The residential property market could start the New Year with a doozy of a hangover thanks to a flood of new listings hitting the market.

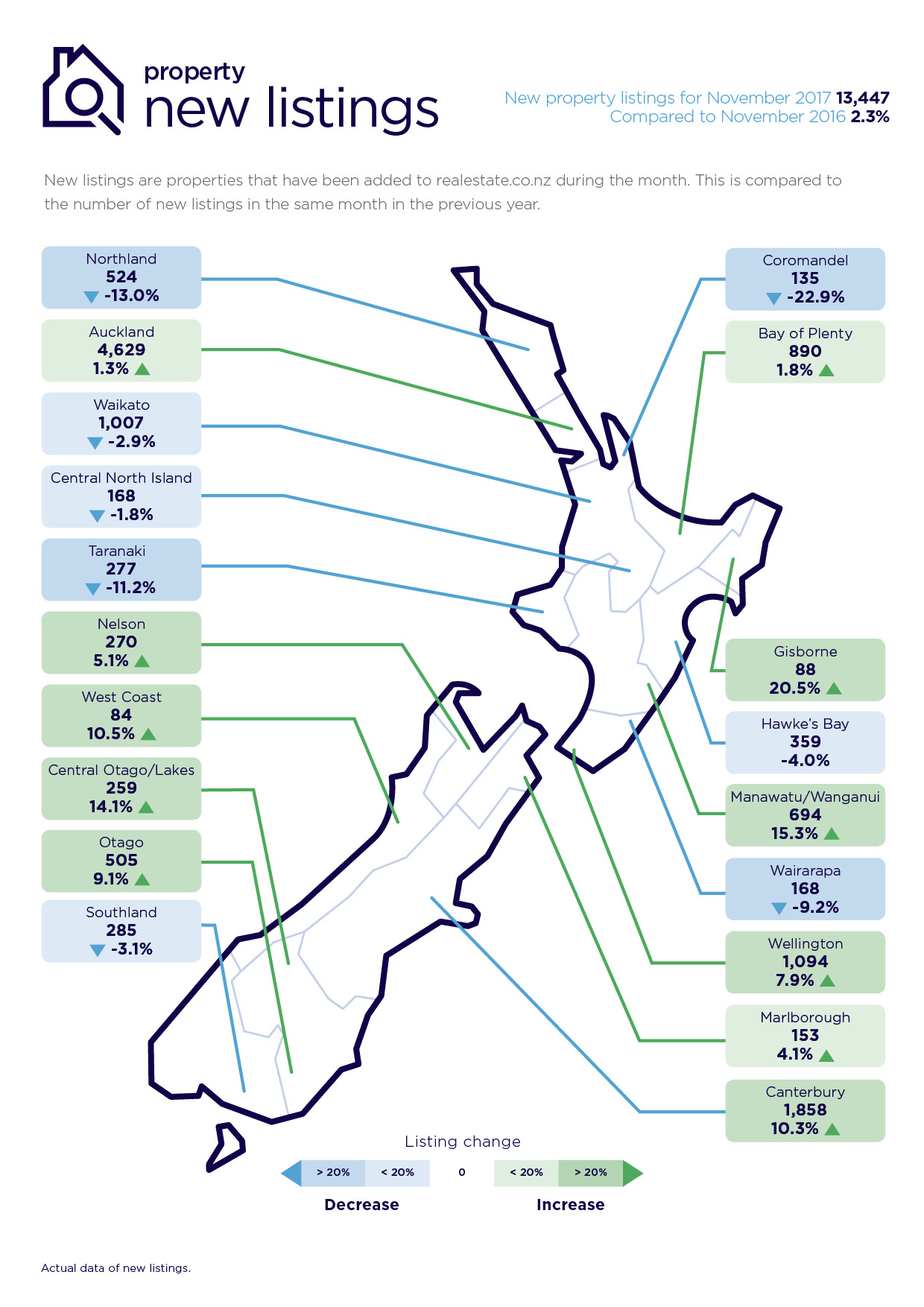

Property website Realestate.co.nz received 13,447 new listings of properties for sale in November, the highest number in any month since November 2014.

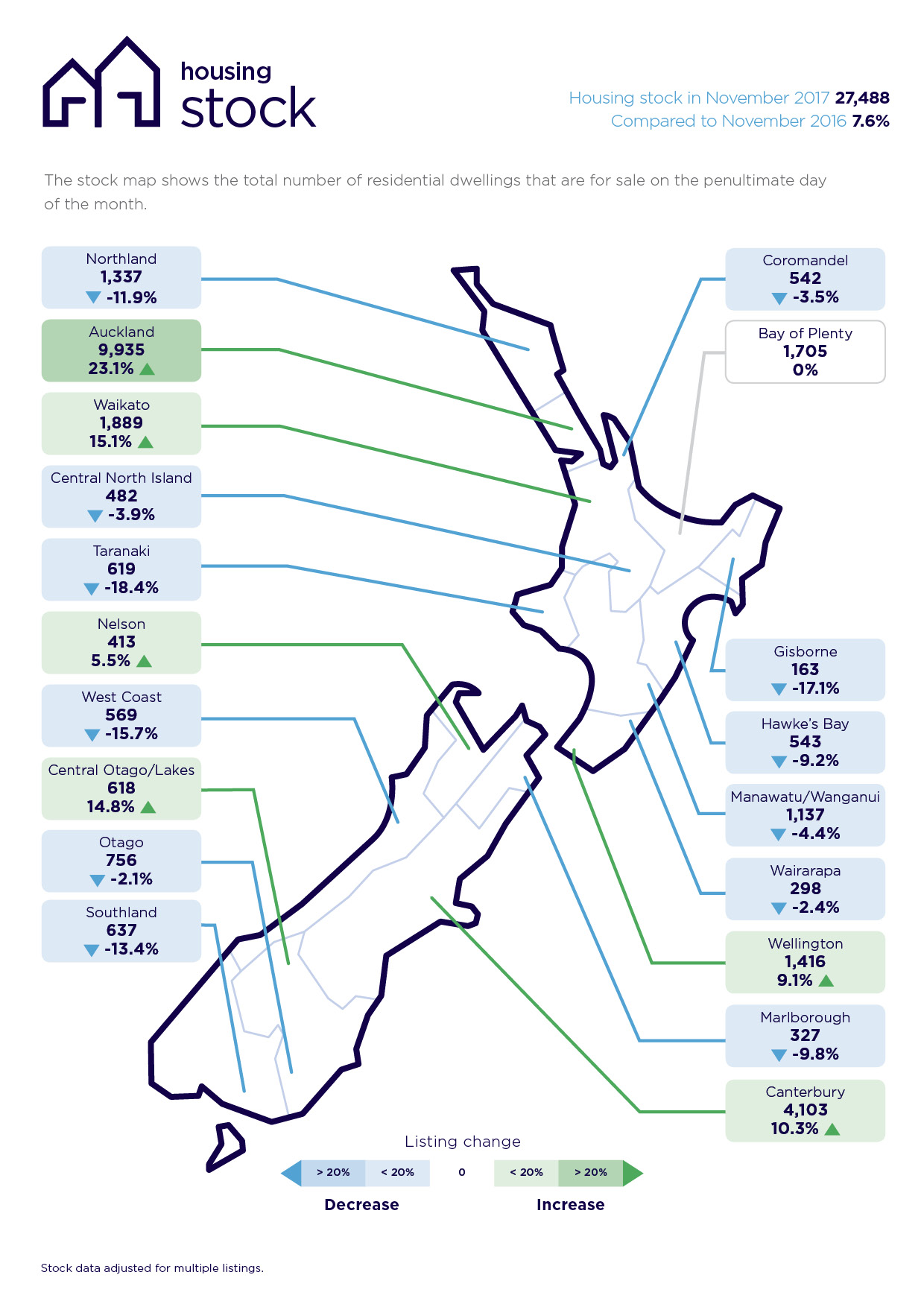

That pushed the total number of properties available for sale on the website to 27,488 at the end of November, the highest number since March 2016.

