By Greg Ninness

The latest movements in interest.co.nz's Rental Yield Indicator suggest a significant amount of volatility in the the residential property market as it adjusts to less buoyant conditions.

The Indicator compares the relative attractiveness of residential property investment in 56 locations throughout the country. It tracks movements in the REINZ's lower quartile selling price for three bedroom houses in each area and the median weekly rent for three bedroom houses (collated by Tenancy services) in the same areas, to produce an indicative rental yield figure for each location.

That allows an apples with apples comparison to be made of the income earning potential of rental properties in each district.

When yields are rising that suggests rents are increasing at a faster rate relative to property prices, or that prices could be falling. And when yields are falling that suggests prices are rising more relative to rents.

The yields are calculated on a rolling six month basis each quarter, and the table below shows their movements from September 2014 to June 2017.

Up until the end of last year yields were trending down, reflecting the rapid increase in prices that was occurring in most parts of the country, with rents rising more slowly.

Then the March figures showed yields starting to creep back up, particularly in Auckland, as property prices cooled.

Quite a messy picture

However the latest figures, based on lower quarter selling prices and weekly rents on newly tenanted properties in the six months to June, paint quite a messy picture, with yields up in some areas and down in others. Some of the movements are quite large.

This is most obvious in the Auckland market, where most of the movement in yields has been driven by movements in prices, some of which have been quite substantial, while rents have tended to be mostly flat or showing modest increases.

In Manukau, the lower quartile selling price for three bedroom houses in Highland Park declined by $17,150 in the six months to June compared to the six months to March, it was unchanged in Papakura and declined by $15,000 Pukekohe. Median rents in all three areas were unchanged.

That pushed indicative rental yields up from 3.5% to 3.6% in Highland Park, from 4.6% to 4.8% in Pukekohe and left them unchanged on 4.3% in Papakura (see table below).

The opposite was true in Avondale, where the lower quartile price increased by a whopping $31,375 and the median rent increased by $10 a week, pushing the yield down from 3.6% to 3.5%, meaning Avondale has now replaced Highland Park as the lowest yielding suburb monitored for the Indicator report.

Further out west it's more of a mixed bag, with the lower quartile selling price for three bedroom houses falling by $10,893 in Henderson and increasing by $20,750 in Massey/Royal Heights.

There were also mixed numbers in the north of Auckland, with the lower quartile price dropping by $11,000 in Orewa/Whangaparaoa and rising by $22,000 in Torbay.

Huge price movements

There was similar volatility in many other parts of the country such as Rotorua, which saw an influx of investors over the last couple of years attracted by its relatively high yields.

But in the Rotorua suburbs of Holdens Bay/Owhata/Ngapuna the lower quartile price dropped by $49,750 in the six months to June compared to the six months to March, while in Kuirau/Hillcrest/Glenholme it was down by $33,750.

In Ngongotaha/Pleasant Heights/Koutu it rose by $74,625.

Those are huge price movements for areas where house prices are some of the cheapest in the country.

Such volatility will not be doing any favours for property investors, or the bankers who must decide whether or not to lend them money and how much, both of who tend to like evidence of clear trends on which to base their decisions.

The latest figures suggest the winds of change are blowing through the housing market, and it's becoming increasingly difficult to judge which way they will turn.

Indicative gross rental yields for three bedroom houses in 56 selected areas with high rental activity during the previous six months. Based on REINZ lower quartile selling prices and MBIE median rents in each area. Indicative gross rental yields for three bedroom houses in 56 selected areas with high rental activity during the previous six months. Based on REINZ lower quartile selling prices and MBIE median rents in each area. |

||||||||||||

| Indicative Rental Yields (%) for the Six Months Ending: | ||||||||||||

| Town/region | Jun 2017 | Mar 2017 | Dec 2016 | Sep 2016 | Jun 2016 | Mar 2016 | Dec 2015 |

Sep 2015

|

Jun 2015

|

Mar 2015

|

Dec 2014

|

Sep 2014

|

| Whangarei - Kamo/Tikipunga/Kensington | 5.5 | 5.4 | 5.4 | 5.9 | 6.1 | 6.0 | 5.6 | 7.1 | 6.5 | 6.9 | 7.6 |

6.4

|

| Rodney - Orewa/Whangaparaoa | 4.0 | 4.0 | 3.8 | 3.9 | 4.1 | 4.1 | 4.1 | 4.3 | 4.5 | 4.5 | 4.6 |

4.8

|

| North Shore: |

|

|||||||||||

| Beach haven/Birkdale | 3.8 | 3.7 | 3.7 | 3.7 | 3.7 | 3.9 | 3.8 | 3.9 | 4.0 | 4.3 | 4.3 |

4.6

|

| Torbay | 3.6 | 3.7 | 3.6 | 3.4 | 3.6 | 3.8 | 3.6 | 3.8 | 4.0 | 4.5 | 4.6 |

4.5

|

| Waitakere: |

|

|||||||||||

| Glen Eden | 3.9 | 4.0 | 3.8 | 3.7 | 3.9 | 4.0 | 4.0 | 4.1 | 4.3 | 4.6 | 4.9 |

5.1

|

| Massey/Royal Heights | 3.8 | 4.0 | 3.9 | 3.8 | 4.1 | 4.1 | 4.0 | 4.1 | 4.4 | 4.6 | 4.9 |

5.1

|

| Henderson | 4.0 | 3.9 | 3.8 | 3.8 | 3.8 | 4.1 | 4.1 | 4.1 | 4.4 | 4.7 | 4.9 |

5.0

|

| Central Auckland: |

|

|||||||||||

| Avondale | 3.5 | 3.6 | 3.6 | 3.7 | 3.6 | 3.7 | 3.7 | 3.9 | 4.1 | 4.2 | 4.4 |

4.5

|

| Manukau: |

|

|||||||||||

| Highland Park | 3.6 | 3.5 | 3.5 | 3.4 | 3.3 | 3.3 | 3.6 | 3.6 | 3.8 | 3.8 | 4.1 |

4.3

|

| Papakura/Drury/Karaka | 4.3 | 4.3 | 4.4 | 4.4 | 4.7 | 4.8 | 4.8 | 4.9 | 5.5 | 5.6 | 5.9 |

