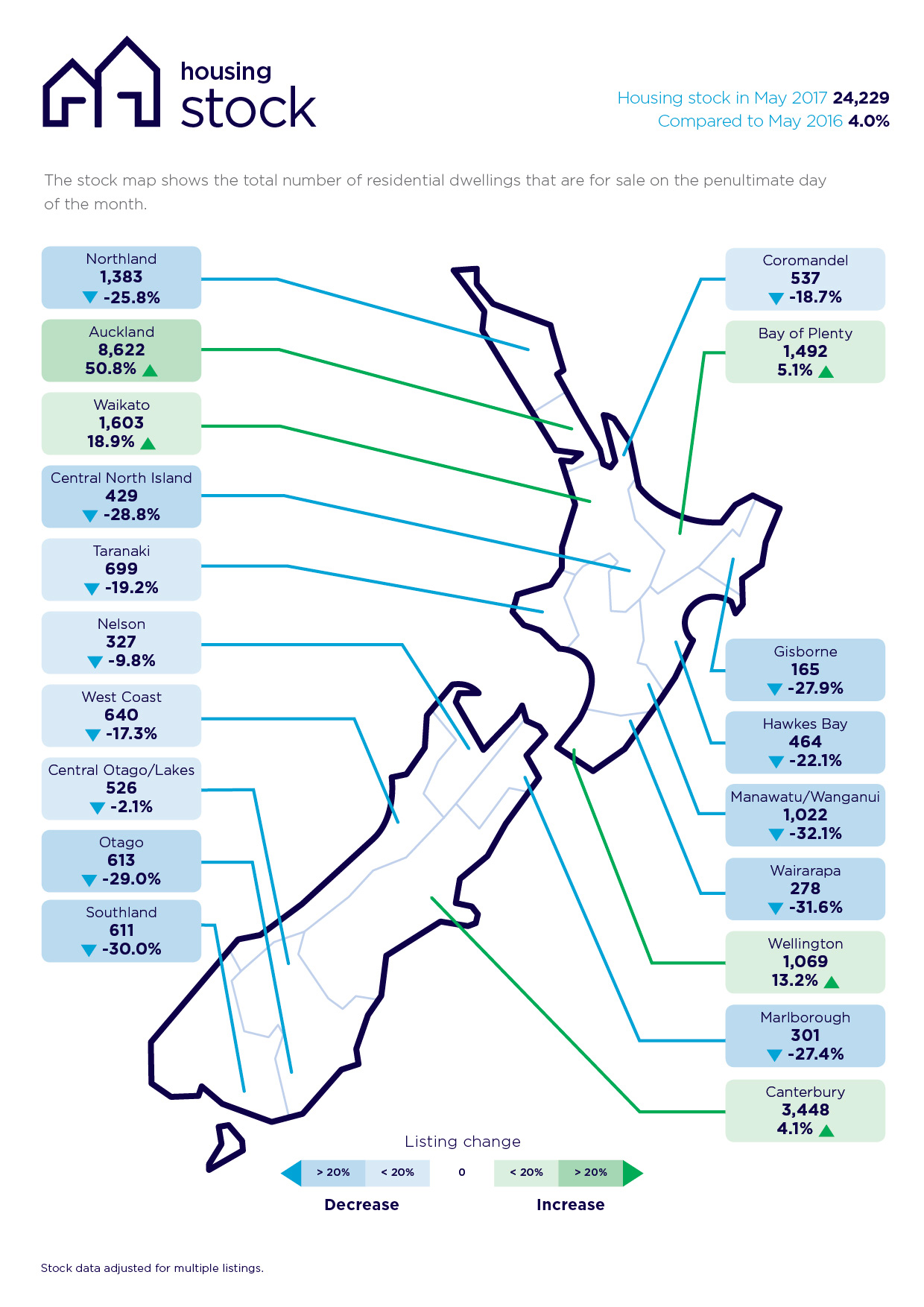

Buyers are increasingly gaining the upper hand in the Auckland housing market as the number of homes listed for sale in the region hit its highest level for the month of May in the last five years.

Property website Realestate.co.nz said it had a total of 8622 Auckland residential properties available for sale at the end of May, compared to just 5718 at the end of May last year, a 51% increase.

It was the most properties Realestate.co.nz has had listed as available for sale in the month of May for the last five years (see table below).

The increase in stock available for sale in Auckland comes as the number of homes being listed in Auckland rises, but the number of homes being sold each month falls.

Realestate.co.nz received 3690 new listings of homes for sale in May, compared to 3544 in April and 3422 in May last year, giving an increase of 7.8% compared to a year earlier.

The Real Estate Institute of New Zealand's sales figures for May are not available yet, but the their April sales figures were down 31% compared to April last year.

That combination of rising listings, lower sales volumes and more properties on the market is pushing the pendulum more and more in favour of buyers as we head into winter, traditionally a quieter part of the year for sales anyway.

"We first saw an increase in Auckland housing stock in August 2016, which was the beginning of the slowing of this market," Realestatate.co.nz spokesperson Vanessa Taylor said.

"The cumulative effect means that potential buyers are more likely to be able to find a house they want, with more choices on offer and less competitive pressure that we saw in 2016."

There are also tentative signs that the turnaround in the Auckland market could be starting to spread to other regions that have until recently been very buoyant, such as Waikato, Bay of Plenty and Wellington, where inventory levels in May were also above those in May last year, although they are still low by historical standards (see table below).

Of the main centres, supply remains tightest in Otago, with the number of homes available for sale in the region at very low levels compared to previous years.

Realestate.co.nz has also recorded a drop in buyer interest in several regions, with the biggest fall occurring in Auckland.

The average number of views per property on the website was down 28.7% for Auckland properties in the three months to the end of May compared to the same period of last year.

That was followed by Wellington -14.1%, Waikato -13.3%, and Bay of Plenty -8.7%.

227 Comments

It's gone burger! Only a matter of time before prices come under some real pressure.

All markets look great at that top. You can talk about supply and demand all you like, but when something goes too far a correction is inevitable.

Just been reading the comments on a stuff article about slowdown. Commentariat are mostly in the 'denial' stage.

Anyone ,who wants to see how psychology will play out in New Zealand's housing market, should read the market reports from Daft.i.e , detailing how Ireland's market turned quarter by quarter. The comments pre collapse are mirrored here . It can't happen here.

I followed the 2006/07 USA bubble closely. Yep, all sounds very familiar.

Yes. I lived it, and was astounded as to the lack of reality in so many people. Too many people were naming the boats that they were planning to buy with the gains from their property holdings... :)

Yes, even for those that should have been the most informed and cautious - the euphoria of that market just consumed them all. A girlfriend of mine from Phoenix - a registered valuer - was talking to me about a potential property flip she was considering one week - and then less than a fortnight later she was laid off from her valuation firm.

A year later she'd been foreclosed on.

Two years later, she'd had enough of living with friends and decided to end her own life.

There is nothing to celebrate in any bubble bursting. Real lives, real people.

Yep. It should never have been allowed to get to this stage, just to magnify the tragedy when it goes. That's another thing that makes this monster so dangerous. All the auxiliary businesses dependent on the bubble continuing. How much of our GDP is in real estate and related industries again?

Imagine being someone who campaigned in 2007 on the need to urgently address the housing crisis, got elected on that platform, then denied any crisis existed for the next nine years.

Man...if you had a conscience, this sort of stuff could weigh heavily on it.

That's two-fold as well Kate - those currently locked out of the market and hurting (innocent in the madness), then after the burst the guilty and bankrupt (complicit to the madness).

It makes you ask the question....why do we do this to each other..?

That is the real tragedy of this all. I feel sick thinking about this scenario playing out here in Auckland too. Sorry to hear about your friend.

New Zealand is not the same as the USA, you don't need to look at it that closely just watch the movie "The Big Short" and you see the totally idiotic situation they let happen in the USA and almost unbelievably they have not changed very much so yes it could all happen again over there.

These daft.ie reports are pure gold. especially when one looks at the comments section. E.g. https://www.daft.ie/report/marc-coleman

What an interesting dataset!

