The shine has come off Auckland's residential property market, with sellers still wanting top dollar for the properties while buyers are being more fussy, according to Realestate.co.nz.

Auckland was the only region region in the country where the number of homes listed for sale on the website (inventory) in October was up compared to October last year (+1.4%), while inventory was down by a whopping 24% in all other regions.

However while the number of homes available for sale in Auckland was increasing, giving buyers more choice, the asking prices vendors were expecting were also continuing to rise.

"[Auckland] homes are spending longer on the market," Realestate.co.nz chief executive Brendon Skipper said.

"Vendors continue to be focused on selling at a premium while buyers are being more considered and taking time to assess all their options.

"With more stock on market, buyers aren't feeling the same pressure they were 12 months ago."

If no new properties were listed on the website, it would take 12.5 weeks to sell all the Auckland homes listed at the current rate of sale, compared to just 9.3 weeks back in May.

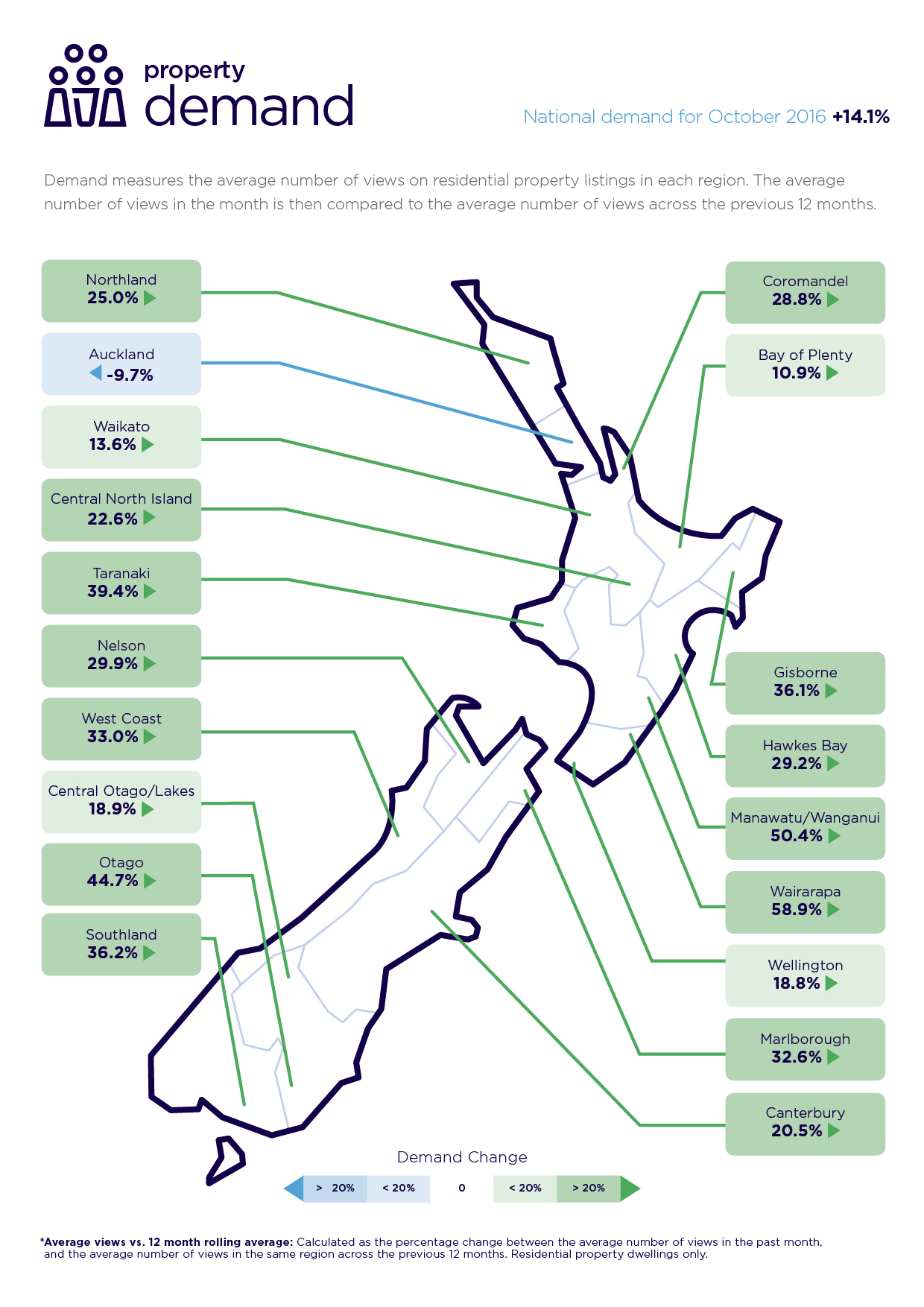

The number of times Auckland properties were being viewed on Realesatate.co.nz was also down 9.7% in October compared to the average number of views in the previous 12 months.

That compares to an overall increase of 14.1% nationally and some huge increases in interest in some regions.

The biggest increase was in the Wairarapa, with the number of views of properties in that region up 58.9% in October compared to the average over the previous 12 months, followed by Manawatu/Wanganui where the number of views was up 50.4% in October.

Auckland was the only region in the country to record a decline in property views in October, while all other regions of the country recorded double digit increases.

39 Comments

DonKey and his cohorts will not be impressed by these figures for Awklund - cue the floodgate to open for wealthly immigrants, who can't get into the States, Canada, UK and Australia to be let in, to again "pump the market" .....come on all you Nats, get behind your leader and get your Awklund property on the market and keep the Nats,banks, RE agents and hangers on happy !!!

It's good news there is finally some cooling off, though it seems more of a spread from Auckland to the rest of the country. Just means people in those regions wanting to buy are likely going to be paying a premium to do so as prices likely rise with demand.

Investors now finally need some cash to buy and they can't buy against other properties anymore (to a degree...). FHB are out of the market in Auckland and 'normal' buyers will buy and sell at the same time.

It clearly confirms how unnatural investor/mortgage/overseas buyers the whole Auckland market is driven...

How this plays out?

