Barfoot & Thompson's auction rooms were busy last week with more than 200 homes up for auction, with sales achieved on exactly a third of them.

The agency marketed 219 homes for sale by auction, and achieved sales on 72 of them giving an overall sales clearance rate of 33%.

The rest were mostly passed in for sale by negotiation, with a small number that were either withdrawn from sale or had their auction postponed.

At the major auctions where 10 or more properties were offered the sales rates ranged from 21% at the Shortland Street auction on March 9, where most of the properties offered were in west Auckland, to 50% at the same venue the previous day, where most of the properties offered where in central Auckland suburbs.

At the Manukau auction the clearance rate was 23% and at the North Shore auction it was 33%.

The biggest auction of the week was the Shortland Street auction on March 7, where 51 properties were scheduled for auction, mostly from central Auckland suburbs such as Remuera, St Heliers, Meadowbank, Epsom, Mt Eden and St Johns, with sales achieved on 35% of them (see the chart below for the sales rates at all of Barfoot's auctions last week).

The details of all the properties offered and the prices achieved on most of those that sold are available on our Residential Auction Results page.

| Date | Venue | Sold | Not Sold | Total | % Sold |

| 5-11 March | On site | 7 | 11 | 18 | 39% |

| 6 March | Manukau | 8 | 27 | 35 | 23% |

| 6 March | Shortland St, CBD | 7 | 11 | 18 | 39% |

| 7 March | Whangarei | 2 | 5 | 7 | 29% |

| 7 March | Shortland St, CBD | 18 | 33 | 51 | 35% |

| 7 March | Pukekohe | 3 | 2 | 5 | 60% |

| 8 March | Shortland St, CBD | 0 | 1 | 1 | 0% |

| 8 March | North Shore | 15 | 31 | 46 | 33% |

| 8 March | Shortland St, CBD | 7 | 7 | 14 | 50% |

| 9 March | Shortland St, CBD | 5 | 19 | 24 | 21% |

| Total | All venues | 72 | 147 | 219 | 33% |

76 Comments

33% is good, it will pick up in spring 2019 :)

wow, there are some who are going to hail the fantastic 33% result..

...some spruikers might even argue that the remaining 67% sold afterwards by negotiation. The basis of which its difficult to prove otherwise! ;-) At 35% clearance rate in Remuera, St Heliers, Meadowbank, Epsom, Mt Eden and St Johns, it is glaringly obvious weakness has spread to the "leafy suburbs".

Some say it is the best time to buy and won't get any cheaper

Don't get me started.

The remaining 67% of the original 100%?

Bozeman, my bad, corrected now :)

The "Housing Crisis" is now so acute that buyers aren't even turning up at auctions.

The Government must step in and force people to attend auctions and bid for houses or face penalties.

Suggest a Buy Line Test where anyone who hasn't been to an auction and bid in the previous 6 months faces a 2 years ban on attending any further auctions.

Haha thats pretty funny.

Talking to a couple of agents over the weekend they both have had a number of cases of people refusing low (in their opinion) offers pre xmas now wanting to accept that offer but being told that buyer has moved on, and then being told they are facing the reality of an even lower price if they sell. Most respond by removing listing and keeping it rented.

I guess the yield will improve with compulsory maintenance and insulation expenses, tax loss fencing, and possible interest rate rises at refinance time...

Also several reports of leverage people being clearly told by their bank that they would not qualify for the loan they currently have in today's lending environment, and to make sure they don't miss any payments. When their term loan expires one hopes prices haven't moved any further downwards, as they will most likely face a margin call from their bank.

Exactly what happened after the '87 crash, mind you agents seeking to "buy" listings did not help the matter.

A margin call from banks...

BigDaddy for leader of National for Progress

Good , now that sales have slumped , we just need prices to do the same .

The reality is that sellers are essentially in 2 catagories ...........

Speculators with deep pockets

or

Desperate due to debt , divorce , death , or departure .

If speculators leave the market , you are only left with the desperate , and thats when prices will come down.

Prices will not come down unless sellers are prepaired to sell for less.

Why do you need deep pockets ? nothing changes unless interest rates start to rise and your over leveraged. if you own your family home then your do not need to sell it unless there are rate rises and/or you loose your job.Kiwis buy and sell houses far too frequently as it is. Every house arround me as be bought and sold up to FOUR times while I have been living there for 15 years.

I don't understand why people on here suddenly think the bottom is going to fall out of the market ?

