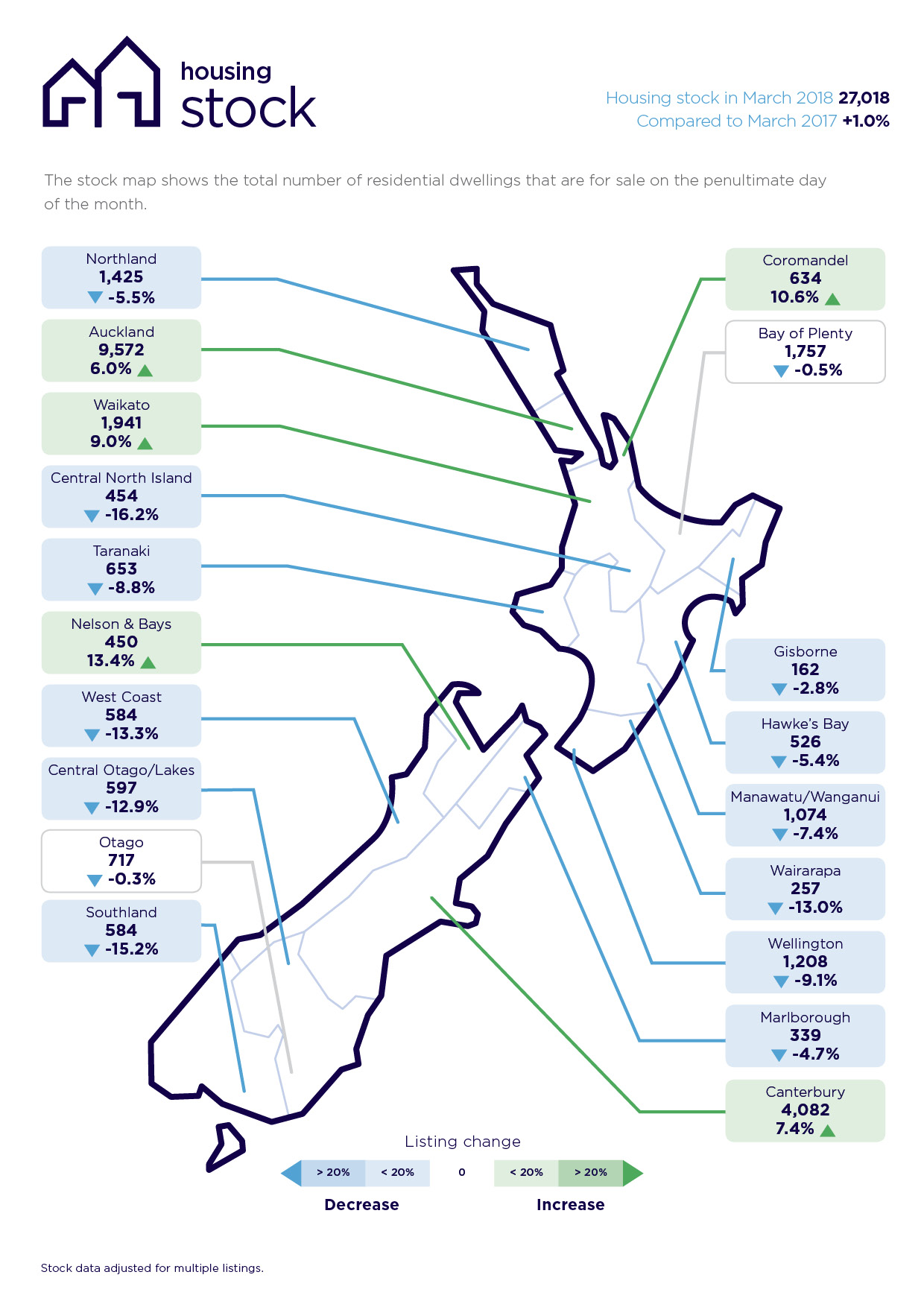

Auckland became even more of a buyer's market in March, with the number of homes available for sale in the region at a six year high.

Realestate.co.nz said it had 9572 Auckland homes available for sale on the website at the end of March.

That was up 6% compared to the 9026 Auckland homes available for sale at the end of March last year, and up a whopping 49% compared to the 6443 homes available for sale in March 2016.

The March 2018 figure was the highest it has been for the month of March since 2012, and was particularly significant because the number of new Auckland listings and their average asking price were both down in March.

Realestate.co.nz recorded 4171 new Auckland listings in March, down from 4700 in March last year, but up from the 3902 recorded in March 2016.

The average asking price in Auckland also dropped back from its record high of $994,175 set in February this year to $963,888 in March, which was slightly lower than the March 2017 average of $969,532.

The figures do not paint a pretty picture for the Auckland market as the peak summer selling season draws to a close and the market prepares to hunker down as it heads towards winter.

There were also substantial increases in the number of homes for sale in the Waikato and Canterbury.

In the Waikato, Realestate.co.nz recorded 1941 homes for sale at the end of March compared to 1780 in March last year and 1687 in March 2016.

In Canterbury there were 4082 homes for sale at the end of March, the highest it has been for the month of March since 2011.

However the Wellington Region went against the trend, with 1208 homes for sale at the end of March compared to 1330 in March last year and 1295 in March 2016, suggesting the market in the region remains tight.