6.0

|

| Pukekohe/Tuakau | 4.8 | 4.6 | 4.4 | 4.3 | 4.5 | 4.9 | 5.0 | 5.0 | 5.3 | 5.5 | 5.6 |

5.6

|

| Hamilton: |

|

|||||||||||

| Deanwell/Melville/Fitzroy | 4.8 | 4.8 | 5.0 | 5.1 | 5.4 | 5.3 | 5.5 | 6.2 | 6.8 | 6.9 | 6.9 |

6.9

|

| Fairfield/Fairview Downs | 4.5 | 4.9 | 4.8 | 4.8 | 5.1 | 5.4 | 5.7 | 6.0 | 6.8 | 6.7 | 6.2 |

7.0

|

| Te Kowhai/St Andrews/Queenswood | 4.5 | 4.4 | 4.3 | 4.6 | 4.7 | 4.7 | 4.9 | 5.3 | 5.4 | 5.4 | 5.6 |

5.8

|

| Cambridge/Leamington | 4.4 | 4.6 | 4.6 | 4.7 | 4.8 | 5.2 | 5.3 | 5.2 | 5.5 | 5.5 | 5.6 |

5.9

|

| Te Awamutu | 5.1 | 5.0 | 5.1 | 5.2 | 5.2 | 5.7 | 6.2 | 6.3 | 6.5 | 6.2 | 6.3 |

6.4

|

| Tauranga: |

|

|||||||||||

| Tauranga Central/Greerton | 4.7 | 4.6 | 4.4 | 4.3 | 3.7 | 5.2 | 5.2 | 5.6 | 6.0 | 6.1 | 5.9 |

5.9

|

| Bethlehem/Otumoetai | 4.0 | 4.1 | 3.7 | 4.2 | 4.2 | 4.6 | 4.8 | 4.8 | 4.5 | 4.8 | 5.3 |

5.4

|

| Mt Maunganui | 4.4 | 4.4 | 4.2 | 4.2 | 4.4 | 4.8 | 4.6 | 4.7 | 5.4 | 5.7 | 5.6 |

5.2

|

| Pyes Pa/Welcome Bay | 4.3 | 5.3 | 4.8 | 4.9 | 4.8 | 5.4 | 5.5 | 5.3 | 5.9 | 5.7 | 5.7 |

5.8

|

| Kaimai/Te Puke | 4.9 | 5.3 | 5.4 | 5.5 | 5.6 | 5.8 | 5.9 | 6.2 | 6.4 | 6.2 | 6.2 |

5.7

|

| Whakatane | 6.0 | 6.1 | 5.8 | 6.5 | 6.6 | 6.4 | 7.1 | 7.3 | 6.7 | 6.3 | 6.7 |

6.9

|

| Roturua: | ||||||||||||

| Holdens Bay/Owhata/Ngapuna | 10.5 | 8.0 | 9.7 | 10.7 | 9.4 | 8.7 | 8.3 | 8.7 | n.a. | n.a. | n.a. | n.a. |

| Kuirau/Hillcrest/Glenholm | 5.5 | 4.9 | 7.3 | 7.5 | 6.4 | 5.9 | 6.3 | 6.6 | n.a. | n.a. | n.a. | n.a. |

| Ngongataha/Pleasant Heights/Koutu | 6.2 | 8.6 | 8.2 | 7.2 | 7.9 | 7.7 | 8.0 | 8.2 | n.a. | n.a. | n.a. | n.a. |

| Hastings - Flaxmere | 9.3 | 8.9 | 8.6 | 9.4 | 9.3 | 10.9 | 11.5 | 11.0 | 12.1 | 12.2 | 11.7 |

11.8

|

| Napier - Taradale | 4.9 | 5.0 | 4.9 | 5.1 | 5.5 | 5.4 | 5.6 | 5.5 | 5.3 | 6.2 | 6.3 |

6.1

|

| Taranaki: | ||||||||||||

| New Plymouth Central/Moturoa | 4.9 | 4.7 | 5.3 | 5.1 | 5.4 | 5.8 | 5.4 | 5.5 | n.a. | n.a. | n.a. | n.a. |

| Waitara/Inglewood | 7.2 | 8.1 | 7.0 | 7.7 | 7.7 | 8.8 | 8.9 | 8.0 | n.a. | n.a. | n.a. | n.a. |

| Whanganui | 8.6 | 9.1 | 9.7 | 9.7 | 10.3 | 9.6 | 10.0 | 14.9 | n.a. | n.a. | n.a. | n.a. |

| Palmerston North: | ||||||||||||

| Kelvin Grove/Roslyn | 6.5 | 6.6 | 6.6 | 7.0 | 7.3 | 7.4 | 7.2 | 7.2 | n.a. | n.a. | n.a. | n.a. |

| Palmerston North Central | 6.0 | 5.9 | 5.6 | 6.5 | 6.3 | 5.6 | 5.5 | 6.2 | n.a. | n.a. | n.a. | n.a. |

| Takaro/Cloverlea/Milson | 6.2 | 6.1 | 6.3 | 6.7 | 6.8 | 7.2 | 7.1 | 7.3 | n.a. | n.a. | n.a. | n.a. |

| Kapiti Coast: |

|

|||||||||||

| Paraparaumu/Raumati | 4.9 | 4.8 | 5.3 | 5.6 | 5.7 | 5.9 | 6.0 | 6.1 | 6.2 | 6.1 | 6.1 |

5.9

|

| Waikanae/Otaki | 4.7 | 5.2 | 5.5 | 5.8 | 5.8 | 5.9 | 6.5 | 6.8 | 6.6 | 6.7 | 5.5 |

