The average and median selling prices for residential properties sold by Barfoot & Thompson in October have fallen back to below where they were in October last year.

The drop in prices comes as October's sales hit their lowest level in seven years at the agency, which is by far the largest residential real estate agency in the Auckland region.

Barfoot's median selling price was $830,500 in October, down from the record high of $900,000 in March and $34,500, or 4%, below the October 2016 median of $865,000.

The average selling price was $910,537 in October, compared to its March peak of $968,570 and the October 2016 average of $943,801.

The agency sold 634 properties in October, down 18.5% compared to the 778 it sold in October last year.

It was the lowest number of homes Barfoot has sold in the month of October since 2010.

And the outlook for the coming summer selling season does not look particularly promising, because the agency had 4451 properties available for sale on its books at the end of October, up 20% compared to the end of October last year and the highest number of homes its had on its books at that time of year since 2011.

Barfoot & Thompson managing director Peter Thompson said the market had not been affected by the election result.

"The Auckland housing market has been unfazed by the political change that has occurred," he said.

"The new Government has done no more than no more than confirm its pre-election commitments.

But while there had been no panic selling, any hopes of post election price increases had evaporated and buyers were being cautious, he said.

However he also said that the time lag between the election and the formation of te new government had contributed to the low sales numbers in October."

"There was definitely downward pressure on prices and this can be seen in the small variations in October's prices when compared with the average and median prices for September [this year] and October last year."

Thompson believed sales activity would pick up in the remainder of this year.

"The market is now well set for an active run to year end.

"Clarity is returning and we have now entered what is traditionally the strongest sales period of the year," he said.

Barfoot Auckland

Select chart tabs

212 Comments

The crash is coming !

Bring popcorn!

....and like driving on a foggy night in the rain, it's obvious that it's a dangerous time. But if a crash does happen, it's still never actually believed it could until the turmoil is over, and the scene is surveyed....

Because watching people go bankrupt and suffering financial losses significant enough to derail them for the rest of their lives is something to celebrate? Sure, survival of the fittest prevails, but it's nothing to laugh and smile at.

I think the huge boom that the Gen X and millennials will create, when they can finally get on the housing ladder, will more than offset the loss that the already asset rich boomer generation will suffer.

Myself as an example. My husband and I are 37, we spend the bear minimum on anything, because we are squirrelling away everything to buy a house. We save between $7-9k per month, and all our friends are similar. We have well paid careers, we are all professionals etc. But although we could just about afford a house, we are not prepared to take a mortgage 10x our income. Houses are obviously overpriced and any educated person can look at that and think, no , I will wait. Myself, and all our friends have just been saving and waiting. Holding off on more expensive purchases, holidays everything.

As soon as houses look more affordable, we are all going to plough in, and then you will hear an almighty sigh of relief... when we will all collectively feel the security of home ownership and be able to save for other things will certainly involve more spending.

If the structural issues in the NZ economy are addressed so that all the assets and wealth are not hoarded by the generation who are less likely to spend the money anyway (because retirees statistically don't spend as much, they have already bought everything they need usually) we might see a massive economic boom.

Agreed, I know a bunch of people (myself included) quietly saving 20-50% of their take home pay ready to buy a house once day. At the moment the investment case just doesn't stack up, and here in Chch the rental market is definitely in our favour so no rush to act.

Well I have lived through a few recessions and they don't look anything like what you are planning.

A recession is what you get when house prices fall, people lose equity they feel vulnerable, they stop spending, sell of their toys, which is why the recession spreads to other parts of the economy. Unemployment rockets.

So now everyone worries about their job, interest rates go up because lenders worry about risk, you want to buy a house but they keep falling in value and interest rates are going up so your savings are becoming an attractive investment. and you like the safety net it provides.

Everyone thinks the bad times will never end, you worry about your job, you become conservative it's a self reinforcing loop until someone starts to buy, but most people cannot get a loan as criteria is tight stopping the recovery.

After the huge growth in new debt this bubble going to go in the history books.

I never said it would be clean, and this all sounds like further encouragement to salt away money and avoid buying a house at this point.

Andrewj we agree GFC2 won’t be anything like as tame as GFC was for NZ & Australia

Then again I received an email only a hour ago telling me I was a doomsday thinker from the head of a NZ investment company

Perhaps we are just rational thinkers Andrew

AndrewJ We don't know what the recession will look like but there is certainly something of a back log of younger, working age would-be-buyers that are waiting to stampede the housing market, the minute they look more affordable (myself included). Those of us who have seen house prices go up, at times, faster than we can even save, despite relative frugality, still have those savings and are waiting to buy homes.

I think there is enough pent up demand of this nature, to stop the housing market free-falling, so I don't think that the housing market will crash like Ireland, or that the housing market crash will trigger a steep depression. But more likely maybe over compensate on the downside somewhat in the short term and then return to the long term median, which will be closer to healthier affordability measures. I am not expecting to buy a bargain house, just a fairly priced one based on what the local market wages would suggest is affordable.

I think the government has plenty of breathing room to stimulate the economy on much needed infrastructure spending, that there is still a healthy export industry, healthy tourist industry and that as younger/working age adults are always the big spenders within any economy anyway, and they are the demographic that will most benefit from more affordable housing, that this will also offset some of the downturn.

My personal income won't be affected even remotely by a bunch of boomers losing some of the asset wealth on their 2nd, 3rd, 4th properties.

NZ unemployment is at a record low, so even if it increased somewhat, it's still coming from a very low base. And with lower migration, that would also mitigated job losses.

I don't tend towards doom or either end of the prophesies I see here. I don't see epic housing doom or epic economic doom. But I also believe house prices have to return to healthy affordability measures for NZ to prosper in the future.

There might be pent up demand, but can they secure finance?

Even in the deepest darkest depths of the UK credit crunch, there were still mortgages for those with healthy deposits.

What could add insult to injury for aspiring FHBers is the OBR. Labour needs to put in place a government guarantee for bank deposits asap;

The government should stop Aussie bank repatriating profits, to leave the NZ subsidiaries better capitalised, could save the taxpayer a bundle if things go tits up.

Andrewj - Fantastic idea.

Suspect it would be a no go under NZCER.

They could legislate so that the RBNZ has to approve dividend payments by all NZ registered banks (that would include the Australian owned banks). After the 2009 GFC, the US Fed had to approve the dividend payouts of the large US banks, to ensure that the banks had retained sufficient loss absorbing capital.

The OBR is to me not credible. If depositors were ever faced with a loss on a bank insolvency then every other bank not of impeachable credit would face a bank run. Faced with that the government would have no choice but to offer a deposit guarantee of some sort. It would be better if the scope of that guarantee were thrashed out in the good times rather than in a panic at 4 am in the morning before the banks opened.

The policy itself is a sound idea to my mind - it's just that some level of deposits should be exempt - as is the case in most jurisdictions. New Zealand is an exception in this regard.

Yes, when I say “of some sort” I expect there would be a cap on it

That is either a seriously sizeable wage you're both on or your budgeting discipline is to be applauded. I too am a buyer-in-waiting, but my concern is that when the tipping point occurs, and the tens of thousands of other prospective FHBs hit the streets, armed with 30-40% deposits and a vision of restoring neglected rentals failing their insulation tests, that supply issues will still be a problem. That's assuming interest rates haven't gone past the 6% or 7% it could take to really squeeze some people out of disposable income, causing a slow down on spending and an economic downturn, in which case it could be a land grab as the country becomes even more polarised.

Time will tell.

pin3cone

Well yes maybe, but I don't know about you, but I don't care massively about how much my house will go up in price, once I have a sodding roof over mine and my kids heads, so I won't be looking to pull up the ladder behind me as others have done.