People will simply not sell unless they have to and will stay put. Those with a brain will realize if they stay put for 10 years the market will turn around again anyway.

because the Queen Bee (the national party) has been dethroned!!!

the speculators dont have any honey left to suck on...

Spruikers call for return of ponytail politics

Sales were always buoyant when ponytails were free to pull

Sometimes life dictates that you cannot sit still for 10 years. Perhaps a job offer in a different region/country, perhaps too many children for the current house, perhaps a divorce, perhaps wanting/needing to downsize. Expecting all home owners to form up as one and refuse to sell is unrealistic.

realestate.co.nz has 365 properties listed with a "change in circumstances"

"change in circumstances" - the latest fool's guide to attracting unwanted attention as to the vendors original intention. Penalty payments on unpaid CGT (courtesy of IRD Investigation Unit)

'k until recently "investors" have been making up c.40% of the property purchases every month, 50% of these have been on interest only mortgages. There is a massive number of them, enough to cause a shockwave.. That's 20% of all the properties sold in a precarious position from the start, sans capital gains, that puts them in an even more parlous state, fold or hold at this point?

Interest only to be converted into P&I, no capital gains, extended bright line test, rate increases, no more negative gearing, fewer bigger fools, that equity that they used to buy those over-priced houses, looks like an ouch moment to me.

Guess the market is finally starting to turn

I do hope it will as I have some nice foreign funds to park

"Prices will not come down unless sellers are prepaired to sell for less"

Unfortunately, it takes two to tango in Real Estate, sellers can ask whatever they like but without buyers, it'll be as good as t-ts on a bull !

I think there’s a misconception that sellers don’t actually need to sell. When a property fails to sell it’s just “oh well maybe next time” and life carries on as normal.

HODL?

Ask the people of Tokyo how that's working out for them.

This is why government will not put the overseas buyers ban / restrictions as that would slow down the sales even more and they do not want to have 'a problem' where actually market crashes.

There is only limited amount of money people can spend on houses. We had that 'untapped' money from China - which suited everyone (apart of regular , hard working Kiwis). Now this is gone.... interest rates are going lower so people can actually afford to buy - and the idea is that people will take mortgages and buy - so banks can profit...

you are wrong.. they will put it thru, but in a way that will encourage new houses built.. they will amend the rules a little, like having to sell within 12 months of being built

Foreign buyers were less than 3%. There will be no effect :)

LOL

Sorry still don't see a problem until we have more people leaving NZ than are arriving.

Quite a few things needs to change before we get a massive market correction and thrown in with that we now have a new Labour government and the the last thing they want is a market crash on their watch.

Sure its going to be an interesting year and anything can happen. I would put my money on an overseas event triggering a collapse if there is to be one because this will then run outside everyone control and we will just have to suck it up.

What's the proportion of low-skilled immigration - who won't buy a house, can't buy a house and will live multiple occupants to a house, vs skilled immigrants who may in a few years be able to buy a house?

I agree with an overseas event having hideous ramifications, that will exacerbate rather than stimulate the problem, the issues are already here without that in play.

I think declines will be mild-moderate, I don't think there will be a crash unless there is a major international economic crisis. Which of course is quite possible in the next 3-5 years under the law of averages

Market reset. The longer Lab.NF,Grn avoid it the more blame they will take as they become a part of maintaining the ponzi. Best to get it done early then the blame clearly falls where the policy actually lies (last govt).

End of the day does the GOVT represent the interest of tax paying kiwis, or does it represent the interests of overseas property speculators and bank shareholders...?

I agree! who gives a toss about rich foreigners.

Foreign currency keeps the NZ e Con omy afloat

Where do you think your mortgage funds are coming from ?

Mortgages are bringing money into the economy. It’s great. If we can continue to grow the housing market then people will continue to get bigger mortgages and the economy will boom. Bring on negative interest rates, then we get paid to import mortgage documents.

NZDan I’m sure that plan of yours will fly National

@Carlos, would a rollback of Dodd Frank be considered a significant global event? - That's the legislation that stress-tested the banks ability to survive another GFC type event, that prevented risky lending and was supposed to prevent another Wall St. bailout by the tax payers . https://www.washingtonpost.com/news/powerpost/paloma/the-finance-202/20…

WallSt getting their stooge Trump to strip DoddFrank of teeth is laughable considering it mostly was put together by bank lobbyists Only one organized public watchdog had real input

Glass-Steagall should never have been revoked it served the country well and was more concise albeit because it was enacted back in 1932.