5.4

|

| Upper Hutt: | ||||||||||||

| Heretaunga/Silverstream | 4.7 | 4.7 | 4.6 | 5.3 | 5.6 | 5.8 | 5.8 | 6.1 | n.a. | n.a. | n.a. | n.a. |

| Totara Park/Maoribank/Te Marua | 5.8 | 5.8 | 5.2 | 5.7 | 6.2 | 6.3 | 6.2 | 6.8 | n.a. | n.a. | n.a. | n.a. |

| Lower Hutt: | ||||||||||||

| Epuni/Avalon | 4.9 | 5.1 | 5.6 | 5.1 | 5.5 | 5.8 | 5.2 | 5.1 | n.a. | n.a. | n.a. | n.a. |

| Taita/Naenae | 5.6 | 5.8 | 6.1 | 6.2 | 6.5 | 6.8 | 6.9 | 7.1 | n.a. | n.a. | n.a. | n.a. |

| Wainuiomata | 5.9 | 5.9 | 6.3 | 7.0 | 7.2 | 7.7 | 7.7 | 7.7 | n.a. | n.a. | n.a. | n.a. |

| Wellington: |

|

|||||||||||

| Johnsonville/Newlands | 5.0 | 4.9 | 4.8 | 4.8 | 5.2 | 5.5 | 5.4 | 5.6 | 5.8 | 5.6 | 5.5 |

6.2

|

| Vogeltown/Berhampore/Newtown | 4.5 | 4.2 | 4.1 | 4.6 | 4.9 | 5.4 | 5.2 | 5.5 | 5.1 | 5.5 | 5.2 |

5.6

|

| Tasman: |

|

|||||||||||

| Motueka | 4.4 | 4.0 | 4.0 | 4.7 | 5.3 | 5.2 | 5.4 | 5.3 | 5.3 | 5.5 | 5.6 |

5.5

|

| Richmond/Wakefield/Brightwater | 4.6 | 4.7 | 4.6 | 4.8 | 5.3 | 5.3 | 5.3 | 5.5 | 5.6 | 5.6 | 5.8 |

5.9

|

| Nelson - Stoke/Nayland/Tahunanui | 5.0 | 5.1 | 5.1 | 5.2 | 5.3 | 5.5 | 5.7 | 5.8 | 5.9 | 5.7 | 5.7 |

6.0

|

| Blenheim | 5.6 | 5.8 | 6.3 | 6.5 | 6.5 | 7.0 | 7.0 | 6.4 | 6.5 | 6.5 | 6.6 |

6.5

|

| Christchurch: |

|

|||||||||||

| Hornby/Islington/Hei Hei | 5.6 | 5.6 | 5.7 | 6.1 | 6.1 | 6.0 | 6.0 | 6.2 | 6.2 | 6.3 | 6.5 |

6.3

|

| Riccarton | 4.7 | 5.0 | 5.2 | 5.5 | 5.0 | 5.7 | 5.0 | 4.9 | 5.9 | 5.2 | 4.9 |

5.1

|

| Woolston/Opawa | 6.0 | 6.2 | 6.5 | 6.6 | 7.4 | 6.3 | 6.4 | 6.6 | 6.8 | 7.3 | 7.2 |

8.0

|

| Ashburton | 7.0 | 8.3 | 8.4 | 6.3 | 6.1 | 6.2 | 7.0 | 6.9 | 7.0 | 6.8 | 6.7 |

7.2

|

| Timaru | 5.7 | 6.0 | 5.9 | 6.1 | 6.4 | 6.5 | 6.4 | 6.2 | 6.6 | 6.8 | 6.7 |

6.3

|

| Queenstown/Frankton/Arrowtown | 4.6 | 4.3 | 4.1 | 4.5 | 4.3 | 4.6 | 5.2 | 5.0 | 4.8 | 4.9 | 4.7 |

5.3

|

| Dunedin: | ||||||||||||

| Kenmure/Mornington | 6.3 | 7.5 | 6.5 | 6.3 | 6.7 | 7.9 | 7.1 | 6.6 | n.a. | n.a. | n.a. | n.a. |

| Mosgiel | 5.4 | 5.5 | 5.7 | 5.7 | 5.7 | 6.4 | 6.4 | 6.1 | n.a. | n.a. | n.a. | n.a. |

| South Dunedin/St Kilda | 8.0 | 7.9 | 7.5 | 8.1 | 7.4 | 7.2 | 8.0 | 8.2 | n.a. | n.a. | n.a. | n.a. |

| Invercargill | 8.3 | 8.3 | 7.9 | 8.3 | 8.4 | 8.7 | 9.1 | 9.0 | 6.7 | 9.0 | 9.2 |

9.5

|

| *Yield is a property's annual rent expressed as a percentage of its purchase price. The yield figures in this table are gross, and are calculated from the REINZ's lower quartile selling price for three bedroom houses in each area during the previous 6 months, and the median rent for three bedroom houses calculated from new tenancy bonds received by Tenancy Services of the Ministry of Business Innovation and Employment for the same areas/period. | ||||||||||||

102 Comments

Given the sizeable capital gains reaped over the 2014-16 upswing period, it should come as no surprise that some (but not all) residential property investors/landlords have to accept lower yields in 2017.

It's the nature of property investment. If you can't handle some volatility, it may not be for you.......

Savvy investors tend to take a long-term view. History shows that most do alright.

History also shows that dumb bubbles orchestrated around residential property are devastating for national economies and not necessarily good for "investors" at the margins. Basing investments on the "prices always go up because they do" belief is the rubbish that the sheeple are sold. The behavior of the sheeple is an essential element in a speculative bubble. That's a more time-honored truism that "prices always go up because they do."

Property value will double in 7-10 years.. said my Ponsonby's Real Estate agent.

Btw, in 2010 if you invested $100 in Bitcoins, it's worth approximately 75 millions in today's value, just slightly ahead of a 3 bedder in Greylynn

Your Ponsonby real estate agent might be correct......

But you need to remember that real estate agents are in a classic "conflict of interest" situation. Their commissions usually bear a relation to property values, so they may have a (personal) financial incentive to promote/predict etc increases in property values.

Thus, best take what agents say with "with a grain of salt".

And consult with others as well, before deciding what to do.

Hold on, they "might be correct"? That is to say, assuming current wage growth continues, in 7 years that property prices in Auckland might be 20x income? Is that what I am hearing you say?

I mean, we can have different perspectives on things, but can't we all accept that possbility is straight out batsh$t crazy!?

Really? Can't we just call that now?

Hi Bobster,

Everyone is entitle to their say - and one of the merits of this blog is that it pretty well allows contributors freedom of speech. All of us are entitle to agree or disagree with what's said - and if we wish, we can respond accordingly.

To me, that's pretty democratic. So I'm happy to go along with it.