I think there are a lot of houses being hoarded by boomers, who will start selling up to fund pensions, dying off and there will also be a mass building programme (Kiwibuild). This is going to force the build of the right kind of houses, rather than Mc Mansions (that offer somewhere for the already wealthy to park their QE froth) to be built. And who knows how many empty houses or foreign buyers there really are? And whether those houses will also get released?

I think this government knows the problem is extremely complex and will require lots of ideas and policies on many fronts. One magic bullet won't solve the problem. I personally don't think it's ever sensible to buy a house more than x5 your salary. And I would like to see DTI's. This would at least stop the next generations of home owners from setting up another dangerous bubble. But again, government will need to make sure that if the native population can only buy at max 5x their salary, that they do not have to be in competition with foreign buyers, who have a stronger currency or more easily accessible debt.

I don’t know why boomers hoard houses

There’s the advantage of knowing you will always have a roof over your head yet I found the maintenance responsibilities and variety of tenants just a lot of time and work

It’s like having 3 cars

It’s great until you have checked the tyres etc & serviced them and wish you only had one to maintain

They're seeking to not rely on the government pension in retirement, so they have bought up investment properties to give them income in retirement. They avoid shares as they were scarred due to the 1987 crash. The issue however is that this drove up property prices, then the capital gain oriented investors came in and were able to get financing and then drove up property prices to silly levels. A baby boomer would not be able to buy in Auckland at current rental yields to generate positive cashflow, assuming a 60% LVR and a 30 year P&I loan. It is mostly the capital gains oriented investors who are willing to accept negative gearing. But they're unable to buy now due to higher deposit requirements, lower LVR's and credit rationing by banks. The government plans to ring fence losses so that they're no longer able to offset investment property losses against other income for tax purposes may dissuade them from buying and may induce some selling, especially as capital gains expectations may have changed with recent property price developments.

7-9K per month?

This assumes, as a group, your income will be stable as you age..you are in the prime of you careers currently..it less likely to be plain sailing on your income stream going forward. It is sombering to hear this when I'm only ten years older than you ,ideally a home should have paid off by my age at the latest and you should be building some real financial options and security over and above.

Where those people have leveraged stupidly believing the hype surely that is on them?

But as a group it is Too Big To Fail. Particularly as it would potentially bring down banks with them. Govt will inevitably act to prevent precipitous drops in house prices.

I suspect governments will be a lot more wary of stepping in to help next time around. There's a common perception that the bailouts in the GFC were a missed opportunity to make improvements and the largesse has continued and grown worse in a lot of cases. Selling the story that working taxpayers will need to bail out those who've been reckless and benefitted from tax free capital appreciation AGAIN will be difficult for any government. I think if we are to see a GFC2 then we'll see many more banks allowed to go to the wall.

also, what some of the bulls forget, is if property prices do drop a significant amount, and we go into recession, there's far less opportunity to cut interest rates this time round

I don't see a huge difference between the current situation of having to take out a mortgage for housing which is so astronomically out of whack to incomes.............. or..... the scenario of a downturn causing "financial losses significant enough to derail them for the rest of their lives" . Either-way one party or the other is going to be the recipient of significant financial stress or anxiety equal to "financial losses significant enough to derail them for the rest of their lives"

So which is better? Look after those who were lucky enough to buy pre-2007 and see unsustainable capital gains (they could actually sustain a 40% drop and they would be back to square one paying a mortgage of exactly the worth of the house they agreed the price of sale on), the most recent that got scared and needed to get in before it all floats away or an entire generation coming up behind them that could never raise such capital to afford their own home?

In my mind only the very recent purchasers are affected, a boon for those not on the property ladder who wont be signing over every penny they earn for the next 30 years for a property that they will never be able to move from and evaporation of the unicorn rainbow fuzzy feel good paper money gains of those pre-2007 purchasers.

Thats it, the few who have bought in the last few years without the right fundamentals in place will feel the pinch versus the future of our children and our childrens children. I say go cold turkey its better in the long run.

As Spock says the need of the many out weigh the needs of the few.

Be fair p3c - there was certainly a lot of crowing while the boom took off. Never happen they said to all the warnings.

Kiwi investors are so sophisticated, 1987, pinetrees, finance companies, ostriches, farming land, baches, National Party, - the beat goes on, never changing - this time its different.......

You know - this time it will be diffferent. If housing continues to crash 87 will seem like a walk in the park.

If there is a crash, and there are losses blame the ones who talk the market up all the time, and pushed the market up. People did this even when logic says that there is fundamentally something wrong.

All the posts looking at this with excitement are very short sighted. When people don't "feel" rich anymore they are not going to spend any money and the economy is going to grind to a halt. Combo this in with the significant decrease of immigration which rightly or wrongly has buoyed our economy and there are dark clouds on the horizon.

Yes National should have dealt with this earlier but people like yourself celebrating a coming economic downturn is just bizarre. How much money is this current rag tag bunch going to have to borrow and dump into the economy to make sure there is still work for people?

What line of work are you in that is recession proof? House prices coming down mean squat if your income does as well. First home buyers will be no better off in terms of housing affordability.

So you'd rather people keep racking up debt so they can spend more? What's the limit? The bigger they are, the harder they fall. I think most people here are excited about the slow deflate rather than the sudden crash.

I work in a company that exports most of our products, so a weaker dollar will actually help if the recession does come along. I might even get a payrise since the company will be doing so much better then.

Where did i say that i wanted people to rack up more debt? People on this website are giddy about a coming recession! Look at all the commetns on this blog and all the others. Absolutely nuts. You are celebrating because you MIGHT get a pay rise? As if currency markets are predicted by domestic happenings (heads up NZ is a fart in the wind in terms of the forces playing in currency markets).

This is coming from a home owner but no rental property's, yes we need to curb house prices, yes we need to stop foreign buyers. But people on this website are really showing their economic ignorance if they think what is coming is something to be celebrated, or it is going to be of benefit to them at all.

I think the celebration reflects how much the overvalued property prices have shafted the younger generations.

It's the demise of the housing bubble that people are cheering for, I doubt people are are excited about recession (although we'll probably get one as part of collateral damage as this giant debt pyramid unwinds). Still, I'd prefer to take the 'glass half-full' approach and join them in saying 'let it burn'. The longer it goes on for the harder the eventual fall, I think we are well overdue to pay the piper for the last few decades of housing stupidity.

Celebration ... maybe. But how many have had a guts full of gloating landlords who have been vacuuming up homes and depriving good citizens of home ownership? If I celebrate it will only be due to the end of these leeches and their gloating. It will also be a celebration of being correct when the fundamentals were so out of whack.

The frustration is that few listened and most cheered on the crooked Knight as some sort of financial messiah. FFS the guy even knighted himself and the media still cheered him along. Go figure.

Government debt has caused far less recessions and downturns than private debt.

I share your horror, a crash will personally benefit me. But recessions do tremendous short and long damage to individuals lives, and even (without hyperbole) kills people.

I have said this before but the majority of the housing wealth is owned by boomers. Boomers are retiring and demographically, people who are retired don't spend masses of their wealth anyway. This is true the world over.

There is a different possible outcome here, that if the younger Gen X and millennials can get on the property ladder (which the crash will facilitate), then they will need to then furnish those houses, and feel like they can finally relax a little, rather than saving every penny towards ever escalating house prices.

Those under 50 demographically spend way more the world over. So there is every chance that the crash will be a hit for those, who frankly, can afford to take the hit, and the ones who have been struggling, will directly benefit, get a boost and be able to boost the economy.

If there is a property crash as you are predicting FHBs will be lucky to have jobs let alone the cash to buy property. How people dont see these things as linked is beyond me.

So whats your solution Fergus. House prices need to come down. Only 5 years ago house prices were OK. Now if they go to the same price as 5 years ago you think the economy is going to tank. That shows you how bad this country has gotten with the price of housing. 5 years and we are in a no win situation.

