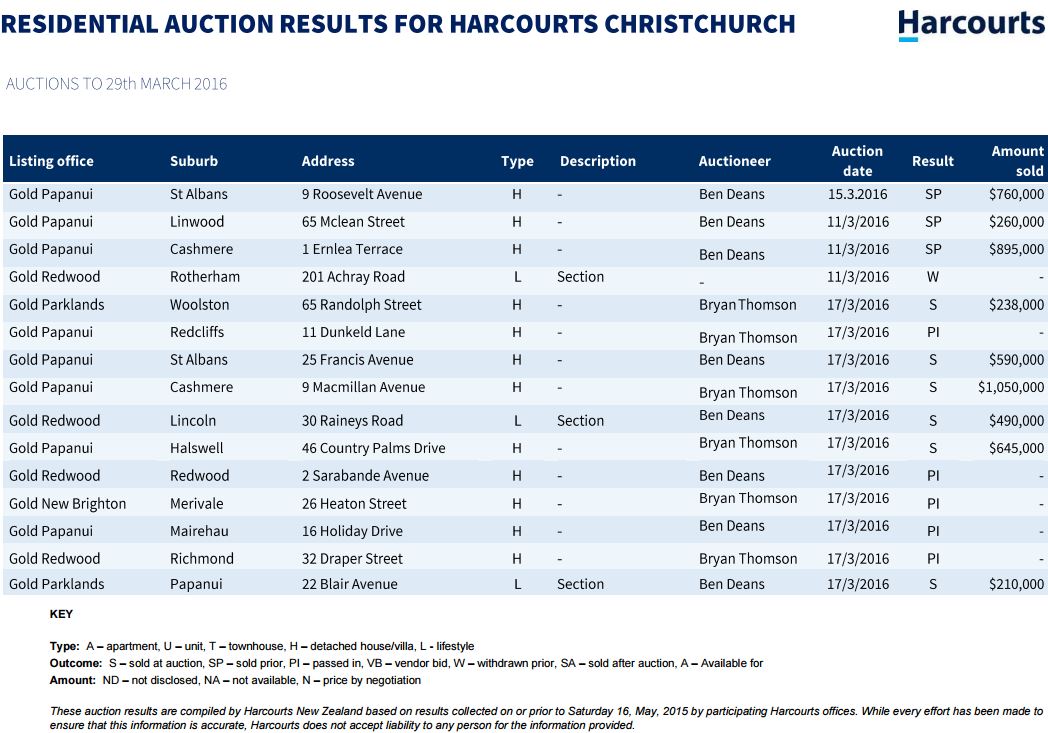

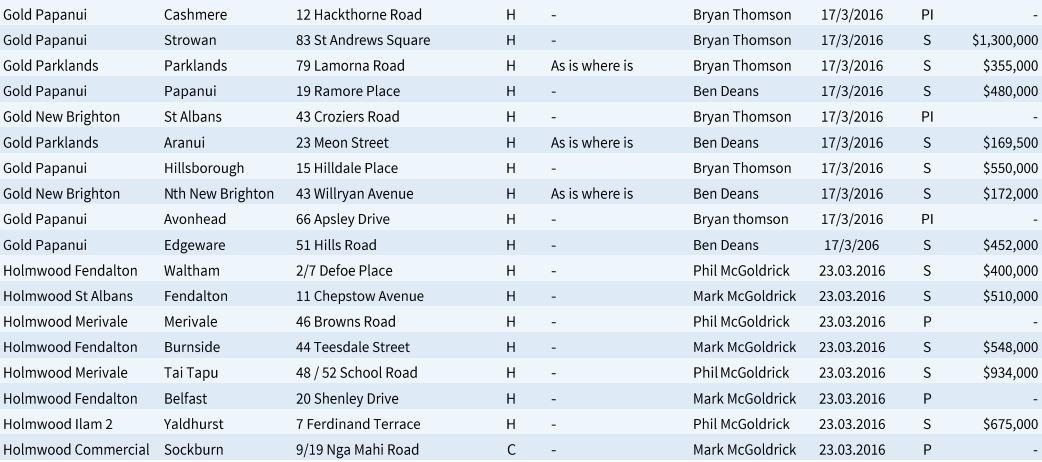

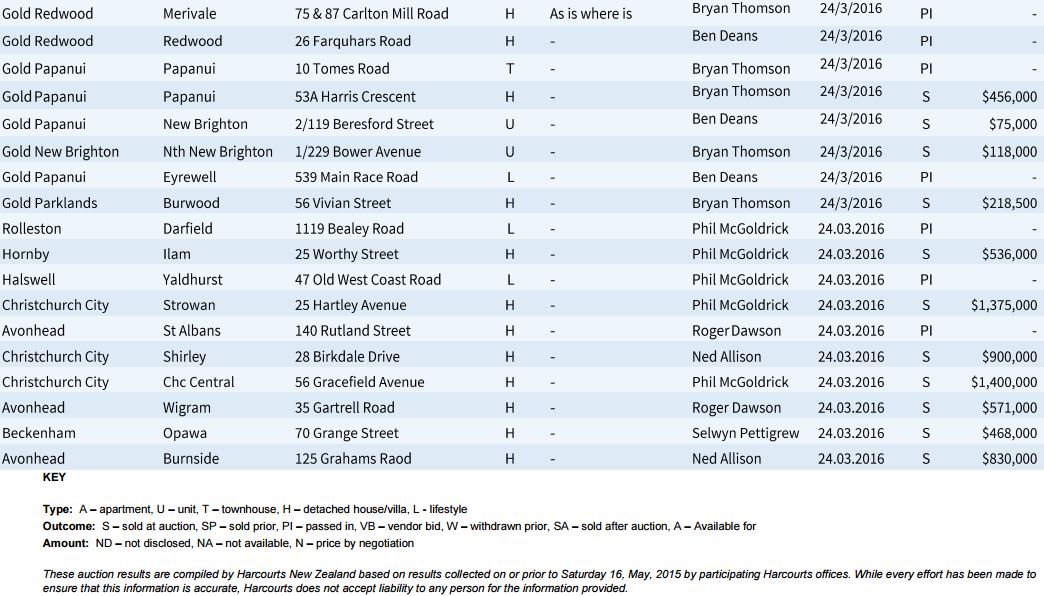

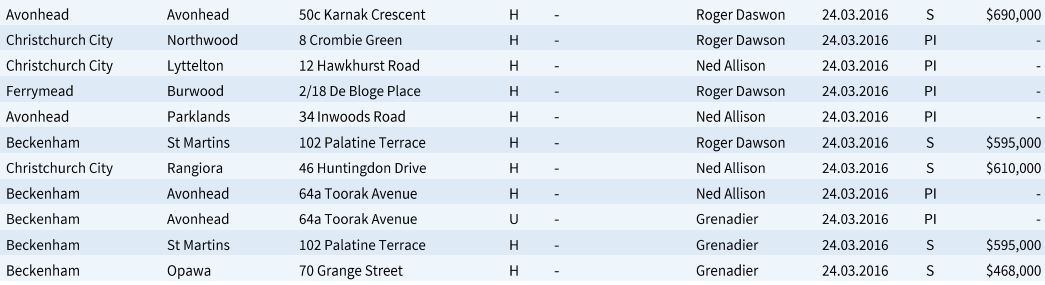

Harcourts auctions sales rates ranged from 80% in Wellington to 63% in Christchurch last week.

