hit hard enough, at the same time, to produce the outcome that you are asserting

She said the interest rate environment isn't supportive of COVID-19 era type mortgage deferrals.

"You wouldn't be doing the right thing by customers by having wide-scale mortgage deferrals, given where interest rates are at the moment compared to where they were during COVID," Watson said.

However, she said there are lots of things banks can do on a case-by-case basis, which is probably more appropriate because people and businesses are impacted very differently.

"The number one thing is come and see your bank as soon as you feel like there's getting to be a bit of a strain on your books."

https://www.oneroof.co.nz/news/tony-alexander-more-than-a-third-of-prop…

1/3 will sell in the next 12 months? nothing sells in winter so next summer maybe interesting, as we at 12 year highs in inventory now, I guess interest rates will be higher by then as well ,ANZ is talking stagflation

Total Rental Properties:

As of Q4 2023, there were approximately 643,000 private rented dwellings, according to Stats NZ

.

Nationally, over 80,200 house sales were recorded by REINZ

over the entire 2025 calendar year

a third is 214333. so that's a lot of extra stock.

“Plan to sell” in a survey and “actually sell” are two very different things

People say they plan to renovate, move, downsize and sell all the time

If a third truly dump stock, then will see it in listings, turnover, discounts and prices

Until then its just a headline, not an outcome

I agree, plans are not actions, if only a 1/3 or that number talking selling 213k list it would only triple the current stinking unsold stockpile ie approx another 71k more listings

imagine if they all list. 5 years ago most investors where going to hold forever.

if only 1 in 6 of them actually list , it only doubles the current 12 year high stock levels, then there is that tip of the iceburg townhouse issue as well. Probably Nothing

Property bubbles take years to unfold, we are probably only 1/2 way there. Most of the "investors" are still in the bubble hoping for recovery. but they are starting to THINK about selling. Be Quick

in the few years most will be wishing they sold in 2026

Agree - I think we've only witnessed the opening act of this downward cycle of house prices. Might be 2030 before things get back to some type of equilibrium again where housing as an investment might stack up (based upon good cash flows and the probabilities of prices gains are higher than price falls - at the moment the probability of price falls is greater than prices rises (in my opinion) and the cash flows don't make sense). Before then I think its like putting water (a persons precious savings) in a leaky bucket.

So we’ve gone from a survey headline to mind-reading investors and predicting future regret?

Thats quite a trip for one comment.

Strong vibes, thin on evidence.

Hey Welly, your speech and views are mostly correlating with that of a donkey deep, Property Investor.

To be in this position, as the investment winds have had a generational paradigm shift. is not ideal.

Hope you wash up ok, in decades to come. So all the best WellyPI:)

SOME HISTORY FOR THE STILL NIAVE: HISTORICAL EVIDENCE APLENTY -

Yet it could all be foretold, as a few of us did, as a dangerous, mine littered ground. All the signs of a certain, future crash, were being baked in the cake, over many years. Where it ends, no one truly knows, but will be between the Japanese and USA property crashes, as seen over the previous 40 years.

Signs and setup for the most epic property price bubbles that world has seen - and yes it was in NZ. World beating......

- Home for Families, became secondary to the "best investable hot cakes" on the investment menu. Homes for families is a desirable good, at 3 to 4DTI.

- Every year that property gained more than 2.5%, it was dangerously extending past, average earnings capacity.

- All the media were in the property speculation trough and had series after series, of only positive property investment articles, while suckling on the REA and FIRE industry teat.

- NZ was besieged with property seminars and "investment gurus" who attempted to Propell - er new, gumby investor fodder, to keep the property bubble/scam aloft.

- Banks lent wildly, at dangerous DTIs past 5x earnings. This was also without regard to much higher interest rates, that were certain to come and as we stand now - will go much higher than currently prevailing, in mid 2026.

- All in sundry would laugh at anyone dissenting from the pro-property NZ Mentality. Warnings of a property bubble and likelihood of a crash, were laughed out of town. "as property always goes up, without fail". "Put all your eggs here NZ, safe as houses mate"

- Almost all of NZ was sucked into the Housing Ponzi - then come late 2021, new gambling suckers, were thin on the ground.

No property investor is laughing all the way to the bank in 2026.

Banks are no longer laughing either, as their loan books go increasing under the tide, this salt water is corrosive to their capital and collateral values. As values slide still further, expect more bank bosses to flee. John key was not wrong to flee ANZ, just early.

In a true "market to market" - some banks will be vulnerable.

What a catastrophic overreaction lol

Three lines from me, twelve paragraphs from you.

That seems proportionate.

no need for mad max, another 5 years like last year down 3.8% and we are down another 18%....