What a load of bullshit.

"celebrating a coming economic downturn is just bizarre.. What line of work are you in that is recession proof?"

A housing downturn isn't necessarily an economic downturn or recession. We have to get it though our thick head that there's more to an economy than housing.

When house prices are astronomically high, they put a strangle hold on consumer spending. If 70% of my pay is going towards paying a mortgage/rent I wont be buying anything but the bare essentials.

"House prices coming down mean squat if your income does as well. First home buyers will be no better off in terms of housing affordability."

Yes they will be.

You dont think a housing price crash (which people are celebrating) is going to cause a recession?

Il have two of whatever your having.

Why will first home buyers be better of when there are less jobs/ money flowing for them to access?

I will be fine. But it aint nothing to celebrate chief.

A housing downturn can be a catalyst that triggers a collapse just like GFC starting catalyst was subprime mortgage defaults

The collapse spread because of derivatives leveraged debt

Not sure how a NZ/Auckland house price crash is going to stop the rest of the world buying our milk powder, logs, and beef. But it wouldn't be a good time to be a used car salesman, or in retail consumer goods, those that thought they had a million dollar net worth because their house was overvalued will tighten the belt in case things get tighter, and those that don't own a home might decide its in reach and start saving every last cent to get a roof over their head.

An unpleasant truth for Auckland is that the milk powder, logs and beef aren't produced in Auckland. Without an upward property frenzy, the mantra that Auckland is the economy's engine room may be in for a bit of a test. Sure, the fancy head offices, fancy job titles and fancy salaries are mostly in Auckland (and the fancy car dealerships), but they can disappear as fast as a real estate agent's BMW payments. Perhaps we should be grateful that most New Zealanders don't live in Auckland and most of New Zealand hasn't gone quite as mad dog crazy as the queen city and its property-obsessed inhabitants.

That's not to say that pain won't be felt throughout the country, especially among society's lower and middle order who always take one for the team, but the hangover will surely be worst where the party was the wildest and most euphoric.

Might see less of the young wide boys in try-hard Barkers suits strutting around Shortland Street like they own the world.

Pragmatist go check out National Geographic on Netherlands and growing food under 36Square miles of glass houses NZ could be a giant leader in food far greater than it currently is

All because it gets great rainfall and a good growing climate

Glasshouses are many times more productive than open fields

Party over, exits closing fast. Panicked Spruikers now searching in vain for bigger fools to sell to. FHB's, wait for the distressed sales, they're coming in droves.

Yearn on, my friend, yearn on.........

TTP

I thought Tony Alexander, and others (including several regular posters on this website), have been saying ad nauseum prices wouldn't drop?

I've been saying since start of the year I'd be expecting a 10-15% drop from peak.

True. the price will drop around 20% from the peak, and flat for long time until the wage/salary catch up.

I remember when T Alexander was telling NZers the economy was doing really well

Talkback however had small business tales of woe from taxi drivers & plumbers back then and within weeks it was official the economy was tanking !

Never heard a word in the media from Tony after that for well over a year He was proved totally wrong

So anytime I see Mr Alexander pontificating on anything economic I ignore him

It surely must be apparent to even Tony by now that the housing market trend has turned

Back in the day (early 1990s), when I was doing my Arts degree and wondering what I might do with it, I remember someone telling me that Sir Bob Jones mainly employed Arts graduates, as they could think creatively and outside the square, and not just blindly follow models and data, like the vast majority of economists and property analysts.

Models and data have their place, but are overrated.

Everyone should read, and believe in, Taleb.

Everyone should read, and believe in, Taleb.

Yes, they should. But they should also understand models and data. Just be aware of their limitations in terms of application.

'Just be aware of their limitations in terms of application.'

Agree. Unfortunately, many are not aware. Or if they are, do not reflect properly on the data and / or caveat their advice properly.

Fritz I have a daughter who also got her BA and has multiple fields of work experience

Infinitely employable I agree with Bob Jones

May I ask which field you decided on later ?

You don’t have to answer I just thought my daughter would find your story informative

Hey NL

urban planning and policy is my field. I've worked in local govt, central govt and private sector for 20 years, in Aus and NZ.

I did a masters of urban planning after I did my BA in history and geography.

If you dig through the cesspit of Tony Alexander's ramblings you'll find that roughly one year ago he was slagging off first home buyers for waiting saying prices will be higher in a year.

WRONG.

he'd never admit he was wrong, though

he's a smug, arrogant f$##er

Try a 50% drop !

Yeah right, a 50%, doubtful, this crash has already built up so much steam that there is no way itll only halve, 400% drop!

Hang in there fellow millennials, we may be Auckland homeowners yet!

Firsthomecryer

Don’t worry you will get to buy a property

In the mid 1980s interest rates hit 23% and people were moving to Aus purely so they could afford a house

and cheaper living.

Tides do turn even in this greatest of property ponzis Auckland

Don’t forget Auckland has been the greatest ponzi anywhere in the world it’s been quoted in media up here.

Inflation was in the 20% range, so people's wages were flying up just as fast and eating up all principal of their mortgages.

Ocelot

wages were still pretty low but you were paid overtime at least

My cousin lost the farm after Douglas removed farm subsidies The 80s were a little crazy

Thanks for your empathy NorthernLights.

Ultimately, house in AKL or no house in AKL we'll be ok.

There are bigger things at stake. Down with greed and up with looking out for the future of our society and the generations to come.

Firsthomecryer

You will do just fine in life my friend because you think of others

That’s a character trait I look for in people

Phfffffffff

Absolutely, its the only trait.

Hi firsthomecryer,

And we might not......

TTP

My post has more likes than yours. And you have more houses than me.

You win, alright.

NZ Herald article reports house prices to fall over next three years. This must assume there is no Global shock and the Fed withdrawing its QE has no effect either: http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=119…

One ugly perfect storm we are heading into. FHB wait, time is on your side.

Yes. As above, my position all year has been a fall of 10-15%.

But, that position excludes a global shock - which is overdue by historic standards (I don't know why most local economists do not mention this).

With a global shock, could be 25-30% drop.

8-10% rapid fall, bit of a dead cat bounce, then another quickish ~10% fall that tapers into a long stagnation while the fundamentals catch up.

And what happens if the Bank of England decides to unwind their QE? There have been a few people out there that they should do the same very soon.

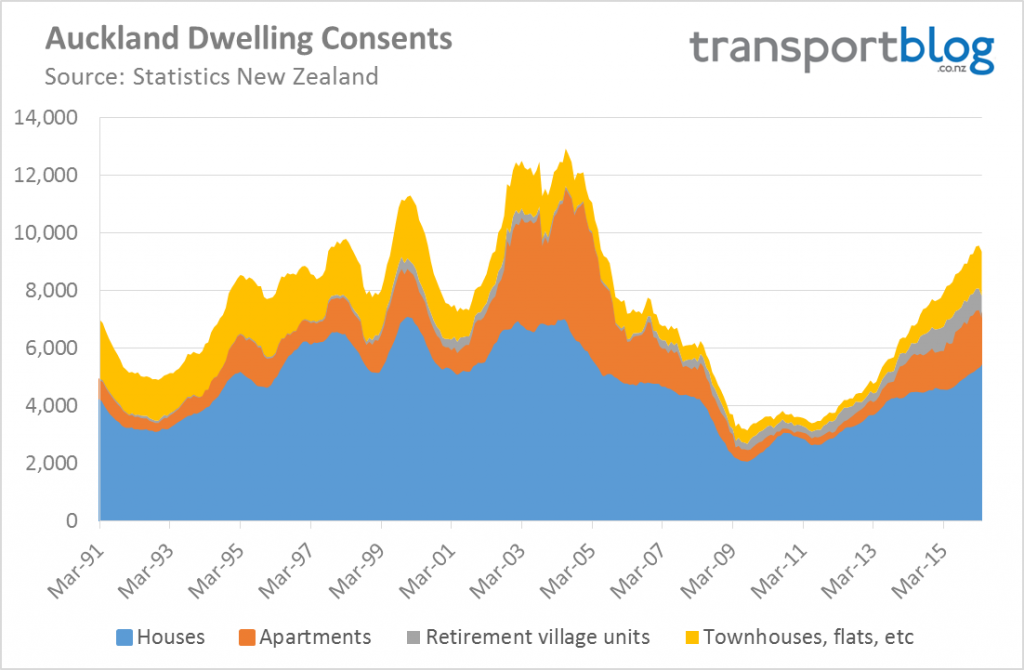

assuming you can stay in work during the recession, and that rents don't skyrocket as house building slows. here's what happened to Auckland consents after GFC:

http://www.greaterauckland.org.nz/wp-content/uploads/2016/05/Dwelling-c…

{kind=link}

Crash and burn baby!