It is educational to read through the various reports, and comments, as the property crash unfolded. One can really get a feel for the various stages of investor sentiment. One can see various archetypes in the commenters, just as we do here. The obvious RE shills were comedy gold, especially so in hindsight. On a more real note, it was sad as to how these shills may have helped some people lose their lifes savings during the property crash. I wonder how they lived with the knowledge that they so misled many people...

It was especially interesting to see how the opinions changed with time. One can see the various stages of a market cycle.

Some of the comments are on point but the grim realisation hasn't hit. Although given that a large number of stuff comments are written by morons it's not surprising.

Lucky the NZ Herald doesn't have a comments section. But then again, it might have more insight than the original article.

"Buyer's market" is double speak for "please catch the falling knife".

Like anything if you know what to do you might be fine. In this case catch it by slapping your hands together not being gun ho and grabbing it with one hand.

When you put it like that, what could possibly go wrong =)

Auckland housing market will prove more robust and resilient than many here anticipate.

Mark my words.

Jeez, that crystal ball keeps getting better.

'Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.' Ben Bernanke 2006

hahaha Yep Ben Bernanke is a clown!

I'm looking forward to seeing the Barfoot numbers and the whole of industry numbers in the middle of the month.

By the time StatsNZ and LINZ get their questionnaires right about jurisdictions and country of residence etc the crack down on Flying Tigers by the mandarins of Beijing the number of foreign purchasers will be so low the National Government will wave the next publication under our noses and say - there you go - told you so

PS - haven't seen the March quarter results yet - any one seen them?

the latest one out have more sellers of non NZ origin than buyers, that in itself tells a story

there was a 6% gap

that was always the plan, buddy.

I've already seen some strident supporters saying "See, told you there aren't any! The Chinese clampdown on capital outflows is purely coincidental."

As much as i would love prices to fall so i could afford to buy a house, I really dont see them coming back very far unless we experience a global shock. The LVRs and general tightening of bank credit has helped, but until we see either a large supply response (not happening) or a large demand decrease (ie migration - which will probably continue for far longer than ppl think unfortunately) the fundamentals will continue to point towards prices staying at crazy levels. It sucks.. but there is just too many vested interests keeping them high, and the only ppl with the ideas to make a difference dont have their hands on the wheel and probably never will

You might be surprised leverageup. Human sentiment can be pretty fickle. The fact that we've all jumped on board housing on the way up, could well mean there's a decent chance that the same fickle mindedness will come into play if sentiment shifts in the other direction. By that I mean there are no fundamental investment principles/grounds to back investors/speculators/darklords in their decisions to buy 40% of the housing stock in Auckland in the last 12-18months. So equally the same argument could be applied in a years time if prices start dropping but immigration and demand are still high.

Supply and demand arguments hold less value when the market is irrationally priced (like which Auckland is in my opinion and NZ as a whole, perhaps).

Leverageup did you miss the news that China just had its credit rating downgraded? Or that economists are predicting an unavoidable hard landing for China from 2018? Or that various investors in Oz are taking their assets and money offshore and recommending people short the real estate market? If you think China's oncoming hard landing isn't the most significant global shock that could possibly impact both Oz and NZ economies then I don't know what would persuade you. NZ and Oz largely avoided the worst effects of the GFC because of their business links to China, and for that reason, they will be hit harder than everyone else when China crashes.

Always enjoy your posts Gingerninja, whether I agree with them or not. I find them informative and articulate. I've been watching this Auckland (sometimes NZ) housing 'crisis' since around 2007. What I noticed during the GFC, people just stopped selling and waited it out. Yes, a few did sell and prices did stall, but there was never a collapse. Why will the impending financial crisis be any different. Why will this one be different? Yeah, I hear all the chatter about certain buyers no longer buying because of capital controls. But in my North Shore neighbourhood, those supposed no longer buyers, are still buying. Yes, perhaps not at auction, but still buying. I can't give you stats, but I see who is selling and I see who is buying.

So what happens if investors just hold out? The way I see it is we're importing 60000 new immigrants a year. We clearly have a housing shortage and even ol' wild Bill's on going fabrication that nz is in the biggest building boom in history, we are still suffering a massive housing shortage nationally.

Personally I just cannot see a catastrophic housing collapse.

" Why will the impending financial crisis be any different."

Because interest rates were much higher at the start of the GFC (variable mortgage rates here -10% odd back in '07) and there was room for a fall in rates to cushion the fall. This time.......

One of the factors kicking off the current Auckland bubble, and which made the 'wait it out'' strategy work after the GFC, was that influx of insurance money from the Chch earthquake. Plenty of investors took that payout and bought in Auckland, and the feedback loop began anew. Relying on a once-in-a-blue-moon rescue like that is a very risky strategy.

I was of the same mind as you Bluemeanie till about a month ago, i'm pretty sure I said on here several times, that I thought it more likely that the market would just slow down, stagnate or just grow slowly in single digits for ages, while wages caught up. However, at that time, commentary was that there was a massive shortage of housing due to immigration and that China was managing to achieve a soft landing and seamless transition to a service orientated economy.

But, being new to NZ, I also had no idea about all the negative gearing and how much of the household debt was actually concentrated in the hands of particular people who owned several properties.

And then I met a specuvestor (in my very own family) and he explained to me, how utterly genius his finances and investment strategy was. He is under 30, he owns 3 properties and a piece of land a few hours from Auckland that he has broken ground on, to build the most obscene, expensive Mcmansion you can imagine. I thought "wow, this guy has done well for himself" until he started explaining to me how it all worked. His parents have used the equity in their family home, to help him and his siblings to buy their first homes. Then each of them, have used the equity in those houses to buy more houses. Until they all own 3-4 houses each around Hamilton. My family member has over 3.5 million of mortgage debt and every single one of his mortgages are interest only AND negatively geared. He explained to me that he had to top up each of his mortgages every month from his salary, but it was worth it, because he was making such amazing capital gains. I should add that he and his family have further extracted equity from all these houses to buy boats and cars. He is also a particularly risky career.

He has gone to various workshops where he learned this model of investment and assures me it is all the rage.

It was then and only then that I realised just how screwed NZ was going to be if the Chinese economy hits the fan, if capital gains began to disappear or if immigration decreased at all.

The good news is that NZ government are well positioned to support the NZ economy when the recession hits, but all the people who have leveraged up to their eyeballs, they are going to have to deleverage. I can't see how they can avoid that, or how that deleveraging can be painless. I don't see how all these various people who are negatively geared will want to hold onto their properties if they are losing equity. And when China crashes that will have a huge impact on the NZ economy, immigration will decline, unemployment will rise.

Although i agree with much of your thoughts, i will play devils advocate for two of them.

1. I think you are using personal anecdotes as too much of a reference. Yes there are ppl in NZ who are leveraged to the hilt and will be stung in a downturn, but generally speaking we are less leveraged than we were pre GFC (relative to asset prices). In this insane rally in house prices, we havent had the same weatlh spending effect that we had in the 2002-2007 boom.

2. Of course we will be affected by a downturn in China.. they are massively important to us, that much is obvious. They will have to take their medicine at some point, but i have been listening to commentators talking about their demise for years. It could easily be another 10 years before they have a big downturn, by which time NZ property prices could have gone many ways. Am i buying a property now? No.. but Im not going to scare others off it by shouting the sky is falling.. when it may not fall for another 10 years or more.

That was a very sensible reply ...and I second your thoughts - china is being talked down by everyone who wants to make some money in selling them short ...

But back to the investment scheme that mentioned by Ginger ... That guy in his 30's was and sort of doing the right thing - however he is over killing it by borrowing too much (greed is kicking in ) and risking to lose a lot on the downturn - this investment strategy is ok if it was played reasonably slowly and safely - certainly buying cars and boats is a stupid idea when you are so highly leveraged !!

Most today's investors have done the same when the time was right back in1999, 2003 and 2010.

Property investment is just like any other , need to know the rules , manage the risk involved and be disciplined with your debt control.