I just got a valuation on a house I sold in 2021 via one roof email , says down 2.58% since last month...

you can keep telling us why we are wrong for the next five years welly,

plenty of posters like you have come and gone in the last 5 years,

and here we still are, All the DGMs still right

remember the dickheads, riverhead guy, was it tothepointless guy, clink clink guy, the time in the markets brigade (quieter now its been 5 years and -20%... ever hopeful dickheads calling the bottom every quarter since late 2021....... you only loose money when you sell guys (never studied mark to market or portfolio theory), most guys who cannot work out a true net yield on a simple resi investment. I can safely predict Welly that you will be just another roadkill poster as the market rolls onwards.

That sale of yours in 2021 seems to be weighing on your conscience.

Hi WellyPI,

What I have outlaid is all obvious stuff, historical fact, and reasonable future projection.

If you were not switched on, could not work out a reasonable yield calculation, bought too much overinflated (BUBBLE TIME:) to buggery property, sorry - but learn and do a little better in future.

You will recover, lick wounds and move on.

Funny thing is none of you know my actual situation.

Own one house? Three? Renting? Commercial? Investor? No property at all? What I do for work, what I earn, or whether I even still live in Wellington.

Doesnt seem to matter.

Question a bearish claim and instantly you get filed under “property bull / vested owner / coping investor”.

Then we get the old “property bulls have come and gone” line, as if forum turnover is market evidence.

More likely some simply got tired of the same identity wars, abuse, and certainty theatre from the usual mouthy suspects.

When every disagreement gets met with labels, insults, and another end-times sermon, plenty of normal people just stop bothering, and the site loses value.

That doesnt prove you were right. It usually just means you were exhausting.

Much easier than answering the actual point.

Go have a cry.

Haha, proving Welly's point..

We test ideas based in financial history and our experience.

The best financial lesson is to diversify imho.

Spread any windfall profit.

To squark against prevailing narratives is fine, Gecko does it often. Dont take ourselves too seriously. Keep it up Welly.

Property is but one asset.

Fine to own your own home.

Yet stacking all your eggs in that basket is very risky and hellishly illiquid. Ive seen owners try to sell for 3 years, and the value has dropped 200 to 300k, while they chase a top dollar sale. As of today, not sold and value collapsed- "not winning"

Property is buggered as an investment with every metric and current/future Govt policy going against it.

We all learn lessons, and best to make our mistakes early on, as we can recover.

Interesting overnight edit.

Diversification guru by night, property undertaker by morning.

You do seem oddly committed to hinting that anyone who questions you must be a financially stressed investor...

Imaginative, I’ll give you that

Wow you copy down what he posts and compare it the next morning? I think the Gecko is living rent free in your head Welly....

They survived till ’25, waited for an economic fix in ’26. Good luck telling anyone it will be heaven in ’27!

One minute response time and I’m the one living rent free?

Cute of you to come to Gecko’s defence though.

Relax WellyPI.

Yes guilty as charged your honour, I do edit typos and add further useful info, that is relevant.

- It all good, above board and should not personally bunch your undies.

Maybe you do need me to pay rent:)

You seem very interested in propping a failing and falling NZ housing Ponzi. |t gives an impression as someone who has stacked the bases, yet now a home run is impossible, such as the worsening market conditions, not allowing a dignified exit.

Don't worry, we have all taken investment losses and it should not be personal.

It is concerning to see the number of mortgagee sale rising. One large rd I monitor, has 3x properties up for sale - by the Bank.

- Knowing this is a small tipped/large underbelly Iceberg should have us all aware.

Many will be financially wiped out and ignored obvious warnings of insane DTIs, abysmal yields, Bubble land, very sad.

Then listings surge larger and larger and remain unsold - this won't end well for many and will be very concerning for banks - who have had to manage this property crash, while not wanting to alert or alarm the Sheeple.

Banks don't want the market to know, the risks they see as insiders, and are on the precipice of !! It very much hush, hush.....

Another long sermon.

You do seem heavily invested in being the heroic one who warned everyone. That identity can get sticky when reality keeps arriving slower, messier, and less obediently than the script promised.

And still remarkably confident about a strangers finances.

A fascinating skill set, really.

Now go and enjoy your sunday :)

Glad you enjoy the true pulpit of PonziTruths:)

Enjoy the beautifully Sunday Wellyone.

All and all, at least we have the Pineapple Lumps NZ :)

Chief ASB economist rates current crisis

ASB Chief Economist: Forget Rate Cuts, NZ Mortgage Pain Is Just Starting https://youtu.be/dS_qDECbCV4

https://www.news.com.au/finance/economy/australian-economy/inside-china…

worth reading to understand how housing crash in china can impact aussie via iron ore prices

Indeed. The only common factor is creation and access to stupidly cheap debt. Then the business of sucking buyers into the endless enslavement to global banking interests... aka the debt trap.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.