The price of Auckland homes auctioned by Bayleys in the last week ranged from $405,000 for an apartment in Grafton to $2.22 million for a waterfront home in Devonport.

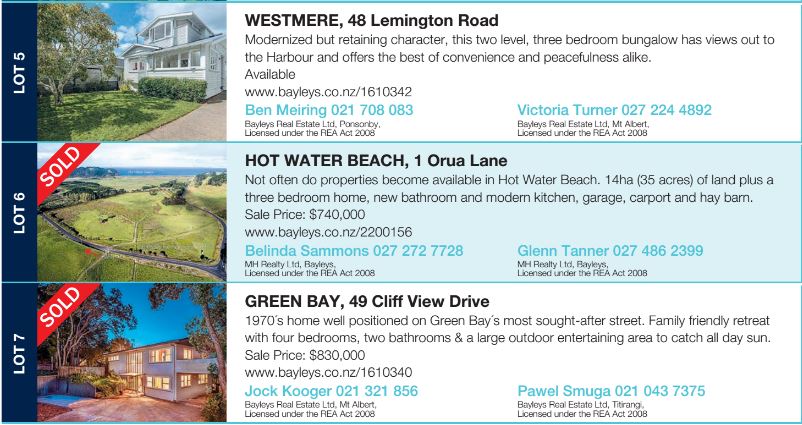

Included in last week's auctions were a three bedroom house on a 14 hectare lifestyle block at Hot Water Beach on the Coromandel that went for $740,000 and a refurbished 1960s-era two bedroom home unit in Herne Bay that sold for $1.125 million.

In the Hamilton auction room a modern three bedroom house at Leamington achieved $520,000.

See below for the full results, with photos and details of all properties, including those that didn't sell:

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

69 Comments

2017 seemed like the year of 1mil average for AKL. Now with the potential OCR cuts - 2016!

Still can't believe 35 Kiwi Road in Devonport sold for $1.82m considering the house is only 100sqm on a 360sqm land with no garage!

Have a look here:

https://www.bayleys.co.nz/Listing/Auckland/North-Shore-City/Devonport/1…

Apart from a new kitchen, the rest of the recent 'update' was no more than a lick of fresh Resene paint and staged furniture.

The trend I'm getting from this is that in the current market, a modest 3-bed 2-bath 1-living property on a smallish section with a smallish garden would go for between $1.7m and $2m in an established leafy suburb, probably be in the higher end of the scale if it's within the double grammar zone in Central Auckland.

P.s. I'm sure Zachary would agree with me ;-)

Please don't read this comment if you are not interested in making money from houses as it will be boring or upsetting and seem a little bit obsessed.

Yes, also it does appear that focusing on making the property immaculate pays dividends.

Another in the list like this is 36 Coyle St in Sandringham with a CV of 890K going for 1,825K - eye watering really.

https://www.bayleys.co.nz/Listing/Auckland/Auckland-City/Sandringham/17…

A house I am interested in is the Te Atatu Peninsula selling for 787K with a CV of 530K =50% over CV. I bought something similar a year ago with no shared driveway. I reckon standalone houses with nothing shared will always be hot property in the super-city. Especially now we have the Waterview Interchange just about ready.

https://www.bayleys.co.nz/Listing/Auckland/Waitakere-City/Te-Atatu-Peni…

The Sandringham property looks really sleek and almost glossy in my imagination. I love a study-nook that can be shut off by the kitchen/dining...it's really handy :-)

The Te Atatu property with a shared driveway did well for fetching $787k considering the newly renovated standalone property from Our First Home ( https://www.barfoot.co.nz/566627 ) only went for $800k.

Same CV at 530k on that one. Quite funky.

Te Atatu has gone a bit crazy recently and I too suspect it has something to do with the biggest road project in NZ aka Waterview.

( a 3 bed house in Te Atatu without storm water went well over 900k a week or two ago as per a BARFOOT agent )

Next stop Massey. (Watch that space)

Massey went crazy last year. Though I suspect the averages were influenced by a lot of new build activity. No matter how much you pay, its still a hole. I grew up there.