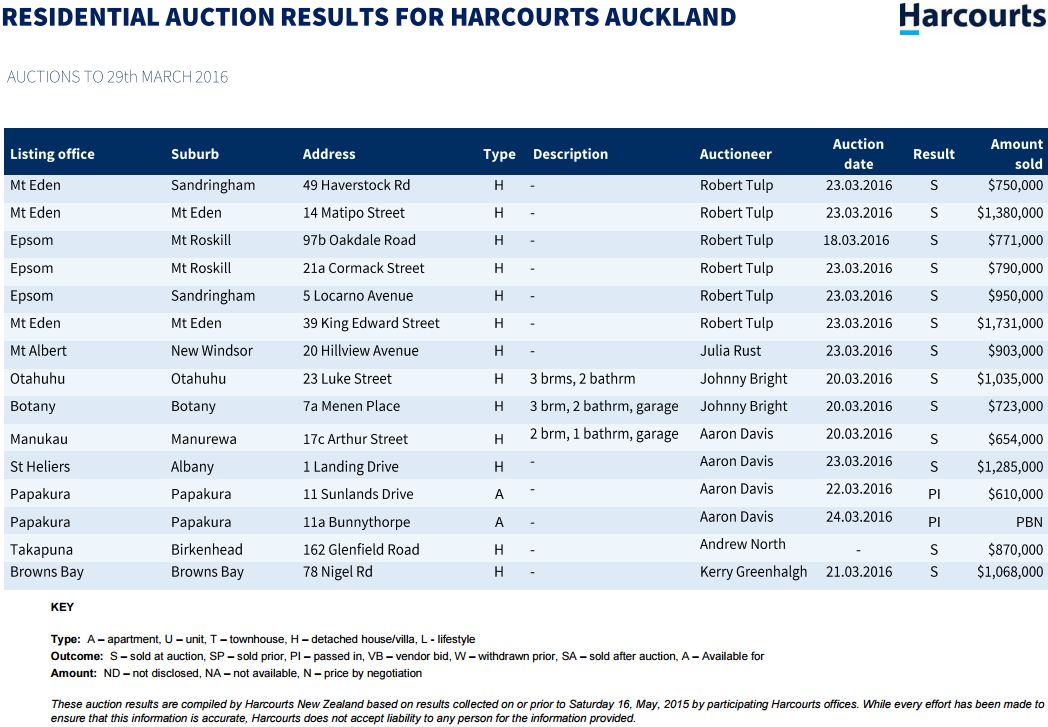

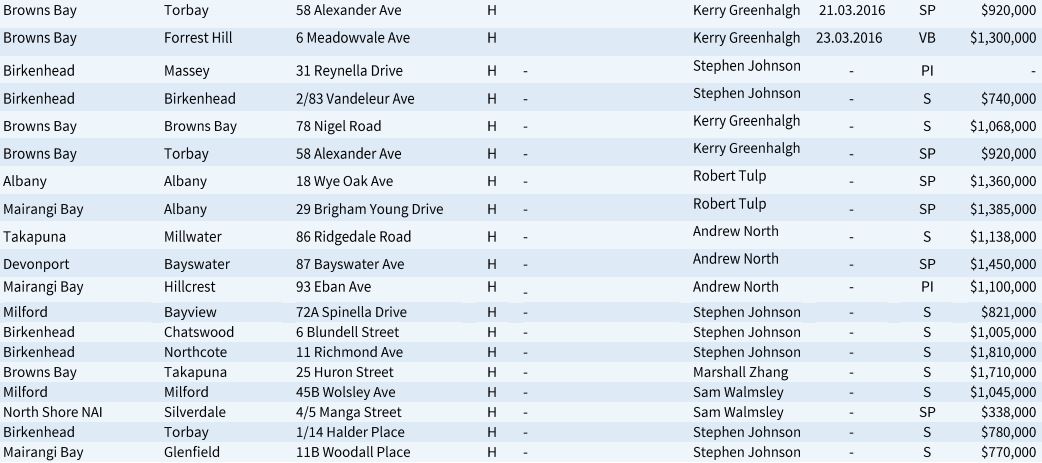

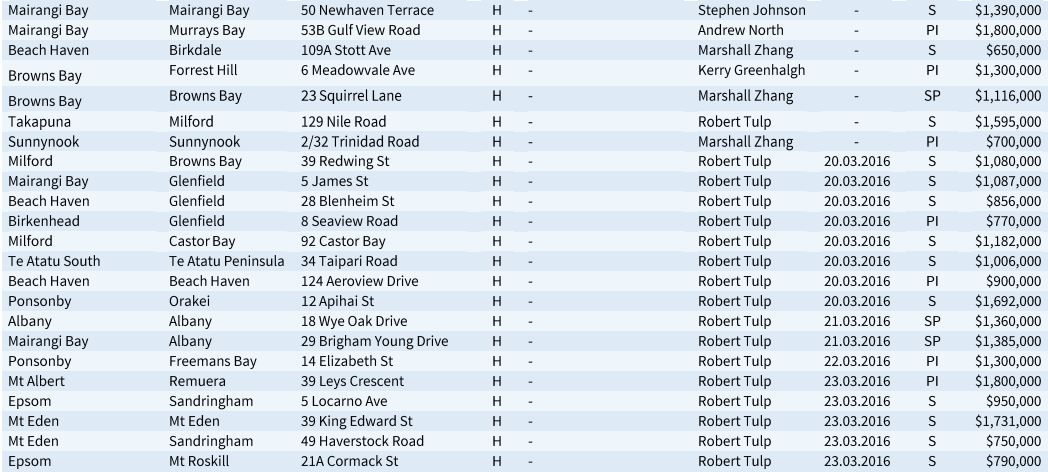

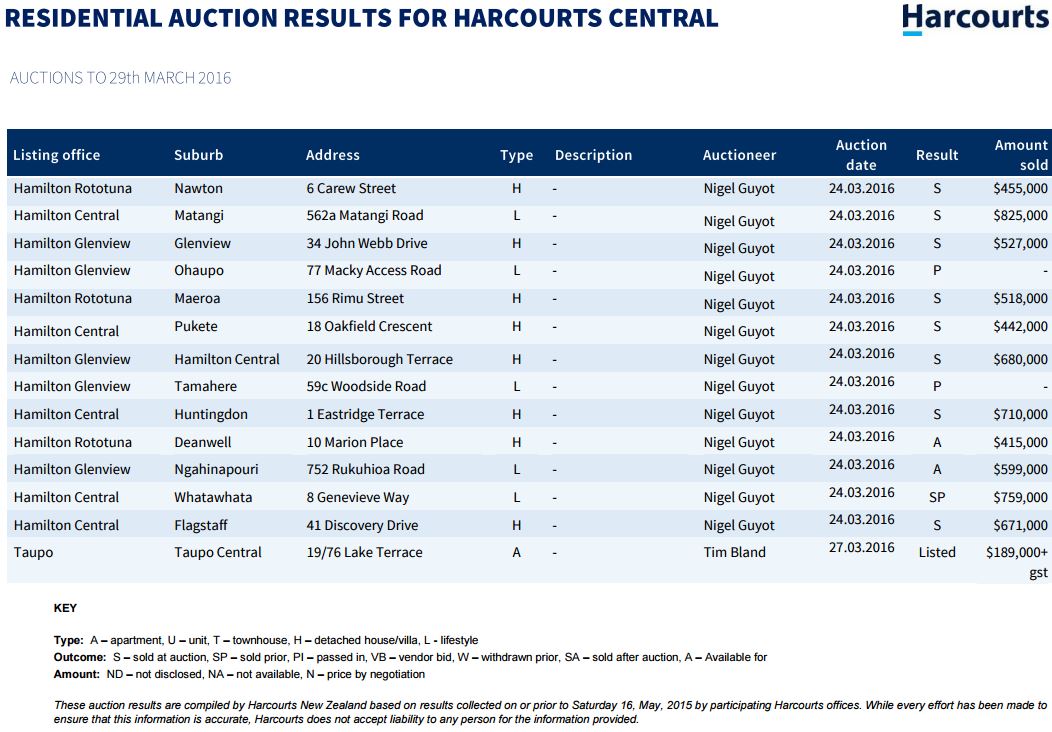

In Auckland 60 homes were marketed for auction last week with 47 of those selling, giving a sales rate of 79% and in the Hamilton auction rooms nine of the 14 homes were sold giving a sales rate of 65%.

