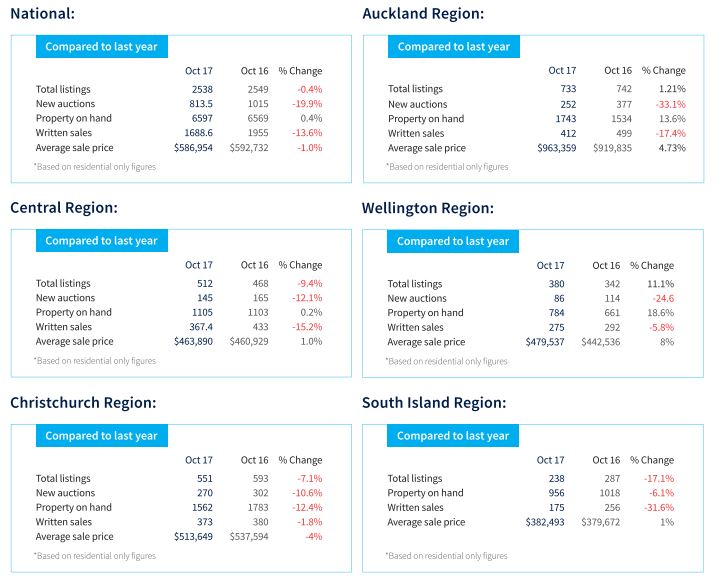

October was a mixed bag for the country's largest real estate agency with sales numbers well down, but prices generally holding up reasonably well.

Harcourts sold 1688 residential properties in October, down 3% compared to September and down 14% compared to October last year.

However October's average selling price of $586,954 was up 2% compared to September, but down 1% compared to October 2016.

The downturn in sales numbers was evident throughout the country although results varied significantly by district.

This was most evident in the South Island where sales were down just 4% compared to last year in Christchurch, but down a whopping 32% in the rest of the South Island.

In Auckland sales were down 17%, and in Wellington they were down 6% on a year ago.

But perhaps the biggest surprise in Harcourts' October figures was in the central North Island district, which includes the Bay of Plenty and Waikato where the market has generally been more buoyant than much of the rest of the country.

In October, sales in Harcourts' central North Island district were were almost flat compared to September but down 15% compared to October last year, while the average selling price dropped $28,400 compared to September and remained just 1% above where it was in October last year. In September the average price in the district was up 7% compared to a year earlier.

There were also marked regional differences in the number of new listings received in October, with new listings up 11% in Wellington compared to last year while they were almost unchanged compared to a year ago in Auckland and down in the rest of the country.

One of the biggest differences compared to a year ago was 20% decline in the number of homes going to auction.

Harcourts chief executive Chris Kennedy said there was a common belief that auctions were only an effective sales method in a booming market.

"In fact an auction's greatest strength is that it will give you an accurate reflection of exactly where the market is and what your property is worth," he said.

However he also noted the market was changing.

"The market is clearly fluctuating as buyers and sellers process developments like the election result, but overall things are steady with a good balance of supply and demand," he said.

Harcourts Sales October 2017

40 Comments

Note: 'Average' used, rather than median

It's going one way, and that's down.

2018 - the year of the crash.

People have been making very similar claims on this website since it started. Congratulations on keeping the tradition alive, however you will be just as wrong as everyone else has been before you.

Average house prices in Auckland down by 1 per cent in the last year.

But up by 90 percent in the previous seven years.

TTP

An even better way to frame it is as follows:

"Average house prices in Auckland steadily increase 90% in past 7 years and market takes a breather over past 12 months"

Communicating with the sheeple is all all about how you frame your comms. You can see that shifting the subject and introducing emotional qualifiers, it all sounds a little different and you would feel much better reading something like this.

After such a sustained boom and tremendous hype and support for house price inflation, I wouldn't be expecting anything other than a plateau on average prices. All the news on the ground, is that there is quite a gap between buyer and seller expectation, so we won't see much movement in price till that psychological issue is overcome (in either direction), as is typical of any market.

I'm still happy to wait it out, if the market is just at plateau like this, with inventory rising...then there is nothing to lose for me really. But the opportunity cost of not waiting, could be pretty high.