Ah, thanks for the insight Xelnaga

Oh yes - three bed, fully fenced = hot hot

For that kind of money - I am sure it's not someone like me doing a 9-5 job. Offcourse unless this city is filled with executives and CEOs Or buyers with massive equity which is highly likely.

The comment from my collegue who is actively looking is - 'buy whatever you can'. Desperate or clever? Only time will tell.

But again it's not just an AKL thing. Other parts of the world experiencing the same.

It is a tricky question. A lot of punters on this site chose not to buy some time ago and this has left them something like 500k down. So they have an awful lot "invested" in their theories. The trouble with Auckland and some other cities is that you cannot afford not to buy.

I can see that this situation is difficult for those that simply cannot afford to buy but for those that could buy and chose not to and kept renting it must be a special kind of painful.

Being able to "afford to buy" is not the only consideration. People are actually fearful of losing. It's all part of prospect theory.

three bed, fully fenced = hot hot

Also two bedroom with internal access garage. Lots of singles, childless couples and retired folk in this market.

Yes agreed, lots of DINKs :-P

There is major competition for family homes driving up the prices to $2m but larger higher priced properties are struggling and vendors having to drop. You get more value if you can stretch much above $2.2ish.

The property in Green Bay selling for 830K looks like quite a good buy. Is that part of Auckland a little under priced currently? I see someone turned the garage into a fourth bedroom. Was That a good idea?

https://www.bayleys.co.nz/Listing/Auckland/Waitakere-City/Green-Bay/161…

Personally I prefer a lock-up garage with a work shop more than a 4th bedroom, especially if it is downstairs. However if I can have both that would be icing on cake :-)

Yes, me too. I have a lot of ladders, tools and stuff to put away. Kids have bicycles etc. Elysium houses need places to store the toys.

What do you think of this one?

https://www.youtube.com/watch?v=uDaxfTB38jo&feature=em-uploademail

The tennis court is right next to the neighbours...not very practical you would have thought with tennis balls flying left right and centre.

Looks like probably above 5 million. Strangely long and narrow site. The tennis court makes good use of it as otherwise , for me, it would be disturbingly proportioned.

Yes it's one of the suburbs like One Tree Hill. Not as big as most other suburbs and hence bit under the radar with not not many listing. I think they have now already caught up in terms of pricing. Not sure about the house in question TBH.

ZS - Green Bay is a hidden gem. Much better family living than Titirangi. Close to New Lynn as well as great west coast bays and beaches. Increasingly good schools. It's beyond the New Lynn SHA zoning hence the lower prices but in terms of great family homes in an excellent family suburb Green Bay is a top pick.

Why were B & Ts numbers so low last month?

Clarence68, I assume you mean compared to the numbers above? If yes then comparatively speaking its due to the suburbs that they mostly deal in. My theory is that Bayleys is mostly dealing over the shores and more affluent suburbs while B & T is also across Waitakere, South etc.

So slowing down in the South and West but still strong in north and Central?

Averages in central and shores is higher than west and south - hope that makes more sense.

Anyways, thats what I think, others may have better insights.

That land and house at Hot Water Beach looks like the best value by far. I would have bought that.

Y and Z would have been horrified to read in the NZH this morning that a Papakura home has gone from $335,000.00 to $590,000.00 in nine months and changed hands five times. This will be a tip of the iceberg. IRD would be curious and will hopefully look to see if all income was returned on those transactions. I presume not much if any was. Where is our National, Local Body and RB leadership? No wonder Y and Z look upon X and the Boomers as being greedy and who have screwed their futures housing wise. Today's article says it all. Reminded me of sharks feeding in a way. I suspect the elderly lady who sold it privately in the first transaction was sown up and ripped off by her buyer. I hope someone looks into that also.

'But at the end of the day' Gordon, this is the cost of being being successful and doing well. So we should be celebrating this and not be at all concerned about it...