Yes, but.....some stuff is just so crazy that you don't really need to spend lot of time on it. It seems to me the projection of houses prices at 20x income in 7 or even 10 years is one of those things. Hey, why stop there, lets say 40x?!

It's bonkers, right? So let's call it.

Bobster, in theory wages should increase over time. So in 7-10 years time house price won't be x20 the average wage, it will be more like 19.6753 times

Ah, I see you've included in your calculations an assumption that National will be running the country.

Bobster, look at a chart of house prices over the last 30 years. In 1987, when your house was worth $75k and so much more expensive than in the past, you could not imagine it could keep on rising and one day reach $100k...

We need to talk real prices, not nominal. It makes most sense to talk of houses in the context of income multiples, which takes account of wage growth and is more in line with real numbers. It is also a better measure of relative affordability. So, assuming wage growth at its current rate of 2%ish, if a doubling of house prices in 7 years from now means that houses go from average of 10x income to 15x or 20x, then sorry but that is bonkers.

It's bonkers now, it was bonkers 10 years ago too. It's a nice idea that house prices should rise at the same pace as income so everyone can afford a house. Has it happened ? No, there is no correlation between house price inflation and wage growth, I'm not saying this is good or right but it's true. I believe in the long term, home ownership will continue to fall. When it goes below 50% CGT and the likes will apply as it won't be political suicide anymore.

IMO there's a better gauge of whether house prices are overvalued or not

The idea that house prices can continue indefinitely to rise faster than incomes is literally unsustainable - there's only so long that reducing interest rates and increasing mortgage terms can soak up the difference. I don't know if the end of the road is now, but it will come one day. Extraordinary gains in the past do not automatically mean extraordinary gains in the future, or else investing would be far, far easier than it actually is.

Prices are a reflection of a decrease in the value of money as well. There is no limit to how much less money will buy.

Hi Bobster,

As I've already indicated, you're entitle to your own views.

What people wish to spend time considering is up to each individual.

Happy to let freedom of thought and expression prevail, in accordance with democratic principles.

Sure, of course, happy for people to spend as much time as they like evaluating patent nonsense

Bobster, the thing you and many bears are missing (think Roger Kerr),is worldwide secular deflation with declining interest rates. This trend may well continue and the smart money including Bill Gross the bond market king, (note Bill Gross makes money essentially predicting medium to long term interest rate moves, self made billionaire moved from counting cards at blackjack to managing 250 billion US) believes the Central Banks models are wrong and post GFC they are less than useless and we will see minimal inflation/ deflation, with continuing low/ falling interest rates.

What happens if NZ interest rates decline to UK levels? Natwest mortgage rates at present are 2 yr fixed 1.14%, 5 yr fixed 1.73%. This may make a 20 times income multiple eminently affordable and I would expect to see retiring baby boomers with funds falling over themselves to secure a 3% net yield on a rental property, especially with term deposit rates less than 1%. Most cannot adapt to the new paradigm, the high debt load that governments/ businesses/ individuals have locks in low interest rates. The US essentially determines worldwide interest rates, if rates rise will the Fed under government direction let the economy implode or will they print dollars to buy bonds and drive interest rates down? Past behaviour suggests they would print money rather than usher in a depression. I think I will bet on Bill Gross being right rather than Bobster.

Who says the declines in rates are permanent? Weren't rates at 9% or so in the GFC? is money going to be nearly free from now on, will interest be effectively abolished? Who knows. You say rates can't rise cos everyone will be bust, well, let's see. You are making the classic mistake of thinking the future must be like the past or the present. I doubt it will be. I don't care what gross says. He may well be wrong.

20x income mortgages over 25 years are plainly not affordable. You pay nearly all your income in debt service. 15x is also pretty loopy.

Bobster, I'm not making the mistake of thinking the future will be like the past. I would say your anchoring to previous mortgage rates of 9% is making this mistake. Regarding free money, note 20% of bonds worldwide have negative rates so would be classified as better than free money. For a moment open your mind, and think to yourself who has been right the last 8 years, has inflation kicked in and have interest rates risen? Who has made the money? Because as a share-trader the market will tell you whether you are right or wrong. Did the bears who sat on the sidelines, stating the sky would fall in since 2010 make money, or did those who purchased assets make money? The saying is some people make things happen, some watch things happen, and some say what the "f**k happened"?. Which category have the 2010/ 2011 bears found themselves in?

wow. Even for you, outstandingly ridiculous. It's not possible to continue doubling exponentially. Sigh.

Im happy to buy a 4th rental with low yields as long as I can sell it for 3 times the amount in about 5 years time...

And if you can't? If there were a guarantee that prices will be significantly higher in 5 years, then prices today would be even higher in anticipation. Do you know something the rest of the market doesn't?

Hahaha Love it !! ..... and that is just about the limit of the thinking with these "savvy" property investors !

OMG! It's not hard to spot where lies the hazard to the entire banking system!

I am happy for you to be declared bankrupt in 5 years time, which seems a more likely outcome

That is investing for capital gain rather than as a landlord so the IRD will be treating the value gain as the business not the landlording side which makes the rental income.

To be clear - Mike Perro is being completely sarcastic with this post right?

Hard to tell, statements by property investors are heavily influenced by poe's law

Good luck

And pay tax.

Why is everyone concerned about Property investor's yield and what they can or not earn from their investment ? ... I thought no one cares if they make a profit or a loss ?

Hi Eco Bird,

I think you're correct with respect to a fair chunk of the property investing community. Annual profit/loss isn't a paramount consideration for many residential property investors.

That's part of the reason why most of them won't sell out - despite decreasing yields (and the general slowing-down of the current market).

They're in it for the long haul......... and, as I mentioned above, most of them seem to do ok.

That pretty much covers it right there, "annual profit/loss isn't a paramount consideration". In the long term there is only tax free capital gain, and the medium term is a balancing act farming debt, tenants, and govt subsidy against each other. Follow link for policy summary on this kind of ..."business".

http://www.interest.co.nz/news/87057/election-2017-party-policies-housi…

Plan your vote carefully,

If p&l isn't a concern it's speculation. Pure and simple. Which is of course your right, but you are liable for CGT if intent was to sell.