1- The rest of the country is capable of building homes in response to additional demand (price of land is sane in bits of NZ not called Auckland), so whilst there will be price increases these will be smaller than Auckland.

2. The additional building created in NZ will mean an increase in employment and wage growth which will fuel inflation.

3. Increased inflation will cause interest rates to rise.

4. Interest rates will place stress upon high debt households who have purchased in high cost Auckland.

Conclusion - NZ is in for a bit of a economic boom and Auckland is rooted.

#1 does the rest of the country have to build homes to keep up with demand, or is existing stock enough to satisfy? Some areas are 'booming' e.g. BOP with a lot of building ongoing, but the smaller areas around the country...who knows.

Is there any data on building consent trends over the last few decades up to today?

Probably yes it can but it will require wage growth, I've kind of worked it out the other way.

Auckland is currently building about 70% of the houses it needs to build to keep up with its demand.

Waikato and Bay of Plenty both are building (or issuing consents for building) at a rate of about 8 dwellings per 1000 people per year. Auckland is issuing building consents at about 6 per 1000 people per year.

The difference in current building rates would appear to suggest NZ (apart from Auckland) will build enough to cope with Auckland type population growth, when the rest of NZ is given a higher price signal.

Investors locked out of Akl due to actually needing some equity now, Chinese on a go slow for severals reasons but akl property not the safe gamble it was, immigration reduced from the fire hose has been, Jaffas fleeing to the regions as economic refugees, and govt being forced by public opinion to restrict access to the ponzis junkie like need of more debt. Pumpkin patch was strangled by to much debt, shame investor losses cant be claimed against personal income tax like other forms of investment.

All that before the trump card, chinese debt issues, indian students confirming study must have guranteed citizenship or they wont come, and a NZ rental slave revolt building up speed in time for the next election are even considered. See http://www.metromag.co.nz/current-affairs/housing-ponzi-turns-septic/

Who will be around to bail out the ponzi...?

Good article. Who wants to invest in a rigged system?

Obviously being a sub editor of Metro leaves not much in the tank for critical analysis of Auckland property market. With misinformation like this being written then any victim will pick up on it. As long as there is religion then my belief is people will believe anything. I really do see a scurge in modern thinking with nonsense like Ponzi in their writings when speaking of open and transparent markets.

Negative yields = Ponzi finance.

You just come across as foolish by calling it a Ponzi all the time.

