Regions around Auckland risk being caught up in a housing market bubble and Auckland property investors are probably to blame, according to property information website Homes.co.nz.

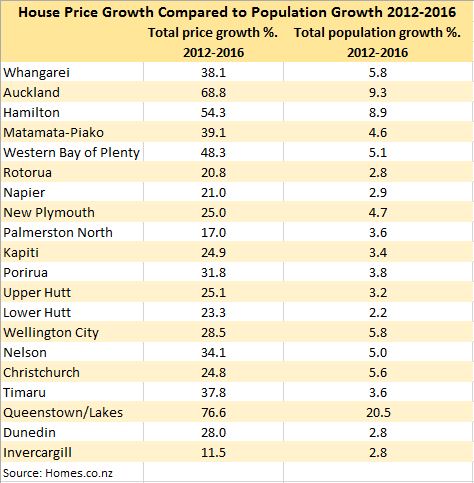

The website has compared the rate of growth in median house prices around the country from 2012 to 2016, with the rate of population growth over the same period (see chart below).

"The data suggests that neighbouring regions are at risk of being in a bubble, and Auckland investors are likely to blame," Homes.co.nz said.

"While Auckland house prices have grown fairly steadily since 2012 alongside steady population growth, neighbouring areas have seen a huge spike in the last 12 months that has clearly outpaced any pressure from population growth.

"For most regions within a couple of hours of Auckland, House price growth in the last 12 months has outpaced population growth significantly, putting questions around what sort of bubble the housing market in these areas could be in."

Homes.co.nz spokesperson Jeremy O'Hanlon said speculative investment activity was probably to blame.

"If there is no fundamental change in the demand for something and prices start sky rocketing, it's reasonable to assume that speculative investment is the culprit," he said.

78 Comments

Is The Herald running some kind of Bob the Builder - Yes You Can campaign?

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

What's funny about this is that they must be churning them out in a hurry. It starts like this;

... Today, the couple have just sold their first property, which was bought in Matamata in 2013,..."

And then goes on to say this:

So they changed their priorities and began working and saving hard, and within a year managed to save a 20 per cent deposit for four-bedroom Matamata property, which they bought in February 2015 for $330,000.

Just last week, they sold it for $410,000.

But Clayton said they didn't buy it to make money, but more so that they could use it to leverage a mortgage on an Auckland property - which they managed just three months later.

I'm confused - were there two Matamata properties, or one? Was it (or they) sold today or last week? And if you buy a house specifically for the purpose of using it as leverage on another asset - and then having achieved that end, you sell it - is the sale subject to CGT?

NZ Herald is owned by NZME, which is owned by APN. Real estate is a key revenue driver for media organizations across Australia and NZ. Ours has always been lighter on the hard sell than across the ditch. The editorial force is steadily transforming.

Housing crisis? What housing crisis! Two more from the herald with the same theme…

How to buy a home before you turn 30: Millennial tradies get a head start

'Toughen up, stop complaining, join the army,' landlord tells wannabe buyers

IMHO the Herald is just the mouthpiece of the Nat propaganda machine.

Dinosaurs! Who reads the Herald any more?

Wow d'oh, there is maybe a global credit fuelled housing boom going on or something.

The only news worth mentioning here is that the regions around Auckland took so long to get involved in the current global housing boom. This delay occurred when NZs 2010-2015 money was sucked into the insane Auckland land price market. From 2010-2015 the land price speculation in Auckland offered returns that beat the global credit fuelled housing bubble. Len Brown blew an even bigger bubble.

However now that land prices in Auckland have stalled NZers are figuring out we can build and make money at the same time - a lesson the rest of the world learnt 5 years ago. Investment is now fleeing Auckland for the provinces, long may it continue.

Well the extent to which you can continually drive the reach and frequency of asset bubbles is unknown. It's fundamental to the economic establishment globally and in NZ, but the implications and consequences are only beginning to surface.

Its not a global house price boom. House prices are only going crazy in some countries where the tax, banking, regulatory and cultural conditions are right to enable it.

Certainly some places are more prone to price exuberance than others, as I pointed out above, no where on the planet had conditions as crazily upwardly inclined as Auckland was under Len "to infinity and beyond" Brown (Lab).

Global interest rates are low and so a boom is occurring everywhere except where there is high unemployment. Some places rise faster than others, some don't rise at all.

And some inflate so fast, right over the top, hit the ceiling and pop way before the others.