Current yields are not a factor as many investors bought at a different time and see thier actual income as a multiple of what they bought for

But that would be In incorrect way of viewing yields. Yield is calculated on asset value, not purchase price. Because, if it is indeed worth that, why not cash out?

Also, given the credit growth in 2016, I am am pretty sure many bought at the top of the market

Rental yields in Auckland are highly likely to worsen as the rental market becomes more saturated so there will be a lot more competition for Tenants. This is because those who need to relocate and can't get the selling price that they're expecting will decide to rent out their property rather than sell it.

Yep, totally agree. Investor properties which aren't currently being sold will also back up. The sale numbers are terrible. These unsold houses need to go somewhere and it will be the rental market. Tauranga looks pretty soft for rentals already.

But with Auckland's population increasing by 45,000 people a year (or not far off 1,000 people each week) rental accommodation will continue to do ok. As always, it's the numbers' game.

Try and find a good quality rental house (not apartment) in Central Auckland right now. If you want a decent spacious house with drive-on, quiet neighbourhood, sunny, outdoor living/BBQ area and so forth, then it's slim pickings.

Just ask anyone who's out there searching......

Auckland rentals are going nowhere, so the rental market is currently reasonably well balanced. This is so even with the current levels of immigration. Materially increased rental supply is likely to put downward pressure on prices.

Yes it's a numbers game, but you seem to ignore the numbers. Rentals are broadly static in real terms, have been for a while. Please focus on the numbers, anecdotes aren't v helpful to anyone.

Really, Bobster?

Suggest you go check out the rental sites!

As I said, good quality, well-located rentals remain hard to find in Auckland - despite mid-winter being the off-season.

You state: "Materially increased rental supply is likely to put downward pressure on prices."

In fact, there are two sides to any (and every) market. Focus on supply, without properly acknowledging DEMAND, is spurious. (There's much more to it than immigration.)

With all due respect, you need to be more rigorous. (I note that you've been caught out on this before.)

Changes in the supply of rental properties may have a significant impact on rents. See Christchurch after the quake. That seems an easy proposition to accept. Supply is normally relatively fixed, but if sales tank and people instead put houses into the rental market then the effect on rental supply may be material ie it may materially increase.

I don't understand your comments on demand. Not sure anyone does. Are you suggestion that demand is elastic ie reduced rents may "induce" more rental demand? I can't see how this will support rentals at a given level, as to "induce" demand rentals must by definition have fallen. And if rentals then increase, that induced demand will disappear.

Look, with respect I don't think what you say makes much sense. I appreciate it is difficult for investors to accept that house prices aren't caused by underlying owner occupier demand, but you just need to embrace it. That's what the rental data shows ie over the last few years there have been no significant changes in occupier demand which are proportionate to increases in house prices. It's the killer metric, it's beyond doubt.

Hi Bobster,

You write: "but you just need to embrace it."

I don't just embrace anything. There's no point in embracing something just because someone wants me to support their viewpoint. I don't come here to do that......

My approach is to think critically, monitor, evaluate and then re-evaluate. And the process goes on. Happy to listen to others but what I strive for is objectivity.

Sorry - but I'm just not interested in "embracing" or the like.

Sure, well it is pretty clear what the rental data is saying.

Bobster, your supposed supply from people who cannot sell their family home, deciding to rent these houses out. Pre-supposes that these families will elect to join the homeless and sleep under bridges, rather than moving into another home. Your statement is illogical.

I note the rental data from trademe showed Auckland rents increasing at more than double the rate of inflation and Wellington's increasing 12.5% over the last 12 months. The Auckland data is consistent with a reasonably balanced market, but the Wellington data is consistent with a significant housing shortage. Neither data set is consistent with excess supply, compare this to Christchurch.

No it doesn't. Those owner occupier families could themselves elect to rent a home, if they thought this was a temporary blip. I assume they actually have salary incomes. Or they could buy into the same market on the basis they are exchanging like for like, so it doesn't matter. i would think the latter was more likely, but the former is also possible.

Yes Auckland rents have increased but by stuff all. I wouldn't say an increase of 2ish% over inflation was a major leap. That increase is totally disproportionate to the large increases in prices. Yes Wellington does look like a shortfall. But the trademe figures can be a bit flakey for smaller samples.

Bobster, renting their house out does not add to supply, unless they become homeless. They either buy someone else's house and the owners or tenants have to move out and find a new house, or they rent a house that leaves the supply of rental houses in the same net position ie no change, they let their house but rented someone else's.

ah yes give u that, good point

Nope, it isn't.

It's an ability to pay game.

You talk about DEMOGRAPHICS all the time, but, interestingly, perceive it completely incorrectly.

I would be very surprised if our current immigration policy is impacting rents anywhere other than the central CBD and Papakura.

Evidence for this is the fact that Auckland isthmus areas rents have been relatively flat over the past few years. Chances are if you are a landlord in those areas, you need reliable, relatively wealthy tenants to pay your $800k mortgages. Minimum wage, unskilled imports aren't a landlord's first choice in these areas due to this obvious fact.

The bad news is that the supply of this relatively wealthy tennant is going to substantially decrease relative to total population if things are left unchecked. Labour mobility, etc. Auckland is stuffed - It no longer supplies the relative wealth it used to, except to poor people. This is the beginning of the end for the city.

So, logic would dictate that there will be more (same amount) of landlords chasing, effectively, dwindling demand. The natural result of this is downward pressure on prices and exit of suppliers.

I predict a huge amount of economic flight from the place in the next 10 years. Enjoy the capital gains if you got them. If you haven't cut loose what you can now and look at guaranteed yield commercial property in Hamilton and Tauranga.

Correct nymad, We're also recognized as one of the most expensive places in the world in comparisons to rent and income ratios and that's largely driven by Auckland and Wellington's rental market.

That very much reduced the high skilled well educated works from wanting to come to NZ.