While that could be seen as signalling a more buoyant market, all of the market signals at the moment point towards sales not keeping up with the supply of new listings, which is pushing up the stock of unsold properties.

The means the market could start next year with a growing overhang of unsold stock, and a hangover for vendors and their agents whose properties may have been sitting on the market over the Christmas break and then face greater competition in the New Year.

But it could also push the pendulum more in favour of buyers, who will have more properties to choose from and greater bargaining power.

Compared to November last year, the total number of homes available for sale on Realesate.co.nz was particularly high in Auckland, Waikato and Canterbury.

"With this increase the market is now sitting where it should be in terms of total stock," Realestate.co.nz spokesperson Vanessa Taylor said.

"The heat that lit the 2015-2016 market is no longer evident.

"The slow start to the 2017 year was equally challenging for buyers and sellers.

"What we are now seeing is a normalising of the market which will benefit both groups," she said.

249 Comments

Combined with 3.95% mortgage rates to prop up flagging prices - should be.good for buyers.

Buyers? What buyers? They can't become Buyers until they've been a Seller first ( ask any lender!)... Vicious Circle stuff....( And, no. There aren't enough FHBers to make a difference this time.They were used up months ago....)

Looking at new mortgage lending in C31 shows that FHB lending on new mortgages is pretty much flat and has been for the past two years. Owner occupier and investor lending for new mortgages is down. For house prices to stay up both existing owners and investors would need to be buying more property or moving up the "property ladder".

Hi bw,

One does NOT always need to be a seller first. That simply isn't true.

There are divestors, as well as those with cash.

TTP

Sorry TTP, Those cash buyers from overseas are long gone. Go take a look at the latest auction results, not much activity there. It's a buyers market do you know.

Hi CJ099,

Your comments are misleading.....

There are cash buyers in NZ - and still some from overseas.

And there are divesters as well.

TTP

What proportion of sales do they make up now vs last year?

Who’s the One TTP ?

Is that your dog ?

Who wants to buy now that Auckland houses have crashed 200k since march ? The Avalanche is starting to fall , and it has not even picked up momentum yet ! Wait untill early next year with all the new panic listings flooding the market. When the Avalanche comes down early next year 200k lose will feel like nothing compared to the pain thats coming.

2018 - THE YEAR OF THE CRASH ( or is it already here ? )

In case you haven't noticed TTP, The majority of those 'cash buyers' will be money launders.

CJ099 - you are right - even the OFH (Obvious Fox Hunters), spooks in the corner taking notes with dark glasses and ear pieces are gone now.

Thanks Smalltown, It seem to be that either TTP is very neiave or is keen to promote illegal activity.

Hi Mortgasge Belt, who offers 3.95% and for what term (I assume 1 year ?) Thanks

Not quite yet, but call centre staff are offering a .2 & .3 cut on the carded 1 year rates at most banks currently without much prompting.

OK, thanks. I got offered 4.20% for 1 year fixed by ANZ yesterday

Dead cat bounce. Last chance!

We're pretty much on schedule for the illusory 'return to normal' phase.

Despair is never fun, but it's coming....

Sad

..but true" Metallica quote

A dead cat bounce is when prices temporarily go up, in a down trend. How does it relate to this article ?

Because I expect the prices to rise minutely for a month or 2 after RBNZ engineers a soft landing although it seemed to me it's more like using FHB to plug the gutter.

This could be the dead cat bounce that they are referring to ...

... going by past cycle patterns, there is likely to be a small “dead cat bounce”, which looks like a recovery but isn’t, in the years after peaking before the market finally peters out.

“This time round, a dead cat bounce will look good in a year or two, but that will peter out. This type of bounce is pretty common but the renewed interest tends to fade out as people realise that things still aren’t sustainable.”

Quinlan said that we are 5.5 years into the current cycle so, assuming it is a “normal” cycle, the market will lose 10% or so from current peak prices over the next four or so years.

The good news is that the cyclical peaks in real terms have been 160% for the 1970s, 138% for the 1980s, 138% for the 1990s, 186% for the 2000s, and 151% for this cycle, he said.

“Add inflation at 1% a year and house prices will likely increase by about 50% over the next cycle.”

https://www.landlords.co.nz/article/6149/capital-gain-time-over

Because past performance is a great predictor of future performance....

And, in the next breath... Real Estate is so different from every other asset class.

:/

CWBW

Yes dead cat bounce alright

Time coming for more home affordability less speculators

Auckland stock available increasing 23%... Wow!

Housing shortage seems to be fading away somehow.

The stock for sale is not directly related to whether there is a housing shortage or not. Most of the houses listed for sale will already have someone living in them - they are not necessarily vacant properties.

I agree, there is still a "housing shortage" in Auckland, just not a "housing for sale" shortage

Buyers need to start being ruthless with lowball offers. No buyer ever must buy, but plenty of sellers must sell.

Let's watch this grotesque house of cards tumble!

I'll admit that I have been doing such things, but the sellers aren't quite ready to accept less than ~20% over RVs set within the past year (I'm not in Auckland though), unless there is something very wrong with the property. It's only a matter of time though. Patience. Patience.

Don't rush. The best is yet to come. Prudence!

Those new council valuations are going to work in favour for FHB . The market will keep tanking as the greedy will hold on and hold on missing the chance to sell when they could. They will become forced to jump to the front of the line and have the best price on offer. And thats going to be way more than 200k less than there council valuation says.

I seriously hope it will be a slow decline.

A quick crash might force to govt to reconsider some of their policies that I see as crucial to this country's future such as

Stopping foreign buyers

Limiting immigration

Reforming tax for property investors

opening up the Auckland urban boundary

Building 10000 new homes each year

These all need to still happen

of course no-one will be able to control the rate of decline....

Brock Landers what a wordsmith

Grotesque indeed

Seems this will be the real test of the market with some decent volume hitting it. Chances are that we will have a lot people unwilling to drop their price, with recent CV's not helping.. Sales turnover remains low.. Then prices can only go one way as people need to move on.

So on a rolling 4 month average, Auckland currently has 5.9 months of residential property stock available for sale. This is the most since 2008, during a financial crisis, when interest rates were slashed . Where is Ted, the housing shortage, the Chinese dudes, where is it cannot happen in my neck of the woods, the pent up demand. Odd that the RBNZ wants to wind down the LVRs.

13583 houses for sale in Auckland, 1632 sold in October, so about 5 months average time to sell. Wouldn't want to be a vendor.

How do you get 5 months avg time to sell ?

fit an exponential decay function to the sales rate and total stock. With current numbers of 1632 and 13583 half sell in just over 5 months. Mathematically analogous to radioactive decay half lives or capacitor discharge through a resistor.

Did you use a flux capacitor? Maybe that’s where you went wrong

.

.

And we aren't even in an economic recession. If we get an economic recession with job losses, and slowing economic activity, the number of financially stretched owner occupiers will potentially start selling as they are unable to meet debt service payments.

Given all the employment created during the development of this housing ponzi, I think the labour market is going to turn down quite quickly soon. The business confidence survey is an excellent leading indicator of that. It's hard to imagine there are as many employment contracts with redundancy clauses in the services or construction sectors. All that discretionary spending created on the way up using houses as ATM's is about to go into reverse.

I wouldn't be surprised if a lot of disillusioned folk head back home via Auckland Airport fairly soon. Learning via social media and otherwise, less will come here seeking opportunities whether the Government cracks down on immigration - or not.

Where does that leave the current and very temporary rental shortage!

Retired-Poppy, FYI - http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

Thank for the Link, hopefully it can be an eye opener to those who just bash an industry that provides service and employs significant amount of people.