Yes, houses are selling on Auckland North Shore , mostly going about 5% under the peak prices back in Dec 16 (apart from the old stock that was over priced ) ...and there are chinese buyers paying top $$ for good houses.

I concur that China is unpredictable. And I am personally not shorting China with any actual skin. I just see a lot of clouds looming over the NZ housing market.

When my hubs and I first looked to move back to NZ in 2011, we would definitely have bought. When we first started looking at moving again in 2015, we would definitely have bought and probably would not even regret that right now.

What we don't want to do is buy at this moment, based on current sentiment.

If the property market just plateaus for ages then we won't have lost anything, if the property market drops, we stand to gain. If it looks to be rocketing up again, we may decide to buy. But I just can't see how it can go rocketing up again. Where is the money going to come from?

Just look carefully at the 50 year history of housing prices ( in auckland that is - other cities can be different) - that will show you that since 1974 we had 4 cycles each lasted few years to rise, then stagnate or fall by max of 10% on average but that stagnation only lasted 2-3 years max - regardless of the duration of each cycle, the price differential between start to finish of each one was about 1.8 times - the last four years was no exception ... There wont be any crash - china is an excuse, there are much more pressing hot spots in the world which could do more damage to trade and international relations - I would buy at a reasonable price before October this year ( reasonable in price compared to similar quality new built and location)

Ecobird, yes but 10% on 1.2million house is $102k that's my kids univeristy paid for and more! I'm willing to take the risk and wait on that.

As far as i am concerned I have nothing to lose, especially as I plan to follow s similar formula as described by another commenter above (credit to mathclub);

wait until:

1 - The sales per month start rising again

2 - The days to sell starts falling again

3 - The number of houses for sale starts to fall again

Once all of these 3 start happening then it's time to buy again. Price tends to lag those 3 indicators so you will have about 6 months or so to buy something good.

Thanks Ginger, would you mind saying where I can find the data for these 3 indicators please. Thanks.

10% in nominal terms, but note than back in the 1970s and 1980s the inflation rate was way higher than today, so in real terms house prices declined by over 40% from 1974 until 1980

Eco Bird,

If this investment strategy was played reasonably slowly and safely, it would be a very different investment strategy. I'd recommend looking at Kate's comment a little ways above this for how the wildly over-leveraged process plays out in anything other than the euphoric bull market. It doesn't take very much of a downturn before the negative gearing results in negative equity and a margin call (AKA mortgagee sale).

I've no skin in this game, and do not ever plan to have any in the future other than owning a home for the purposes of living in it rather than as an investment. I've done far better, with less risk, by investing my savings in equities, bonds, etc. as compared to investing in property. I've seen too many people go for the get rich quick schemes as exemplified by the anecdote about gingerninja's family member, and seen virtually every one of them wiped out a decade ago in the US. But then again, I've been given to understand that "it is different this time" here in NZ.

I remember hearing this "its different now" phrase and message bantered about in 2000 during the late stages of the dotcom boom where everyone and their brother/sister were momentum investing in the absolutely stupidest possible internet companies. When the music finally stopped, it turned out that it wasn't different after all...

Well thought out response to a well thought out point.

I must raise this one though... you say "but generally speaking we are less leveraged than we were pre GFC (relative to asset prices)".... but isnt the point that if the asset price is inflated, then the leverage is higher. What matters is debt relative to household income. Which is well up.

Ruh roh

Reading about your family member reminded me of the scene with the stripper in the Big Short. Does he have any concept of how f****d he would if the market turned and he lost his job?

"The Big Short" should be compulsory viewing for everyone. Great movie based on real events leading up to the GFC. Hedge Funds are already investing to short our Oz banks and have been for sometime, which of course will magnify any bank losses ten fold. That is truely frightening!

I'm not certain about your conclusion regarding the likely effects of shorting on the Oz banks.

A successful short play actually reduces the magnitude of the share price movement rather than increasing it. A successful short has the short seller selling the stock at a high price, thereby reducing the demand at the high price. The the short seller then purchases the stock when the price is low, adding to the demand for the stock at the low price. There are numerous devils in the details though... there are lots of games played if one has enough backing so as to wipe out short sellers. google "volkswagen short squeeze" for an example. About a decade ago, Volkswagen briefly became the worlds biggest company by market valuation as short sellers got burned very badly.

Yes great movie but the USA situation is unique and not the same as the NZ/AUS setups.

I would say the rise of using interest only loans for owner occupation puts us in a similar situation to the USA toxic loans IF interest rates rise by 2%

I reckon you're on the money, Blue Meanie.

Of course, there's hype here today based on the headline for this item. That's why Greg Ninness came up with it. Journalistic license.

But it doesn't actually amount too much.

Without doubt, Auckland house prices will be "sticky downward". Sellers won't sell unless they have to. Longer term prospects are excellent for Auckland...... So why take a short term loss when you could make a handsome gain in the longer term.

Spot on Gingerninja. I agree with your explanation of facts completely.

If you're a speculator sitting on big capital gains and watching the tide turn why would you sit tight. It only takes a few houses in a neighbourhood to sell low to re-price the whole neighbourhood. Once sentiment turns this will unravel rapidly.

How many chancers are waiting for the 2 years to be up to escape the bright line capital gains tax I wonder?

They probably won't have to worry about capital gains if they bought 12-18 months ago....

I dont know about you, but I consider a 50% increase in homes for sale to be a rather large supply increase. Especially combined with a rather large 28% reduction in buyer demand. When you have too many things for sale, and not enough people interested in buying them, prices fall.

Hi Leverageup,

Agree with you.

Auckland house prices won't fall by much at all.

There will be no crash - which will disappoint some contributors here.

Nobody could know that - you're making stuff up. Is this the line you've been hounding people with at BBQ's for the last 5 years. And everyone's been believing it aye?

Judge it on it's track record, backed up with systematic analysis. Don't fall for all the hype posted here today.

By the way, I never attend BBQ's.

So who's "making stuff up"?

Have you been extending that trend line on your house price charts again? Past equals the future?

Sounds like very systematic analysis....

"We're obviously going through a significant slowing period, which as best as I can judge is quite likely to be temporary," Alan Greenspan 2006

lol Alan Greenspan should have been put out to pasture in the 1990's and given a pension for life. We may not be in the situation we are in now, if only that dinosaur had been dealt with early on. Love your sarcasim by the way.

I've circled the wagons, General Custer!...............Meanwhile "Sitting Bull" the new Reserve Bank Governor quietly raised the interest rates 1%.............. and they were history.

Said everyone before every crash.

Wait.... what....??? BUT BUT BUT there is a housing shortage!?!?! There is a housing crisis based on a housing SHORTAGE in Auckland... and annual YoY increase in inventory of 51% makes no sense if there is really a housing shortage.

Unless the whole thing was a total have and the shortage was caused by specuvestor and foreign specuvestor house hoarding?

^^^^ This...

I think you'll find that there is a shortage of reasonably priced property in Auckland (pretty much 0). There isn't a shortage of over priced properties that no one can afford.

Someone needs to tell the Buyers its a "buyers market" as they seem to have disappeared...

That's right - and then you have to ask - what are the buyers going to buy the expensive house with? It can't be money because it either doesn't exist or it can't be created....(either no more capital or bank can't create due limits).

If all of the crazy investor/Asian buyer money has gone then we are left with local buyers and FHB who are not going to find value until we see drops of 30-50%.

In the meantime if we get enough of a swing we will get mortagee sales. We just need a capital flight back to Asia to finish things off.

Back in 1987 when we saw a similar bubble in the Gold Coast, Japanese buyers were selling up and sending money back home, one case I remember seeing they sued the hapless real estate agent for giving the wrong information. They sold 25-40% lower three months after buying, his response was, well that's the market.

The locals will always look to long term value.

In case you havent noticed, the capital flight is not back to Asia, its to Bitcoin. Bitcoin is the new Chinese investment frenzy. Property was so last year!