Educate yourself.

It didn't mention Ponzi once in the body of that article.

Minsky described 3 forms of finance which arise as an investment cycle matures.

1/ hedge finance.. ( cashflows covers costs, interest and principal is repaid )

2/Speculative finance ( cashflow covers interest payments eg. normal interest only loans)

3/ Ponzi finance ( cashflow is insufficient to even pay even interest costs... Totally reliant of capital gains, and the greater fool theory )

In the context of "Minsky".... in regards to "ponzi". u can see the term is often misused and used out of context.

My guess is that there would only be a few people buying houses based on "Ponzi finance"...??? but I dont really know..

( And I would consider "cashflow" to be the total cashflows of any purchaser...not just the cashflow of a particular property ).

" Ponzi " gives Bubbles a bad name !

Thanks for that Roelof - much more sensible. Total cashflow is the way to look at it I believe.

Agree there on that one Keywest, however in this case I think she has capture the undercurrent of real public concern on this issue quite nicely. Never something to be blindly ignored going into election year.

The process of bubbling up prices with successive sales to the next speculator/risk taker I mean investor, is ponzi like in nature, as what happens when the music stops and there is no one to take the last sale? Just like musical chairs you fall over and land on your a##.

Lets also not forget that the bright line test is 1 October 2015 for two years must pay tax window. I wonder if that will have a bearing on whether we have an early or late election, especially if DTI or disadvantaging overseas buyers (Que Winston) becomes and election sizzling hot potato...

It may be a Ponzi scheme but anyone who bought into it 10 years ago now cannot loose, doesn't matter what happens to the market. If you bought a house in Auckland and your smashing your Mortgage on the current low interest rates you made the right decision, end of story. You can keep on babbling away about ponzi to try and justify why you didn't get on the property ladder but your just fooling yourself. One thing for sure is that the vast majority of FHB are now locked out of the market. Unless both you and your partner are on really good money your pretty much stuffed. No regrets here, going to retire early with the house already paid off.

The RBNZ and not grace has been your benefactor,

Buying in a desirable location was the key factor.

The question is will Auckland be the desirable location in 5 or 10 years time?

Auckland has spent this entire boom not building anything and will end up with a selection of cold un-insulated ancient housing on offer at extortionately high costs. Every competing city will have housing which is modern and plentiful.

Auckland might be exceptionally undesirable at the end of this boom.

Desirability was a key factor and will continue to be a key factor for the foreseeable future. Auckland is New Zealand's premier city and a transport and tourist hub. Air travel is set to get cheaper with the new economical long haul jets like the Boeing 787.

I'm all right jack. - says Mr. 1967

You bet mate, I took the risk and worked my ass off for 10 years in crap jobs this country specialises in and at times 80% of that crap money was going into the Mortgage, so yep I'm all good now thanks.

"now cannot lose.."

Carlos67 - have you tried eating a house? When the economic Ponzi collapses all value will be lost.

I'm sure Carlos67 will continue to see great value in owning a mortgage-free house even after the "Ponzi collapses". Preppers still need somewhere to store weapons and provisions.

whether your house is mortgage free is and will be irrelevant (near zero interest rates reinforce this point). Your comment shows an underlying assumption that some sort of reset will occur, where bad assets get picked up by another entity and aay we go again.

Debt wise, we are at a point now where paying off debt is truely the wrong thing to do - and its actually exactly what the central banks need everyone NOT to do to buy everyone more time. They need consumption growth => debt growth => commodity demand to hold. A deflationary spiral in commodities(read Oil) will crash everything. Asset inflation is neither here nor there, its all about spending.

The flip side question is, is this the best thing to do for my kids/grandkids ..? The answer is absolutely not, but there is no stopping now. Its either grow or collapse.

hamneggs

Ok.... You state the obvious.. ..and yet what u say is as meaningful as saying that when WW3 comes asset prices will crash....

Tell me when u think this is going to happen, and why ?? share your knowledge.. Do u know something we don't know..??

for me... I've learn't the hard way that the Giant economic forces are like the Titanic.... they take forever to change direction... AND... the giant economic forces are Central Banks and Govts.... I've learnt to be very cautious betting against them.. ie.. They will do ANYTHING/EVERYTHING to stave off the the ponzi crash u predict.... too maintain the "satus quo ".