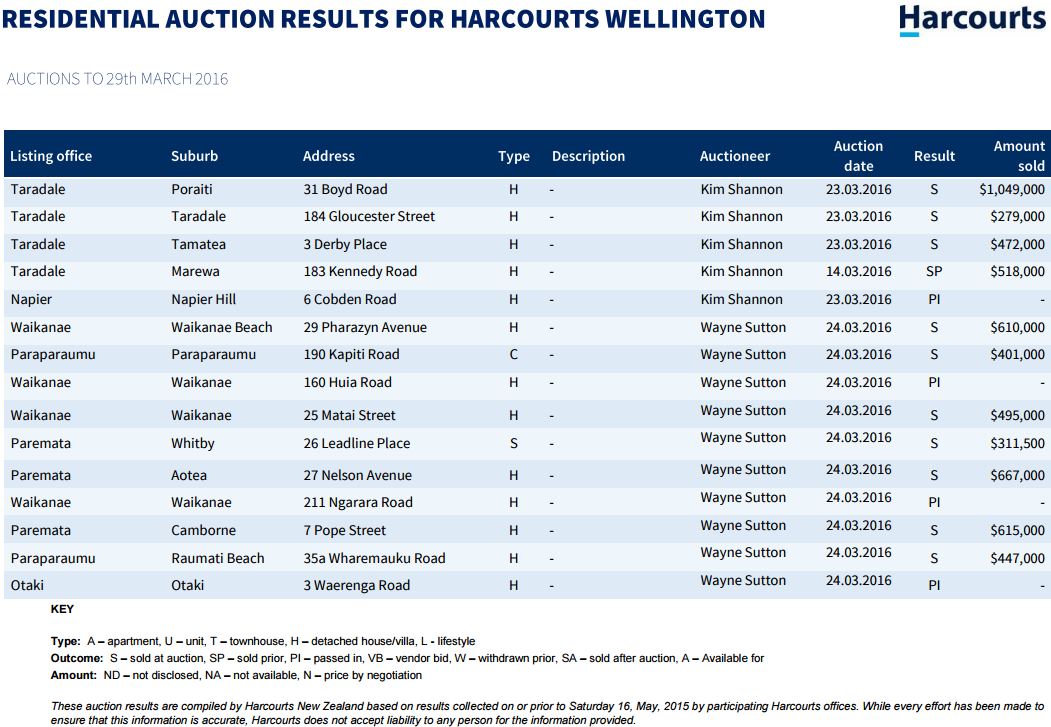

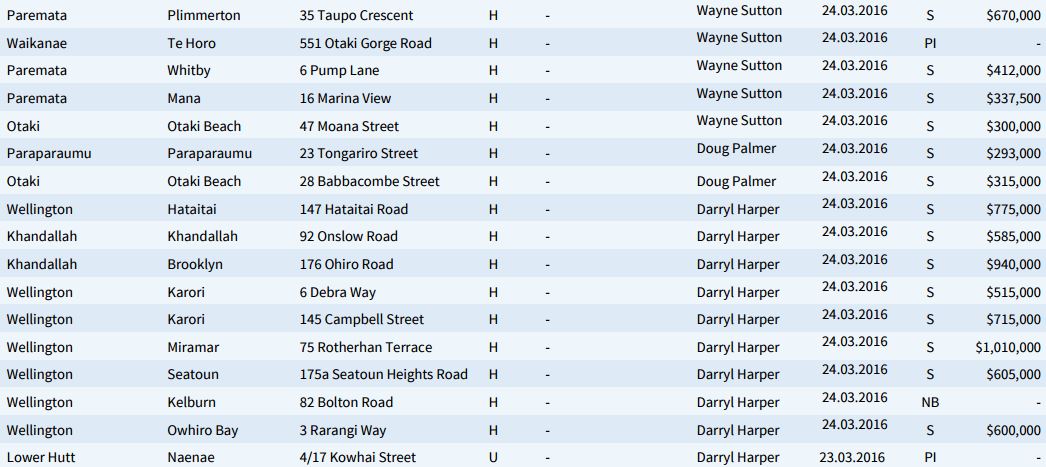

Wellington had the most successful sales rate last week, with 16 of the 20 auction properties selling, giving a success rate of 80% and in Christchurch almost two thirds of last week's auction properties were sold.

In Auckland the most expensive sale was a house at Northcote on the North Shore which sold for $1.81 million, pipping at the post a couple of others that sold for $1.8m.

In Hamilton prices ranged from $415,000 to $825,000, while in Wellington only two properties sold for more than $1 million and a house in Levin fetched $112,250.

