This is an excerpt from MSD's report, Household Incomes in New Zealand: trends in indicators of inequality and hardship 1982 to 2016, written by Bryan Perry:

High housing costs relative to income are often associated with financial stress for low- to middle-income households. Low-income households especially can be left with insufficient income to meet other basic needs such as food, clothing, transport, medical care and education for household members.

Housing affordability can be measured in a number of different ways. From the perspective of potential homeowners the simplest measure is the ratio of average house price to annual household disposable income, which in effect gives the number of years needed to cover the purchase price of a house (on average). Other more sophisticated measures incorporate the cost of financing as well (eg Massey University’s Home Affordability Index).

The recently released Housing Affordability Measure from the Ministry of Building Innovation and Employment uses a mix of administrative and survey data and covers both renters and aspiring first home buyers. It is based on the notion of ‘residual income’ for households, very similar to this report’s income after deducting housing costs (AHC) measures.

This section on housing costs and housing affordability uses a measure which is relevant to both homeowners and renters, and takes the perspective of households already in the own homes or renting. The ratio used is that of gross (unequivalised) housing costs to (unequivalised) household disposable income, in much the same way that home-loan lenders do for assessing risk.

The figures and trends in the summaries that follow are national average figures. There are regional differences that a relatively small sample survey like the HES cannot pick up (see, for example, pp73ff in Johnson (2015) for regional differences).

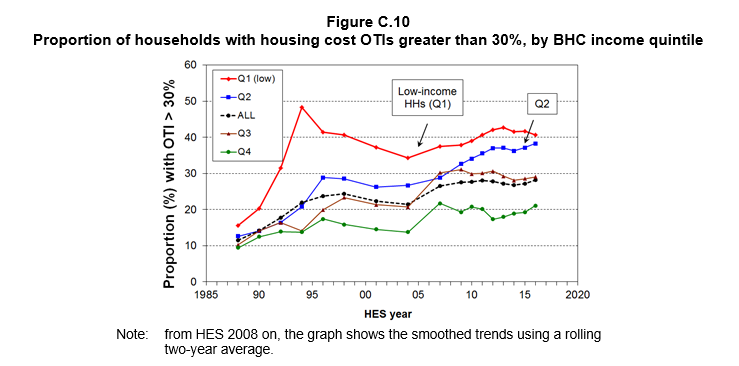

Figure C.10 and Table C.3 show the trends by income quintiles for households with high “outgoing-to-income ratios” (OTIs), using 30% as the benchmark for high OTIs.

In 2015 and 2016, 29% of households had high housing OTIs (>30%), compared with one in five in the early 1990s, and one in ten in the late 1980s. These are national average figures, and there are variations regionally.

For the bottom income quintile, the proportion with high OTIs steadily reduced from 48% in 1994 to 34% in 2004, as unemployment fell, employment and income rose, and income-related rental policies were introduced in 2000 for those in HNZC houses. It then rose steadily from 2004 to a 41-43% plateau for 2011-2016.

For households in the second quintile there was a strong rise from the 1980s through to the mid 1990s, followed by a relatively flat trend to 2004. From 2004 to 2011 there was a strong rise from 27% to 36%. The rate of increase has slowed since with the rolling two year average rate was much the same from 2012 to 2016 (37-38%).

The rise for the third quintile from just over 20% in the late 1990s and early 2000s to a new plateau of around 30% from 2007 to 2016 is also noteworthy.

From 2007 to 2016, around 15% of households had an OTI greater than 40% - up from 5% in the late 1980s (see Figure C.11 below).

For those in Q1 (lower quintile), the proportion with these higher OTIs peaked in the late 1990s at 34%, declined to 25% in 2004, then rose again to be close to the 1994 rate in 2011 (33%) and is similar in 2016. The proportion in the second quintile rose from 15% in 2001 to just over 20% in 2011 to 2016.

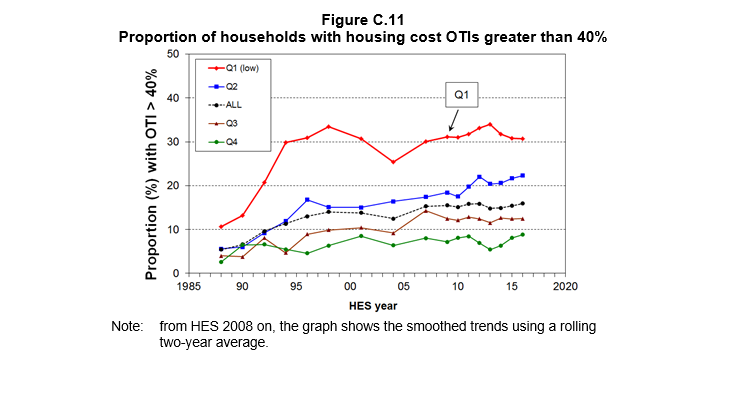

From HES 2011 to HES 2016, around one in four Q1 households reported spending more than half their income on accommodation (Figure C.12). This is similar to what it was briefly in the mid 1990s, but is otherwise historically high.