( eg... Helicopter money might be the next form of Monetary measures )

Nicole Foss has been waiting for her 90% house crash prediction to come true.... since 2009 ..

since the early 1970s' ... the " ponzi economic world ending" has been preached every decade..

(one of the most freaky times were the mid 1970s' ..from what I've read )

I'm sure there are people who have held off making investment decisions for the last 40 yrs , because they were waiting for the "Big meltdown"..

I don't have my head in the sand.... At some point you will be right.... but how many yrs will u cry "wolf" before it happens,,..????

I agree, the momentum holding things together when logic says it shouldn't is easily underestimated. But a lot comes down to misplaced faith that it must hold. Near zero interest rates show we are close to game up.

The last 40 years have been about debt growth in place of real growth, and interest rates going ever lower.

A housing price collapse wont happen because when it does the game is over. So you are absolutely correct, they will throw everything they can at it to keep it afloat.

A comment saying mortgage free homeowners "cant lose" and can relax into retirement is unfortunately a fiction. It all comes down to when the energy supply chain is disrupted.

"the only surplus that exists can only be a surplus of energy. Money can be printed, so a surplus of money is a nonsense. Money only buys access to more energy. If there’s no energy available, money has no value...

Wealth creation only worked if oil production continued to increase which explains why real wages have stayed around the levels of the 70s/80s.

Everyone believed it was forever. Nobody believes the oilparty is over."

You're wrong:

If you bought a house in Auckland and your smashing your Mortgage on the current low interest rates you made the right decision, end of story.

Auckland has a very slow building rate for a city of its size, but there are plenty of other cities and young people can move. Compared to any other city in our region Auckland is the construction dead zone.

One thing for sure is that the vast majority of FHB are now locked out of the market. Unless both you and your partner are on really good money your pretty much stuffed.

Your problem is that FHB aren't stupid and they can work this out too, so when the Aussie economy picks up FHB are going to move there. They will then be getting better money and living in a home that they can own.

If/when FHB start leaving the Auckland property market, we will have an immigration pattern very similar to Adelaide's. Adelaide's median house price sits around $350,000-$400,000 - good luck retiring on that.

Adelaide is not a transport and tourist hub while Auckland is.

Auckland is not transport hub, it is a regional city servicing a population about the size of South Australia. And Adelaide is a lovely place to visit, got some great wineries nearby.

Auckland is NZs premier city because it grew much faster than any of the others, but now Auckland's building rate is terminally slow. We are being out competed by most cities in the region. Why should FHB buy here when there are so many faster paced, quicker developing cities they can move to?

If you're a first home buyer in Auckland with a decent deposit, what do you do?

Wait for a crash and hang onto my money, or buy in and risk having my one and only asset plummet in value?

Or will the lack of supply mean the crash doesn't happen?

Honestly no idea what to do anymore.

You should work to change the institutional systems that tilt the playing field in favour of incumbents and away from FHBs such as:

- negative gearing for investors

- bias of banks to lend toward existing home owners

- lack of requlatory limits on lending particularly to investors;

- artificially low interest rates

Lax lending is not your friend, it is the cause of your difficulties

Yet these same practices are building a plethora of new housing choices for FHB in Brisbane, Melbourne, Perth, Tauranga. Why can't we have those choices here?

The only institutional problem we face is called Auckland Council and its decision to price Auckland land 2 or 3 times higher than it would normally be. Auckland median land costs are higher than Melbourne's, this is by every conceivable measure is bat droppingly insane.

Appreciate your sentiment. If only we were a voting mass, but unfortunately Gen Y drew the short straw.

I'm like you, I have a decent deposit and would like to buy in the Auckland region. But I am not going to.

Because lack of supply is a myth.

Lack of supply is not a problem in the Australasian region. Brisbane, Melbourne and Perth by the end of next year will have a surplus of housing, these cities have built twice as fast as Auckland for years. Currently BoP and Waikato are building significantly faster than Auckland, and they are starting to really ramp up supply.

Lack of supply is a complete myth if we are willing to do one simple thing.

Move.

Unfortunately that's the one thing I'm not willing to do!

Lol.

In Manukau was rising but since last 10 has been fjpalling. Was appox 2190 and now is appox 2090.

April to June is important.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.