Bitcoin and Gold Bullion which the Chinese have been stashing away for a very long time now. They are onto it. Gold versus Fiat Currency which is basically worthless paper based on current sentiment and a promise that it actually represents currency at the time of valuation. And we all know that currency valuation fluctuates daily and every now and then it just crashes!

Yup. I hold a lot of GBP so believe me when I say I know the pain of currency devaluation. :-(

We already know its a buyers market. We've known for a long time. Even the RE agents have known for a while (many of them told me months ago). The thing is the vendors refused to listen. Only now are they beginning to drop prices to what a property is "worth" when you first looked at it 2-3 months ago. The problem is, the new price is what it was worth 2-3 months ago, we buyers following the market down over the last few months think its still over priced and needs to go lower. So we still will not buy. Only those that hit the market straight away with a good price will sell - the rest of the vendors will be playing catchup with patient buyers waiting for their bargains.

Got to watch this first hand a decade ago.

The seller thinks he can get $XXX, puts the home on the market. Turns out that the asking price is 5% above market value. After a few months, drops the price by 5% to meet the market. By that time the market price has dropped another 5%. Rinse and repeat. This is not a new phenomenon, and it isn't very enjoyable to watch play out. It isn't certain to happen in Auckland, but the data presented in this article suggests that the odds are very much increasing.

Its happening in Christchurch now. Two properties on the market both dropped their prices by $20k this week. One has been on the market for 3 months, the other for 3 weeks. The newer one is looking pretty enticing ($359k instead of $379k) but the older one, compared to the price of the newer one, is still looking expensive despite dropping from from $469k to 449k). The sharper the price point of the new listings, the more over valued the old ones look. And practically nothing has sold since February, so stock is piling up. I cant wait until all the new stock hits the market in the spring - it will be vendor panic stations then :-)

Just you wait...... If prices drop a few per cent, buyers will be back in droves.

There's an enormous underlying demand for houses in Auckland.

It's practically been a buyers market since 2001, difference then was you couldn't include prospective flatmate income in your calculations when apply for a mortgage to purchase your own home how times have changed try buying your first home now without factoring in flatmateS income in Auckland! 'Buyers market', At what price?

Message to all First Time Buyers; DO NOT BUY NOW! The Auckland market needs to bottom out that could take six months to a year. You don't want to get trapped by negative equity.

If we do get a downturn, it is likely to take a couple of years to reach a new equilibrium. six months to a year isn't nearly long enough for the cycle to sort out. Expect a one or two false recoveries prior to the bottom occurring. We've barely reached the "anxiety" level, much less capitulation. Safe to say that we have passed the euphoria stage.

Yes you could well be right. Not sure how far this rabbit hole goes, there's so may factors to weigh up. The biggest one being many foreign investors are being pressured to sell off their off shore property assets??

This is no usual cycle! Vendors and RE agents know that the market could swing upwards on a dime if the Chinese Communist Party politburo relaxes their capital controls. Also, there's still money leaking in from China as evidenced by lucky number 88A Kohimarama Road which I see last week sold at auction for 3.1 million dollars. Add to that mix an angry disenfranchised Auckland population who can no longer afford Auckland houses with domestic Auckland incomes, and a looming election. Too many variables and unknowns for anyone to predict.

Ok all you naysayers - it's Friday (be happy) - I'd be interested to see you put a stake in the ground instead of just gleefully pointing out the tide is turning. That's nothing new - these sorts of calls have been coming in since Nov/Dec last year.

What actual % decrease do you see coming? Do you think this is going all the way back to 2012 levels, or are we simply correcting to a new average price that is still 50% higher than 2012 levels?

I'd presume a number on here are waiting to buy once the market drops back - at what point are you going to see "value" again?

I have no vested interests one way or another - would just be nice to read people actually making predictions instead of just saying "financial armageddon is coming". Personally I don't see more than a 20% drop - similar to 2007 (which may have been closer to 10% if I recall).

Cheers

Out of interest, what's your prediction or ideal for the future of Auckland?

Price-to-income ratios of 25+, and native New Zealanders forming a servant class for new foreign overlords?

I can't stand what Auckland's become in the last decade, so ideally? Prices drop then stabilise for a decade while wages catch up, and foreign ownership is banned. Focus goes back on getting FHB and families into homes instead of speculators or foreign owners sitting on empty homes.

Only natural population growth (and actual skilled migrants) until the infrastructure can support the number of people here, and deport the scam student visa holders.

I personally will be voting for change this election.

Which change are you voting for will be most likely to result in the outcome you wish to have happen?

My expected outcome? Home prices drop on the order of 30% over a period of about two years, then stay stagnant for around ten years. The follow-on effects of this is likely to return NZ to the position of more people departing than arriving without any structural policy change.

Anyone else remember the headlines of a while ago, bemoaning the number of NZ people leaving for greener pastures elsewhere and speculating as to how this loss of skills will ruin NZ?

I remember that time very well. House prices were cheap and stagnant for years. I have educated my 20 year old daughter and her builder partner to how quickly these cycles change and that nothing stays constant but is in fact a whole system of moving parts that are affected by so many outside factors, that in the end house prices eventually return to equilibrium and more in line with real incomes.

I'm not really into betting on percentage drops because there's too many variables and irrational house purchasing behaviours. I think that for regions outside of Auckland that going back to a 2014 price could easily occur. For the area I live in this would mean a 28% price drop. However when I put an actual figure down I have a history of falling short.

In the past I disgreed with PWC who suggested a 10% increase in property costs (and prices) and I said it would be more like 30%. Of course it turned out to be 50%+. So if you factor in my history of being wrong then by the same ratio then I would say 47-48% decrease in price. A decrease that large would put us in the region of current US housing costs outside of areas with a large population of high earners.

It all depends on how bad things get, will there be significant job losses, bank failures, etc. These are unknowns. Maybe we have a correction and flat prices for many years, maybe we don't realise that we are in deep trouble.

You need to keep up WMC have you missed all the extremely poor auction results, the warning from the Reserve Bank all the news on China's capital flight restrictions. And by the way that is why you've been hearing these wanings since very late last year which is when those Capital Flight started restrictions kick in removing the top end buyers.

Property market crashes or corrections how ever you want to word it, do not happen over night. They play out over a period of years. The last one I experienced at first hand in the UK, the 2008 property market crash took two years to bottom out. Where there hundreds of property repossessions (Mortgagee), which doesn't benefit anyone.

Actually no CJ099 the UK property market took a lot longer than that to bottom out across the country, don't you remember "the double dip"? I sold in London in 2011, just as prices had recovered a bit, then they flat lined again and I held off to buy the house I currently own, which I bought at.... wait for it..... 2006 prices.

Hi Ginger, Yes I don't disagree with you. I had to rent my house for five years as a Reluctant Landlord (Rented rather than sold due to the property market drop). My house was in Surrey and sold just under two years ago but it took five years for it to climb back up again. I know price drops varied depending on where you were in the UK and some areas still haven't recovered in the North of England.

I do think the situation here is slightly different, it that the Auckland market became too dependent on Foreign Buyers who decoupled highend central prices from wages particularly in the last few years. So logically the more at risk owners are those with very high mortgages and rapidly reducing equity.

And of course those Landlords who have used their equity as a means to purchase other property are also at high risk.

Yup. I have friends in Ireland that still have negative equity too :-( these things make one very cautious of bubbles

And when you drive through NZ's countryside and that of various other countries you realise there's no shortage of land, really. And there are plenty of towns in which you could live in reasonable proximity to a hub with a hospital etc.

(Fibre internet might be the killer must-have haha...unless Musk et al get global satellite internet down to a cheap price soon.)

No one knows the actual % decrease or increase. It's impossible to predict. It's also foolish to look at price as a guide to make these decisions.

As someone who WAS currently looking to buy in Auckland but is now no longer seriously looking I will wait until:

1 - The sales per month start rising again

2 - The days to sell starts falling again

3 - The number of houses for sale starts to fall again

Once all of these 3 start happening then it's time to buy again. Price tends to lag those 3 indicators so you will have about 6 months or so to buy something good.

Anyone throwing out percentage drop guesses is doing just that ... guessing.