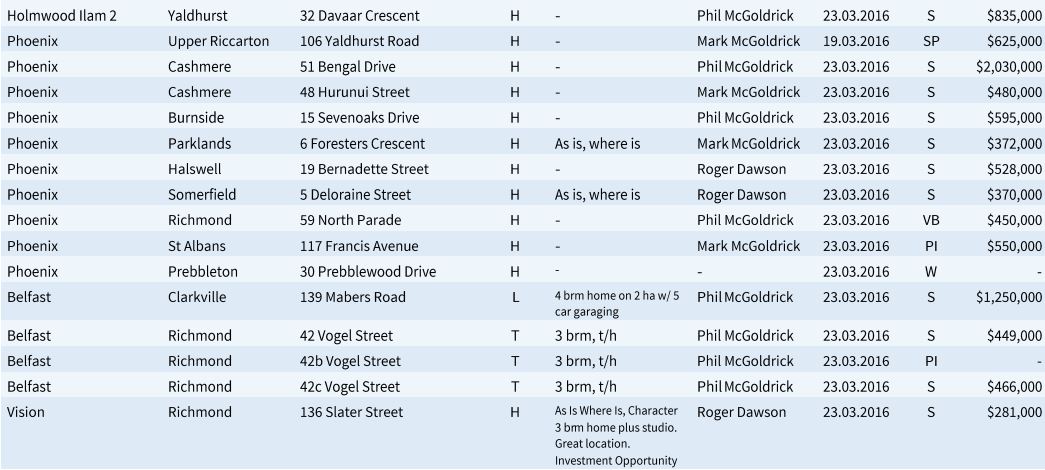

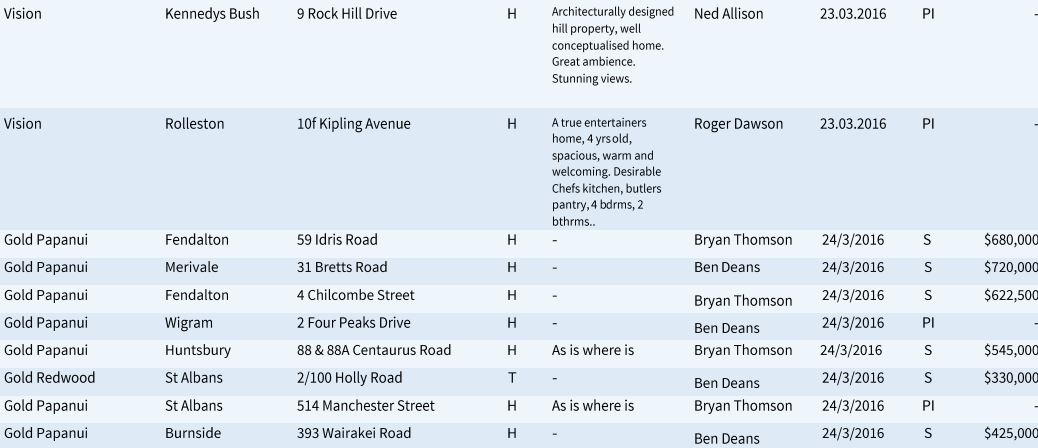

In Christchurch prices ranged from $75,000 for a tenanted, one bedroom unit in New Brighton sold on an "as is" basis, to $2.03 million for a house in Cashmere.

See below for the full results:

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

62 Comments

Actually 47/60 = 78% not 80%.

And how come none of these auction results show a "SA" for sold after the auction? More twigged results no doubt to make the market look stronger than it really is.

Market is going bananas. Ron Fong Choy was right.

Not what I am hearing SpaceX. Getting worse in fact. Very few overseas buyers. They know sentiment is changing and are watching from the side lines as more comes on the market. My niece has still not sold. Prime 3/4 acre home with harbour views. Owned less than a year.

From what I hear on this website everyday, the market is going to be busier than 2015. It's that simple, nothing has fundamentally changed since then, no reason for the party to stop, in fact as interest rates continue to fall, people will borrow much more.

Good for you, bad for me as a first home buyer.

SpaceX, you are completely full of shit!

I'm just regurgitating what is reported on this website.

No first home buyer talks of there's "no reason for the party to stop", that's not the language of someone missing out.... you are full of it and have vested interests.

I've been in property for over 20 years and I know BS when I hear it.

It must be tough though. I was thinking where might be a good place to buy one's first home in Auckland and came up with Massey. I heard prices may have retreated there recently. I did a search in TradeMe and came up with this which at first glance looked sort of reasonable with asking price of 600K.

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

Yet CV is 375K making the asking price 60% above. That's pretty typical of this type of house. It would seem quite a risk really.

Disclaimer: Grew up in Massey

New mall generated lots of hype last year. Dollar signs in everybodies eyes. Agents talking it up breathlessly. Perhaps now waking up to the fact it's just another souless mall and it's still Massey.

Suspect that a number of the upmarket new builds coming through the pipeline have been skewing the average suburb figures recently also.

Risk should be evaluated on a timescale of years. Could say the whole of Auckland is risky at these income multiples.

I do hope Chaston charges Zach Smith for the free real estate listing.

Trust me Triple. I'm not full of shit. I'm trying to get on the ladder and if shit keeps going in the direction it is, then it'll be time to look for a new country to move to. Trust me, it's beyond fucked when you save 90% of your income and you still cannot make any gains towards getting a house.

It's depressing

I saw the first five houses go to auction at Barfoots today and they sold for an average 39% over CV. I think you are right SpaceX and low interests rates have hurt the FHB more than helped them in Auckland. The typical house a FHB would be interested in is way over priced. It is also the house that one wants to live in so will be fought over and demand a premium. Low interests rates have pushed house prices up and made them even less affordable than before.

SpaceX is no first home buyer. Nothing he writes adds up - which typically means he has vested interests, just like many other spruikers on this site.

In fact some idiots with vested interests would probably have 2 alias' to try and be clever and influence naïve readers.

I don't own anything. And my bank savings are returning less and less every month. And yet prices keep going up, I want a crash but that's not going to happen, I was hoping for a stagnant market, that's not happening either.

Whether what you are saying is true or not, it is definitely an actual reality. I spent a bit of time on here on Sunday explaining that I'm currently working 3 jobs (on lunchbreak now and stupidly checking in on here for false hope) and will need 5-6 years doing exactly this, consistently to even get close to the $120K deposit I'll need for the $600K shed somewhere. Sunday I was heading for a breakdown. Today, I don't know. I had a lot of good feedback from here from people starting to realise the very scary reality us renters face for retirement and just wanting a humble home for shelter when we stop working. My thoughts are at the moment it's time to quit at least one job and having a life again. You just wonder why you are doing it when looking at whats going on, I may need $240K in 5 years time as a deposit. 10 years with a life on hold is starting to make me feel sick.

