Bayleys sold 16 of 38 Auckland auction properties last week, with the remaining 22 passed in, postponed or withdrawn from sale, giving an auction clearance rate of 42%.

Among the properties sold was a large character home in Herne Bay that was in three flats and ready for refurbishment, which sold for $1.52 million.

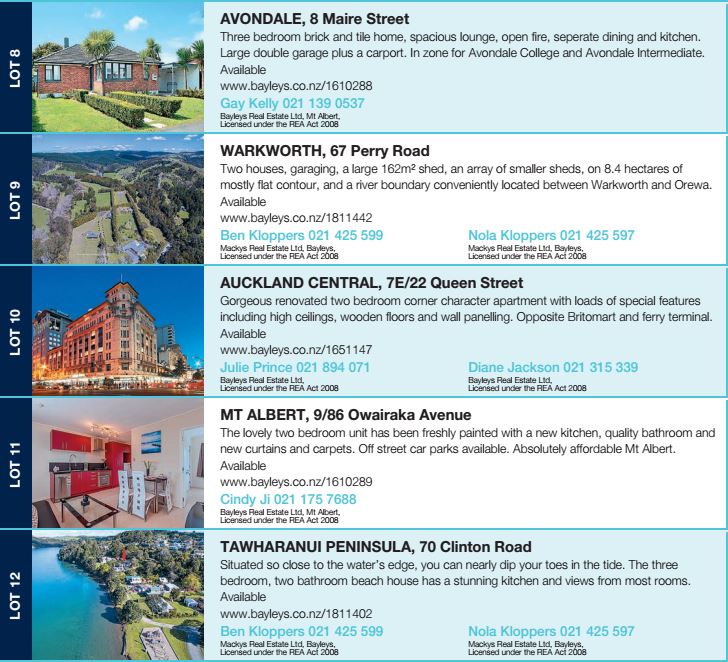

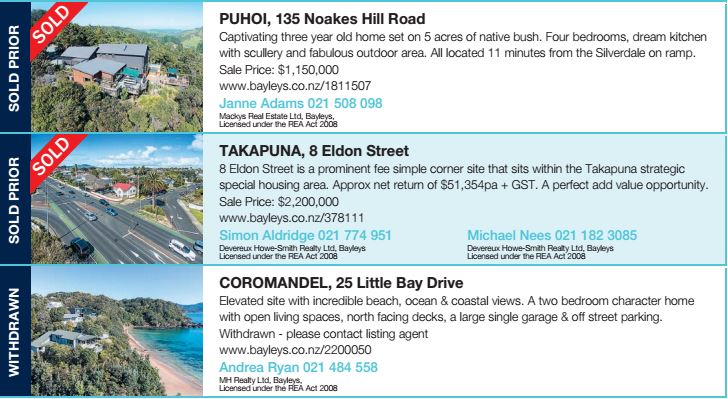

The most expensive sales of the week were both on the North Shore where a potential redevelopment property at Takapuna sold for $2.2 million and a Devonport villa fetched $2.05 million.

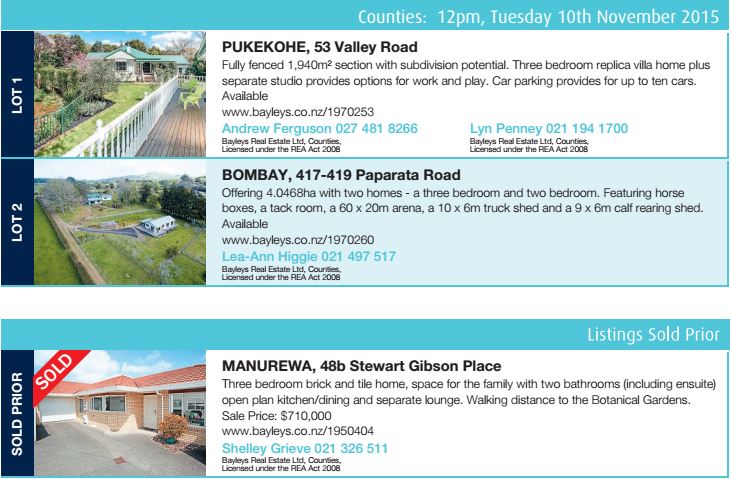

Among the cheaper properties were a three bedroom house at Forest Hill that sold for $780,000 and another in Manurewa that went for $710,000.

See below for full details of last week's Bayleys auctions, with photos and details of all properties, including those that didn't sell:

46 Comments

who would have thought that a speculative bubble would ever pop..

Is this the same Simon talking up the market a few weeks back?