C'mon we're guessing to freak everyone out. Just say you think house prices will drop 100%.

I like this games. -200%. It will be so bad your negative gearing will mean you owe the bank another house. Some will laugh because its a joke, some will laugh hoping its a joke.

Some have never seen negative equity in a house before. Everything's fine so long as you can keep up the mortgage payments, or cover the interest for the interest only until the bank gets nervous.

Most buyers are actually buying their own "home". They are not too worried about equity in the short term. So if it drops it drops.

The Banks getting nervous (Greedy is probably the better word) now that is something I see happening. The Aussie banks are definitely showing the first signs.

I'd say some of the NZ banks are more nervous :

http://www.interest.co.nz/business/88040/rbnz-notes-small-banks-have-do…

Massive growth on their books at a time of rising prices = super risky. Limited capital (e.g. Kiwibank)

Arent all depositors in Co-op actually shareholders?

It only takes one to fail, and the confidence will be gone, then boom! there go the rest.

I am making the exact same play mathclub. As soon as there are the early signs that the market is picking up again, I will buy.

WMC, my best guess would be Auckland/ Hamilton/ Tauranga/ Rotorua fall 15-20% from the top. Christchurch 10% from the top. Wellington + Dunedin probable track along with inflation, based on fundamentals.

Regarding multiples of median price 3-4 times median wage, this will never occur again in major centres. On average more wages per household. Also from statistical basis, in an environment of falling property ownership levels need to use median income of property owners. If adjust property prices for median home owner income and projected interest rates going forward, can use US 10 or 30 year treasury rates +margin, property outside overvalued areas (see above) is relatively cheap.

With automation, low to middle income earners will struggle to get gains in wage levels, hence will not be able to purchase property in most cases, and their median income levels are generally irrelevant in using income multipliers for property price projections. May not be fair, but it is the way the future will unfold.

Keep the supply under control is the name of the game. Things won't change.

Thing is this isn't a crash caused by a recession but a healthy market correction, people are too busy spending money at the moment rather than looking to buy houses. Pay attention to how many people around you are going on an overseas trip. (workmates, friends, families..etc)

Personally I can buy $1m house now, but it means I will eat baked beans on toast for the next 30 years. The last time the market dropped ave house prices were nowhere near the current income ratios, so there was a floor much closer than now where kiwis could afford. My prediction is that it will drop to the same floor of around 4 times ave income, so 40- 50%.

While I agree a drop is coming, a) its not here yet, b) it could be more like 60~75% c) if there is such a drop there would be an underswing beofre a correction did you allow for that? d) if we saw 40% I am fairly sure the impact on the banks and NZ would actually be pretty huge. Maybe someone can comment on the Banks [in]solvency if the value of their assets 1/2'd? I'd assume we are talking an OBR scale event here.

I own a house in West Auckland valued at 750K. If it dropped in value by 75% it would be worth 188K. That is less than one year's salary for my me and my wife combined. Less than one year's salary for a lovely brick and tile house with internal access garage and its own driveway. One year's salary.

Nothing wrong with baked beans on toast, Green_mamba. It's a healthy diet and farters' favourite.

You will live a long life my friend.... well beyond the next property boom!

Personally I can buy $1m house now, but it means I will eat baked beans on toast for the next 30 years. The last time the market dropped ave house prices were nowhere near the current income ratios, so there was a floor much closer than now where kiwis could afford. My prediction is that it will drop to the same floor of around 4 times ave income, so 40- 50%.

I've heard some baby boomers say they went through hard times when they could only eat sausages. Sausages are a damn luxury compared to beans and toast. Although having toast is as fancy as smashed avocado. The true poor diet (which will eventually kill you) is rice and beans.

You right, toast implies I will have money for electricity and a toaster! Maybe a luxury a I can do without as per Tony X.

Don't see a major correction myself, several other things need to change at the same time for this to happen. Sure there may be a lot of houses for sale but how many are people that then need to either up-size or downsize to another. What about the building costs of a new house ? until these take a dive, why would house prices in general take a serious dive ? What about the steady population growth ? where are all these immigrants living ? in cardboard boxes ? My prediction, a small drop its winter and election time and then watch it recover that loss in summer and remain static or very slow growth in prices over the next few years unless some major global event gets thrown into the mix, then all bets are off.

You forget, those that sell still need to get close to their asking, otherwise they don't have a big enough deposit

You forget, those that sell still need to get close to their asking, otherwise they don't have a big enough deposit

Still a long way to go down before there is value in this Auckland market .

My advice to buyers is to sit on their hands and do nothing until the market bottoms out

So enthusiasm by web page view for Auckland housing has dropped by 28 percent year on year, despite surging migration, low interest rates, supply shortages,headline news ra ra ra , latent demand,Chinese, martians with large heads. Anecdotal but consistent with many other hard data that is gradually smothering New Zealands most popular religion.Forget finding a exit door, just jump.

Next news story is... "Over 300 hundred property investors still unaccounted for as fire swept through an Auckland Property Investment Seminar on Aucklands North Shore. The latest unconfirmed report suggests that only 2-3 investors at a time could make it safely through the Fire Exits before the rest were engulfed by the smoke. We are still confirming numbers but at this stage it looks like only about 5% made it out unscathed. More to follow...

So a good return on investment then.

If everyone is now in a hold back and wait for prices to bottom out to whatever that perceivable figure is, my question is where are the hoards of people (backlog included) and future residents going to live? If they are holding out on buying a house for an indefinite period, I would imagine they would have to rent, so who is prepared to either buy that land and develop or buy that rental and rent it out??

So how much activity will still have to be under way in the market to facilitate and accommodate day to day living for the increasing thousands waiting for rentals or homes for their families? Personally, numbers might be at stupid levels now, and still there will be thousands waiting to buy or get into an investor property as a rental whether the increasing local population (birth rates and natural progression) or immmigrants. With 50% more listings on stream there is still going to be a significant amount of activity.

So will it plummet 40-50% I'm not so sure.....

The rate of building and permits has slowed, it will be years before some projects are even at finished levels to be sold and rented and yet our demand increases by the day! With a demand factor growing each day pressure remains on the market and will keep prices high, perhaps they may drop 5-10% or further but 40-50% seems a lot for the short term. The REINZ figures with boom and busts along the way over the past 20 years show now signs of anything near 40-50% short term crashes, so I'm unsure what logic some are speculating on here? My house my have doubled over the past 6-7 years but that would indicate that even at the increased rate it has gone up, it would have to fall at a significant rate to get to 40-50% of value in a short term, and there is even more demand for housing now than there has ever been that I can remember since I've owned a house.

But just like many in the property market we are all speculating based on what we think and the fundamentals we think will be drivers......who really knows what's around the corner.

Yeah but supply and demand are never the only factors in housing markets. Look at the UK in 2008. They had a housing under supply in 2008, they had year upon year upon year of huge net migration figures!!!! And yet house prices dropped significantly.

External factors can be every bit as significant to a housing market as supply and demand.

The price of any asset is determined by one thing, and one thing only - the ability to pay for it. That can be from retained earnings ( savings); borrowings or a combination of both ( most often in the case of real estate). But if whichever alternative is used fails to provide enough to buy, there won't be a transaction until the price reached an attainable level. In the meantime, to answer your question, the standard of living falls - 25 people live in one house etc. But underlying all assumptions is - the ability to pay. And with credit being rationed, regardless of the price of that credit( interest rates could fall from here and still no credit is available. NB Falling interest rates from here probably spells a tightening credit market, not a loosening one) asset prices could fall.....

Exactly right BW.

The price drop in the UK in 2008-2009 (and again in 2012-13) was divorced from the long standing supply/demand, mass migration issue. In 2008 there was a credit crunch. People went from being able to get a 100% mortgage, or most commonly a 95% mortgage to only being able to get a mortgage with at least 25% deposit. BoE interest rate was rock bottom and if you had 40% deposit you could enjoy 2% and less mortgage interest. I think at one stage with enough deposit you could even get a 10 year fixed rate at 3%. Of course very few people had this, because house prices had tanked so LVR's worsened. FHB could not raise the huge deposits, the term boomerang kids (adult kids who had to move home to save for a deposit) DTI ratios were introduced and only cashed up investors were active.