Makes me wonder how GR ( in his speech today) would replace a 13% contributor to GDP and find that growth elsewhere ?? Talk is cheap !!

property speculators and traders are all gone now, this asset class has ceased to be a tradable commodity for making an instant buck. we have genuine buyer and seller now who would either live in, add to investment portfolio ( only 7% of landlords said that they would) or buy to develop and explore hidden potentials out of existing underutilised homes or land.

What is left now is the usual flow of property sales and purchases as to when the need arises to move, upgrade, terminate, immigrate, or downsize.

The reduction in new supply and its elevated building costs renders existing quality houses more valuable - and as we approach this balance in the market, quality houses will appreciate ( in my view) between 2-5% pa in the main cities which is much less that the 10 -15% pa appreciation in construction annual costs.

There will always be desperate people at any given time and season and they will be forced to sell at a discount ( depending how fast they need to move) or how fast they need the money ( like selling a deceased estate)...these will not affect the general market at all.

I agree with the view that most buyers need to Sell first whether moving out or upgrading, hence selling at a discount and buying an expensive upgrade will be a deterrent for change to most !

Housing market cannot stop, lowering house prices will stall the construction industry and reduce the overflow of this Market's benefits to the entire economy. we remain hopeful that this Gov knows what it is doing !!

Hope that next year will pass without too much Damage !

CN, thank you for the link - says it all really! A timely reminder employment in the construction industry would be hit too!

1) the real estate agents with lower transaction volumes, lower property prices leading to lower commissions, so potential reduction in real estate agents,

2) mortgage brokers - lower loan volumes, leading to lower revenues

3) home staging businesses - lower transaction volumes, lower demand for house staging

4) property construction businesses - developers, sub contractors, tradies, general labourers

5) banks - loan losses, banks cut staff due to fewer loan applications, implement automation, probably hire staff in process mortgagee sales, loan default

6) property sector lawyers, accountants and other service people experience lower revenues, cut staff

7) slowdown in revenues in construction materials by property renovators - businesses such as Bunnings, Mitre 10 see lower revenues as fewer DIY renovations, etc due to no expectation of capital gains.

8) lower spending by the people in above businesses impacts consumer retail spending - new car sales, coffee shops, cafes, restaurants, bars, clothing, jewellery, entertainment, etc - job losses in these areas as these businesses see revenue reduction

9) job losses in (8) further reduces overall spending.

10) manufacturing for the local economy slows down - potential job cuts which leads to lower consumer spending ...

Prices drop, FHB start buying with lower mortgages and therefore lower repayments, actually have money left to go out every now and then and get the car serviced. Mechanics and restuarants get busy again.. blah blah blah.

Anyone can write a heavily biased report saying how great their industry is for the country. Heck, i'm sure the motorcycle gangs can dream up lots of reasons why their drug trade is good for NZ.. all that black market cash has to go somewhere right?

All that black market cash went into real estate.

True, I don't think it's irrational for younger Kiwis to prefer the scenario of a crash followed by a recovery, over things staying as they are. Times will be hard for them, sure, but time is on their side much more than for older investors who would prefer the status quo to remain for decades. The young Kiwis will be doing it hard either way, so it's irrational to expect them to prioritise protecting older investors who seem to have had no regard for younger Kiwis following them.

Corazon Miller's usual "property is the best" article as much as anything highlights that having property investment as one of the major pillars of the economy is a bit silly, really - compared to countries that are doing more productive things to make money.

Rick

You know the reason property ownership is desired is societal stability

Generally this is a desired paradigm but I agree in many countries renting is the norm long term too and it works if the landlord is a big business or a housing authority

The US govt for example sought home ownership for the poor as a way to improve their lot

Sadly that experiment was corrupted by worse than subprime lending where there was no possible hope of loan payments being made. Lending for commissions with no care.

Ultimately we seek stability if renting or owning our homes

I know I’ve experienced a landlord selling the home I was renting ! Typical amateur Auckland landlord

I bought his property but not everyone renting can do that

The NZ governments across most of the 20th century also sought home ownership as a way to improve the lot of Kiwis, they just didn't rely on sub-prime mortgages to do so. But NZ's home ownership rate did soar because of such prioritisation of policy. Until housing was turned into an investment for some, rather than homes for NZers.

At the same time, I agree we need a more professional renting market, and should look to countries such as Germany where renting has successfully worked for many.

Indeed, and much more .... everyone knows that the housing and building industries are one of the important and significant pillars of any economy - People do not think before they emotionally wish for a crash and advocate for it ! ...

The RBNZ was clear and took a very clever step by moving on LVR now before more dire consequences were faced by the collapse of housing prices.

It is essential to address poverty and homelessness, but we should stay away from foolish radicalism and knee jerk reactions ( mostly influence by the Green) whose major incentive is jealousy and other similar stupid ideology.

This Gov is obviously repeating the slogans to get people prepared for some stupid ill- planned moves it will take ( PT announcement today) - returning to socialism and Nanny state of the 70s is hardly the answer, but hey, this lot doesn't know any better !!

3 years to go, the more their empty promises are revealed and exposed. the sooner they will leave tail between the legs. ... BUT, this is NZ , even noobs have to have a go !!

It will be sad and amusing to watch them backtrack and strip off these promises one after the other .....( water tax is a start)

You have made some good points.

The economic contribution of a sector that requires the preservation of Auckland prices at 10x income and household debt to income ratio of 170% is not a contribution worth having. It’s fools gold. The current value of the RE and residential construction sectors reflect the stimulatory effect of the tsunami of mortgage credit that has hit the economy over the last few years. The principal effect of this flood of money has been corresponding increases in agents commissions and the cost of labour and materials in the residential construction sector, not corresponding increases in productivity. When that tide recedes those costs will fall, in my view again without any corresponding impact on productivity. The cost of construction will fall. There is no national interest in having a residential RE and construction sector whose costs and revenues are artificially inflated by a credit bubble. That sector is currently operating on a completely unsustainable cost and revenue basis, and that needs to change. It would have been far better if this ridiculous credit bubble had not been allowed to occur in the first place, but we don’t have that option anymore.

Yes I very much agree with you Reitired Poppy. There's another elements to add to that mix. All the accumulation of unsold Auckland property is going to be entering the rental market. Been there, done that, during the GFC in Europe.

An oversaturated market will be a huge influence on driving down both property sale and rental prices.

Currently on Trademe.co.nz there are 4,501 properties listed for rental, then there are another 300 listed on Airbnb. I realise that both of these cater to different markets. Not sure how many landlords are moving from looking for longer term tenants to shorter lets on Airbnb and other similar sites - this obviously means fewer places for rent for longer term tenants. If the owner of an unsold investment property then decides to rent out their investment property, then this increases the supply of properties for rent.

Do we have a shortage of rental accommodation or affordable rental accommodation? With 4,500 houses listed for rent I don't know the answer. Perhaps we have a shortage of single unit accommodation for students in inner city suburbs ....

The total number of listings in the Residential section of realestate.co.nz is currently 39,258. Where is the 27,488 figure derived from? I've been tracking new listings on RE an TM since Winston made his announcement to go with Labour - 20 October. It took a couple of weeks for vendors to get their properties market-ready but by the week ending 3 November listings had increased 10-20% across all main centers. The realestate.co.nz November report is going to be an absolute doozy.

JRSNZ, dwellings and properties are different.

39,258 current listings for sale vs October transaction volume for NZ of 5,689. This is roughly 6.9 months.

JRSNZ

Surely you are scaremongering!

We have 3 semi eloquent spruikers here who all proclaim business as usual

Yup could be right about waking up, but will be a rude shock, won't know what hit them

I think the sharemarket equivalent of false return to normal is "suckers rally"

If you treat our housing market like Enron then this is the point where they convince their employees to buy a lot of shares.

I'd guess the Real Estate Agents Collective all have as many as they want/can buy, already! Unless their employers do a Fonterra and bring in subsidised in-house lending? Maybe that's already been going on, as some of the bigger ones already own a mortgage broking outfit on the side, so even that isn't an option.