If you do the full analysis on quitting one of the jobs, you may find that you won't lose as much money as you think. I've no clue what the jobs are, obviously, but how much travel is involved? How much time and money does that travel cost? Do you have to buy special clothes or equipment for it? What's the actual hourly rate once you've factored in the time and expense? All questions to ask when evaluating which to quit.

Being exhausted and sleep-deprived isn't the best state for clear thinking and decision-making, and on Sunday you definitely sounded like someone needing a bit of a break.

..Organise a national rent strike. The people in control wish to push the young to breaking point. Get cracking on social media and orgnanise a national rent rent strike. Get the message that property speculating is not risk free - watch the market correct then.

Do what the workers did when I was younger...power by numbers. I can't see any other option - no one is acting on this property crime and you guys are getting screwed.

if by rent strike you mean tenants give their landlord notice, then i don't think you'll have much effect.

If perchance you mean refuse to pay then that is why we have the inexpensive tenancy tribunal which has the power to make awards of monetary damages, if your landlord is going to take you to court for not paying rent anyway he might as well add any other minor stuff that he wouldn't normally bother with. If the property that you live in is managed by an agency then you'll also have a black mark by your name in their records. If the strike is of any significant size i foresee rental agencies sharing data.

The oppressor has spoken...

..na, the oppressed are too quiet. I'm fine, but I hate seeing the 1% ers dicking our young around. My father and his generation fought and died for me........and what do we do for our kids?? Sit back and watch them get screwed by hopeless policy and greedy politicians.

The problem still remains that JK only does what pleases the voting majority. And they're BB's who own a lot of rental properties...

The problem is young and poor people don't vote. Giving free reign to Key and the selfish generation.

...if enough sign up the tribunal will be powerless. Its called anarchy, its how progress can be made when an authority will not listen to the masses.

I'm sure the banks would be totes patient and generous and understanding about the non-payment of all those highly leveraged rental mortgages for a few years while the Tribunal tries to climb out from under a backlog of thousands of eviction proceedings and appeals.

more like a few class actions will be derived based on the material circumstances of each case and they'll all be done together. Any loss that can be proved to have been a direct result of tenant action is likely billable to the tenant.

Also in a worst case scenario landlords will lose 90 days of rent (that being the eviction notice period for rental properties in NZ) which will be covered by their insurance. Most landlord insurance policies provide for up to 6 months of lost rent cover I believe.

Yes, I'm sure the insurance companies will be lovely and cooperative about paying out for thousands of cases without trying to get out of it, and all the billed tenants will pay up, no difficulties at all.

when the alternative for the tenants is bankruptcy... (which lasts for 7 years and comes with attachment orders on all payslips)

Insurance companies probably value their clients enough to pay out without too much fuss, especially as it'll be well below their re-insurance limit and people with landlords insurance tend to have multiple policies (home, car, contents, rental property1, rental property2, etc...).

Bear in mind that landlord insurance is essentially house insurance and as such has 6 or 7 figure policy limits and appropriate underlying re-insurance. Additionally in paying the landlord the missed rent the insurance company essentially purchases the tenant's debt from the landlord and can then pursue the tenant for the money.

Well in that case, don't worry your pretty little head about it. It's not as if you've got more to lose.

I hate to say this...but it might be time to get the hell out of Auckland or NZ...I know it's not solution but no one should be subjected to this. I have half a deposit and my GF has the other half and even I feel hopeless. I went from less than 10k savings beginning of 2015 to almost 55k today. This country is F'd mate.

SpaceX, I am bit surprised that no suggestion has been made to you about investment in gold (or even in bitcoins)

Where is the house, Gordon? Sounds lovely. Is it high end? There are some very smart places not shifting round us. Vendors asking for silly money and it only seems to be nosey locals turning up at the open homes.

Prime 3/4 acre home with harbour views is not your typical home. I believe Gordon once said it was around two million but it would be interesting to know what the CV is. My feeling is that such a home is worth around 20% over CV. Desirable typical low to mid range homes in Auckland with no issues are selling for 30-50% over CV.

I'm thinking it's off the SW mway with a peek of the manukau. Better of building a couple of houses then selling them all of separately. .

Why give that assclown the publicity he craves?

Got to give credit where it's due. I was optimistic about a flat market that would finally let me get a house...but nope. All that hope diminished now. It's frustrating.

February and March are always peak months.

Hong Kong Phooey said May would bring the return of the money launderers, not February. No credit due.

He was just advertising his little landlord school anyway.

Last year the market was still going bananas in May, no reason to doubt that won't happen again.