If it is true that if capital gains disappear everyone will simply hold tight and ride out the storm, how come that hasn't happened in all of the world's proceeding property busts? Why will NZ be different?

There's more than enough accomodation. Just look at NS rentals available spiking as I track this as well. The so called shortage that's been talked up is actually an oversupply of accomodation coming on line as new builds get completed. Look at rental price increases vs house price increases. Not nearly the same. Most immegrants live together as they simply cannot afford houses. It's greed that caused the bubble and it will be greed that pops it due to oversupply by specuvestors and developers driving up prices

They will live cars,garages, under bridges and ghettos.....just like any other failed 3rd world country.

The hoards of people living somewhere would suggest we will see rent auctions in the not too distant future.

or maybe we can fit 150 people into a garage in South Auckland.

Gingerninja - how much did the prices fall in the UK? 40-50% within those 2 year periods?

Average UK property price fell 18% top late 2007, to bottom early 2009. 190K to 155K.

Yup MJA has it. Although some properties only went down by 10% and some by nearly 30%.

We are in uncharted territory in NZ.

I can't even compare NZ directly to the UK in terms of the boom and bust despite the comparable supply/demand problems.

The UK has CGT, rising percentage stamp duty on each purchase and other structural disincentives for housing speculation and investment. The UK also doesn't have negative gearing, in fact recently HMRC legislated that landlords couldn't even deduct mortgage interest as a cost in their annual returns on the house they actual let out. Mortgage interest as a legitimate deduction will be removed entirely in a few years. HMRC have also introduced a higher stamp duty for any house purchases after your first one.

Thats it. I've read enough headlines and commentary over the last couple of weeks on this site and others. On the balance of probability this tide has turned and this trickle could become a torrent. I don't want to be in harms way.

I suspect there are many more young Kiwis who are rethinking whether they even want to be in Auckland for the longer term if nothing changes. Is it a place they want to buy, to raise kids in, to retire in? Maybe not so much. It doesn't make sense in terms of price to income and it's making increasingly less sense in terms of lifestyle factors too.

It might just be eventually left to old folks and their new foreign overlords unless something changes fairly significantly.

I wearily remind common taters that all of this angst is a North Island phenomenon. Down 'ere on the Mainland, and always excepting Queenstown (which, like the Vatican, is really a separate country altogether), it's still quite feasible to buy a plot with a '1' something price and a house/plot for a '4' something.

The bubbular smell is primarily Awkland, with an osmosis effect on those localities unlucky enough to be proximate. So please don't assume this schemozzle is Universal.....

There's a huge obsession with property ownership in this country, as evidenced by this blog and dozens like it.

If there's a significant fall in house prices, it won't last too long. There are plenty of people poised ready to snap up any bargains that eventuate........

Chances are that there will be a plateauing off in prices, rather than a significant fall.

Just like there was an obsession with housing in every other country that has had a real estate bubble. Good observation.

Bit like that obsession with shares in 1986, or that obsession with tulips in 1637.

If you had bought good quality industrial shares in 1986 and held onto them, you'd have done very nicely indeed by now (despite the fall-out in October 1987).

But property's less risky than shares anyway.

Property is expensive, needs maintenance and not liquid in crisis. Shares can be sold in any market immediately. The return can be thousands percent , if you buy right share. I bought shares for $20 in 1994 and now these are worth $20000.00, and returning $1500 every year as income from dividend. This is only one company I am talking about. Other benefit of shares is not all eggs in one basket , some will give loss but the profit from good shares will be multi fold to cover the loss and earn profit as well. It will not be ideal to compare property with shares. The property has its benefits but this is entirely different issues. These two are not comparable. In summary, if you are long term investor then there is absolutely no risk in shares. I am technical person but in shares since 1985, I made equity for my house I now live from shares and now I am teaching my daughters , as how to save $100 every week to make a equity from shares for buying their first home.

Diversity is really just a fantasy. Everything is linked.

If housing collapses then a lot of people are in trouble (as are the banks) it will lead to a massive collapse of the sharemarket (2008 is a prime example)

If shares collapse, then jobs are in trouble, which means mortgages don't get paid and housing collapses as well. (Your example is a prime example - using shares and equity to buy a house)

As for this "Shares can be sold in any market immediately."

1. Anything can be sold in any market immediately - it just depends on the price.

2. To sell a share still requires a buyer, no buyer = no sale = no liquidity.

I agree with your sentiment on linkage. Both are somewhat risky.

Where shares have a *slight* upper hand is that it's not all or nothing. Can't sell part of an investment property. Although, perhaps there's a niche market there waiting for disruption....

They tried (and failed)didn't they. Can't remember the name of the group but they offered a share of an investment property a little while ago.

It's the linkage that's important. It's all based on ROI, which is all based on money, which is inherently a fantasy - as long as everyone believes, it works. But.....

Thats what makes me laugh. A lot of kiwis say 'I wouldn't touch shares - I got burnt way to badly in 87. So what I learned from that is to only invest in housing, and lots of it.'

Similar attitudes, different asset class.Flash forward 10 years the narrative will be back to shares again - won't touch housing, didn't you see what happened in 2017?

Even if you made 'Popular Delusions and the Madness of Crowds' compulsory reading in every school, people would still do this. Price we pay for being a hierarchical social species, I suppose.

It's pretty tough to tell your mates you think they're morons for buying 3 properties interest only or their first and only for $1,000,000...you find out quickly that is socially unacceptable to see through the madness.

Especially when they've gained 25% since then

Share portfolio has done pretty well also....without the social consequences of locking young families out of home ownership - or risking the stability of the economy by taking on excessive debt.

"without the social consequences of locking young families out of home ownership"

I disagree - it is the need for a return on shares that see companies pay as little as possible to the workers, yet charge as much as possible for the good/service they provide.

House prices aren't the only thing stopping FHB - Low income and high costs, resulting in an inability to save a deposit are also hurting many.

..... and those who buy a house (or two) in 2017 will be sitting pretty in 2047.

Housing is a very good long-term investment - if you judge it by its track record.

But it's not just about investment. Houses are a consumption item as well - the intangible satisfaction of owning the roof over your head roof and enjoying the garden, pleasant neighbours, etc etc etc.

If you buy a house that's right for you, you'll seldom regret it. Better to buy the right house in a boom, than the wrong house in a slump.

WRONG - Shiller proved otherwise in his book Irrational Exuberance. That is why I was trying to get David Chaston to put together an inflation adjusted housing index (all time) for NZ to see what our real returns on housing are. In the USA housing returns barely did better than inflation. Returns from 1890 through to present were terrible. Like 1-2% terrible. It was the worst of the investment classes by a decent margin. Shares were the best performing long term investment.

Perhaps NZ is different....but if you're applying the trend for the last 15 years to the future - I think you're going to be in for a horrible surprise. Do that for your chart in Japan 1990 on-wards you'll find you're roughly 90 degrees out. Do it for USA/Ireland 2006/2007 you'll find you're closer to 150 degrees out...That's a lot of degrees.

You should consider changing your name to "Independent Thinker". New Zealand needs more people like you because so many have lost the ability to think for themselves and will just follow the herd over the next cliff.

I beg to disagree with you, Independent Observer.

For one thing Chaston's index only looked at capital growth ("stock" variable). If you factor in the rental return as well ("flow" variable) then the overall performance of housing as an investment (i.e. the TOTAL real return) over time is, in fact, pretty spectacular. What I'm arguing is that the yield from the "flow" (i.e. the percentage return on investment from the rental income) is, in fact, central to the performance of a housing investment - and, thus, should not be ignored!!

And, of course, from the rental return one can claim the depreciation allowances and so forth - and the whole picture gets even brighter......