The trick with commissions is to take the money and diversify it, and not reinvest everything into the same market. There were stock brokers and financial advisers making commissions from selling Bernie Madoff's fund who though something could be wrong but also invested their money in his fund. Investing ponzi scheme commissions back into the ponzi scheme is just another poor decision.

To use another Enron analogy. Who is on crack. The buyers or the sellers ?

Never mind, the wise and prudent Kiwi investor will skillfully unwind their long position in housing at an amazing profit just at the right time and then throw everything at Bitcoin just as it takes off vertically.

Oh the sheer talent.

I hear Warren Buffet is to jet into NZ to pick up some tips off us.

He will no doubt be visiting Heinz Watties Head Office in Parnell because he owns it and the staff have been expecting his visit for a couple of years.

or a "bull trap"

Bull crap you mean

of a "bull trap"

Lower mortgage rates - tick

Tighter bank lending criteria - tick

Collapsing business confidence - tick

Healthy homes bill - tick

Increased listings from worried vendors - tick

Collapsing auction clearance rates - tick

Buyers market - tick

Time to buy? - NAH not yet......the decline has only just begun.

Foreign buyer numbers down considerably due to external conditions - tick

We best remember that this trend started quite some time ago, around about the time the Chinese government tightened up capital flight from its shores.

RE agents waking up to reality - tick

RE Agents to be replaced by technology to reduce commission fee and business expense (Via a mobile phone app). - Soon to tick.

> Tighter bank lending criteria - tick

Didn't RBNZ just announce easier lending? (10% of loans to LVR's to 15%)

What RBNZ want to increase doesn't mean banks will fulfill. Banks are doing their internal property valuation for every mortgage application now. If purchaser is over the top with their offer, they'll have to increase their deposit substantially or it gets declined. Gone are the days only selected properties are thoroughly screened.

Rents in Auckland rising fast - tick

Shortage of rental properties available in Auckland - tick

Continue to rent or time to buy? .... the demand for rental properties has only just begun.

http://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=119…

What rubbish! There's always a 'shortage' of properties according to Anne Gibson. It doesn't matter what they are or where they are, Anne will write about a shortage. Ask her how many rentals she owns!!

What there might be is a glut of former rental properties all For Sale, as their owners try to move them on ex-tenant. But if they don't move, guess what will happen to them? Yep. They'll be back on the rental market hoping for some kind of rent, any rent, to cover the ever on-going bills.....

..the decline in ability to pay has only just begun - tick

Saw the headline "Four reasons Chinese house buyers love NZ " and knew it had to be her

http://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=119…

Is it too early to start talking about how Chinese New Year will solve everything??

She is paid by NZHerald who gets a lot of revenue from B&T and quite often has market comments from ..... you guessed it Peter Thompson

No, it is too late

Not a surprise that rents are rising with less rentals available.

Declining house prices and increasing rents will improve yield markedly and at some point, it will make financial sense cashflow wise, to buy a rental house again. (providing interest rates remain where they are)

Rents aren’t rising significantly, see the trademe figures YOY. For Auckland, about 2-3% in real terms. that’s been consistent over the last 4 years or so. So no, there is no rental “surge” nor any recent change that will make a difference. The NZH commentaries bear no relationship to the data. They never do.

People continue to move out of Auckland... TICK

Do you really think the RB & banks are going to let prices deflate?

No, they will heroically hold it back, like King Canute did with the tide.

How are they going to support the market? The chinese money tide has turned, rental yields are rubbish and need healthy homes insulation installed, and there doesnt seem to be a massive amountof FHBs willing to take on 3/4 million dollar mortgages to buy a 1960s poorly insulated shoebox in ellerslie/panmure.

Lower interest rates ... Oh I forgot, not much room there

It's no secret that consumer and business confidence is now slowly deteriorating despite the lowest interest rates in 50 years. As things further deteriorate, getting access to this credit could well prove harder and harder by the day, further pressuring house values, stressing businesses and slamming the labour market - a domino effect.

As many already know, the RBNZ FSR for Nov 2017, the average debt to-disposable income ratio of households with mortgages was noted to be 325 percent, up from 280 percent in 2012 and eight percent of households currently own investment properties but these households account for around 40 percent of housing debt.

In the May 2017 FSR, it was mentioned that banks had tightened credit conditions in response to slowing deposit growth and (elevated credit risks in the property development and dairy sectors) In the same FSR, it was also mentioned the most indebted 20 percent of farms as owing around 50 percent of dairy sector debt. I find it hard to imagine this part of the picture has changed much - if at all.

Our great country is now more vulnerable than ever to another GFC, made so by the many who have leveraged themselves up to their eyeballs. Now banks are nervous and appear to be on a race to the bottom in an effort to reduce exposure.

On a global perspective, I think we are just one more event away from full blown deflation that more QE might prove pointless. It's the daily reminders of folly like behavior, such as Bitcoin, that serve as proof it could all turn south on a dime.

I know this echoes others with similar thoughts, let's pray it never happens.

Heh. Like the little 'prayer meetings' periodically on Gold Rush:

'Dear Lord, God of all things, please make that there Hill exude all of its Gold right into ma Outstretched Paw. For this we pray and thank Thee in fervent anticipation. Amen.'

RB took years to take serious action to stop crazy house price rises despite flagging it as a financial stability issue. I wouldn't hold out too much hope that they'll save the day in the other direction if it comes to that.

The Reserve Bank do not control the trend, only the peaks and troughs within the trend. They have been a miserable failure on the peak, so expect similar for the trough. They have also been a miserable failure in controlling inflation, with the money supply growing at 7%.

So to summarize the Reserve Bank has been a miserable failure. As I have commented before the RB is famous for its too little too late & too much too soon,

The Fed, BoE and ECB all tried with previously unheard of levels of stimulus and failed to prevent house price falls across the board. But surely the RBNZ can do it.

I have found this video of RBNZ actions to be taken during a financial crisis.

https://www.youtube.com/watch?v=m53jnZQP32g

Thumbs up to Interest for using a drunken muppet as a metaphor for the housing market.

True! It's very ZeroHedge, right?

That's an actual photo from a RE Agency's Xmas party !

Trademe. Hamilton. 19% more listings than 12 months ago. Now at 772, hit 700 back on 15/11. Expect the Waikato to be hit hard - silly money paid by silly Aucklanders for rubbish houses and poor tenants. It all looked so cheap from over the hill.

Agreed. On realestate.co.nz Hamilton City had 821 residential on 20/10/17... now at 1002 this morning. 22% increase in just 6 weeks. Lodge sold just 3/15 at auction, Lugtons 5/5, Harcourts 2/13 for a grand total clearance rate from the big 3 of 30%. It's been under 50% for a few weeks too.

A wee Friday anecdote for y'all.

Property for sale in a good part of Auckland: it went to auction recently, not a single bid. Vendor has already purchased elsewhere. They were hoping to sell for $1.4m. Latest CV came back at $1.2Xm. One offer so far at $1.1m. Vendor was borderline furious "the cheek!" "how could they". Vendor now seeking some comfort and is talking about the "I'll just rent it out" option (you know, just for a year or so).

The problem: this is the logic that caused lots of properties to be withdrawn from sale late 2016/early 2017. It's happening again now. The vendor in my example will incur a cash cost to carry their property from here on (I would guess $10k+ per annum). And the property will likely be worth less in 12 months. What then?

It's a negative feedback loop and it's only going to get worse. The RBNZ getting cute trying to engineer a soft landing won't work. They can either continue to restrict credit (LVRs + current interest rates) and have lending volumes decline, prices falling. Or, they can "release the kraken!" and remove LVRs + drop interest rates and keep the market running on fumes for another 12 months or so.

The opportunity cost of holding that 1.1 million property is approx $50,000 per year. Add $10,000 in cash costs, and I hope they have deep pockets or manage to rent it out for a premium.