Does anyone know what happened to the recent article regarding NZ being the best place to live??

They're a dime a dozen. City and country rankings are how publishers drive revenue and traffic and raise awareness of their brands.

The April Fools article should still be floating around. Tried to direct link and got access denied. Hahaha.

Kate, why would,it be liable for Capital Gains Tax?

The first property was for their own occupation and the 2 year Brightline for tax was brought in well after 2013!!

Don't know that was my question.

The only way it works as leverage is by an increase in value. If I were ird I'd be all over it.

Yeah, that was my question - if one purchases a property for the specific purpose/intent of achieving a capital gain for the purpose of leveraging a second/subsequent property purchase - is a sale of any property purchased for that reason subject to capital gains?

Someone from interest.co.nz ought to ask IRD - and let us know.

I remember reading something about the definition of "income" according to a New Zealand Act or statute thingy. It was something along the lines of that anything that is bought and sold with the intention of making a profit/making a profit counts as income. So going by that then flipping a house would count as income and would be taxed at 30% or 33%. I also read about how the Gubmint wants to tax the capital gains made from the asset appreciation of selling gold and silver.

Seems dangerous then to publicise one's intent to do this in a newspaper for all - including the IRD - to see.

Subsequent retractions likely..."No, we didn't originally plan this, honest."

The article said they bought in 2015 feb... sold march 2017... what a coincidence one month after bright line. However, if bought for gain, still cgt liable

For Christ sake you want to tax someone who has bought a house to live in!,,

The prices would have gone up by far more in Auckland over that time so she is certainly no better off.

Geez, there are some pathetically jealous people on here!,,,,,

I'd use the descriptor of rational myself.

I know more than a few people that shift every few years to generate "tax free" capital gains. I'm a strong proponent of a CGT, even for a primary home, if there was evidence of intent to generate capital gains. The article makes it clear that the intent was primarily capital gains. These gains should be taxed in my opinion.

@TheMan2 --- where did it say anywhere that she lived in it???

Lol, if she bought it to live in then why did she sell it a month after the bright line test expired?

The article never said they lived in it... it said they bought to get leverage... eg capital gains. Pretty sure she didn't earn 200k doing financial security consulting in matamata. Whatever that is. If financial advice, was she registered?

Wow Hamilton is growing almost the same as Auckland!!!thought there was more trafic on the roads!and what about Queenstown it's going ballistic!!!

And National leader says that their is no speculation but only supply issue is the reason.

How in the world can anyone getaway with such justification. Even media is silent and fail to expose national.

Corrupt vested intetest

Election Year.

Asking price of 1 miilion plus very common now in Rototuna,Hamilton.Had a look a 2 of them in the weekend;

(just to see how the other half live) and they were beautiful homes.I don't know how they would stand up to 2/3 kids running around.

The problem is with people wanting over 1 million for their homes a basic 3/4 bedroom home in the surrounding areas is around 550k to 600k far too much for what they are.

Did this story fall down some kind of wormhole from 2015?

The torrent of foreign-related money pouring into Auckland housing is spreading indirectly to other regions.

Surprise surprise.

It's not necessarily a "logical progression."

These inspiring stories of first home buyers really show how straight-forward it is to buy a house in Auckland.

And if these stories are run every day, then the people may be persuaded?

Can you believe they just added another one. Shouldn't there be another angle on this or is the Herald completely biased?

Perhaps political minders or similar have ordered a home buyer story every 2 hours?

Let's analyse this. According to the article:

The house cost $750K.

Amy had $150K deposit.

When Amy is 30 (7 years from now) she can access $100K left to her by her grandfather.

She has a $500K mortgage.

They pay $470 per week on the mortgage.

There is mention of a partner Tegan, but the article does not say if Tegan had any money of her own to help with the deposit. Let's assume Tegan brought nothing to the deal, and the loan is indeed $500K. Presumably, the bank found a way to let granddad's $100K in 7 years for now count as part of the deposit.

A quick go on the interest calculator shows that $500K, at 4.5% interest, would cost $584 per week.

How to get the $470 per week figure quoted in the article? Interest.co.nz's calculator wouldn't let me put in a loan term of more than 30 years. So I lowered the interest rate to 2.75% and that gave $471 per week.