I stand by what I've said above. Based on its long term track record, housing has performed very well indeed as an investment. And, on top of the investment return, of course, come the consumption benefits - including those which are intangible and not easily subject to measurement and valuation. The intangibles are, nonetheless, very important benefits to people and, thus, need to be included in any comprehensive analysis.

So because of those intangible and not easily subject to measurement and valuation criteria (ownership, gardens, place to call home etc that you mention), that would mean you wouldn't ever become a property investor because that would deny that intangible enjoyment from another owner, correct me if I'm wrong, who would like to enjoy those particular freedoms? - instead of being forced to be a renter?

I take it you're not a darklord then and you're against the practise? Oh but that would conflict with negative gearing practices that property investors use. So you like living in your own home, but you also like receiving rental income and using negative gearing...I think I see how this works....Do you like having your cake and eating it too?

Hi Independent _Observer,

I your response above, you have chosen to ignore the key point I made above about the flow variable - i.e. the rental yield.

Are you disagreeing with me and maintaining that rental yield is not relevant to a housing investment? Or will you swallow your pride and admit to the obvious flaw in your argument?

Also, one does not have to live in one's own house for a consumption benefit to materialise from that house. Any such suggestion would be nonsense.

No pride to swallow here - I agree with you. If you think there's a way that earnings or a P/E ratio in conjunction with capital value could be combined and indexed in real terms over the decades I think it would provide valuable data. I know Shiller has done this with stock market valuations in the states (he's put together an inflation adjusted chart for P/E ratios - and is usually an indicator of an upcoming bear market or slow growth).

Good.

Tothepoint riddle me this..... I wish to buy a house.. Probably a house I hope to own till I am so old that I need to downsize, or leave to my children. In other words a very long term house (I was born in 1980). You say... if I buy in 2017, I will be feeling very happy in 2047.... but if I buy in 2017, will I be very happy in 2018, 2019, 2020, 2025?

The kind of house I want to buy currently costs 1.2 million. If there is a downturn and I can buy that same house in 2019 for 1 million or even 1.1 millon, why would I regret not buying in 2017? The house I buy in 2019 for 100-200k less than 2017 prices will still be worth a great deal more in 2047. The difference being that 100-200k is the difference between vast amounts of compound interest on a 30 year mortgage. It is the difference between being able to afford family holidays, sending my two kids to uni... all kinds of things that are valuable beyond measure.

I try to remain dispassionate to your continued undermining to the plight of my generation but sometimes it just seems cruel. It's as if you simply don't care about the stakes for our real lives and our children's lives. You go on and on and on about how in the future houses will be worth more and forget completely that those years you so readily dismiss are some of the most important in our children's development. Years of hardship that we would never get back. Yes,, for some housing is a cold, calculating long term investment but for many of us, that kind of spend is the difference between being able to be relaxed stress-free parents and sleep deprived- stressed out parents. And that's without factoring in what increased wealth inequality will do to the society that our kids grow up in. You might not care about that, but as a child and adolescent mental health professional, I really do care about that. So please, stop and think before you make your flippant comments, this is way bigger than your long term investments.

well said

Ginger - If you feel so emotional about your kids and holidays and those "bigger thing" etc - then dont buy a house and live happy every after in a rental of your choice -- my son is almost your age and thinks the same way too ! so i know how you feel and will give you the same advise as i gave him ...

So, sorry to break this sad news to you, in this day in age , just like it was in our days, you cannot have both , guaranteed returns and stress free sleeping and the holidays unless you were lucky to have a nice fat inheritance from some wise parents who most probably have done the hard yards for their kids and suffered to achieve that ... Not sure why your generation and the one after think that they should have everything at its best NOW or else life is not fair !! well life is fair enough to people who are content with what they have and can make it better in time - not by the press of a button...

Houses in 2047 will be worth min 3 times what they are today unless WWIII would wipe every equity on the planet - it is up to you to spend the money on your kids, holidays and rent until 2047 ( BTW it is so much cheaper to rent) .... Or buy a home as an investment for the future both for you and the kids -

If you want to buy now and keep it till 2047 you don't have to worry about 100k down if that happens next year or the year after ( you are not going to pay 100k more or less , you are paying 10% or 20% of that !!) ...why do people who are living in a house they own (long term) worry about its valuation every minute?? your mortgage will not change and your debt will remain the same ( actually debt is going down as you pay it) .. so your 100k analogy doesn't make any sense really ( you dont own that money).... people buy homes to settle and build a future and raise the kids and be happy ... it is worth what its worth now and then - start worrying about valuation when you become a property investor :) or a darklord !!

I hope this helps

Ecobird Wow just wow.

1. I don't have parents. I was a foster kid. No one looked out for me and every possible horror you can imagine was part of my childhood so don't patronise me about the hard life.

2. I bought my first house at 19, because I knew, more than the average kid, what it was like to have no home and no security, so I appreciate the psychological value of it, more than most.

3. I managed to buy that house and afford the mortgage by working 80-90 hours a week as a healthcare assistant. A few years after, I did 3 years at university to train as a nurse, and I worked every weekend and several evenings during that time too.

4. When I was pregnant with my second child, the ward that I managed was closed owing to austerity cuts in the NHS (we didn't get redundancy). I decided to move out of London, take what capital I had and buy a totally trashed house. I spent a period of time during my second pregnancy in a wheelchair and spent 2 1/2 years waiting for surgery on my spine but after that I knuckled down to teach myself to brick lay, plaster and renovate the house, because I couldn't afford the tradies. That house is a masterpiece.

6. Never in my life have I taken benefits or had any help from anyone including family.

So ecobird, with your assumptions, can go suck it.

Hi Gingerninja,

Apologies - I don't wish to upset or offend anyone. And certainly not the many younger (and older) people who would like to own their own home. I think that issue is both sad and bad. As I mentioned/acknowledged above, houses have an important consumption dimension - they're not just an investment item.

It was tough enough to get into a house in my day - 40 years ago. Now, it's far tougher than then. New Zealanders seem to have an insatiable demand for property. It's heavily favoured as a form of investment.

I'm not sure what the solution is - or whether there's a solution at all. Concerning Auckland and Wellington, I think it's highly unlikely that either will ever become places where there are cheap/affordable houses available. The horse has long since bolted.

Personally, I favour more balanced development across the regions - especially job creation in the provincial cities through to small rural towns, where property is far more affordable. But I've been blasted here for suggesting that approach.

Property investors do push up house prices by increasing demand - no doubt about that. Property is popular with investors because it's yielded good returns over many decades - no doubt about that either. Government regulations for property tend to tinker around the margins but can have some short-term effectiveness, as we've seen with LVRs etc. In the long run, however, property tends to find its own (price) level as market forces dominate and overseas investors and so forth enter into the arena.

If, say, there was a property crash and that led to a failure of the banking system (not impossible in my view) then that would not lead to a good outcome for anyone. But as I've said, I don't think that's likely - and hopefully it will never happen.

Anyway, those are my thoughts for the moment. I do worry about the current property conundrum and its potential negative effect on the fabric of our society.

The fact that property is heavily favoured and structurally favoured as an investment is big part of the problem.

I also agree that Auckland or Wellington are never going to be places with cheap houses available. But I would say there is a vast difference between cheap housing and affordable housing. 10-15 times the median salary is not affordable. Successful cities attract the best employees, the best employees attract the best wages, the best wages afford the best houses. That is why houses in successful cities shouldn't be cheap. Normal, healthy market fundamentals. NOT because of speculation or foreign capital or poor local government planning, or whatever else has contributed to this sh*#storm.

I would suggest some of the same measures that made housing more affordable back in those days: government build activity, land tax (this time, with lowering of income tax) etc. I.e. policies to rebalance houses from being about investments back to being about homes again.

Policy shouldn't be all about sacrificing young and coming generations of Kiwis for the investment portfolios of those born at the right time.

@Indp_observer .... You are living in text books and trying to prove a tough correlation between two completely different asset classes ... Forget about the theories and Shiller's work ... Here are some facts for you regardless if you call them darklords or otherwise ...

1- property investment has excellent proven returns over the long term 10+ years - and that is $$ terms not percentages ...