You do what you need to to offload some auckland rubbish before the market really tanks.. learnt from the best... No not at all, Ive been a bear on auck property for last 2 years, granted if you had bought 2 years ago you're probably still ahead, but may not be for long

Agree. There will be tears.

http://www.interest.co.nz/property/74363/olly-newland-says-property-inv…

If you bought 3 months ago you're still ahead. If you bought 2 years ago, you'll still be ahead if the market value drops 35-40%.... which is unlikely.

If you bought a handful of properties during the 2008 crash you're still laughing all the way to the bank yay!

I take it you are factoring in losses from negative gearing Esprit. All that hard earnt after tax paid income paid to the bank/landlord to prop up those rentals.I bet you haven't.

If you only bought three months ago, those wouldn't amount to anything at all. I was metely talking about prices at face value.

As for me, I don't own any investment properties so it makes little difference to me. If the market goes tits up I might be on the lookout to acquire some though.

Thanks Greg - up to date, no BS, accurate information of where the market is currently at.

Good stuff - please keep it up!

if this starts to be come a regular thing it will be interesting to see how many hold and hang on or take what they can get

Just checked one of the properties out of interest (based on all I have heard about the north shore market) - the Forest Hill property that sold for $780k has a CV of $790k. Quite the turnaround!

So CV of 790k at sept 2014, prices WERE up 25% on year on year in September, so correction of around 25% already on the cards. I know of a number of similar examples also of places struggling to get close to the sept 2014 GV prices at auction. Any one who bought between then and now could see a 100k or more down the drain

Its about quality stock, 1/35 Merriefield is a shoddy plaster home, if it were weatherboard or brick based, 1M all day long and sale price is representative of this. Keep your hopes up on the meltdown if it help you sleep easy ;o)

Yeah - plaster homes will be the ones to really suffer first.. (There has been a lot of bad press about new immigrant building standards but remember these houses were built by the local top notch kiwi builders who now consider themselves brain surgeons with the rates they are charging)

With the plaster house sales a falling tide shows who has been bathing naked etc etc.....

i doubt most people would touch a plaster clad home built from the 80's on if they have been here awhile so have heard the horror stories.

Yeah - was watching a beautiful plaster house built in Castor bay - sold for 1.3 in 2013, sold for 1.8 in 2015. Built in early 2000s. Chinese all over it - haven't they heard???

Bought a plaster home not so long ago. Allowed me to get into a good suburb, with a good plot of land (623sm) and the only reason i could have afforeded it, was because of the stigma around plater clad homes (got a builders report and a cladding expert in to give it the once over). Warm, secure for the kids, low maintenance, good location, so not all bad ...

get an old time builder to look at it for you.

plaster clad and watertight do not go together. all it takes is one little crack water gets in and because new houses don't have breathable vents it does not dry or escape.

your best bet if you can afford it is to reclad

I'll leave it to the experts ... Plaster clad on cavity blocks plus a sizable cavity into the inside wall should do the trick. Having came from Europe where thats pretty much standard, but in a more extreme climate, i was happy with that .. Anway, back to topic, plaster clad is not the end of the world, just worth doing some pre work before you buy.

And for what its worth, i think the prices will drop again for another few months before it return's to BAU early next year. If i was an investor and could afford to hold out from selling for a few months, i would :-) I have said it before, but there are a lot of people on this site that all they seem to do is see the dark cloud in the silver lining for whatever reason when they should be trying to see the wood from the trees. That is all :-P

Nothing wrong with plaster clad, like any disaster it takes a series of events and not a single event to cause major problems. As long as it has eves, window flashing and a roof that doesn't leak and you clean your gutters once a year you will not have a problem with it. If the design was wrong and the builders were useless then you have something to worry about.

But is all well in landlord land?

Super thanks.

Of course xelnaga... all's well in landlord land. In my own situation, I have been advised by property managers that rents on several of my properties are rising by the amount of $50 per week (per property).

I am very happy with that and have no reason to sell. Not that I ever would.

Rent inflation will continue

which is no help in getting the economy moving, more money not being spent in shops or on goods but headed to the banks then to their shareholders most of which live and spend in australia

(disclosure, shareholder in all 4 big banks)

If labour claimed the majority sold to that group70%from memory

First home buyers took a small percentage of loans issued

That group is making aussie bank shareholders rich and our poor tenants are making a small portion of contribution as well

Thats should cover your rates and insurance increases, not sure about maintenance though. Factor in the decreasing property price into your yield yet?

When prices are rising we are told they're just paper gains and we can't factor them in until we sell. If prices are declining (which I think in a few months we will see they are not) shouldn't the same hold true? Anyway increasing rents are better than increasing values for most true investors. Increasing values are just a nice bonus... and generally lead to increasing rents.