Derivatives are the problem & WallSt loves them because the returns are like 500% and you can always package & onsell the junk.

Pot scrubbers, petrol attendants, fruit pickers and truck drivers all make over 200K a year, they will be buying the average priced 900K Auckland houses.

They might as well buy 2 they are so cheap.

Swapacrate sarcastically states the sad current paradigm

Worse if you consider the fact NZs minimum wage of $15:75per hr is double USA minimum wage $7:25per hr

and yet it’s cheaper to live in Nth America

I think the current NZ govt are far more aware of the lack of spending power of the wage & salary earners of NZ

If a real estate salesperson will receive a financial benefit when offering one sales method versus another then they are legally required to disclose it to the client! Most real estate companies offer an internal incentive in their pay structure that means pitching an auction will see them receive a greater share of the commission if another salesperson on the team has the buyer. This is why they push auctions so hard at time of listing - watch out for that and ask them - will you personally receive a larger cut of the fee if we list as an auction vs a negotiation or asking price. The current climate is not conducive to auction at least in Auckland.

Agreed. Auction is all about forcing seller to accept less in the pressure environment. Watched it up close in the GFC. Agent/House wins kind of like a casino.

estateagent,

In your opinion, what would be the expected fixed financial cost to the vendor of holding an auction?

i.e a cost that they will incur regardless of a sale or not.

This is the first important point made by Solidname, most of the immigrants coming here are not wealthy enough to buy a million dollar house. How would they even meet an average banks lending criteria? They have no address history, are unlikely enrolled to vote and so on, all these things the bankster-credit-algos like to see before they say yes.

To be honest I don't believe there is a shortage in housing.....there is a shortage in affordability. These are two separate issues and one of those issues will simply not be solved by building more houses. If we have a shortage of housing in Auckland than over the last 15 years or so, rents should have increased at roughly the same rate as capital values. But they have not, not even close. Given that, it is surely the case that the demand is in ownership and not in housing itself.

Real Estate booms are always associated with cheap credit. It is the price of credit that matters ultimately and overall. NZ interest rates have been in bear for the last 40 odd years......but they will break out, and not because of (insert convenient statistic / revisionist news blurb here) but because people drive the market, people are not rational, this has not changed, and what has happened before will happen again.

This ties to Boatmans point, not only are sellers of only two groups so are buyers. Buyers now are wealthy people of whatever description or nationality or people who think they are missing out and desperate to get in. They have to be wealthy to be able to afford to buy at the current levels, or desperate enough to overlook the inherent dangers of leveraging yourself so highly. Even with interest rates at unprecedented historic lows, if you are buying the average Auckland house on the average Auckland income.........it's a stretch to be able to sustain those prices and debt levels. This explains why prices are holding up in the leafy suburbs as that's where wealthier people want to buy anyway and can probably still afford to buy. For now.

I will put my hand up now and say I have been a property bear for the last 10 years. I have seen blips come and go, but have been reluctant to say this is the crash and I still am as timing any market is virtually impossible. But what has made me bearish for the last 10 years, as a student of value investing, is the simple fact that NZ houses are very expensive. You can use any measure you like, ounces of gold to buy a house, barrels of oil, % of weekly outgoings, or multiples of income. By any measure NZ houses are expensive in historic terms. And as everything eventually reverts to mean (and in a crash usually goes right past it) then at some stage, you can be certain there will be a correction. There will be a crash......or a massive surge in all other asset classes to catch up with houses.....something to return balance. But every other time, it has been a crash, so why would it be different this time? There is no new paradigm here (there seldom ever is).

And forget a soft landing, or a plateu-ing. This also never happens and won't happen this time. I see a 50-60% correction to get back to mean, and then another 10-15% past mean reversion, because that's what typically happens in a crash.

Those points aside, I will say this correction does feel different. We have had a final blow off phase in 2015/2016 when things went a little crazy, on an already impressive run. We also have the tallest apartment building in Auckland being built (the pacifica), government and council finally moving on building more affordable housing/re-zoning/supposedly loosening planning obstacles (government is always late to every party), and the amount of cranes in the cbd has dropped quite significantly, in the last 6 months. These three are quite strong anecdotal signals of a top. Couple with the drop in activity, increase in market supply and I think this is finally the start of the big one. But as a bear I need to acknowledge my confirmation bias and you should all take everything I have said with a pinch of salt! I am trying not to see what I expect to see, but I am just as bad as every other human.....we are all generally poor investors!