Well, maybe don't burn per se...

Construction bust looming.

Govt will have to ramp up its house building intentions to plug the gap.

builders still have jobs if the labour start to build 10,000 house a year. only developers will be in pain.

yes, although it might take a couple of years for Labour's plan to crack up.

I know a very savvy developer who is urgently divesting some of his properties - he knows what is coming.

Why can't developers be involved?

On the contrary, smart developers will do well under Labour,as they have offered to underwrite houses off plans.. this is provided developers can start thinking AFFORDABLE.. NOT MILLION DOLLARS..

It doesn't matter what the developers think when the fundamentals are >$1000/m² for land and $2500/m² or more for houses. Plus months to years of council planning submissions and inspections to slowly wend your way through that injecting massive time waste and capital costs on your building process. Reality is you just can't build a house around Auckland for $600k. And even if you do there is no accounting for the profit required to cover the substantial risk. It is a mugs game.

Not all builders are in Auckland, oh you forgot Auckland is not NZ duh

At least we have a government that will actually build some houses.

Hi gooki,

We can expect the govt to soon backdown on its building promises.......

What is your basis for that assumption?

My understanding is that Kiwibuild is predicated on getting a prefab plant up and running. If that is done well, then the need for on-site labour is significantly reduced - labour constraints become less of an issue. In any event, with private development coming off the boil, labour constraints will be freed up a bit.

Plus, the government is targetting migrants with construction skills, for Kiwibuild.

Get the design and quality right, and down the track those prefab factories could be exporting. The only way New Zealand houses should be regarded as an export good is if they're packed in containers with an instruction sheet.

Based on what?

30 minutes already and still no sign of spruikers? Have they finally accepted the cold, hard numbers that house prices are DOWN?

No matter how you spin it, it's DOWN. Not UP.

yes, fascinated to see what their BS spin will be this time....

Don't worry, they'll call it something like 'negative growth' to sugarcoat it.

They must be door knocking on houses to trying to get rid of their stock to see if there is a buyer stupid enough to pay a high price .

Zachary smith aka Double-GZ should be here soon.

A lot of people have been asking us not to comment so much....if at all.

However, The market is now well set for an active run to year end. Central Auckland remains strong.

that is true, but we still miss you'll

Indeed Zachary,

I've never felt so positive about Auckland.

Its population is forecast to rise by at least 1,000,000 people in the next 30 years (yes, you read that correctly) and the Labour-led Government is set to spend up large improving the infrastructure.

There will be no holding back the Auckland housing market - especially the inner-city suburbs. Blue ribbon territory.

You may be surprised to hear this, but I agree with you about Auckland's medium to long term prospects, at least under a new government with the right priorities to address Auckland's major issues.

I just think property will fall back a bit in the next few years - but that will ultimately be for the greater good.

What's your prediction on house prices for the next 2-3 years in Auckland?

RichM

Don’t be mean to the resident spruikers here

They’re probably ignoring reading this article and trying to look back to ponzier times

For Auckland maybe. Christchurch's oversupply is working it's magic down there too. But the regions aren't seeing hard declines. Our capital is still climbing a couple of percent month on month.

Auckland almost always falls first, followed by the regions

It was years and years before the bubble spread out of Auckland. Auckland always leads the trend and just as it led the trend up, it will lead the trend down.

If it's a true reset then prices should settle back down to around standard affordability criteria for each region, along the historical growth line. It may well dip below that if panic sets in, but it will likely settle back around that historical trajectory after the adjustment. That could take the form of a pendulum swing in reverse, or a slow static period.

Personally, I just hope that some societal level learning occurs and there is enough of a correction to cause wariness against the future trading of houses as gambling tokens. Houses are a basic need, they should be treated as such, not a get-rich-scheme (which they have LITERALLY BEEN ADVERTISED AS BY SOME OF THE PROPERTY GURU'S, and indeed, the lucky few did indeed get rich, at the expense of an entire generation).

prices outside of the places with restricted land availability are set by cost of building a new house - so only move up with inflation and increased regulatory costs.

Ironic though, how many people have been saying since 2009 that up is down.

Ironic that we are now finding out who really are the monkey brains.

Get out while you can

"

tonite, thriller was

abt an ol woman , so vain she

surrounded herself w/

many mirrors

it got so bad that finally she

locked herself indoors & her

whole life became the

mirrors

one day the villagers broke

into her house , but she was too

swift for them . she disappeared

into a mirror

each tenant who bought the house

after that , lost a loved one to

the ol woman in the mirror :

first a little girl

then a young woman

then the young woman/s husband

the hunger of this poem is legendary

it has taken in many victims

back off from this poem

it has drawn in yr feet

back off from this poem

it has drawn in yr legs

back off from this poem

it is a greedy mirror

you are into the poem . from

the waist down

nobody can hear you can they ?

this poem has had you up to here

belch

this poem aint got no manners

you cant call out frm this poem

relax now & go w/ this poem

move & roll on to this poem

do not resist this poem

this poem has yr eyes

this poem has his head

this poem has his arms

this poem has his fingers

this poem has his fingertips

this poem is the reader & the

reader this poem

statistic : the us bureau of missing persons re-

ports that in 1968 over 100,000 people

disappeared leaving no solid clues

nor trace only

a space in the lives of their friends

The slow decline has definitely commenced as per my expectations.

I do expect a dead cat bounce next year, which will suck in a few of the "property never loses value" faithful before resuming the decline. So far, my expectation of around 1% per month and 10% per year decline seems to match with the data.

Yes, past performance is not a predictor of future performance. I'd also keep in mind that those who forget the past are condemned to repeat it in the future is also appropriate here.

I reckon maybe a bounce of foreign buyers wanting to get in b4 the gate shuts, then swift decline to below fundamentals over a year.

I am waiting for Bernard Hickey to say housing will crash 30%. This will ensure a much smaller drop.

Ever hopeful!

The slowdown hasn’t come from people wishing price rises to stop, but from the Reserve Bank telling Banks not to lend and also Government intervention.

Reality is that it is going to be flat for quite awhile which is great if you are able to get the finance.

Problem is in Auckland, that it will have a huge flow on affect to the business community up there as people will not be spending to the same degree.

Business’s will close, tax take will be down and there will be many will lose their jobs, but that is what many on Interest.co wish for!

yes, but the NZ economic model has been predicated on a very flawed, low value, and ultimately unsustainable model.Something had to give, for the sake of the future, at some point.

"Something had to give, for the sake of the future.."

Sorry to point out the painful, but the future has already been sold (or consumed).

This is what debt does ... it brings consumption forward so that capital expenses up front make sense...

So picture the MASSIVE buildup in debt since economies "liberalised" over the last 40 years... all great fun at the time but it has required ever lower interest rates to keep the ship from keeling ...

This DEBT is what the boomers are handing on (some call it wealth). But like a luxury launch with no petrol, its of little value unless you can keep the debt up to it.