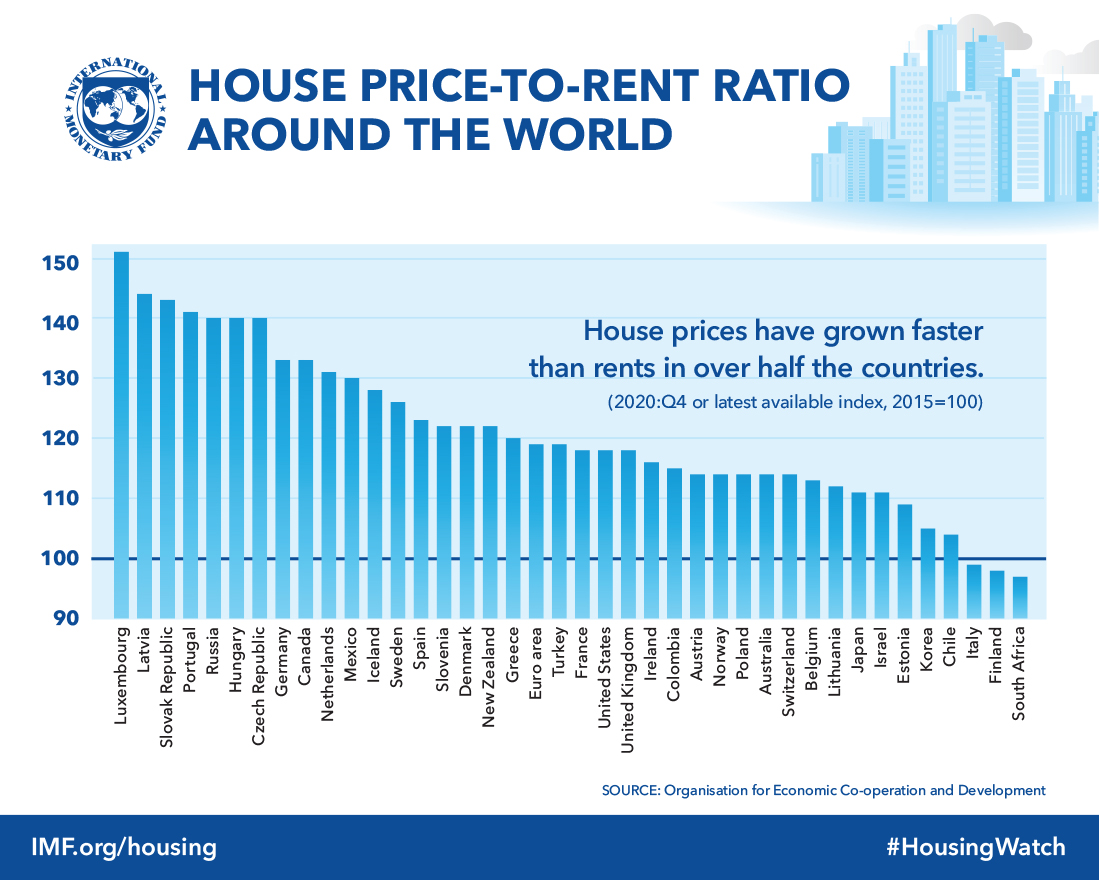

IMF stats: http://www.imf.org/external/research/housing/images/pricetorent_lg.jpg

{kind=link}

Hi nymad,

You write: "Auckland is stuffed - It no longer supplies the relative wealth it used to, except to poor people. This is the beginning of the end for the city."

That's a subjective view of extreme pessimism. Most likely a reflection of personal biases.

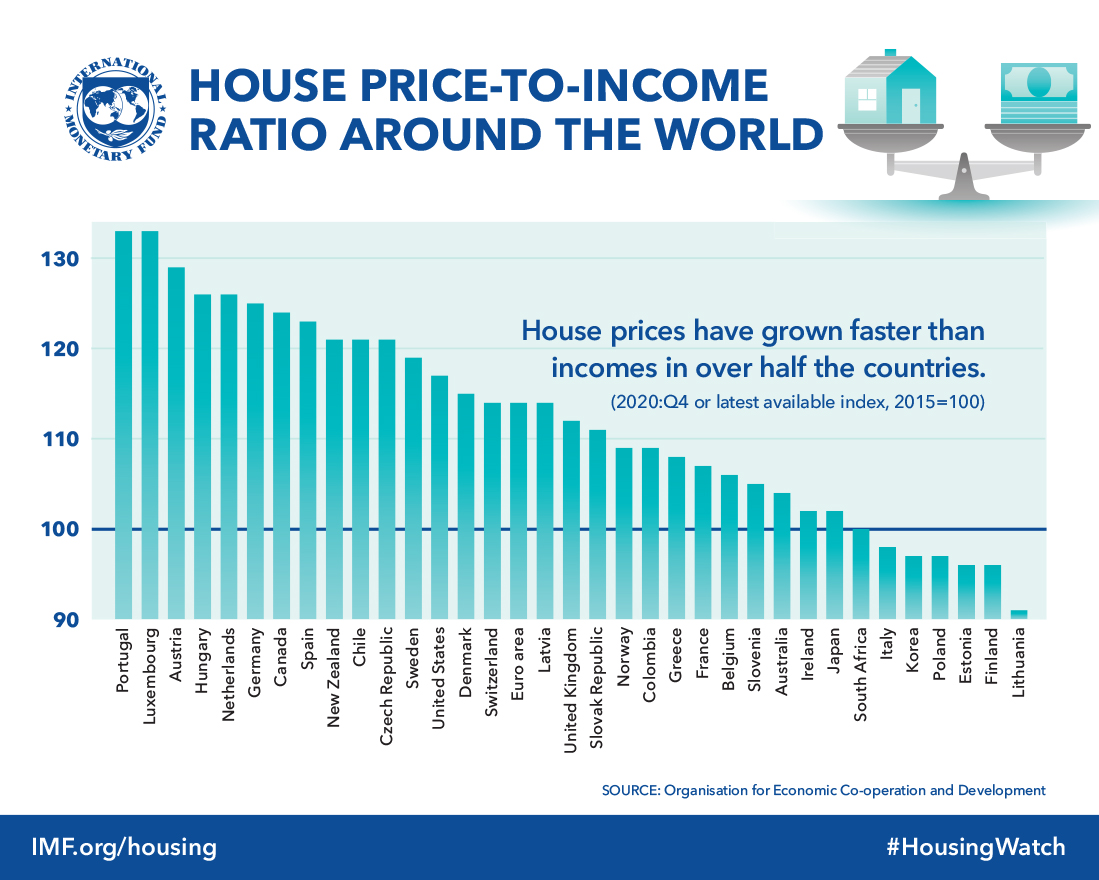

Well you might want to take that up with the IMF (International Monetary Fund), who have research this far more than you ever could. They also say that NZ (Mostly Auckland) is stuffed too!