I am a fearful person and it means I have missed out on the best gains in the property bubble. But I believe it is better to protect yourself from loss then follow the trend and speculate on the bigger fool. In the long term all that matters is price, and if you make an investment in something that is expensive then it is very difficult to make money from that.

At the moment there is a stand off between buyers and sellers. Something will break and one side will be right and the other side will be wrong. On the one hand markets can be irrational longer than one can be solvent, on the other hand every asset class in history has reverted to mean after any strong run.

Good luck everyone, which ever side of the coin you are on.

Are we getting to the point where spruikers are seeing dark clouds or not ?

Denature do not fret there will be opportunities

I don't fret good sir. There are always more oppurtunities and with investing FOMO and impatience are always your worst enemies. When house prices have dropped to the point where rental yields are 12% plus then this bear will be bullish and I will hopefully have some money to by some property.

If anything is still standing in this funny little land of ours!!

Brilliant – well composed and thoughtful comment.

Ultimately, you may be right or wrong – but you’ve thrown your heart and soul into it.

I generally agree with everything you say – however a 50-60% correction to get back to mean, and then another 10-15% - although mathematically it maybe should happen, it simply won’t – it’s not the US and non-recourse loans - helicopters et al.

What about all the mums and dads using equity in their own homes/property portfolios to get their kids into houses?

I would NEVER fund my child into their own property in this market! I actually feel sorry for those parents who drank from the punchbowl. I imagine their hangover will be long and blinding.

Yeah ditto. Some real pain on the way for some of these families, methinks

Assuming my children were at that point e.g. starting a family and I had the means (sufficient left to see out my days) I would help them no matter where the market was and likely will when the time comes. The only thing I need to work out is how to make sure the money stays in my blood line, probably through some form of loan.

Ex Expat, from what I've witnessed (in my extended family), loans are a bad idea. When it comes to kids, money can only be a gift that you never expect repayment. In instances such as this, me thinks it just pays to close the eyes and trust the kids have partnered up into solid lifelong partnerships.

At least that's my opinion.....

You would fund your kids if you had enough money, its a no brainer because it completely changes their lives and puts then 15 years ahead of the curve. Thats what my parents did and I could retire at age 50. What is more important is the nature of your kids, do they work hard and are they going to keep the money in property for the long run or will they just take the money and p#ss it up the wall ? thats the criteria I would be looking at.

Why thank you

Thanks you for your kind words custard.

I don't use much maths for that calculation, mostly it's history and human psychology.

I am pretty sure no serious thinker believes in man or women as the rational economic actor, we are all just bumbling cavemen with a lot of instincts that don't help us much today. It will take thousands of generations for evolution to select that out.

In the meantime the best we can do is try and recognise these failures in us all, not be too precious about being wrong, be humble when we are right (because being right can be a fluke sometimes) and help people when we can. And invest accordingly.

It may be that we don't have NINJA loans here, or non-recourse etc, but I think what we will see is some different configuration of factors that will lead to the correction I outlined above. I can't predict what the are, I doubt anyone can but thats chaos theory. The market will find a way to correct, that's what always happens. And unless human behaviour changes that will not change. In these cases history and human behaviour always trump maths.

We will see, but for all the people who have made good money on this impressive bull run, well done, but if I was in your position I would be taking money off the real eastate table.

I would desperately like to own my own home but cannot afford current prices. I would like prices to fall back significantly but am skeptical that they will. It seemed back in 2008 that they should fall 20%, they didn't and I strongly regret not buying at the time

Nice post denature. I find this interesting. Our banks can either borrow from us via deposits, or from the wholesale banking system. Wholesale banking rates have been going up steadily since their 2014 low of 0.5% to their current 2.5% or thereabouts.

https://fred.stlouisfed.org/series/USD12MD156N

Perhaps we are too focussed on our local reserve bank and overlook the more powerful global forces at play.

Thanks Roger.

I think you are correct. Ultimately I think we give central banks far to much credit either for their knowledge of what is happening or there ability to control it. It seems the central bank model is of an economy as a machine, if you pull lever 1 it increses flow to chamber three and pressure is release in valve 7. We all know that the economy does not work like that. It's why it's so ridiculous when governments say they want to build the next silicone valley. How, they didn't build the first one!!! A bunch of circumstances wound together to form silicone valley, no one guided it. Governments provide an illusion of control.

We have all heard of the bond vigilantes....they have been quiet for a long time.....I guess enjoying their bull run. But whether they are actual people, or some aspect of the system regulating itself, that we do not yet understand, it really doesn't matter as the results are the same. In the US 10 year, I think we can see they are starting to get restless.