- those living in HNZC houses and receiving an income related rent subsidy such that their housing costs are less than 25% of income

- older New Zealanders receiving NZS, many of whom have low housing costs through their mortgage-free homes

- low-income working and beneficiary households in private rental accommodation, many of whom receive the AS.

NZS has been rising in real terms in recent years which in part explains the apparent flattening of the OTI lines as it acts as a counter to the rising trend for low-income working-age renters.

OTI trends by household type

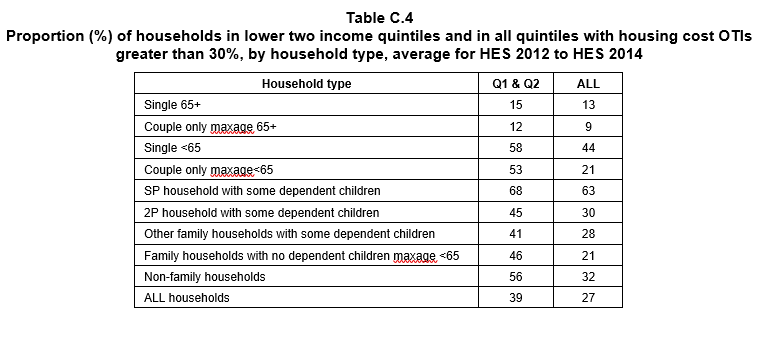

Table C.4 provides a breakdown by household type. The analysis uses the “30-40 rule” that is common in Australia and elsewhere – that is, it looks at the those in the lower two quintiles (40%) who have OTIs greater than 30%.

Sole parent households have the highest housing stress on this measure. As most sole parent households are at the lower end of the income distribution it makes little difference as to whether all sole parent households are considered (rate is 63%) or just those in the lower two quintiles (rate is 68%). Taking only the lower two quintiles only does however have an impact on the relativities between household types compared with taking all households into account. For example, using the 30-40 rule, all working-age households except for sole parent households have much higher reported housing stress.

Around one third of sole parent families live in larger households with other adults. The sole parent household figures in Table C.4 do not therefore fully represent the situation for all sole parent families, a good portion of whom are captured in the “Other family households with some dependent children” row.

OTI trends using the individual rather than the benefit unit or household as the unit of analysis

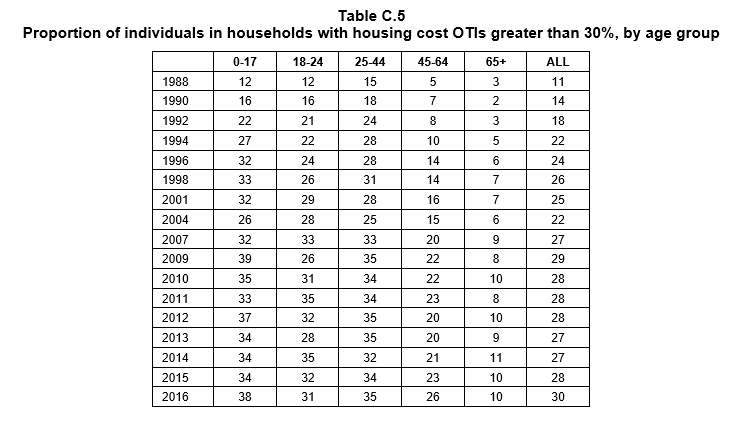

Figures C.9 to C.11 above use the household as the analysis unit. For some purposes, such as examining the different levels of housing stress by age, analysis needs to be done using individuals rather than households. Table C.5 provides a breakdown by age group. The proportions with high OTIs in 2016 (or even 2015 and 2016 on average) are much higher than in the late 1980s for all age groups (doubling or even tripling for some), although still remaining relatively low on average for older New Zealanders.

Long-run trends are very similar whichever unit of analysis is used (compare, for example, the “ALL” columns in Tables C.3 and C.4). There can however be some divergence from survey to survey especially for sub-groups, mainly because the bottom quintile (20%) of households has only around 17% of the total population in it, reflecting in particular the high proportion of small households in decile 2 (the top half of the bottom quintile). As a consequence of this difference, the second quintile of households does not perfectly coincide with the second quintile of individuals.

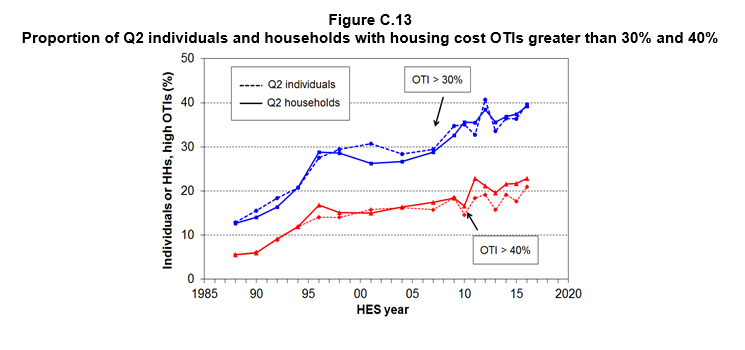

Figure C.13 compares the trends for second quintile individuals and second quintile households and shows that despite the wobbles and divergences that are evident at times from survey to survey, the overall trends are much the same.