Opportunity cost of waiting Ginger ?

Do you believe Auckland property is going to get more expensive over the next 12 months ? 24months ?

I’m betting the cool off will run for awhile and any sign of interest rate increases or employment downturn will

pressure the undercapitalized property owners and once negative sentiment takes hold it will be a good buying time. Heck the new government policies have yet to embed in the market yet

NorthernLights. I agree with your prediction as the most likely outcome actually.

My personal opportunity cost in waiting is;

A. paying rent in the mean time

B. watching houses come and go that I may have been interested in buying (this doesn't bother my husband at all, it's just me itching to get started on a new renovation project)

C. the risk of a serious credit crunch and not getting a mortgage next year (My hubs and I run our own UK LTD company so technically earn "foreign income" which in a serious credit crunch banks *may* get twitchy about). As it is now, our bank will only lend on 70% of our income. We are pulling together a whopping deposit though, so hoping that will mitigate any tightening. If GBP/NZD returns to the historical norm any time soon (2.2) then we might not even need a mortgage at all. That's pretty unlikely though, Brexit negotiations so far are a blood bath ;-).

There is an opportunity cost for any decision. But if the market is flat, the risks of waiting out the market are pretty minimal!

Ginger my advice

Find a cheaper city to live in NZ or elsewhere. I’m old yet still made the big shift overseas.

Auckland is just too hard at the moment and may take awhile for prices to drift south.

If your UK business controlled via the internet ? Highly commendable

I’m sure you’ll do well

"........ but overall things are steady with a good balance of supply and demand."

This statement is meaningless! No doubt, it's supposed to sound positive - but, in fact, it adds nothing useful to the script. Put another way, it's a waste of space.

TTP

Exactly, if you can't spin it, fudge it!

"Put another way, it's a waste of space." Yes like the repetiive drivel from property speculators.

TTP, But up by 90 percent in the previous seven years. If in the short term prices were to even stay static (take a breather) at best - how will the specuvestor cope? Not well. Bank pressure and anxiety will eventually lead to more selling - it will all be self sustaining in the downward leg like a snowball. It was their impatience, greed and borrowed money that got us here. Greed WILL turn into fear as specuvestors experience "buyers remorse", clearly not in it for the long haul. It wasn't that hard to trot down to the local bank and say "how much can I borrow" The following article gives an idea of how far we have come down this one way road. TTP, this sick market is the new normal and is not going to end well simply because of the leverage factor alone. I'm sure you will agree that to get 3% return after tax on a term deposit is smarter than negative returns year after year: http://www.nzherald.co.nz/sponsored-stories/news/article.cfm?c_id=15037…

Hi Retired-Poppy,

"Specuvestors" are risk-takers by definition.

There are standard ways the market has for dealing with the likes of them - if/when they go belly-up. These include mortgagee sales and bankruptcy proceedings.

But good luck to them. Some are astute and savvy - and do very well. (Having money in the bank earning 3% interest after tax wouldn't likely appeal to them.)

TTP

The title says it all. https://www.stuff.co.nz/national/politics/98813714/if-youre-old-and-ric…

Geez, hard to understand why there are so many bitter and negative people that comment on here!

If you have so much energy You would be far better off spending your time improving your properties to improve the value, like I have been doing today!

...value aspirations aside, (if you're a Landlord) your tenants might even thank you, providing you don't hike the rent! : https://www.stuff.co.nz/life-style/homed/community/98750401/landlords-s…

Hi THE MAN 2,

Please note that disaffected people have been congregating and worshipping at this parish for some time now.

Sadly, many of them have never owned (and are never likely to own) a property.

They're just too negative for their own good.

TTP

TTP, your apparent lack of insight has lead you to become insubstantial with your assumptions.

Is it just me or are there a shed load more houses being listed with asking prices on Trademe? I don’t look very often but I feel like the last time I did pretty much every house was by negotiation or auction.

Dont look at Trademe, there seems to be a rash of urgent and reduced listings. Auckland listing for sale are increasing by about 100 a day now. Lets hope the xmas rush starts early this year to take the downward pressure off.

Yes, I highly recommend sticking your head in the sand and ignoring whats going on around you... Who wants to see the guillotine before it lops their head off.