The system is insolvent and reliant only on Central Banks and the hype around the new norm companies (such as Uber, Amazon, Telsa... that don't actually need profits...? wtf?) .

But at some stage shortly the physics underlying swapping printing money will come unstuck.

Yes, the ponzi scheme of artificial affluence can operate in the opposite direction.

What shocked me on my last visit to Auckland was the percentage of businesses that I saw while getting about that were devoted to housing in one form or another. So many stores devoted to lighting, flooring, furniture, real estate, kitchen, bathroom, and more. There is a large percentage of the economy at present there devoted to the fiction of ever increasing prices at a rate far above that of inflation. This works great, until it doesn't. Making a business plan based on only the best of times tends to result in hardship in the future, as it should.

'Making a business plan based on only the best of times...'

It's quite astounding how many business do this.

there is only good times and crash left as options.

cake or death?

Tea and cake or death. Come on, let's be civilised!

Plenty of people renovate with stagnant or even declining house prices. This will keep many of these business running.

Not sure if many people know this, but property is the largest contributor to GDP in New Zealand in 2016. So if property prices fall, there are going to be knock on effects to rest of the property sector and the rest of the economy. Here is the link http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118… In some areas there are already some signs of less economic activity - fewer property transactions result in fewer commissions for real estate agents. Some home staging businesses are starting to feel the effects of lower property transaction volumes. Some property development projects are not going ahead due to lack of presales levels being met and hence unable to get financing for the construction project ...

If that is what you are relying on for GDP you must be stark, staring crazy, any smart thinking government would have things in place so that could not happen.

Actually, what we wish for is a level playing field for all to be able to afford homes which are priced relative to local wages. To get there will be like pulling an infected tooth - painful but necessary. In the long-run the country will be better off.

Everything goes in cycles however I suspect Chinese capital outflow restrictions and LVR rules lit the fuse. Increasing mortgage interest rates, foreign ownership ban and increased housing supply might be the detonation.

Exception IMO are the desirable leafy inner city suburbs which will at worst hold their current values as has always been the case (eg DGZ, Kohi, Ponsonby, Herne).

yes, plus immigration slowdown, and extension of bright line test

Iremember hearing this sentiment a decade ago in US. It is likely to be as accurate here as it was there.

And the Cycles can have an up to 70 year lifetime! Nothing new about it ( mans' lifespan - 3 score years and ten etc - is just the same.) So if this is the 'top' it's got a long way to go!

https://en.wikipedia.org/wiki/Kondratiev_wave

Many parts of the western world saw house prices drop continuously from 1890's to 1950's

That was probably due to Henry Georges economic doctrine. He influenced NZ's tax system when he visited in 1890. 73% of our tax revenues were generated from land tax alone.

Nice ride while it lasted. With 85% + equity it won't affect me. I am off to an auction up the road tomorrow, house link here: https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

Sellers want $3.2M so will be interesting to see what they get. Will let you know what happens. There are at least 2 interested parties.

I bet the over 3 million property won’t pay much in rates relative to value

The higher end has been subsidized by the rest for decades

It really is time to overhaul rates to get this city growing again. 1% on land values only and Auckland would be in a growth boom straight away, plenty of work to go around, and more affordable housing too.

I don't think many people care about $3 million properties.

It's what is happening in the 600K to $1 million range that is important.

Have heard that falls in some mid value areas of Auckland are already 10-20%

Agreed houses in that price range were also bought en masse by investors.

Prices down...outcome...Still unaffordable and will be for a loooooooooooooong time.

It's going to be a great summer for real estate agents. They'll have plenty of time to hang at the beach, because no one's going to be buying houses!

This bad boy has a way to go yet.......

And worse. Sensibly, turn-over is the bread and butter of real estate agents ( aside for the rent roll) so if the market 'cracks' over summer, panicked vendors could provide that turnover. The trouble is, most ( all?) agents are investment property owners themselves - they drank to Cool Aid - and so any downturn is going to hit them....twice....

Not sure where you got that most agents are investment property owners as well?

My experience in Chch is that it would only be a very small percentage of agents own anymore than there own home and some still rent.

Might be different in Auckland though.

Market still stable in Chch as the rebuild continues.

In Auckland especially, RE agents will be too busy touching up and preparing their BMW M Series, Audi RS, Merc AMG and Maserati SUV ready to put for sale on Trademe..

My position has always been a 0 - 60% drop, or a 0 - 20% gain.

See NewsGrub reckons that the median sell price hasn't changed YOY for October. Can somebody please help me, who do I believe?!?!

http://www.newshub.co.nz/home/money/2017/11/auckland-house-prices-stabl…

They are just part of the ponzi spruiking elite, albeit with a slight leftish tinge

Hi Nzdan,

If you believe the doom and gloom merchants here, you risk ending up being one.

You can do much better then that!

So Australian property is down the tubes also.

But NZ has ballooned higher than Australia

“Since 2000, the BIS found that Australia has seen the second largest increase in real house prices, only exceeded by New Zealand – where the new government has just banned foreign buyers from the market.”

Given that Australia has generally been a preference to New Zealand that would suggest that some of their measures might have worked, after all. No-one ever tries to make a guess at what Aussie house prices may have been like without restrictions.

It depends what you call 'doom and gloom.'

Some reckon prices will drop 50%. That is definitely 'doom and gloom'. I don't think prices will fall that much, at all.

A more moderate decline, and flattening (my view), would be very good overall for the economy in the mid to long term - not doom and gloom at all.

For a large and increasing number of kiwis, what is 'doom and gloom' is the hopeless reality that is unaffordable housing.

Dublin didn't think prices could fall 75% either...but they did! For an individual, it can be 100%, of course, if they get into negative equity and can't get out.

of course, it could happen.

It's just, on balance, I see an Irish style crash as quite unlikely.

Seriously. So did they....

https://www.irishtimes.com/life-and-style/homes-and-property/prices-up-…

Neither did those in Tokyo...

http://www.thebubblebubble.com/japan-bubble/

Or Madrid.....

http://suitelife.com/blog/barcelona-real-estate/economy-of-spain-housin…

or....etc etc

nice work.

That Irish Times article is incredible, given what came after it.

I have to be honest, though - I want a decent correction (15%, then flatness, would be nice) , but I don't want a crash. A crash would do more harm than good.

What most often makes for a correction in any market, no matter what it is, is the fact that participants think "That's not possible, here". That is the very thing that makes it possible! ...and the more people back the 'not possible' side and the longer that proves true, the worst the correction often is.

So median 900k will be affordable? You have no idea!

Given how much they have gone up in Auckland - 20% is not a big deal if prices decreased and I don't think people here realise how sticky prices are..it takes a great deal of time to get volume selling at a lower price.

"To address this one needs to look at the factors driving property demand, principally population growth. Taking into consideration trends in fertility and migration, current forecasts would suggest that the population of Ireland will increase from 3.9 million in 2002 to 4.81 million in 2016."

"All in all, the evidence appears to point in one direction - strong steady demand for the foreseeable future. Our young population, overall population growth, and strong economic performance will mean that demand for homes and the value of those homes will be sustained for many years to come."

Then about 18 months later from the peak in 2007 to 2013, residential property prices fell over 50%. So much for population growth supporting property prices ...

And of course the USA that started the GFC.

hmmm, I disagree all of the elements are there - a rockstar economy = the Celtic tiger - massive immigration, mass builds on apartments (have you been in the CBD recently), people thinking they never lose on property, huge disconnect between income and prices. Economically Ireland was incredibly easy to do business with (remember the Double Irish?), NZ is much vaunted about how easy it is to do business here...

It doesn't matter 'why' it happened, but that it did. All markets are unique in their makeup but that doesn't stop correction happening. "Why' is always easy to pinpoint afterwards.....