As people we all have such short memories. How many people owning houses or investing have experienced interest rates at 15 or 20%? Rates of that magnitude are utterly unremarkable, but I wonder how many investors out there at the moment realize that? Yet here we are living in the most unusual market environment, in history potentially (I have not seen a chart that shows negative interest rates ever!) and yet we seem to all think this is normal and will be sustained. Somehow. We will get a nice flat plateu and everything will be honky dory. I would say that not only the market, but the universe itself begs to differ. In trying to maintain stabilty we move inexorably to our minsky moment.

It's interesting that you mention lending from wholesale deposits Roger. I bank with TSB as they actually do fund a lot of their borrowing from their deposits, and I think they are a relatively safe bank, although I find their aggressively low loan rates at the moment a little disconcerting as a cusomter who banks with them for safety. But most of the banking is controlled by the big four Austrlian banks directly or via proxy. Signifincant parts of these are then held by banks such as JP Morgan / HSBC / Citigroup. Any of these names ring bells from the GFC? And do we believe these banks are operating with low leverages and largely acting with deposit funding? Have they become smaller and safer, or are they just too bigger to fail?

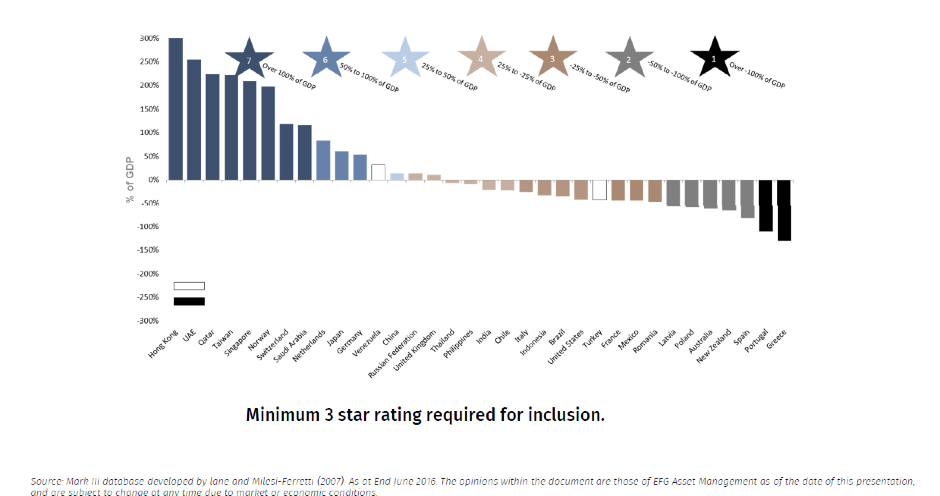

For anyone who thinks NZ is ok because our public debt is relatively low, I offer you this chart (I hope the link works because I think this is a vital chart for all New Zealanders to see and think about) https://www.southbankresearch.com/wp-content/uploads/sites/9/2018/01/1T…

This chart represent the "net foreign assets as a % of GDP" that is goverement sector, corporate sector and household sector assets held overseas less the value of domestic assets owned by foreigners. As you can see New Zealand is well and truly with the PIGS by this measure.

Personally I find this chart very sobering. We are already very much at the behest of what happens in other nations.

Be very careful everyone. Especially with debt and especially now. We have been too flippant with debt for too long and I believe it will come and bite us, in the not too distant future. We have spent too much of our future earnings and eventually the bill will come.

{kind=link}

Yes and no, our RB sets the OCR based on the state of the NZ economy (have I missed something here?) and what the RB wants to do to it. Just what the external wholesale rate is is moot for our economy in terms of the OCR, which means life could get interesting.

I would beg to differ, Steven.

Firstly the OCR sets its rate on what it "thinks" is happening. To be honest Steve, although I know virtually nothing about you, I am pretty confident your guess on what will happen tomorrow is as good as mine or the OCR's. Predicting the future is impossible. Does anyone trust a weather prediction three days out? Me neither, so why do we think the Wizards of Oz can predict what will happen over the next month, let alone quarter, or year?