IMF House Price To Income Ratios Around the World

http://www.imf.org/external/research/housing/images/pricetoincome_lg.jpg

{kind=link}

If that's the one thing you took exception to in that comment, I'm not worried.

I mean, don't debate me on the content. Just assume I have some sort of bias.

On the notion of pessimism - what's wrong with that?

It's better than advocating the opposite when the evidence suggests the opposite.

"On the notion of pessimism - what's wrong with that?"

Pessimism focuses only on the negative, like a cancer, it spreads into all areas of one's life, friends, family, business etc until there is only darkness left

If you are going to quote me, quote the whole statement including the subsequent clausal sentence.

That was pure Yvil man

I agree with your final conclusions, however my logic is different.

Cities attracting young poor people is what they are meant to do. A young energetic workforce is not a fault, it is a feature. What happens next is where things get bad for Auckland.

Cities exist and flourish by creating wealth amongst poor people. Poor, young people get together in cities to create new ventures and take advantage of the opportunities provided by the cities to grow. Capital is attracted to this dynamic growth and the city flourishes. Poor people become wealthy, everyone wins.

What Auckland has done is slow its construction rate so much, that the opportunities for new groups of poor young people to grow within are getting reduced. There is becoming less opportunity for young poor people in Auckland, than in Tauranga or Hamilton or Melbourne. Auckland is constricting the ability for dynamic growth and thus will attract progressively less capital investment as time passes.

Nymad, if you were a landlord of properties in high end CBD areas you would realise that your tenants would typically be professionals aged from 23-35 years, who flat together and pay $200-300 per room, rather than families. This means the rents are not to much of a problem, my most recent let was a 3 brm to three female friends a lawyer, marketing person and back office derivative risk manager at one of the big four banks. The rent was not an issue, they just wanted a modern, freshly decorated property, near the CBD.

I think that was largely his point. This segment is sought after ... professionals with good income... by landlords and there is an expectation of quality. Much of the recently purchased housing stock is not quality... think Clendon, Manurewa, Randwick park... which all shot up in value. These will struggle to attract the kinds of tenants required to make sense financially.

Prices ran themselves upwards on perceived demand, they can just as easily (or more so) unwind.

What's more, good quality tenants rarely have rent increases, because a savvy landlord understands keeping them there happy for longer reduces vacancy risk.

Well spoken, mja.

There's no shortage of young professionals (singles) earning top $$$ who want nice houses in central Auckland.

A good quality 4 brm house in the inner city (e.g. Ponsonby) with drive-on for a couple of cars and some outdoor/BBQ living can easily fetch $2,000pw. That's the sort of house/location they want.

But such rental houses are damned difficult to find - and often professional couples will be chasing them too.

Most have to settle for apartments.

So in complimenting mja, you compliment me - He just reiterated my point.

So, thanks.

"There's no shortage of young professionals (singles) earning top $$$ who want nice houses in central Auckland."

Well, there mustn't be an oversupply of them, either - because rents haven't moved on those properties for a while..

And FYI - that $2k figure you quote...There is property on Paraitai Dr for less than that figure per week, if you check Trademe right now... In fact, there are only 18 properties in all of Auckland Central that are listed for rental in that price bracket.

You are deluded by your own stupidity to suggest that there is huge demand for that high end sort of property.

Either you are drinking the koolaide by the gallon, or you are trying to sell it.

I don't care which - I'm not the one who is made to look stupid by the comment(s).

Hi nymad,

You write: "In fact, there are only 18 properties in all of Auckland Central that are listed for rental in that price bracket."

That's because they get snapped up pretty quickly.

There is now a vary large number of tenanted properties in Auckland fetching over $2,000pw.

In fact, there are some houses (and luxury apartments) fetching over $4,000pw.

hahaha

Not so sure there's as large a market here as you think.

But let's imagine there is. What this proves is that properties are massively overpriced and those on high incomes might rather rent than own. The Paritai drive one for example - gross annual rent = 104k, value of property = $3.7m, so gross yield of 2.8% -- before any costs. Ouch.

Toothypoint, suggest that you rethink your shortage of nice houses in central Auckland for rent. Quite a few . available and waiting on multiple websites. The market has turned ,no plateau, no soft landing , its become somewhat constipated . You appear not to have noticed the flow of data.

Interesting comment, Cowpat.

I see that your mate nymad, above, says there are only 18.

Well, you can't both be correct.......

Toothypoint . Correct about your delusion, stupidity or koolaid drinking ?

No point trying to dodge the issue, Cowpat.

Everyone here can see that either you or your mate, nymad, has stuffed up.

By avoiding the issue, you create the impression that it's you that's made the botch-up.

Well, it wouldn't be the first time......

Yeah right... because everyone has a spare $1M in their back pocket to buy somewhere else while they rent their house out... pfft

Owners occupiers who are moving may well chose to buy in the same market, but investors may well tenant it and try again later.

Yeah right... because everyone has a spare $1M in their back pocket to buy somewhere else while they rent their house out... pfft

Should this website be called PropertyPrice.co.nz???

Apart from borrowing and using the bank's mortgage money, who would then overlook the 6% after tax yield from quoted industrial property shares?

You can even get the bank to give you a margin lending facility on those and are able to sell the shares within a day , pocket the cash in three and move on.

When median rents are used alongside lower quartile selling prices to convey a favourable gross yield it is understandable why so many property 'investors' are removing money from their own pocket each week to cover the outgoings and maintain the illusion , whilst seeking further' investors' to enter the 'scheme'

The headline indicates that 'investors' face headwinds. Yes. As a person who owns property and also is in business with employees I see the change as just one where 'investing' has been basic, easy and able to be done by anybody, to a situation where is just as hard as everything else already is.

Well said KH

Bobster, if , BIG IF, if a big amount of investors over the last 2 years brought mainly low to medium priced housing and have tenants in, if slowly these investors got rid of half and ex renters brought them making them now owner occupied houses and to also throw something else in you mighted like me to say but I think you make the most sense on here, that is this ONLY 3% that entered the market of overseas investors that mainly pushed up the mid to high price bracket started exiting what's your view

Sorry, don't quite follow, what's the question?