Zombie Ponzi

Auctions are not suitable in current market conditions

RE agents love them because it forces vendors to wake up to their outlandish selling price and gleans some extra profits carrying out the auction charade for the REA

I sold for a full 300K higher than the best auction bid less than 2 weeks after auction via negotiation and there was no negotiation It was this is my price .

Markets completely different today regardless of what the 3 Spruikerteers here say otherwise

In the last week or so the listing on TM has been relatively steady - for Auckland anyway. Sitting around the 12,100 ish mark. The interesting part about that is the number of new listings. It is easily at least 100-200 per day. Where are all the other listings going. It must be listings being withdrawn from miserable auction results? My observation indicates that at least 100 are coming off TM each day. B&T only sold 82 for the whole of last week at auction.

Exactly, see anecdote above. Funny that there might almost be as many pent up potential sellers as pent up potential buyers.

The only thing precluding a deal is a 20-30% reduction in price (or a 20-30% pay rise....lol).

TM listings are up around 22% since the election announcement.

The smart rats are abandoning the sinking ship - COL New Zealand.

Seems to be more property ads on radio at present like the guy moaning about the compulsory Xmas break. Anyone who goes into these schemes are stupid.

Agreed. Property get rich schemes serve the interests of the developer, by passing the risk to you. Mind you people still fall for the Nigerian cash up front for some diamonds scam, after its has been circling the internet for close to 20 years.

As they say...one born every minute.

Yeah I know, still waiting for my $200M from the $10K I sent, that was 1998................

What's scary is seeing Corazon Miller and Anne Gibson at the NZ Herald pushing these sort of stories regularly. Oh, the decline of a once venerable NZ newspaper. (I've heard, anyway.)

Labour claim that property gap in Auckland is about 40k, this is absolutely bullshit as 30% of houses are owned by multiple property owners.

Err, who owns the properties doesn't factor in to the size of the so called property shortage. People can live in a house whether its owner occupied or rented. Its more or less :- Population/ avg ppl per residence vs number of residences. Except that the number of ppl per house is higher than the number they are using, so there isn't so much of shortage, just a lot of overcrowding. Drive thru mangere and otara and see how many garages have beds in them.

Hi Pragmatist,

Quite a few garages have beds in them - but they're in storage.

TTP

That's some good eyesight you have TPP.. To see what's happening in garages in Mangere from Chch. Or perhaps just more of your wishful thinking?

Pragmatist

I think TTPs thoughts are purely wishful

Not just Mangere but all over Auckland garages have people living in them

Cars parked outside

I can confirm that people are sleeping on beds in garages in Otara and many other South Auckland suburbs. My daughter and her partner were renting a very new and modern one bedroom standalone townhouse in Otahuhu until recently and I witnessed for myself, a large family occupying a 2 story housing NZ house which had two elderly grandparents sleeping on couches on the covered porch upstairs. I mentioned it to my son-in law and he just said, "Oh I think that is just part of their custom to sleep outside because they come from the islands". WTH? I wasn't ready for that response! I think he is a little miss-informed!

Its not just in South Auckland, there's a lot of garage sleepers in our area (inner west) and in the last few weeks we've noted a number of family tents in people's gardens too - and they're definitely not temporary given that we've seen proper furniture and power connections being run into them.

.

I just spoke to an Eastern Bays agent. He's sold three houses this week, all good prices and two to offshore buyers sight unseen. Cash sales. Sorry if that doesn't fit the tone of the day for some on this board.

You're a good story teller..

I specialise in non fiction, unlike some on this board. I have no axe to grind. I have an un-mortgaged home in 1071, no investment properties and no intent to sell as I will pass the home onto my children in 25 or so years. The only reason I was in contact with the agent was that a member of his firm posted pro labour sentiments on FB and I asked to be removed from their mailing lists.

you get better by the minute

Thank you. Continuous improvement is a personal goal.

Such courage. Its going to be a long journey!

Is Hamilton's main street still emptied? haven't been back to Hamilton in years

"i have no axe to grind" > " a member of his firm posted pro labour sentiments on FB and I asked to be removed"

I hear grinding sounds :)

Probably your teeth as you realize the COL promises of $35 Billion of pre election spending promises will result in more tax, more debt more broken promises or most likely all three achieving a rare trifecta of mistakes for which NZ will pay dearly.

You must be fun at a party

That's funny. How dare they say something pro about a political party. They should be stoned.

Real estate Agents in business dealings should be politically neutral so a justified comment.

Why supporting labour or national have no impact whether they do tthe best they can for customers. To me customers are my focus.

Ex Expat, you know what they say, when you start speaking to yourself. I have a number of medical colleagues who can help.

Good to know offshore is still bailing out specuvestors. Key implication being...not for much longer.

I think those properties in good location in Auckland are still being sold quickly. I’m interested in a three bedrooms townhouse in Remuera within DGZ, texted to the agent One day this week by asking the rental appraisal for the property and the agent replied me it’s just sold that day. It was only on the market for a couple of weeks.

Not true. Two properties on my street (in Parnell) went to Auction in the past 3 weeks and didn't sell. You can't really get better than that for 'good location in Auckland'.

There simply aren't many high price buyers shopping IMO.

I know but if they are in DGZ should be better.

They are in DGZ. Nowhere is selling!

Really? I should have a check for that. I only put “Remuera” as a suburb for search, under 1.5m within DGZ there’re only two properties at the time. Thx

DGZ is a large area including large portions of Mt Eden, Epsom, Newmarket, Grafton and Parnell. Remuera is on the edge of the zone. This website might help you: http://nzschools.tki.org.nz

Thanks for that, I know it as I live in AKL. Just like Remuera a little bit more so I am thinking whether I could buy one in that area also in DGZ. :) Since the market has been cooling down but when you’re really looking for it’s not that easy.

Oh, you're searching under 1.5m – cuts out p much everything.

Parnell has alot of leaky buildings. I know the area well. Were these unsold apartments?

Excerpt on Australia's feverish attitude towards property investing driven by irresponsible bank lending practices. Sounds familiar eh.

"How a train driver can service five million dollars of property on $2,000 a week of positive cash flow comes through the magic of cross-collateralised residential mortgages, where Australian banks allow the unrealised capital gain of one property to secure financing to purchase another property. This unrealised capital gain substitutes for what normally would be a cash deposit. This house of cards is described by LF Economics as a “classic mortgage ponzi finance model”. When the housing market moves south, this unrealised capital gain will rapidly become a loss, and the whole portfolio will become undone. The similarities to underestimation of the probability of default correlation in Collateralised Debt Obligations (CDOs), which led to the Global Financial Crisis, are striking."

"Today 42% of all mortgages in Australia are interest only, because since the average person can’t afford to actually pay for the average house- they only pay off the interest"

http://www.thebull.com.au/premium/a/70753-australia's-economy-is-a-hous…

Our exposure to the Aussie property market really worries me. That market is a disaster waiting to happen. The Aussie govt and regulator will give no support whatsoever to the NZ subs of the Aussie banks, they will be 100% our problem. I am also sure this cross collateralistion approach to LVRs is rife here.

.

Scary as hell. Are deposits in NZ banks safe from an Aussie bank run?

wouldn't be an issue until people start defaulting on paying the interest. Thats a while away, needs high unemployment and higher interest rates. NZRB would drops rates to zero to stop that ever happening.

Yes re defaulting, but, I think the OCRs practical lower bound is well above 0%. Nobody is going to lend New Zealand money for 0.25% if they could earn 1%+ in the US or elsewhere.

I think a possible outcome is OCR stalls around 1%, NZD gets smashed, RBNZ caught between high tradable inflation and a housing bubble bursting.

900,000 Australian households currently in mortgage stress, up 20% since May. 2018 looking at 1 million.

Incomes not covering expenses in 30% of households. if these are right, then it's started.

No they are not. In OZ there's a 200k guarantee per bank. In NZ nothing but a govt imposed "process". They freeze your money, give you enough to live off of until the bank is bailed out or put into liquidation, then they give you what's left over if any. They carry too much risk for an "essential service" for my liking.