2- negative gearing is NOT a crime, it's a facility available by LAW and REGULATIONS for property investors - and there is nothing immoral about using it - some like to call it loop hole but it is there for a reason!!. AUS tried to cancel it and backed off after one month!!

3- Anyone who purchased his first home about 12 years ago and then used his equity to buy a rental after few years has actually paid his Home off after in only 10 - 12 years instead of 25 - 30 years and now has more than 50+% equity in his rental property - if he had bought more properties, then the equity would now be higher. If he had bought them 20 years ago instead of 12 , he is now almost free hold on all of them and getting a small income and paying taxes on that. Is that what you call worse than shares? BTW, this was the sound financial advice 20 years ago to save for your retirement.

4- His net worth $$ today is about 4 -5 times what his worth would have been if he had bought a home and invested any extra money for 10 years in the share market - Why? because he was able borrow 9 times his original investment and borrow again against his equity and make that work for him at an average return of 10 - 15+%pa on the total lot ...while you could only borrow 30% against your A class shares and risk the Margin Calls.

these are practical numbers from the real world - so regardless what names others try to call these INVESTORS or dive deep in the gutters to dig some dirt on them ... they are providing a service and making legitimate money under the sun just like any successful business out there and the returns speak for themselves - otherwise no one would be in this business.

As to the morality of the issue which some sick people try to indulge in agitating the ill informed, then I ask why is it shameful to provide rentals to people who cannot afford buying houses, or need temporary accommodation for few months or years ?... would all motel and hotel operators be Darklords too, how about investors in serviced apartment business ... maybe supermarkets should also give food for free , after all it is immoral to make profit on FOOD - right??

It is so unfortunate and shameful that the NZ public is dragged into this discussion because of political agendas making this subject like hot potatoes in an election year.

How many rentals do you own?

That is beside the point - but my figures are , as I said, very real

I have investment in both asset classes and its the property side that supports the good returns in the share ownership , in fact the first class made it possible to invest in the other.

It's not beside the point. You have a strong bias. More than 5?

Self serving, negatively geared rationalisation.

This risky behavior (negative gearing) can work when the market is increasing in value to increase ones gain via leverage. The reverse is also true, in that when the market is decreasing, one loses money equity quickly. Margin calls, those happen in real estate as well... playing with leverage is a great way to make large sums of money, as well as to make large sums of money disappear. Personally I'm not a fan of gambling...

I think I'll follow Shillers rational wisdom over your 'real world' leveraged property speculation practises that's had a lucky run

There are always people who make money from pyramid schemes.... but then, at some stage, it falls over.

Remember Madoffs investors had to give back the returns they were paid out... would be nice if that happens here when it tumbles down.

I love how the sentiment is all from Baby Boomers implying they were wise and did real hard work, when it was simply a matter of right time right place. *sigh*

It is completely wrong to compare Madoff's fraud with Auckland housing. Madoff practically didn't have any investments that could be sold or earn an income. It was a true Ponzi where investor's money was paid to other investors as returns. That's why some people had to return their income. With Auckland property you have some of the best real estate in the world that actually can earn an income as well.

Keep telling yourself that.

Danger will robinson.

If there were no supermarkets, people in cities would go hungry and produce would spoil in the fields in the country.

If there were no residential property investors, people could own their own homes and pay much less for them.

15 year trends - housing has been going up since before shares were even a twinkle in some historic dudes eye.

Landed Gentry, royalty, nobility, landlords, dictators. Call them what you will, but the rich and powerful have always held property.

A house, mansion, or even a castle may indeed be worthless. But land in invaluable.

Do you really think the 70k + migrants coming here are doing it for shares, bonds, and term deposits?

Good point - so when are we stopping foreigners from buying our houses?

20 years ago would have been good.

>Landed Gentry, royalty, nobility, landlords, dictators. Call them what you will, but the rich and powerful have always held property.

That's why previous NZ governments used land tax to break up such holdings and free land up for everyday "mum and dad" Kiwis. Unfortunately some generations seem to have forgotten the efforts that went into making housing affordable for them, and feel no obligation to pass what they were handed on to the next generation.

It's the passing on that causes the problem in the first place.

We broke up holdings at one point in time, allowing a few extra people to get on the ladder. Once on, they left the property to the next generation - giving them a huge leg up compared to the ones with nothing.

We are seeing the modern version now - Parent's with paper wealth putting it on the line for the kids to get the foot in the door.

The rich get richer, the poor get poorer. You can legislate all you want, but you can't stop human nature.

I O, you're just ignorant

"..... and those who buy a house (or two) in 2017 will be sitting pretty in 2047."

Or, will be bankrupt in 2019.

"the intangible satisfaction of owning the roof over your head roof and enjoying the garden, pleasant neighbours, etc etc etc."

Garden, pleasant neighbors? Now I KNOW you aren't talking about Auckland.

"Better to buy the right house in a boom, than the wrong house in a slump"

I'd argue that by definition, buying a house in the boom is the wrong house.

House prices aren't a ratchet. eg. They don't just go up and then won't go down. They are really the same as any commodity, they can go up an down depending on what someone is prepared to pay for it. Yes there maybe people waiting in the wings to buy if the price does drop, but why wouldn't they want to wait to see how low they will go? Banks also may start getting jumpy, and worried , as they don't want to lend to these buyers at the amount they may want to borrow, if they see the potential for houses prices to drop a lot.

"New data from credit information website CreditSimple.co.nz showed North Shore homeowners under 55 had an average debt of $542,600: the highest debt in the country."

"Some people were already paying interest-only on their mortgage, meaning the debt was not going down, he said."

http://www.stuff.co.nz/business/property/93278506/mortgages-highest-on-…

If you're prepared to wait another 10 years - the same crazy cycle will repeat and the same people will jump on board the housing wave (that apparently won't crash).

New Zealand comes in just behind Iceland for being the world's most peaceful place in 2017:

Well done all those people who restrained themselves from giving others the bash. This has got to be good for Auckland house prices, the city being the best city in one of the most peaceful places in the world.

My Elysium project truly is coming to fruition.

And they live untouched by sorrow in the islands of the blessed along the shore of deep-swirling Ocean, happy heroes for whom the grain-giving earth bears honey-sweet fruit flourishing thrice a year, far from the deathless gods, and Cronos rules over them

— Hesiod, Works and Days

Ask the very rich folk in Johannesburg and Rio about their Elysium. It's starting in our dairies and I can assure you, the contagion will spread as the "have-nots" in society give up on their own humanity because they have nothing left to lose. Having been to those places and actually spoken to both groups, smug is not a character trait of the rich. Fear is the underlying emotion. Maybe even terror. So a little advice to the smug, be careful what you wish for.

So true.

Most "rich" South Africans I know live in houses that seemed straight out of the Movie "The Purge". As one friend put it, "You can have it all, but one bullet and it's gone"

That's what I'm saying Noncents. Houses like prisons. When society becomes disparate and people more desperate and their rage robs them of their humanity. I can tell you some horror stories on the state of mind of some people who have nothing. The terror of people who've encountered that rage.

"The horror! The horror."

From 'The Heart of Darkness.'

Hmmm let me see, South Africa 123/163 and Brazil 108/163 while NZ is 2/163 whereas last year we were 4/163. Seems things are getting better!

The economic impact of violence on the economy is enormous.

On average, violence accounts for 37% of GDP in the ten least peaceful countries, compared to only 3% for the ten most peaceful.

Like I said; we're at the arse end of the world that's what helps to keep us peaceful.

That would mean Papua New Guinea should be peaceful too. I think you need to look a little more closely.

Anyway there is no arse-end now we have the twin-engined wide-bodied jet and the global gateway city of Auckland. Also high speed Internet.

This notion of being the "arse end" is very outdated, gone the way of black singlets and gumboots. It's a Global world now and there is no working class, just consumers, clients and resources of various diverse origins.

Well according to your map there; Papua New Guinea actually is better than the US which ranks 103 where Papua New Guinea ranks 98. And again Papua New Guinea is very close to lots of other countries, which give more opportunity for division and tension.