If this is success what does housing failure look like? It is simply unfair. Especially in Auckland and Queenstown/ Wanaka and you were born in the years 1945 to 1985 or so you were lucky in terms of housing. If you are unlucky enough to be born from 1990 or so to now you are stuffed in terms of housing in those areas unless there are two of you, have two great incomes and/or a rich mummy or daddy who can help. Timing is everything as they say. I am one of those who were lucky to be born at the right time and I can house my kids who are equally lucky. ZS/DGZ is still to answer me. If he was a Y could he get together 4 houses in Auckland today and if so how could it be done. And get through a marriage break up. She had a lucky escape from a cruel thinking supporter of Trump in my view. How did he get a second. Probably Russian.

I have a wealthy mother. She won't give me anything. I think any inheritance will go to homeless cats.

You should be able to successfully contest that, should it occur.

Gordon, life has always been unfair. People have to play with the cards they are dealt (I got four aces!)

What about the poor young people who were born in the 1920's having to face the great depression and then WW2?

I think I have expressed my views and political leanings reasonably clearly.

My viewpoint currently is that the current generation don't have much hope and they are a bit of a lost cause. We cannot return to a traditional way of life because no one wants to, especially young people.

Neo-feudalism sounds rather good to me. I am applying for a Lordship. Feudalism wasn't all bad. We built great cathedrals and went on crusades. Even rural life and tradition had its good aspects.

Perhaps the new cathedrals will be the super-cities?

We build another kind of giant useless monument to superstition. How's that SkyCity Convention Centre coming along?

Kakapo, with all due respect, you are the type of person who epitomizes the typical citizen of today. The reason why I have given up hope. The great cathedrals are giant useless monuments to superstition? They are the epic foundations of the greatest civilization ever.

Under neo-feudalism will you be Lord, priest, merchant, mason or serf?

Before you get any serfs, I advise you to familiarise yourself with s.98 of the Crimes Act 1961.

Serfs aren't slaves. They are cherished and protected by their Lords and the feelings are reciprocated. Don't believe all the silly propaganda the Victorians made up about life in the "Dark Ages".

You haven't done due diligence on the legislation, have you. Too lazy without a serf to do it for you?

You're right i searched the Crimes Act 1961 and it mentions serfdom three times. How about that?

The Crimes Act is fab and has all kinds of whackiness in it that may be left over from its predecessor, from 1908, if memory serves. I also recommend having a look at the section on Piratical Acts, just for the LOLs.

don't forget Bandits who love to cut Lord's throats...

I'm intrigued so I'll ask - how is this "being successful and doing well"

Current National party stance on NZs inflated property prices.

It made me feel sick. The elderly and young are the ones who will taken advantage of most at the moment.

Hey but just make sure you lock in those capital gains tax free asap then get them into a Trust.

Will you stop lumping X in with boomers FFS? It's nonsense. X had the 'good fortune' to start work in a severe recession where they had to take whatever low-paying opportunities were going, and were hammered by student loans with compounding interest from day one. Not so easy to climb out from under that and get a deposit together in time before the bubble kicked off. That's why X generally have the backs of millennials in this mess, because they were effed over in the same way, and have empathy with the poor sods starting out now. X were unjustly smeared as slackers, Y are unjustly smeared as entitled brats. It's the same silencing tactics from the vested interests who want them to just shut up and hand over their money.

When did X face 10 plus times to buy houses? Timing, when you were born, is everything.

You are both right. I think X can be divided into early-X (born 60's to early 70's) and late-X (born mid 70's to early 80's). Early-X's are the ones Gordon is referring to and the late-X's are the ones Kakapo is referring to. Happy?

With Y there seems to be a split like the one between early and late boomers. The ones who started out before GFC got a pretty good start, but the ones who hit the job market after 2008 are doing it hard.

But it's all putting hard divisions and artificial categories into something that's really a continuum, so pinch of salt, and probably much less impact than the socio-economic class lottery.

When did X face 10 plus times to buy houses? Timing, when you were born, is everything. X started in 1965 so some now 51 years old. My greediest clients were from X not the boomers.

They are now, if they were still saving when things started getting out-of-whack around 2002. Those compounding loans, and the recession, were a real handicap.