This debate isn't about NZ house prices, it's about a credit binge on a massive scale in ANZ.

Answer is NO and worse your deposit account is an unsecured asset not available as set off against any debt and even worse the Covered Bonds issued are secured against the better mortgages so they will not be available for secured or unsecured Bank debt. Should there be a Global GFC mark 2 the destruction of wealth will be like an H Bomb exploding in downtown NY.

The businesses of the Aussie banks in nz are generally conducted via wholly owned nz subsidiaries. Loans and deposits in nz are run via that nz sub. The RB is strict on this as a result of its experience during the GFC: these loans and deposits were at that time run via the “nz branch” of the Aus incorporated parent, such branch being a regulatory device and not having a separate legal personality from the aus incorporated parent. So when the RB came to consider how to give credit support to the nz banking operations of that bank if so required, there was no clear means to give credit support to that aus incorporated parent in a manner which was ringfenced to the nz operations of that bank. In my experience the exception to this nz sub requirement is hedging products which continue to be sold via the “nz branch” structure. But the hedges are probably pretty small beer overall.

So the nz operations of the Aussie banks are ringfenced via their nz subs. There still may be problems if balances in the nz sub are swept to the Aussie parents accounts on a regular basis. This was a problem in the Lehman uk insolvency as end of day balances in London were swept to NY, but this wouldn’t be happening here. And even if the Aussie cos were placed in an insolvency process this would not mean that otherwise solvent nz subs would be subject to that process (surely we would not allow that). So the nz subs are ringfenced from an aus group insolvency process, but equally we need to recognise that we need to pick up the pieces of the nz subs, and the Aussies will not bail us out.

..nope. But your aussie deposits are govt guaranteed. Not so in NZ.

NO.

Bluff. watch the movie 'the Big Short' on Netflix. Tis different, different but same... this time...

It is a great movie! True story.

"Today 42% of all mortgages in Australia are interest only"

Surely that cant be correct....

The story gets worse...64% of investor lending is interest only. IO (interest only) loans had a rate hike recently & regulation imposed to 30% of lending. The IO term is 5-10 years then principle repayments start. From the RBA:

"Interest-only (IO) loans account for a sizeable and growing share of total housing credit in Australia, now representing around 23 per cent of owner-occupier lending and 64 per cent of investor lending (Graph B1)."

Interest only figures are generally in that 30-40% range. I pulled up some quick figures for NZ and of October's new lending 31% was interest only of the total amount borrowed. The figure quoted for Australia seems reasonable, and not unusual.

And here's an interesting turn of events!

I have an IO loan due 15/12. It's 100% OffSet. But when I queried the amount to be debited from maturity date onwards ( for the remaining 20 years) I was told: " You will be debited with the P&I amount as if it was 100% Un-OffSet". Needless to say, I'm, 'in discussions'. Why, would a 100% OffSet loan have to make notional interest payments? If that's right, then I'd suggest many more than me will be surprised at roll-over time!

BW,

Also won't the size of the payments increase substantially from an IO loan to a P&I loan? I estimate about 30-40% increase in payments.

Quite right! I'd expected that as the interest is 'taken care of' via the Offset, that the only amount due was the P. The I being $0 ( as it has been for the first 5 years!). But apparently, not!

(NB: Why do I have a 100% OffSet loan; why don't I 'just pay it off'? Because I learned the hard way, a long time ago - "NEVER give the Bank back it's money unless you absolutely have to ")

BW,

Quite a few borrowers on interest only will potentially come under significant cashflow pressure as a result of this. For those property investors who bought in 2015 / 2016 at LVR's of 70-80%, and given current low rental yields in Auckland, for many property investors this can mean the difference between a property being in positive cashflow which suddenly turns into a property with negative cashflow. What financing options do they have to remain on IO?

1) refinance with another smaller bank, or

2) refinance with a non bank lender

3) pay P&I from current undrawn credit lines

4) sell the property and remove the negative cashflow property from their portfolio

(4) is not as easy as it looks!

Downsizing a portfolio ( removing the 'bad ones;) can't be done in isolation. The Bank will want to see that any equity released gets applied against the remaining properties in the portfolio. Many 'investors' falsely believe that 'they can sell the one they bought back in '75 because it's positively geared', but it doesn't work that way! *( as I'm sure you know).

BW,

Those that borrowed at 80% LVR in 2015 will have their interest only period mature in 2020. About 2 weeks before the interest only maturity date, they will find that surprise that you just found out - that they need to pay P&I on their offset account. That is unless the property prices have fallen significantly before then and the banks ask them for additional collateral before the interest only maturity date - in which case they may be forced to sell when property prices are down.

You are correct and the banks have already started analysing investors total lending portfolios to bring it back in line with our RBNZ lending restrictions (LVR's) mainly. The banks aren't negotiating these days, as all of them are being squeezed by the new rules, hence the reason why the banks haven't been lending out the full 10% allowed to those customers that meet the criteria. They are using the other 5% allowance to meet the RBNZ deadline or face serious fines and sanctions.

TainuiBabe,

1) Do you know if the large banks are actively seeking additional collateral from borrowers to bring them down to the 60% LVR (soon to be 65% LVR as at 1 Jan 2018)? If so, this will put potential additional cash strain on borrowers.

I have heard that if property investors are over the 60% LVR at the moment, that banks are not yet seeking additional collateral. However if an investor sells an investment property, then the bank is retaining all the proceeds until the 60% LVR is being met. As a result many property investors are sitting and waiting as they cannot recycle their equity. Refer - https://www.stuff.co.nz/business/property/98994461/lvr-restrictions-con…

2) do you know at what level of LVR will the the non bank lenders start to seek to reduce LVR's by way of collateral call for a buy and hold property investor?

The non bank lenders have been lending at 80% LVR. So if they lent in March 2017 at 80% LVR, the property price may have fallen 10% which would make that loan potentially 90% LVR. At what stage would the non bank lender decide that a collateral call is required? 90% LVR, 95% LVR? At some point the collateral value may fall short of the loan value and the non bank lender is exposed to potential losses on the loan.

Hi CN. I do know that Banks are assessing "Total Loan Portfolio's" due to an increase in risk amongst other factors such as the RBNZ policy to ensure our banks raise their capital. This means that there is a definate raise in risk profiles across the lending sector. We need to remember that our banks know exactly what the overall picture of their "Asset Ledger" looks like from month to month, because they are required to report their ledgers to the RBNZ on a regular basis, which of course is then used by the RBNZ to identify rising risks across all banks, which leads to policy changes and enforcement. Banks generally don't start forcing it's customers to reduce leverage unless markets change ie prices start dropping, or if their customer starts defaulting. But, because of enforced rules by our RBNZ, the banks are required by law to start looking at those customers most at risk and especially those where "interest only" loans are coming to the next review. We are talking about "Liquidity Levels" changing fast and yes these are the loan portfolio's that carry the most risk and the banks are starting to play hardball. The easiest way for a bank to reduce risk is when a customer sells off a property and yes they apply that proceed of sale across the entire property portfolio, reducing the customer risk dramatically from defaulting, but also taking all of the capital gains. As for at what point does a bank decide to call in a loan, that depends entirely on how many loans have already gone bad or are in the proceeds of turning doubtful which is 3 months of payments made in full. After that the Bank starts formal proceedings towards a mortgagee sale. My understanding is that it only takes 5% of the entire mortgage market to become distressed before all hell breaks loose, given that our banks are only required to hold 13% of the total assets (customer loans) at any one point in time. That is quite an eye opener for most people. But that is how our "Fractional Reserve Banking" system has worked since the 1980's when banking regulations were changed.

Also, non-bank lenders are a completely different kettle of fish. Think of these finance companies who take investors deposits and pay a higher rate of interest to their customers and then make loans to property investors who can't get a loan from a big bank. These property investors are the highest risk of all and the most over-leveraged! That is exactly what happened after the GFC when our Finance Companies collapased and left most of it's investors dirt poor as they lost their entire life's savings! History doesn't repeat but it often rhymes.