It's notable that Harcourts has fewer listings in Auckland for Oct17 than it did in Oct16. Also Auckland average sale price is up 4.73% for the year. I've just been looking at the prices that houses achieved on the weekend and last week and things look pretty normal with some very good prices for sellers. Quite a mix of properties too.

wow 4.73% yoy increase that must cover the mortgage interest off with a nice lump left over.

I sense a bit of sarcasm but actually, yes, if it were realised it would be a very nice lump left over. I'd be perfectly happy if it was consistently 4.73% yoy.

Oh - Zachary!

Can any property investors help me out, I am thinking about buying an investment property https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

I'm running the numbers for a 760k loan and its about 1k a week. The tenants are paying 425 a week which is great. So if i'm paying 575 a week to top this up how long until I am making a profit?

Two lifetimes!

I'm no property investor, but I'm pretty sure you'd need a $315k deposit to buy that place as an investment property. That means your mortgage would be $470k. $450 per week would cover the interest @ 5%. That's only $25 a week top up + the opportunity cost of the deposit. Sounds like you're onto a winner.

Moneyphobe, first I think you will find the mortgage interest payments are considerably lower than 1k a week, for a hardcore investor with connections more like 630 a week on a one year interest only loan. Secondly I imagine the investor is likely to consider he has at least 250k equity. In this scenario the rent is covering interest costs although rates, insurance etc would be a negative. This particular property doesn't look great at first glance for any unusual appreciation. If it had the potential for turning into a funky three bedroom house or was in a particularly promising location things may be different. A personal reason like a future home for the kids or downsizing or something like that may be factors to do something that is not all that attractive otherwise.

i would put money on it that the house has been reconfigured, might pay to get a builder to double check the work that has been done.

Last week's sales posted in the auction results page show that yet again what did sell sold for very good prices from a sellers's point of view. Twelve properties listed with a sales figure of 24.31M and an RV of 15.57M giving a result of an eye watering 56% over RV. All tended to be in good locations.

Zac, I find your updates interesting, and would like you to continue, even if/when it does not prove your point anymore.

I also think you need to consider that a lot of auction properties are picked by RE's as worth going to auction for, so might be skewed towards the better ones.

In the past you regularly mentioned homes.co.nz valuations, but since they have not recently been very helpful in proving your point, I also think you need to consider them a more balanced reflection of total sales, including distressed ones, and the non-auction quality homes.

I agree that the houses going to auction are mostly those likely to sell at auction. When looking up RVs I find TradeMe to be a lot quicker to access than homes.co.nz.

The point I am trying to prove currently is that the desirable locations will be largely unaffected by a downturn in house prices and Auckland has an awful lot of these locations.

Hi Zach. I dont think I would disagree that good location will always get good prices. Hopefully they reduce a little, but these areas are aspirational, and people will save or have good incomes to get them.

For me its all about average houses and average incomes. House prices will need to come in line with what is affordable for people, without those people getting in trouble financialy should circumstances change.

I too want you to continue, ZS.

I personally can't wait to see what your analysis shows once the CVs have been updated.

Real Estate.co Auckland listings 13077 and rising @ 70-100 per day - no area immune. More listings returning after failed auctions with "negotiation"or fixed prices. It's the new normal and might I add, a lot more sane. No matter how Spruikers spin it by comparing it to out of date CV's, real prices continue to slowly drift down. In previous downturns (in particular 1990) I observed that even in desirable areas, house prices tanked - in fact more so. What makes leafy areas immune this time around? It's Spruiker talk. QE + Cryptocurrencies, ETF's, shares, bonds & property, minus QE = bust.

Letter through the mail yesterday from Harcourts on prices of 10 or so properties sold in my area and it looks like 30-40% over current valuation if you have a decent property to sell. The new CV's coming out very soon and sell prices are in line with the 40% expected increase in the last 3 years.Expect the new figures to strengthen the market, its all about perception.

Well when I buy a house I have to pay money. My dreams wont cut the mustard. So its really comes down to what I can afford to pay without my kids starving.

Other people may be different.

Real Estate.co.nz Auckland listings now 13129

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.