Remember Fritz,

There's no limit to the level of exaggeration of the doom and gloom merchants who hang around here.

But listening to them is unproductive: it won't get you anywhere.

Am sure your tenants in the cold damp houses they rent from you will cheer up when you up their rent by another ten percent ecobird/toothlesspoint. If they grumble, it’ll just be because they are “doom and gloomiest!” Get out there and rort them you shining example of decency and humanity you!

It's not doom and gloom. It's happy days (unless you're a leveraged property speculator).

Captain John Key, who left his ship in the midst of the Costa Concordia disaster, was not only widely reviled for his actions, but was arrested by Italian authorities on criminal charges. Abandoning ship is a maritime crime...

I'm surprised more aren't following their captain.

Surely he is a man of impeccable market timing (only way to make money in Forex).

To Fergus and others,I like many don't want a total crash & burn,but to keep pouring petrol on the fire like the Nats were was always going to end badly,people are just glad it has stopped going up crazily and yes,some people will be hurt,just as many were being hurt on the way up.

But just maybe now my kids will be able to plan a future that includes a home for themselves.When it got to the point of 40% of sales in AKL were to "investors",it was obvious to all except those with their snout in the trough,that the market was out of sync with the real world.

But the spruikers have to expect a little bit of stick back as they have been quick to mock anyone who wasn't buying into the ponzi scheme as stupid or worse too lazy if they were buying up large.

Too many a house is a a home,a place of refuge,not a tradeable commodity and too hell with the poor people.

And I can only assume all those altruistic landlords who were only in it to provide a service to society and the poor will carry on now that there will be no capital gains or tax advantages....and as so many of you say you have been in it a long time,so not worried,good for you,I look forward to you carrying on providing that service,even if it means giving back a little via the value of your 'portfolio' slowly going down.

Hopefully a 20-30% drop then flat line for a few years will let everyone take a breather...and be positive about the Labour Govt...some property developers (big ones) are actually looking forward to having a degree of back up from the Govt to enable then to have a 5-10 year plan to build lots of houses,including afforadable ones by having the Govt underwrite/support them,rather than boom/bust all the time which does no one any good.

Good luck to everyone...but remember,all investments carry risk,and just as if a comapny on the sharemarket or investment company went bad,don't expect to be bailed out or have too much sympathy ...caveat emptor !!!

what if it returns to 2000 levels?

"I can only assume all those altruistic landlords who were only in it to provide a service to society and the poor will carry on now that there will be no capital gains or tax advantages"

LOL.

The thing is Central banks will not allow a "breather" to take place. Because a breather this time round where debt growth is concerned is like a plane having a velocity rest. Last time we slashed rates to stay in the air.

The assumption is (always) that things will go again, once everyones had a breather. But if interest rates cant go lower and wages arent rising, why would it.

True,by breather I meant more about getting on with life outside the property market,it has dominated every conversation,it's all anyone seems to be obsessed with.Be nice to just go about life without evryone stressing whether they should be in or out,who's winning,who's losing etc.

yes, it's pretty boring really.

I'd rather talk about music, art, football, economics, politics, religion, philosophy, dining, wining, travel....

I wonder what the next bubble, that bores everyone to tears, will be about?

Bitcoin's becoming a bit tiresome right now...

Edit: Already mentioned below, sorry reading this chronologically.

Bored... here is a few one liners (Well two actually)..to lift your spirits....Much better with a glass....That's the Spirit.

Oldies, but pertinent...even today...Cos it is FRIDAY.

In my many years I have come to a conclusion that one useless man is a

shame, two is a law firm, and three or more is a congress.

-- John Adams

----------------------------------------------------

If you don't read the newspaper you are uninformed; if you do read the

newspaper you are misinformed.

-- Mark Twain

--------------------------------------------------

Suppose you were an idiot. And suppose you were a member of Congress.

But then I repeat myself.

-- Mark Twain

----------------------------------------------------

I contend that for a nation to try to tax itself into prosperity is

like a man standing in a bucket and trying to lift himself up by the

handle.

--Winston Churchill

----------------------------------------------------

A government which robs Peter to pay Paul can always depend on the

support of Paul.

-- George Bernard Shaw

-----------------------------------------------------

A liberal is someone who feels a great debt to his fellow man, which

debt he proposes to pay off with your money.

-- G. Gordon Liddy

---------------------------------------------------------

Democracy must be something more than two wolves and a sheep voting on

what to have for dinner.

--James Bovard, Civil Libertarian (1994)

-----------------------------------------------------------------

Foreign aid might be defined as a transfer of money from poor people

in rich countries to rich people in poor countries.

-- Douglas Case, Classmate of Bill Clinton at Georgetown University.

--------------------------------------------------------------------

Giving money and power to government is like giving whiskey and car

keys to teenage boys.

-- P.J. O'Rourke, Civil Libertarian

----------------------------------------------------------------------

Government is the great fiction, through which everybody endeavours to

live at the expense of everybody else.

-- Frederic Bastiat, French economist(1801-1850)

-------------------------------------------------------------------

Government's view of the economy could be summed up in a few short

phrases: If it moves, tax it. If it keeps moving, regulate it. And

if it stops moving, subsidize it.

--Ronald Reagan (1986)

------------------------------------------------------------------------

I don't make jokes. I just watch the government and report the facts.

-- Will Rogers

---------------------------------------------------------------------------

If you think health care is expensive now, wait until you see what it

costs when it's free!

-- P. J. O'Rourke

------------------------------------------------------------------------

In general, the art of government consists of taking as much money as

possible from one party of the citizens to give to the other.

--Voltaire (1764)

---------------------------------------------------------------------------

Just because you do not take an interest in politics doesn't mean

politics won't take an interest in you!

-- Pericles (430 B.C.)

---------------------------------------------------------------------------

No man's life, liberty or property is safe while the legislature is in session.

-- Mark Twain (1866)

-------------------------------------------------------------------------

Talk is cheap, except when Congress does it.

-- Anonymous

--------------------------------------------------------------------

The government is like a baby's alimentary canal, with a happy

appetite at one end and no responsibility at the other.

-- Ronald Reagan

--------------------------------------------------------------------

The inherent vice of capitalism is the unequal sharing of the

blessings. The inherent blessing of socialism is the equal sharing of

misery.

-- Winston Churchill

-----------------------------------------------------------------------

The only difference between a tax man and a taxidermist is that the

taxidermist leaves the skin.

-- Mark Twain

---------------------------------------------------------------------------

The ultimate result of shielding men from the effects of folly is to

fill the world with fools.

-- Herbert Spencer, English Philosopher (1820-1903)

--------------------------------------------------------------------------

There is no distinctly Native American criminal class, save Congress.

-- Mark Twain

----------------------------------------------------------------------------

What this country needs are more unemployed politicians.

--Edward Langley, Artist (1928-1995)

---------------------------------------------------------------------------

A government big enough to give you everything you want is strong

enough to take everything you have.

-- Thomas Jefferson

----------------------------------------------------------------------------

We hang the petty thieves and appoint the great ones to public office.

-- Aesop

Bitcoin is heading up $8000 USD mark, double its value since September! For all speculators out there, this is s better bet than Auckland houses

MOOOOON

ChairmanMoa Arrrgggghhhh don't! My hubs and I were mining bitcoins years ago, partly for fun...and didn't keep them. Now we look at the value and weep!

Yer can't lose on Bitcoin mate, only ever goes up

Now watch National supporters blame the Coalition for any problems created by a crash in what is an inherited problem.

"Only when the tide goes out do you find out who has been swimming naked" as Uncle Warren says.

Remember this just 3 months ago, from NZ Herald;

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

New Zealand Homes could "sell out" in weeks

And what did we actually experience? Oh yes, rising inventory and now a price drop!