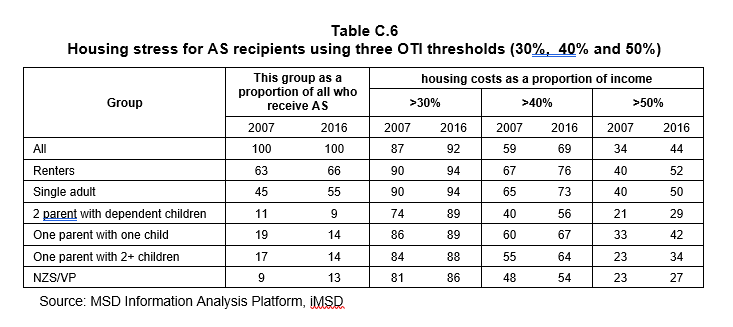

OTIs for those receiving the Accommodation Supplement (AS) – information from administrative data

- In February 2016, 44% of AS recipients were receiving the maximum payment, up from 25% in February 2007.

Table C.6 shows the proportions of AS households that have high OTIs – those that are spending more than 30%, 40% and even 50% of their income on accommodation:

- In June 2016, almost all renters receiving the AS spent more than 30% of their income on housing costs (94%), three in four (76%) spent more than 40% and half (52%) spent more than 50%.

- These figures were all up on what they were in June 2007 (90%, 67%, 40% respectively).

- 55% of those who receive the AS are single adults – their figures are close to those for renters noted above.

The provisions in the 2017 Budget package (higher incomes across most low to middle income households and higher AS rates and area changes) can be expected to improve these figures for the 2020 Incomes Report.

Housing costs now a much larger component in the household budget

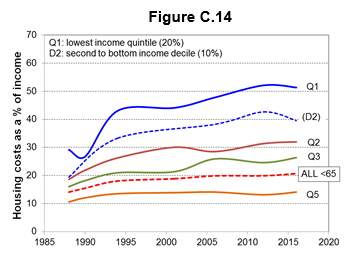

All the above analysis is a reflection of the fact that housing costs these days make up a much greater proportion of the household budget than they used to. Figure C.14 shows the trends in the average housing costs as a proportion of average income for each quintile of households (under 65s):

-

up from 14% in the late 1980s to 21% on average in 2015 and 2016 for under 65s[1]

- up from 29% to 51% on average for the bottom quintile, and 19% to 32% for Q2.

_______________________

[1] Statistics New Zealand reports that housing costs took up 17% of household income on average in the 2016 HES. The difference in the numbers occurs because (i) Statistics New Zealand uses gross (before tax ) income whereas the Incomes Report uses after-tax income, and (ii) the Statistics New Zealand figure is for all ages, rather than the under 65s as above.

9 Comments

Is anybody surprised at this report?

Hello tothepoint no I am not surprised at all. I feel like I don't have a life anymore with most of my income both from my day job and my rents spent on house maintenance. I don't know how long I can keep going like this anymore but I must grit my teeth!

Chin up old boy. You'll probably be able to capture some capital gains after the ten years or so. :)

no, there is a strong correlation between the prices of houses and the expenses required to run them.

the disappointing part is a lot of those funds flow offshore so are no benefit to the local consumer economy.

and when interest rates rise that will suck even more out

You're a wise and tenacious man, DGZ.

Struggle on, my friend. I look forward to shouting you a pork chop and a pint one day soon - perhaps at an establishment near your most salubrious neighbourhood.

A bowl of OTI s and a glass of fresh squeezed citrus will ensure that your out-goings exceed your inputs. :)

Everybody knows that the dice are loaded

Everybody rolls with their fingers crossed

The poor stay poor, the rich get rich

That's how it goes

Everybody knowsEverybody knows that the boat is leaking

Everybody knows that the captain lied

Everybody got this broken feeling

Like their father or their dog just died

Everybody talking to their pockets

Everybody wants a box of chocolates

And a long-stem rose

Everybody knowsAnd everybody knows that the Plague is coming

Everybody knows that it's moving fast

And everybody knows that you're in trouble

Everybody knows, everybody knows

That's how it goes

Everybody knows

(Leonard Cohen, 1988)

These graphs represent the greatest failure of the current government. If they had just protected the averageman's ability to put his own roof over his head vs supporting foreign and domestic speculation, they would sail in for the fabled fourth term unopposed.

And key wouldn't have had to leave but did knowing of the up and coming embarrassment around the corner

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.