If you look at the chart in my post above, you will see that net, around 75% of our assets are controlled by foreign interests. I expect a lot of that is represented in mortgage borrowings. If the circumstances in their regions change then they may be forced to sell these assets, or increase the charge (interest) on them to cover an increase in their risk or charge (interest). They may also have borrowed against these assets, which means we have a further step removed of somebody connected to us. Perhaps some of these holdings have been chopped up and collateralized........is any of this starting to sound familiar? Supposedly spreading the risk to make things safer, but actually concentrating it and making the system weaker. We could have a sudden sell off in these foreign owned assets or an increase in the cost of maintaining them, either way interest rates would increase. And this could be caused by a foreign owner 5 or 6 times removed from the actual physical asset. And without the OCR raising a finger or having any idea what the hell is going on.

Note I am completely ignoring any currency problems. A devaluation of the dollar, whether relative or actual, will force the price of imports up. Then the OCR may be forced to raise rates to reduce inflation or protect a run on our hghly traded currency.

All these things could be caused by a change in the external wholesale rate, particularly in the US, but possibly in China, Japan, Europe as well. It depends how much of those foreign assets are owned by whom. I don't know the answer to that Steven, but I think we should probably be thinking about these things, and we should certainly be borrowing less in this country until our debt is at more sustainable levels.

Some say it's due to the Chinese Year of the Dog coinciding with the astronomers dream of BCG-2018 eclipse. Some say it's due to cyclone Hola failing to continue a low interest Ola. But one thing you can confidently feel are that like an obvious assets-commodities bowel irregularity...

"2018 YEAR OF THE DOGS"!

Still crap clearance rates, pressure is rising

Still poor clearance rates

Sounds so much better

Expert predictions are that within 30 years Auckland will have as many people as Sydney - as reported recently in The Herald.

That means far more houses need to be built in Auckland (and urgently) or the prices of the existing stock of houses will go through the roof.

Those people who think that Auckland house prices have reached unsustainable levels need to think again.

I reckon we've seen nothing yet........ (Mark my words.)

TTP

I truly and sincerely hope that we do not allow such a stupid population increase. That would just be absolutely ridiculous.

Phew – thankfully they’re just “expert predictions” so no need for concern…..

The difference in Sydney is you can earn more money. How do people get loans if they do not make enough money.

Houses can have average cost of 4 million, but if no one can afford them and banks dont lend, then how do house prices increase. All well and good saying house prices will increase, but how.

How will Auckland grow ?

It has a population of 1.5 million and $6Billion in super city debt which will never be repaid and remain a noose around Auckland restricting its infrastructure build & thus its growth

Note where the current govt plans it’s affordable housing to go

Sydney is not sitting still for the next 30 yrs either

have these same experts factored in that it will cause Auckland to grind to a halt, we dont have the mass transport setup to handle that many people and all that will happen is more and more cars and costs and down time for people and businesses will increase

Traffic engineers now considered that the morning peak went from 5am to 10am, while the afternoon peak stretched from 2pm to 8pm

https://www.stuff.co.nz/business/78241308/43-000-more-cars-on-Aucklands…

The point you are missing here is that current price levels are unsustainable for the industry that is based there. If teachers can't afford houses then blue collar industry (still large in Auckland) certainly can't. What we are seeing in Auckland prices is pure bubble - proved by the fact that prices are so much out of kilter with rentals.

Prices are also massively higher than building costs, which is currently disguised by high land prices. Auckland may well grow, but only after the housing market returns to some resemblance of normality.

Mark your words that in 30 years time ........TTP you''re drawing a pretty long bow there.

Staying back in 2018 the Auckland RE market is looking pretty damn weak

Anyone else got this scene playing in their head https://www.youtube.com/watch?v=gXY9TuuwyL8

The collapse of CBL is actually a major leading indicator of a big "stress event" and yet nobody is talking about it. How many deposits have been lost? The collapse of CBL NZ has already brought down 2 off-shoot companies in Australia within days. If a company that buys sub-prime mortgages (LMI) from the banks books and re-bundles these and sells them off to investors, and then goes broke, what will happen to our banks when interest rates start rising and more customers start to default on their loans? The short answer: Banks start to fail.

It really doesn't get more abysmal than a 33% clearance rate at the ABSOLUTE PEAK of the selling season.

The resident Lemon Party will be squawking that now is a great time to buy, while sitting on their hands, for they know that DOOM and GLOOM is on the menu all winter long.

Why Brock Landers you fascination

I cannot understand why vendors are still accepting real estate blah that auctions are the way to go - its past time we went to putting prices on property for sale and letting the any prospective purchasers have a more transparent process without racking up auction fees and promoting the real estate agents. Vendors to have power to make this choice- auction is easier for the agent.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.