Perhaps Amy has tapped into the corporate bond market as a viable non-bank funding source, as Roger Kerr recommends :P

Tegan is maybe the "flatmate with benefits" maybe paying $120/week rent to Amy

I'd like to see an honest 'how we bought a house in Auckland' article. "We imported hundreds of kilos of ContacNT from China concealed in packets of potato starch. We got it through Customs by bribing workers. Then we forced a chemist to cook meth for us, and distributed it through the local gangs. The cash was piling up, so we put it into real estate, because the government hasn't extended the money-laundering regime to houses."

"I'm a complete moron, and all I do is instagram myself doing idiotic gang signs in my dad's backyard pool area in Parnell. I have a trust fund. Happy Days!"

Here's what that dropkick slumlord really thinks of us kiwis.

{kind=link}

Interesting image - I saved it. I have often thought that praising an ethnic group is as bad as disparaging one. The implication with praise is that one is better and another is worse, two sides of the same coin. I do think that new citizens who come over here and take advantage of decades, nay centuries, of municipal, societal and institutional development may be missing some compassion, missing the big picture. I'm reminded of a conversation I had with one once about New Zealand. He said that Europeans had built a great society in New Zealand, much better than communism, but it couldn't last as it was unsustainable to give such assistance to the poor with so many new people arriving.

Edit: This is great to wake up to this morning:

Prominent Kiwis pen open letter saying free speech is under threat in NZ universities

It is profoundly important that we don't introduce new laws that criminalize opinions. It could turn out that mass immigration results in us losing our great social welfare system AS WELL AS our freedom to express opinions and associate with whomever we like. This is critical to who we are.

This is why I don't think that you and DGZ are the same person. I don't agree with everything you say, but you have genuinely interesting and insightful (albeit controversial) comments to make about the bigger picture, like this one, whereas DGZ just waffles on about house prices and school zones and not much else... like a monomaniac. :)

Basically what he said was:

Chinese less likely to empathize with people they aren't related to

Chinese less likely to donate

Chinese less likely to contribute to society

We don't need people who don't contribute.

My SO went to a Chinese shop in Atrium on Elliot the other week. Came back saying "That's interesting...they offered me a cheaper price for paying cash instead of EFTPOS".

One wonders...stores in central Auckland possibly offering "cashies"? How common is this becoming in retail stores, you wonder. I hadn't seen it before.

Keep your eyes peeled and you'll see businesses with separate tills for cash and eftpos transactions. Way of skimming off the cash without a paper-trail.

Keep an eye on what is being rung up on the till if you are paying cash, I use cash quite often and I can attest that more often than not, it is not rung on the till.

oldest trick in the book been around for years, next time you buy a paper they give you change from sitting on top of the till and not ring it up

adds up x amount of papers sold per day for a year profit not counted

I never buy newspapers

Wow...

He might want to add "more stereotyping than the average New Zealander".

Or - autobiographically - "we marry rich girls and get a $200,000 house deposit from her daddy better than the average New Zealander".

But I'm confused, if all one's characteristics work so well...why would you want to migrate to a society created by inferior people? Surely not because it's better in any way, right?

First time poster, long time reader.

I'm really looking forward to the Barfoot/QV figures which must be due out tomorrow. No conspiracy theories but if they show the first year on year decrease for Auckland, I wonder if Barfoot will try and pip QV like they usually do or just hold them back.

It's worth noting for all the people who say next month will be better that April has some things going against it. It has both Easter and ANZAC day so surely this will suppress buying interest. That has been the claim previously.

While I'm on a roll, those NZ herald articles are awful. I thought the stuff series was bad but the Herald really one upped them. Great for readership though. I forwarded them to my mates and they all read and were outraged. The worst was the fellow who got started with $200,000 from his family. Talk about unrealistic.

Finally, I just want to give a shout out to DGZ-Zach. I love your performance art, keep it up.

I try my best to avoid visiting the Herald, but I admit I often succumb.

I really don't want to pump the revenue of that trash rag, with all its agendas.

I agree; I'm on the point of removing it from my bookmarks, because it's just mostly junk now and flat-out, in-your-face, shameless property spruiking and Daily Mail trash articles. However, there are some good finance/investing articles sometimes (e.g. Brent Sheather, Mary Holm).

A tip: You should only visit the Herald with your browser wearing a full-strength ad-blocker. You really need protection! Doesn't stop the dirty feeling you get afterwards, though...

You can always use http://archive.is to create an instant web archive of the page and post that instead. It avoids giving the Herald ad revenue if you wish to share some of the optimistically titled 'journalism'.

No dgz Zac comments today... he's too busy writing herald articles.