TainuiBabe,

FYI, this is the annual report for Homeloans.com.au - the parent of Resimac in NZ. They are massively leveraged - their total assets to equity ratio is 49.1x. A mere 2% of their loans requiring writeoffs would wipe out all of their equity. Bond holders of this company are definitely at risk of bearing some losses ...

And how many unsuspecting investors will loose a portion of their savings via Managed Funds or via High Interest Earning Term Deposits?

This might scare you. $500k interest only at 4.65% = $447 per week. At 5% 30 yr mortg = $617 per week.

Best hope a combination of int rise and forced onto mortg don't happen at once huh.

Dictator,

Here you go

https://www.rba.gov.au/publications/fsr/2017/apr/graphs/graph-b1.html

Also interest only loans are

1) 23% of total loans

2) 16% of total banking assets

What we don't know is the LVR on the interest only loans - if it is low (say 30%), then the banks are well covered in a property price downturn. If it is above 70%-80% then there is obviously less buffer for the banks ...

IO seems as bad here at 40%. Love to know the default rates at maturity of the IO period or circumstances where loans are refinanced or IO term extended. These are great when times are good, foolish when things get bumpy. RB should be putting the breaks on the practice.

What about the possibility of $500 billion in "Liar Loans" in Oz, according to UBS.

I have been seriously thinking about off-loading my Aussie Bank Shares because of these reasons. But at the same time, the stupid Australian government are more than likely to bail out their banks, so I'm tempted to just keep holding them. They have well and truely paid for themselves now anyway, over the past couple of decades. It is interesting to watch events starting to unfold within the banking system in Australia. What happens over there will follow through over here.

TainuiBabe,

If the Australian government bails out their banks, then the existing shareholders of the bank are likely to see their ownership diluted significantly. Look at the examples of Citigroup in the US, and AIG in the US, RBS in the UK during the GFC - all the value was transferred from the previous shareholders to the new shareholders (the government). If I were you, I would be selling all of it.

Thanks CN and yes you are quite right. But most often the share price will come back higher, even if it takes another couple of decades and I still have some time on my side, although I have definately thought of selling up and then buying back in after they get smashed! lol

Realestate.co.nz has conveniently left out the Total Stock graph and Seasonally Adjusted Price graphs from their November statistics. Why?

Because it doesn't support the view that prices are collapsing. There you go:

"The average November asking price across the country sat at $636,719 which is only an 0.8 per cent increase on the previous month."

“... Auckland recorded a two per cent jump in average asking price in November to $956,387 following a comparatively quiet year for the region,”

You can ask what you want for something, that doesn't mean people will pay it. I've got a bridge I can sell you by the way, I'm after $20m for it.

Solidname - Your offer of the bridge reminds me of the infrastructure Simon No Bridges was promising for Northland in the 2015 Northland By Election.

If the asking price had been down instead of up, it would have been mentioned in the headline with a photo of a broken house at the bottom of a precipice

So asking prices not moving much, but sales plummeting. Yep, its a good strong market :)

no one said it was a strong market

all headlines are overly sensationalized in the modern era, it used to be the thing of tabloids but is now unashamedly mainstream....

Speaking of headlines, I have noticed that our media are no longer publishing front page news articles on how much the average Auckland house value has apparently returned to it's owner a paper wealth week by week. It wasn't that long ago that we were all reading articles about Auckland prices increasing at the rate of $700 a day. I need to google the old links to the stories. I get worried when the media goes quiet.

TainuiBabe

Those headlines fuelled prices going higher and the fear of missing out ...

They sure did! I had to live through the daily hype in Auckland and all the conversations around the lunch room. Crazy times!

Friends bought unconditional in Howick "upgrading" from another part of Howick,their old house went to auction on a night with quite a few others...not one offer for their home.

Just sold yesterday by negotiation as they had to sell due to their unconditional purchase...they were listed at 1.5 mill...sold for 1.1 mill...ouch !!

Surely not that's impossible. Houses only get sold for what the sellers ask for. Sensible people hold onto property. This must be fake news.

So that’s good time for some FHB, not need to rush but can get into the property ladder if there’s a good bargain there. :)

$1.1mil and FHB.. does not compute.

Vman, what was the new updated CV on the property?

Sorry,I don't know that.

Vman, If you provide the address of the property sold or link to property on trademe.co.nz, then I can show the CV to you.

Who do they bank with? I'm changing banks! lol

If you say it quickly,four hundred thousand doesn't sound too bad...

That property in DGZ was sold quickly with the price “Just under the asking price” using agent’s words. I guess it’s not 400k less.

Poor old Kermit - https://youtu.be/DbCI68eSNsA

"Just under the asking price..." could meananything in RE speak...

Translation: Sure, I lost $2k on the commission compared to what I would have got at asking, but at least I got a commission to make the next payment on the Audi + negatively geared rentals. Phew.. :)

Got a link vman? I am very curious to see this.

And once the specuvestors get their head around the reality of the loss of tax advantages regardless of when they were bought....watch out.

Refer excerpt from Interest.co.nz article the other day:

"However investors currently offsetting losses from residential investment properties against other income would not be so lucky.

Once the new regulations ring fencing tax losses were introduced, they would apply to all residential property investments regardless of when they were purchased.

So investors who are currently offsetting losses from rental properties against other income such as wages or salaries, had better start working on plan B."

And if everybody's plan 'B' is to cut and run....

It's that time of year... Jingle mail, jingle mail Jingle all the way...

https://en.wiktionary.org/wiki/jingle_mail

I know investors who are cutting and running just because they can't afford to insulate their properties before the deadline. One investor isn't even aware of all the new policies that are about to be enforced, such as no tax relief. Property is looking like a bad deal for the Self-Funded Retirement Property Investors. Shares are looking great again.

A low risk 3.7% term deposit rate is looking more attractive by the day!

International Equities is where i'm putting my money at the moment. Australasian equities will take a pounding once the real estate ponzi collapses, but I'm just not sure if the rot will spread out of Australasia once it sets in. I guess its a case of you put your money down and wait for the roulette wheel to stop.

No Bitcoin then :)

Lol, no, I'm not trying to catch that hot potato.

just like musical chairs, when the music stops you dont want to be THAT person

Or the guy that lent him $200k..

Gave up on term deposits when they went below 5%.

Got a few REITs still yielding close to 6% tax paid. It would take a significant value drop to cover the difference.

Not only that but you can sell and have the cash in your bank in three days.

Seriously, Interest.co should change their slogan from “helping people make financial decisions” to “a bunch of negative, jealous people who haven’t got a clue”!

FFS most of you are just jealous uninformed people who wish they had purchased property and now just go on and on about how these greedy landlords and Asian’s have forced the prices of houses up to more than what you can pay.

Truth is that most of you negatives will never own a property in NZ despite any downturn in prices in Auckland.

Yes I know you will all attack “The Man” but at the end of the day “The Man” is one of those very successful so-called greedy landlords that is providing accommodation for you dreamers!

Go on give me heaps as I am going to go into exile from this site full of mostly no achievers!

For the pro property commenters on here, keep up the good work, but you are wasting your time blogging on here and you will be better off leaving the negatives to it!

I am sorry you find this site upsetting, please do feel free to leave. That’s a “win win”, as they say

Never just leave quietly when you can throw a ridiculous tanty and do the full Miss Piggy flounce. Flick that feather boa, diva!

*shoves another handful of popcorn in mouth*

So off you go TM2. Won't miss you childish comments with the other poster about CHCH going up or down, or how great you were for stacking debt on housing like a junkie getting free candy. Summary zero value or Insite shared with community. But that's a word PIs struggle with isn't it...community.

Most people just don't want to be rent slaves for the rest of their lives. It's a fact that govt and international finance policy has allowed NZ values to ballon well past income of NZ born and raised tax payers thus compromising their right to the security that home ownership brings. I'd go so far as saying it is the biggest failing of the Key and Clarke governments.