I absolutely agree it's a timing thing, and X got unlucky in that. But they were even more unlucky in the big numbers game of bribes for votes, because they don't have the numbers to be worth targeting policy at, and that too-small-to-bother-with factor endures, whatever the economic situation. Gen X know they're on their own and will have to look after themselves. I'm entirely confident that when retirement age is raised, and means-testing for superannuation brought in, it'll be carefully timed to hit gen X, so that protest is minimal and it's bedded in and normalised by the time the Y's come through.

But I hope that Y's will do better, just through being another large demographic bulge, and a potential voting bloc worth courting. They were targeted with the interest-free loans policy, so perhaps will again with housing policy. If their collective parents back them up. Admittedly, that is a big 'if'.

Sydney houses forecast to be bought up strongly by Chinese

http://www.domain.com.au/news/chinese-buyers-to-reach-new-record-in-201…

^ oh joy. Just when we thought things couldn't get worse. The AU is weak at the moment isn't it?

The locusts

No property bubble burst, while floods of foreign buyers, Foreign Trusts buying property, immigrants, and panicking NZ buyers keep buying.

If 'Supply' was the issue then why is Sydney sky high with many apartments supply to choose from? Tauranga, Napier, Hamilton has plenty of 'supply' - but prices climbing strongly. So 'Supply' is not the issue. It's huge and insatiable Demand.

Perhaps it's the wrong type of supply.

When you have some buyers in a market who are not particularly price conscious then increasing supply is not going to lower price.

Isn't that the definition of a bubble?

Perhaps it is deja vue. Again and again and again...flipping heck.

http://www.marketwatch.com/story/the-next-housing-crisis-is-pending-201…

This is interesting http://dailym.ai/1s2R7Iw

Interesting video. This YouTuber has a lot of good stuff:

Intergenerational THEFT via Boomer Ponzi Scheming Economic Vampirism

I see from Stuff his morning that the boomers and X have been very busy in Queenstown. Not only have they pushed up the price of houses and rent they also pay them two fifths of you know what when they want the millenials a to work their businesses. You cannot have it both ways. High staff turnover and staff disatifaction has to be the order of the day. That is if the big new businesses can get staff at all. I suppose they can live in tents.

there are going to be some sorry looking faces around town in the not too distant future. what goes up ....

Been hearing that since 2004. Know what side of the trade Id rather be on.

It is a fact that there are a lot of sorry looking faces among the crowd waiting for property prices to come down.

Ohhh its coming Zack, just wait until {insert some thing that never happens or will have no effect here} then there's going to be a 40-50% correction and you'll be crying into your cornflakes.

The amazing thing is that you really truly believe that it could never ever happen and are prepared to state this publicly. Why do you think the RBNZ is so nervous about hyper inflation of houses?

The GFC was the worst event since the Great Depression. I think we all agree it was pretty bad. Loose lending for the better part of a decade caused it. During that time Auckland dropped 15% for about 18months. What do I see now? I see very strict loan requirements, a rate tightening cycle (as you pointed out will only make prices higher) , I see huge immigration and hardly any supply so no - I dont see a 40-50% correction coming anytime in the near or medium term. Graeme Wheeler needs to worry about doing his job which is meeting inflation targets. He needs to cut rates now.

Not just about inflation :

Per the Reserve banks website:

"One of the Reserve Bank’s core functions is to promote a sound and efficient financial system.

There are a number of ways the Reserve Bank helps to maintain financial stability, including through the regulation and supervision of banks, non-bank deposit takers and insurers, promoting the smooth operation of financial markets, and building sound financial market infrastructure.

It is also important to understand developments that could make the financial system vulnerable to instability, and respond appropriately. The Reserve Bank conducts regular surveillance of financial risks and reports on its assessments in the six-monthly Financial Stability Report."

WIth private debt growing at 8% per annum and 200bn + outstanding it is time they opened up their tool box and reined in this excessive lending practices. 50% LVR and Loan to income ratio's of 4 to 1 should do the trick. (NZ wide)

To date they have failed completely.

The point is anything can happen and the higher prices rise relative to income the more unstable they are. No one knows the future and wealthy property owners making great proclamations about how their wealth is just going to grow exponentially to those who are in a less affluent position is just screaming 'pride comes before a fall'. I would just keep quiet if I were you.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.