Well said Machi...

Frazz, my friend, not everybody bought their investment property last week!

I am a long long-term property investor. Of course I have maintenance expenses but the minimal costs of my mortgages ( NB: I don't ever want to be mortgage free because no borrowings is inefficient use of my capital) mean the yields I get can easily cover all expenses and leave plenty of dough left over.

You say yields are poor. I say look at the long-term property investor's situation. In my case, a lot of properties I own are now yielding circa 20% (yes... 20%) ON PURCHASE PRICE.

Gosh mate, the lesson I keep proving to myself every day is the longer I own property the easier it is to finance it, and buy more. And, 'cause I ain't ever gonna sell, rent increases are more use to me anyway.

Then you have to choice at anytime to sell a few boosting your cash flow even further

May I ask which area is your rentals

Hi Mastery, all the properties I own are "cash-flow positive" (as the saying goes). There's money left over after all my costs. If I sell one I will reduce my income.

So why sell one?

I have always had a long view about property. I buy them and concentrate on reducing the borrowings to a point where my overall cash flows are what they were before I bought. When yields are low (like now) I am glad I don't have too much borrowings. When yields rise, the extra cash means I can afford to borrow a bit more and operate with higher loan-to-valuation ratios.

I am conservative... for sure. But that's what an investor is, compared to a speculator (which is what most people on this site seem to be) or a developer.

My properties are in Auckland, north and south of Auckland's harbour bridge and in several North Island provincial cities. The Auckland properties have provided good capital growth but the provincial properties have provided better cash flows to help fund everything.

Thanks for the report Greg, keep them coming

There seem to be a lot of landlords selling up in taupo. Several comments have come back that these were investments made in the 2006 era, thereafter prices dropped substantially and the recent movement in properties is giving them an out. My assessment of the properties is this. They are a mess. The little spent on some of them has since been erased by yet another tenant, most have had no upkeep. In general the housing in Taupo is awful anyway. A lot of the hardiplank tiny boxes of the 70s and 80s. We went to see one recently, private sale open home. The pics showed a spotless repainted new kitchen home. The truth. This was done in 2011, by 2015 it was a pigsty. The cheap kitchen was bugrd, the bathroom was rotten, etc etc.

Sounds like the average NZ rental. Not great investments therefore not maintained by landlords. Certainly not looked after by tenants.

Good luck finding work in Taupo. Your still better off buying than renting if you take the long term approach. How are you going to survive when you retire if your still paying rent ? answer you can't so like they say, your just going to have to keep working till you die.

Yes Carlos, the tourist industry pays peanuts, and the new power generation sites are completed. Dairy is having a mare. Drystock is looking a bit iffy. So why the buzz on the RE. Interest rates, some pent up demand, and ex aucklanders??

Its hard to decide what to do. My gut says if the family can keep renting at 400 a week they are better off. No rates no insurance no upkeep. And a 400 a week rental in taupo gets you a decent house.

21k per year in rent, vs 22k per year in interest and rates, is saving 1k really that important? Or buy a 300k house and use the change to improve the property :)

First read below where rates are a rort. Personally I am not into pinching pennies, I tend to look at the bigger picture. Having spent money on my own house recently I know its not an insignificant thing to do. And how do you really improve a 1970s box? Perhaps use the spare cash and savings to put into a business? From the numbers of lanndlords looking to be ex landlords around here, and govt getting tougher on them by the day, after this rush of money into the provinces, will there be a turn the other way come the new year or will these low interest rates push the boom further..

It must be cheaper to own at 4.5% interest rates than it is to rent somewhere like taupo?

If your going to live in, keen to improve the place, no question buying over renting in a place outside of auckland where prices are still sensible

I dont know that Taupo is sensible any longer. It has had a pretty good boost in the last couple of months. Rates in Taupo are crazy also. A 400k home will be a bit under 4k.

That is crazy a house in Auckland worth almost twice that has almost half the rates.

The only advantage of renting I can think of is it makes you very mobile, probably good if your single with no kids and want to be flexible to move at short notice both around NZ or even the world if your job carries you in that direction. Probably also good if your not a practical person who cannot even change a light bulb.

The New Zealand Herald website has a note today that house prices are up significantly in Hamilton.

As previously observed, Auckland's rising prices are spreading around New Zealand and it's coming to a town near you too.

Is that too late to put my bet on wellington now?

You should do you own research buddy, and come to your own conclusions.

For me? Wellington is another provincial North Island city. Owning a house there - for the long term - is a great idea.

Manage the debt.

But if ya wanna buy and sell - speculate - oh well good luck, you are less patient than me.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.