Let's put in a climbing context. Camp 1 fans (it's all fluffy unicorns for ever) are pushing for the summit stretched out on debt/cheap oxygen. Camp 2 (maths long broken and gravity will return) are further down the mountain hunkering in with good shelter, and no or little debt building reserves. Ask Rob Hall (RIP) what happens when the storm hits and your out of oxygen with nowhere to hide.

Frostbite (a stalling market) is just the start.

Your name overrates you!

You will come back from exile because as you will get angry about something the government of the day has done that effects the value of Christchurch houses. You should have diversified as Christchurch returns are pathetic and getting worse.

I think you may have been mis-informed. From what I have read amd gathered information from most respondents is that most on this site are already home owners/property investors, but not property speculators. So there would not be many people envious of the people who might have all of their investment eggs in one basket and up to their eyeballs in debt. Try not to judge the wisdom of others and their experience by comparing it to your own.

Read the comments from the start and you will see that they are mostly from people that don’t own property and are jealous of those that do because they can’t personally afford to!

Life is about what YOU do and not about what OTHERS do!

You will be far better off taking care of your own actions and you will achieve far more than moaning about what others have achieved.

Put down the bourbon, Kermit.

Goodness, are you still here? Oh.....

TheMan2 I really hope you and Gordon are happy together, whatever you decide to do with your relationship outside of interest.co.nz. May your passion and chemistry always be as strong. xxx

Ginger, not that fussed on Gordon, so that leaves the way open for you to talk to him doesn’t it?

Gordon you may well be right for a change,

The coalition will make it better for first home buyers in Chch and prices will rise.

Admittedly returns we have are pathetic.

Between 6 and 15 per cent and average about 10 per cent guaranteed plus the obvious capital gains but we don’t sell.

I can see You salivating!

THE MAN 2, since we're well past the peak and any talk of another near term peak is dreamsville, I thought you might benefit from the following Herald article. It's not doomsday prepping, it's logical common sense down to earth stuff:

How to survive a housing market crash (including Christchurch):

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

Enjoy :)

FYI,

Five Steps of a Bubble

Minsky identified five stages in a typical credit cycle – displacement, boom, euphoria, profit taking and panic. Although there are various interpretations of the cycle, the general pattern of bubble activity remains fairly consistent.

1) Displacement: A displacement occurs when investors get enamored by a new paradigm, such as an innovative new technology or interest rates that are historically low. A classic example of displacement is the decline in the federal funds rate from 6.5% in May, 2000, to 1% in June, 2003. Over this three-year period, the interest rate on 30-year fixed-rate mortgages fell by 2.5 percentage points to a historic lows of 5.21%, sowing the seeds for the housing bubble.

2) Boom: Prices rise slowly at first, following a displacement, but then gain momentum as more and more participants enter the market, setting the stage for the boom phase. During this phase, the asset in question attracts widespread media coverage. Fear of missing out on what could be an once-in-a-lifetime opportunity spurs more speculation, drawing an increasing number of participants into the fold.

3) Euphoria: During this phase,caution is thrown to the wind, as asset prices skyrocket. The "greater fool" theory plays out everywhere.

Valuations reach extreme levels during this phase. For example, at the peak of the Japanese real estate bubble in 1989, land in Tokyo sold for as much as $139,000 per square foot, or more than 350-times the value of Manhattan property. After the bubble burst, real estate lost approximately 80% of its inflated value, while stock prices declined by 70%. Similarly, at the height of the internet bubble in March, 2000, the combined value of all technology stocks on the Nasdaq was higher than the GDP of most nations.

During the euphoric phase, new valuation measures and metrics are touted to justify the relentless rise in asset prices.

4) Profit Taking: By this time, the smart money – heeding the warning signs – is generally selling out positions and taking profits. But estimating the exact time when a bubble is due to collapse can be a difficult exercise and extremely hazardous to one's financial health, because, as John Maynard Keynes put it, "the markets can stay irrational longer than you can stay solvent."

Note that it only takes a relatively minor event to prick a bubble, but once it is pricked, the bubble cannot "inflate" again. In August, 2007, for example, French bank BNP Paribas halted withdrawals from three investment funds with substantial exposure to U.S. subprime mortgages because it could not value their holdings. While this development initially rattled financial markets, it was brushed aside over the next couple months, as global equity markets reached new highs. In retrospect, this relatively minor event was indeed a warning sign of the turbulent times to come.

5) Panic: In the panic stage, asset prices reverse course and descend as rapidly as they had ascended. Investors and speculators, faced with margin calls and plunging values of their holdings, now want to liquidate them at any price. As supply overwhelms demand, asset prices slide sharply.

One of the most vivid examples of global panic in financial markets occurred in October 2008, weeks after Lehman Brothers declared bankruptcy and Fannie Mae, Freddie Mac and AIG almost collapsed. The S&P 500 plunged almost 17% that month, its ninth-worst monthly performance. In that single month, global equity markets lost a staggering $9.3 trillion of 22% of their combined market capitalization.

Retired, not sure of your point?

Chch market is not going to crash, totally the opposite.

Chch population is increasing and will be the city of choice in NZ in the future.

THE MAN 2, gawd, for you to suggest Christchurch house prices are going to buck the great fallout = you must have a lot at stake.

Best you step back, take another look at how illogical your statement just sounded.

City of choice in the future? Not for a couple of decades minimum, and likely not at all. Some people I work with are still scared witless from the 87 Stockmarket crash and won't touch equities, but you think an Earthquake which destroyed good chunk of a city, killed ~200people , and still wasn't anywhere near as bad as it could have been is going to disappear from their minds in a few years? Bwhahaha. And that is before the dodgy repaired houses have really started floating to the surface. Chchs own leaky homes fiasco playing out soon in that city near you.

Some of the 'fixed' properties in Christchurch are starting to float to the surface now. I have sympathy for those who bought them, even ones that were advertised 'as is, where is' only to find that the 'repairs' were never really done...

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11931169

No wonder every comment from The Boy is so angry these days. He should have diversified. Putting all ones eggs in one basket is dangerous.

I hear the teenager is looking to close out all his loss making housing and throw whats left at Bitcoin.......

It could work.

Smalltown, if that was aimed at “The Man”I will take the teenager comment as flattery and I will accept that gladly!

Gordon, if you find every comment from me as being angry, then you are living on another planet, but then we probably know that you are not exactly up with the play!

Go The Man! These guys wouldn't have a clue about property and are never likely to. They will always be the complainers, the guys that are too scared to do anything. The property market in NZ will be in a lull or flat for the next 2.5 years and then it will all take off again. Buy now guys while you have a chance.

PKchew, your typo (2.5) is certainly excused. The best possible outcome would be that prices remain flat for the next 25 years. This scenario is far better than the more probable 60% plunge followed by a 25 year recovery path.

It's possible that prices might drift gently downward for your said 2.5 years then collapse.

The way I see it, the house market is cooked - fundamentals are stretched.

The way you see it, fundamentals no longer matter as its different this time. Values are just a number, the skies the limit and 2 million average price for an Auckland dwelling just around the corner.

Dreams like this come at a cost - they ruin finances.

PK Chew. The current state of our housing market says ever so clearly that you so called experts had not a clue.

Home owners are voters. No government wants a bubble to burst on their watch. The current government will let prices fall for as long as they can blame it on the previous government. Then they will deploy the parachutes and enter the market as builders,buyers and financiers to reallocate housing assets . Better houses and cheaper rents for their voters who can't afford to buy and home ownership for their voters and potential voters that can qualify for government assisted mortgages or rent to buy schemes. Housing market begins to recover pre 2020 election. New home owners/voters go to the polls with equity in their pockets. Guess who they vote for.

The govt has no control over this bubble any more. It can pick up the pieces at the bottom, that’s about it. It should keep its powder dry, that’s all it can do.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.