There's some missing information in the statistics. What is the net worth of the people entering those regions? Where will the extremely wealthy baby boomers choose to live in their retirement?

I always thought Taurnaga would do very well out of that transition. Perhaps Bay of Islands or the Coromandel? All have great soil, great weather, great beaches, geological stability, and proximity to Auckland. However, Tauranga is the only one with infrastructure, a bit of a vibe, and hospital facilities.

Interesting the Herald leaves no room for comment particularly for the Asian who attacked, abusing kiwi culture, calling us lazy f*****s whilst feeding of the local renters and getting rich ;) suggest the little C watch his back. Property industries must be desperate, at the bottom of the barrel, years of quantative easing and asset bubbles is probably coming to an end, debt can't go on for ever exceeding GDP and the average earner/family must have affordable housing/roof over ones head for our community to function properly. Do you think the media will revisit these commercially savy property tycoons if the market returns to real economy incomes? Do you ever read of people loosing in property?

(repeated post, please see my reply above, sorry)

I bought my first house in the early 1990s. I had a Ford Cortina and the love of a good woman. Actually, the love of a super hot woman. Everyone talks about the value of my house, but not so many about the value of my wife and children to me. Go figure.

Sounds pretty good. My generation got priced out of having children.

Like everything else we used to make in NZ we just import from China now.

One is very much the max around most of my friends. There are a few with two or three but they are usually lower income earners/work part time. They have the time and energy to look after the kids while getting large subsides from the GOVT. Only one of them is a home owner (god bless. Welcome Home Loans)

Or maybe they put a higher value on family than they do on assets and that drives the choices they have made.

Could be, we had three and love them to bits but some friends have restricted themselves to none or one out of concern for the future environment. They feel pretty cheated with our outrageous open immigration policy.

Auckland 2100: https://www.theguardian.com/global-development/gallery/2017/mar/02/plas…

https://www.theguardian.com/environment/2017/jan/31/bay-bengal-depleted…

>"outrageous open immigration policy"

I believe you meant "National party economic plan".

Easy to say when that "higher value" is supplemented by leeching off the taxpayer.

One can only apply that if the financial incentives are removed from having more kids.

I in no way meant to discriminate or put down their choices, it was more of an observation from my circle of friends.

Can someone tell me how the couple earning $117.000/year is getting $500k mortgage while me earning $150k/year got MAXIMUM of $500.000 ???

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

Different situations. they are a young, no kids, less expense. You probably have several kids to feed, a luxury life style, huge credit card limits and so on. Cancel your big credit card, and willing to save some money. Bank is protecting their own interst.

ZERO credit card spend (do not own one!). I was told it will be 3x my income +/- - im 41 ... is that the case?

Have you tried using a mortgage broker?

Because there is something you arent telling us. Looking at a big bank calculator, it says $150k for joint app with 10 children, yes 10, would still let you borrow $580k. So....

Is your income verifiable? Or is it from 10 boarders? .... is there other debt? etc etc. Apples with apples Jerry.

Population growth for Western Bay of Plenty is given as 5% over that period. What would be much more interesting would be the population growth in Tauranga/Mt. Maunganui relative to house price increases for that period. It would look very different.

First post and not my area of knowledge. But if you divide the price growth by the population growth to get a sense of relativity, seems like areas like Lower Hutt, Timaru and Dunedin have had highest growth in price relative to population? Maybe a sign of people moving to where houses are cheapest, yet limited housing stock? Or effect of lvr rules meaning investors looking for cheaper houses where they can afford 40%?

I don't necessary agree with the headline that

"...regions outside of Auckland ... into housing price bubble territory"

Apart from Hamilton and Tauranga (WBP) all regions have risen less than 40% and many a lot less. Add the fact that all these regions had zero increase from 2008 - 2012 and you get max 12% - 39% increase in 8 years, far from a bubble

In response to the Herald article about Aimee buying the $750K house that is referred to, above.

I have figured it out: if they pay interest only on the $500K loan at 4.89%, that would cost $470 per week.

If that's the case, then is it ''buying''? Maybe it is more like renting from the bank. And, taking the very big risk that either the value of the property will increase in value, or anticipating that Aimee's income will increase over time.

I think you are correct. Even if they do pay capital back they may not regard that as a cost as it is a bit like saving. I never consider the capital part of a mortgage repayment as a cost and if I was describing what my housing costs were I would only include interest, rates and insurance.

Which would be wrong. Paying off capital is not like saving, it's like paying off debt.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.