If housing is simply being changed from renters to ownership, my tenant buys my rental , wouldn't property prices not change

You may be a willing seller. The new owner will take advantage of your keenness --or not.

Price will depend on the whole market.

What will you do with the net cash you get? What is the new owners cash flow before and after?

Who is competing for your property and how does yours stack up against others?

Complicated ain't it?

Anything but simple.

I don't know. It's very chicken and egg isn't it. A higher volume of rental properties in a speculative bubble pushes up prices but moderates rents. If rentals are sold to owner occupiers it reduces rental supply but also reduces rental demand. Is the effect on prices neutral? Don't know. Pass.

Just wondering housing shortage, rental shortage u would think with high immigration, people can't afford housing with thousands of houses for sale , overseas investors gone but make no difference, interest rates so low when in 2008 they were 8.5%, I give up

In simple math; say before we have 120 tenants with 60 rentals available = 2 per rental. Now 180 tenants and still 60 rental properties = 3 per rental. This trend is already happening in Sydney and Melbourne where the head-tenant will try to squeeze more people in to keep their rental cost down. With the current tenancy laws (which is pretty pro tenant), there isn't much a landlord can do about it.

All I can say bobster is housing is unaffordable , 5x is the barrier, and if interest rates, risk, outside forces aren't keeped in check I guess nz will keep doing this boom bust wast of time and happen quicker

Cashflow is the oil in the engine, I would not buy a property if I cannot extract at least 2% yield above the mortgage rate.

Unless you are an economic refugee from the Chinese crackdown.

Then yield is not in the mix. Capital preservation is.

That may involve holding on to any property so that there is no show of cash movement.

.

Watch it... tothepoint, Eco bird et al will tell you you're not a real investor for wanting cashflow and positive yield

I don't see why the fact that housing goes up over time keeps coming up, I'm sure everyone knows that, of course it does , and everything does, it's the booms and busts between every 10 years we seem to keep having, if you can afford to keep your house or rental or rentals because you were wise, that's great, hopefully most people over the years do, but on the other hand threw boom period some make money and we seem to go to far, what in to far, I don't know, but here we are again like many times before hoping for the best, just as some made a killing some will get crushed, buy low sell high, first in wins the most, first out dont loose so much, keep your rental for 30 years and pay it off, everyone to there own, read ya tea leafs

This is a bit of a rubbish article really

No invester goes "yay my yelds are up but the value of my investment has dropped" or "oh no my yields are down but my investment value has risen".

Most have a calculation on what their yield is based on what they owe whilst getting a capital gain over time. When capital gains disappear then a decision on whether to take the profit has to be made, and the alternative is to stay in for the long haul and expect the investment to rise over time. This option will have to take into account the probability of a massive correction in the medium term, which looks inevitable.

I imagine it's more aimed at new/topping up investors deciding where to allocate their capital, and it should be useful info for current investors too. If I saw my risky investment returning 4% before costs and vacancy, I'd be seriously looking at selling and reinvesting elsewhere.

Because housing can be pushed up in price from many ways , low interest rates , overseas investors, momentum,government,RBNZ, making timing a issue for those to young or saving then having to save more missing out doesn't mean they shouldn't try to cheer the market down us owners cheered it up, there's no difference at all, it's not as if this is the first time this has happened it's about every year ending in the number 7, and generally lasts 4 years, and didn't 1967 last to 1974 and drop by half, the years that followed were good I think but didn't get back the gains for years, 2002 to 2008 was great, but Iv never seen such a short boom as this, special outside Auckland

i thought this was a housing and immigration election, NO MORE

Bobster 20x could be ok, it can't b wages because we'll never export a thing again, didnt Ozzie just price itself out of the car building market and think it was smart take wages up and housing so high, like us I guess, dumb and dumber, but we have taken mortgages from 20, 25, 30, many to death is the answer, and we spend 75% of our weekly wages on a mortgage to, who needs money to buy stuff that people don't need to make anymore

You are saying house prices at 20x average incomes is ok? So you are saying you could service a mortgage that was 20x your income over 25-30 years? Err, no you can't, that's loopy.

I'm joking, sorry I wasn't clearer , change mortgages to 60 years haha, that's how stupid all this is

Don't know why interest rates seem a big deal, if they were 9% now like 2008, it would be a big deal because they could be dropped from 9% to normally around 4.5, at your bank, but the RBNZ is already at 1.75 % and isn't that a new low, interest rates aren't a big thing , Unless we can't stop them from going up, now that's a big problem

Ok 20x income , rents so high 20 in each house, the rich own everything because they own homes now and from this day on homes owned by the now old money, sorry we don't say 20x any more just renters forever, lucky we do have governments to stop this bullshit

If it gets to that point Gareth Morgan might become PM on a young voting base who want to return NZ to its historical mix of land tax and income tax.

Property investors were buying 5 or more years ago and now pay tax on the rental profit their houses earn.

Property speculators purchased more recently and are negatively geared with rents not covering their outgoings. Mortgage, insurance, maintenance and rates being an income loss which reduces their tax burden and erodes their regular incomes.

Property speculators dream of capital gains and the opportunity to pay tax on the profit they hope to make. If the property market corrects they lose big time. They gambled.

Unless investors have a big portfolio they have not been in the market for a couple of years now. They wait patiently paying tax on their rental income wondering when the next price correction will be. When that inevitable correction happens the property market can welcome back the investors as they feed off the speculators who timed it wrong.

Everyone knows that Auckland has done it's dash and prices are now going backwards. In my opinion you'd be bat-sh!t crazy to buy in Auckland today.

Given the current state of affairs in NZ at the moment, id like to ask a few questions to you fine folk out there.

I have a mate, he is small in stature but huge in wisdom, and cash for that matter. At the moment this cash and wisdom has him stuck between a rock and a hard place as to what to do.

He has no PPR and rents in the Southern Lakes. If you had cash would you be buying real estate in this current market, if so where would be a good place for the long term? Or do you honestly think that holding your cash and waiting for a decrease in current house prices will occur?

All opinions will be greatly appreciated.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.