Probably. But this March doesn't feel as stupid as last March. Less money launderers around so far.

For anyone who wants to know some "real/honest" under the hammer results -

B&T auctions this week:

Bays and Central 8 sold from 14 = 57% success

Manukau 14 sold from 28 = 50% success

The authentic numbers tell a slightly different story.

The news coming out of Melbourne apartment market although slightly sensationalistic in the way it has been reported certainly will make people more cautious. Prices tend to go down much faster than they go up.

As a matter of note London Property statistics are showing Chinese buyers are about 25% of what they have previously been. From what I hear that is probably fairly similar to what is going on here.

Auckland listings have dropped 11 percent since end 2015. As to whether that is due to property being removed or sold the upcoming churn rates sale vols will offer insight. As an aside Waiheke Island has surged in price and listings have plummeted. Land has become very scarce . For many relocating Aucklanders and migrants Waiheke may potentially offer significant upside

Where is the house Gordon?

We need the figures to assess the situation! The auction results tell us a different story to Gordon and ex-agent. All around me the signs have big sold stickers on them. Some houses sold in two weeks. I'm not really a spruiker either, I actually want them to cool a bit and stabilize.

In a place the size of Auckland you would expect some houses to sell. The REINZ monthly reports have been telling us for some time that the sale volumes are down in numbers from their peak. In Auckland that is.

Yes I agree, we really need to get clarification on what is actually happening with the housing market (Even if the focus is on Auckland)?

So we all know there's been two main factors that drive the housing market. 1) Overseas investors; when the new regulations came in to force last Oct the Auckland market dramatically dropped by around - 8 to -10%.

The other main market driver is First Time Buyers; These have been more recently encouraged back in to the market by banks lowering interest rates (Plus the bank of Mum and Dad), which I think is currently propping up the housing market.

So to get clarification on the situation. Is there any way to get the recent figures on Overseas Investors now that they have to register their purchase here?

My house is being sold by auction on Saturday. Trust me. There's no shortage of buyers in Auckland. First home buyers and investors. Auckland is pumping.

Please report back and let us know how it goes.

I can tell you now. It will be sold for three times what I paid for it a handful of years ago.

That's my retirement sorted (at fortyish).

And for the grumpy naysayers, this was my first house. I scrimped and saved on one income to buy it and every week was a struggle in the first year. It's never been easy. I won't ever be easy.

But there's a place for everyone who wants one. You just have to really want it.

Sounds to me like its three times harder than a handful of years ago...

Well there's one thing for certain. It won't get any easier. Simple economics tell you that.

Simple economics - what an oxymoron!

Why are you selling if you are certain that it won't get any easier? Would that imply you think houses are going to become more expensive? And that salaries will not. And yet you're selling.

I'd guess thst you bought post gfc when prices were still subdued, you had less than 20% deposit before banks tightened up on fhb, and that you got in a semi decent outer suburb with a decent plot of land, say 600sqm. Ask yourself if you could buy anything now with that same deposit?

The goalposts have moved further away and gotten narrower for a lot more fhb these days so don't assume we don't want to work for it, it's just a different market we're up against. .

We're up against greedy and unpatriotic New Zealanders and Chinese foreign buyers. Just give up and move to Perth.

And you are one of them....

Why am I one of them?

Well I hope you don't have children otherwise you may find that you have to down size or give up your retirement plan to help them afford a home in NZ.

The market is just as tough. I had a student loan and 20% deposit that I saved by working my butt off for. I also bought in a very average suburb a shoebox on a postage stamp. The GFC didn't affect my suburb so prices never dipped. The problem with those who assume is they also moan. Just get on with it. There are houses for sale everywhere. I saw an opportunity and now I see the opportunity to sell up and diversify my portfolio. I can buy three houses in Tauranga with better yield. Why wouldn't you.

I love how Joe Average kiwi investor thinks that diversifying means to own 3 properties in a city instead of one.

We are walking, talking, financial comedy!

You should change your username to Bootstrap Yourself.

why don't you get a job instead? Or start a business? You know, something good for society? No. screw everybody else.

This diversified investor has shares, bonds, overseas market investments and additional Auckland property as well as high yielding rentals. I call myself diversified. Yes. I am simply adding to that diversification. But thanks, again for assumptions.

Only problem is the house they own represents a large portion of most people's wealth. Most people do not have much in the way of "other" assets. If you want to invest in property buy units or shares in the listed property companies, otherwise there are heaps of good company's to invest in.

The whole market thing comes down to one concept supply and demand - look how things have changed in the dairy industry, oil, metals .....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.