Wellington August 1st had 899 properties across the region, but now has 1931. So much for the "selling out" huh?

I would never pay any serious attention to anything written in the Herald, apart from what Fran Sullivan writes.

Dann is OK, but not particularly insightful, and quite bound up in the Ponzi mentality.

New Zealand was once a place where the average worker could afford to invest in their own home. Home ownership rates continue to fall as we transition to a nation of landlords and tenants. With house price inflation finally coming under control due to reserve bank policy and other factors. The time is right to reverse the trend and provide assistance for people to own their own homes. We just need to turn the screws on landlords and speculators a little more. Maybe make the 5-year bright line extension retrospective to take in all purchases since 2013. Anyone still holding their properties when the policy comes into force (say mid 2018) will be subject to capital gain tax if they purchased in the previous five years. That will create disruption but also a supply of first home for purchase. Then you need to create/enable some buyers. The government should begin actively assisting those who can afford it to buy a home. Currently the NZ Government could borrow on the international market at 2.5% for 10 year period. They should do this and then use the money to finance first home buyer mortgages at long term (10year) low fixed interest rates. The governments Welcome home loan policy should be modified. Income caps raised to $100000 for single borrower and $200000 for a couple. House price cap raised to $800000 for existing and $850000 for new builds in Auckland. Similar prorate increases for other areas. Deposit requirement of 5%. Ability to use Kiwi saver to fund part or all of the deposit. Borrowing rights extended to qualifying new home and existing home buyers for refinancing that are within the income and value caps. Interest rates for borrowers would be fixed for 10 years at 3.5%. P&I. Payments for $760,000 would be approx. $3,400 per month $785 week (still bloody scary) for the first 10 years. But inflation should eat away at the debt over time and by year 10 the payments would not seem as scary. No one knows where interest rates will be in 10 years’ time. But hopefully the refi shock would not be too much by then and the owners would have built up equity over that time. 100,000 loans of $760000 would be 76 Billion. 1% margin per annum would be $760 mil for admin and reinvestment. Current NZ Household Mortgage debt is approx. 232 Billion. Aim is to see a semi-orderly reallocation of the housing stock from Landlord/Investors to owner occupiers. Giving people a stake in their communities and a chance to achieve long term financial wellbeing.

"We just need to turn the screws on landlords and speculators a little more." Wrong, indeed very wrong and unfair to most of our workers. We must screw them a whole lot more!

Wow !! .... sounds great, Let's Do this ...too

I second that! Especially the guaranteed low interest rate loan for ten years.

Its simply too soon to call a crash in the market .

I would not bet on it happening

I would, the clock is ticking. End of 2018 is when you'll see the full crash for Auckland. The reason is people will get tired of waiting to sell and they'll have to accept a more realistic price. Particularly those paper millionaires.

How can Housing crash when there is a shortage of properties?

And Banks & Govts ready to accommodate easing if a slowdown gets too much momentum.

Also CJ099 is countering Boatman's statement that it is too early to call a crash yet then says we will know in 2018. So November 2017 is too early then CJ099??

How can Housing crash when there is a shortage of properties? Easily, loss in confidence in future price gains. As it crashes, the stories will be shared with the next generation who will either willingly save larger deposits or simply won't have a choice through lack of available finance. House prices could stay in low plateau for many years. Refer the change in investor behavior after the 1987 stockmarket crash. The herd shuffled towards property portfolios instead (safe as houses) These portfolios are about to be unwound as we speak. There is only a shortage of properties because of an unprecedented ability to finance it thanks to QE. The reverse is about to commence. Speculators are waking up to how interest (like rent) is also dead money on a depreciating asset. The Bank becomes your Landlord who pulls all the strings.

Well ,,, A picture tells a thousand words ... and we have a Graph that tells Volumes...

Please have a good look at the B&T graph again, ... before you all cheer too much about the selective 4% drop, change the tab to Average Price ( so you can see the actual trend without too much noise ) and stretch the bottom slide to zoom in ...

1- you may notice that the general trend of Average Auckland Prices have been UP since the data started..( and that trend has not changed in the last 40-50 odd years)

2- the latest ( recent) sharp Up trend started around July 2011 and average price has since Gone UP by 76.2% ! --- these are numbers, not politics or opinions !!

3- In the midst of the GFC, Between the peak of March 2007 to the end of the slowdown May/June 2011( just before the recent take off) , average prices have gone down by a MAX of 7.64% during these 4 years ... and note how they have fluctuated around ±2-3% during these dark, slow, and Horrible years ....

4- Everyone can assume what he/she likes, but a historical graph like the above also shows how counter measures adopted by both buyers and sellers in each market condition succeeded in balancing supply and demand ( and consequently average Prices) That clearly shows that this market is a very fluid and dynamic asset class and has its own defence mechanisms to continuously rebalance the ship as it goes by the collective buying and selling decisions of ALL Participants.

5- Even in healthy and good years, fluctuations and corrections of ± few % points are quite Usual.

Get over the noise ( unless you just like to feel good) - be patient, ... Relax ...We are not in 2008, 09...11 ...we are in a healthy economy, employment and Growth ( for now!! ) and no one is rushing to the exit gates in the foreseeable future despite the huge efforts pushed by of some media and social websites.to paint a bleak picture

This is a long term game where buying and selling decisions are not a matter of luck, it's a matter of Need and/or correct analysis of the market of the day and what the future might hold ...

Hunting for that bargain or waiting till markets bottoms is like catching falling knives ... Funny that once you buy you would like the market to STOP falling at once and Go up again ( feels good eh?)...

Couple of counter points for discussion:

1) Past performance does not guarantee future performance. Sure in our market the general trend has been up, not so for places such as Japan since the late 80s and Ireland. If it can happen there it *could* happen here.

2) This trend has a sharp correlation with the drop in interest rates we've seen over the same period which has had a positive bearing on affordability of bigger and bigger loans. If that reverses will the same happen with correlated house prices? We are already starting to see unwinding of QE in the EU, UK and US, this is likely to flow through to us eventually - particularly given that we are already starting to hit capacity constraints. If this starts flowing through to wage growth then that will flow through into inflationary pressures. We might see a bit of an uptick from rising oil prices and from the lower NZD if that doesn't recover.

3) The GFC didn't hit NZ all that badly because we had room to provide stimulus and nowhere near the household debt levels that we have now.

4) Markets do reach an equilibrium, not going to disagree with that but the "historical data" has never reflected a period where DTI ratios have been as high as they are now. It is always dangerous to use data collected from a source that has different parameters.

5) You are correct and I also think it's a bit early to call a "crash" but a trend is starting to develop. Particularly relevant is that the only differences in the market are that it is significantly harder to achieve finance at highly leveraged levels and a crackdown on money coming out of China. Neither of these should affect the fundamentals (yield etc) of the market, all that has diminished is the expectation of capital gains. Employment is still very high, migration as well. So if we conclude that the recent rises were driven by expectation of capital gains and this no longer exists (if anything the new government is going to have more of a negative impact on this front) then we could start to expect the market to try and reach its historical equilibrium where yields would be nearer 6-7% gross. Rents can't go up that much as they are constrained to a large degree to what households can afford and wages (currently) aren't increasing much. A similar thought process could be applied to FHBs. Add in the downside risk for an external shock or I think there is a lot of potential for the current trend to continue.

Of course all of that is in the short to medium term, I completely agree that in the long term prices will appreciate. For a lot of people though their own home isn't just a way to make money - that just happens to be a happy side effect.

Hi Risky,

I will try to answer briefly as you raise very good points, .. In general, getting tangled in the details and over debating each twist and turn of this market leads to losing sight of the bigger picture ( and that is what most are concluding in a hurry).

Past performance in NZ is a very strong and undeniable indicator ( especially in the last 40 years -- after 1987) ... but I agree it cannot be 100% guaranteed ( especially when you have Gov interventions and regulations spoiling the market)... NZ is not Japan or any other country and will never be - we have our own set of culture, attitude, expectations, etc , so I dismiss comparison with others and draw any conclusions on that basis.

We can argue the effects of Interest rates, inflation, cost of living, and wage pressure - all these are details which have had mostly the same effects on the market boom, from memory, between 2002-2007 when immigration floodgates were opened , but interest rates were up in 7- 8% etc ...FHBs then had similar issues, however, I bought most of my investment properties then ....my point is : Look at the results of that period, house prices in Auckland appreciated by almost 91% in 6 years .. this time we only gone up by 76% in 5 years..

GFC had a sever impact on spot house prices, some falling as much as 20% ( obviously there are a lot of anecdotal examples) as well as businesses and liquidity in the market there were a lot of mortgagee sales ...but again the average price indicated in these graphs show ~ 7% peak to trough --- 2008 to 2011 was a period of stagnation in Auckland House sales ( very similar to the current market) - I believe that the household debt is an individual problem when it comes to housing and should not be generalised in predicting housing market behaviour or momentum ...there will always be certain percentage of people who would not afford the prices at any given time and today is no exception ( although some are pushing for that to happen). Yes, its implications on the country 's overall financial situation is important but we are passing through a good growth and productivity period to compensate for these effects on borrow rates.

Yes, it is slightly more difficult to buy now mostly because lending criteria has been tightened. We used to borrow up to 95% @ 7.5% pa for a $450-500K house in 2007-- that was a massive 36K of interest pa --- compared with 80% at 4.5%pa for a $850-900K house today ( similar areas and houses) -- which is $32.4K of interest pa and wages have risen a lot since then ... Main issues here are: Buyers' expectations are High ( most expect to buy at 2007 prices), and the numbers are now bigger so, with the 20% lending rules, buyers who did not save enough deposit were caught off guard by a fast roaring market - -- the other issue is lending restrictions, should lending goes back to 95% for FHBs as used to be at some stage about 10 years ago, I believe that you would notice a lot more buyers around, Yet again you hear buyer refusing to take on large mortgages ( people are afraid of big numbers).

I do agree with all other points you mentioned, however I believe that the days of 6-7% yield in Auckland are gone and it will take a while to get there again ( if ever) ..Property CG will also has to wait until the next cycle - However, the imbalance between Supply and Demand is sizable and will take 3-5 years to narrow that gap ( if there is efficient management of the problem, which is questionable thus far )

In the short term, We might be looking at similar market performance we had between 2009 and 2011... with a slight push of the average prices to the upside (in the range of 0 to 2% + CPI).

Rents will go up because of the accumulation of increased running costs be it regulatory, insurance, and rates & services ...these costs are hitting everyone living in Auckland and tenants won't be immune to that ....However, IMO there won't be huge rent increases in the foreseeable future (again, in the range of 0 to 1% + CPI)

There is no magic bullet, and markets tend to smooth out unless someone makes a blunder and cause the balance to tip over.

If the property press tbis weekend is anything to go -fat as bro- boomers and speculators are starting to rush for the exits. All it will take is a bunch to take less money to start accelerating downward trajectory.

Before the usual punters start posting how cool central auck is, and that they arnt worried, the coming route will be the unsofisticated and simply end game investors cashing up for retirement. Of which there will be plent.

Are you able to point out to a single time in NZ property history when that happened in a magnitude to cause a price crash ?.... or it is just wishful thinking and "Speculation" ?

However, Such an event (If ever happened) will push rent yields sharply UP to 6-7% again come summer, and the Gov will have a disaster on their hands ( they just cannot imagine dealing with an extra 1000 homeless families ) ... So properties changing from Rentals to Owner Occupiers will stress the already saturated rental market and that does not solve a problem but creates a bigger one!! --- Would be ideal if Tenants could buy their rentals, but that is almost impossible in the majority of cases.

Property press magazine does get fat this time of the year, every year ... its called spring listings !!

Ecobird,

There are lots of factors that have contributed to the recent NZ house price inflation that are totally new and unprecedented, so I don't think we can compare this bubble to previous ones, quite so confidently. QE on such a mass scale has had unforeseen consequences that we will be analysing them for decades to come I suspect.

Ecobird, debt addicted specuvestors will shortly discover how quickly their friendly bank Managers morph into venomous snakes, greed will also Morph into fear. QE IS unprecedented and I am certain there is an unprecedented price to pay for it. As reported 80% of bank lending is backed by property. The risk of the system freezing up in a crisis is now very real.

"All it will take is a bunch to take less money to start accelerating downward trajectory" correct, and the opposite of that is what we have been experiencing for some time with foreign buyers, a bunch paying a lot MORE money accelerated the upward trajectory.

Here is another indicator for what its worth:

Despite challenging conditions, residential prices increase across NZ

"https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2017/Reside…

"Are you able to point out to a single time in NZ property history when that happened in a magnitude to cause a price crash ?.... or it is just wishful thinking and "Speculation" ?"

Yes Eco Bird. "From 1974 to 1980, house prices fell by around 40% in real terms. By the end of the decade houses were no more valuable than they had been at the start. That’s shown in the following graph, which I’ve compiled from Reserve Bank data on long-run house prices and consumer price inflation."

https://www.greaterauckland.org.nz/2016/07/11/remember-the-last-time-ho…

YES, But Don't get caught with with an eye-catching headline - While that was true at the time BUT the devil is in the detail, the report clearly concludes :

"" Back then, overall price levels were inflating at double-digit rates. As a result, all that it took to get house prices back in line with wages (and prices for everything else) was for them to stand still for a few years. In dollar terms, house prices actually held constant from 1974 to 1980, while prices for everything else increased around them. Today, consumer price inflation has dropped to almost zero. This means that getting real house prices back in line with incomes, at least in the short term, will require prices to fall in dollar terms. That is, understandably, a scary prospect for politicians, bankers, and homeowners. But it could happen.""

Hardly comparing Apples with Apples Didge !! .. Of course hypothetically it Could happen Actually, by the same logic, anything could happen at any time !! - Trump might light up a devastating WWIII next week in Asia, and the whole world could collapse .. !! :)

thankfully , not everyone shares such pessimistic dire risk profiles ....

Excuses excuses!

:) ... no excuses, but it seems that you have never had the chance to live through double digit inflation times to have a feel of that kind of Struggle !! -- a bit like folks talking about War horrors in peace times with a cuppa ! .

Tut tut. I am older than boomers. I paid of my mortgage on my first house in a little over ten years because of double digit inflation.

Thing was, the double digit inflation was on both sides of the ledger, what inflation we have now seems to only be on outgoings, especially where housing goes.

Exactly.

There is no way you can wrap this up as proof of a crash coming but it is certainly clear that the boom is over for the time being and the lack of buyers would suggest that a correction is inevitable to close the gap between asking prices and sustainable financing.

this correction could be up to 25% drop from the peak pricing IMO, and no that isnt a crash because the price hikes were just a crazy, property flipping, speculator, Chinese money driven over hyped bubble with no foundations in reality.

theglc

So if the peak in Auckland was a million (it was more or less there) and prices drop 25%....you wouldn't consider a drop of $250,000 to be a crash?

If the national peak was $600,000 and that drops by 25% ($150,000) you wouldn't consider that a crash?

Sorry i was referring to Auckland alone, the rest of the Nation may well be overvalued at the moment too but probably no where as much as Auckland.

If properties in Auckland lost a quarter of their value overnight, that would feel like a crash, but that wont happen.

But consider this, a dump of a house sits on a $500K piece of land, the house and improvements are worth $200K at best, but it sells for $1m, The buyer bought in the frenzy, but what is the true value of that property? If they have to sell and get $750K for it, has the market crashed? No, someone has just paid a true value for it.