And the band continues to play in the regions.

According to Realesate.co.nz, the top 10 regions with the largest increases in asking prices did not include any of the main centres.

"In the regions where the market is lively, it represents choice for both buyers and sellers, wherever they are on the property ladder," Realestate.co.nz spokesperson Vanessa Taylor said.

"In some regions such as Auckland, a fall in asking prices could result in renewed opportunities for buyers, including those who want to move up the property ladder," she said.

101 Comments

What is remarkable is that the inventory is rising, but Auckland prices seem resilient to a fall. I am sure that they will decline, but it seems that with each passing month they continue to defy gravity.

Until sellers become much more realistic, the inventory will just pile.

The longer the buyer wait the better

Paenski, I sure am happy I waited and didn't buy a house in Ponsonby for $300k, 20 years ago

Yvil, WARNING!, in this instance, eyes to the front! By assuming uninterruptible capital gains, you'll trip up, landing face down in a deep pit containing disillusioned debt junkies!

Good for you if you bought it from the time where the property is still meant as a home and not a mode of investment.

And I will feel pity for you if you buy a house in Ponsonby now. Time will tell, but I'll stick to the basic principle of supply and demand for now. #HODL

"I'll stick to the basic principle of supply and demand for now."

.

I have news for you then, there's more demand than supply in Auckland,

(but you couldn't know that, it's a close guarded secret that there is massive immigration and not enough houses in Auckland)

Oh you mean the old news, here is the latest one. I got you covered: http://www.scoop.co.nz/stories/PO1803/S00388/net-migration-predicted-to…

Although I base my thoughts on facts and not on predictions and surveys. I am hopefully waiting for the actual announcement plan of the current Government to release a tighter visa approval. Until then, I hope your "proudful assets" are not one of those in the inventory.

Quote from your own link:

"A new report from the Ministry of Business, Innovation and Employment (MBIE) is predicting that net migration will fall to around 65,000 in June next year compared with the June 2017 figure of 72,300"

Com'on, are you really saying immigration is low and backing it up with the above link? Really?

Yvil, high immigration is a meaningless argument in favour of increased house prices if the inventory on arrival is already severely unaffordable by world standards.

Don't you get it yet? THERE IS A GROWING SURPLUS OF UNAFFORDABLE HOUSES - DUH!

well said

high inventories = a lot of supply

low sales volumes = little demand

There's 22k ghost houses knocking around Auckland at the moment, (that excludes residents who weren't there for census) I'll wager that number will increase come census publication time. I'm going to go for 30k as a number, Labour have promised 100k houses, there'll be 30k right there that are being "banked", nearly a third of the entire promise, owned by about 10k people, Gareth Morgan's got 6, "use it or lose it" time. 10,000 disgruntled parasites vs 60,000 happy new voters, sounds pretty winning to me.

Bring in squatters rights for the win! If in G Morgans make sure you bring lots of cats!

Softening prices would actually indicate there is more supply than demand.

Nobody in their right mind thinks the prices being asked are worth it anymore. Not without the capital gains.

This market will remain flacid for a long time to come.

Hehehehehehe flaccid.

Good to see I’m not the only mid to late fourties schoolboy here

Hi Brock Landers,

Where's the evidence of softening prices?

Auckland house prices are, in fact, holding remarkably well.

Sure, I'd like to buy a well-located Auckland property at a heavily discounted price. Yippee! But like most other people, I'm not kidding myself that it's going to happen.

TTP

The number of people needing accommodation is different for the demand for house purchase. Demand for purchase is strongly affected by price, access to credit, and sentiment.

Yes and no.

Much of Auckland's population growth in the last few years has been from students. They are often cramming into city apartments or doing homestays. That takes the edge off the demand side

The vendors still do not have to sell as they properties are often rented paying for itself. Many crappy houses for sale with all the issues will see prices lowering first...

Indeed! I've stayed in four different countries more than a year. It is a surprise to me that CRAPPY and UGLY house properties asking price are way higher than it's supposed value across NZ

Golden Homes for 3 million, its like the Twilight Zone.

The reality is that vendors don't get sufficient return to make renting an attractive option. A property with $650 pw rental in Auckland would probably have a CV of a $million; whereas in wellington a property with same rental income would be a sale price of around $750k. If you are funding a mortgage you are needing to top up the rental each week

.

Last year paid 137k and getting 380 per week and 200k getting 470 per week, in Chch. no insurance at the time!

Previous year 146k and $400 per week. Full insurance in existence.

2 years ago 380k and returned 560 per week.

Housing investment is all about buying right and being positively geared and the capital gains for investors are just a bonus but only if you ever sell.

Why would investors sell,if they are pulling in double digit returns?

Hi TM2 I saw this quote in an article I read

"only 35 per cent of those renting through property managers rated their managers' service highly, compared with 54 per cent of those renting directly from landlords who rated their landlords' service highly." I hope 100 percent of my tenants would rate my property mgmt well and I dare say you would also be the same. It shows we are on the right track self managing.

Renters get poor deal with property managers

http://nzh.tw/12025742

Housework’s, yes we self manage because we can look after both the tenants and our assets better than what someone else that hasn’t got a financial interest in it!

We recently had a management company obtain a tenant for us just after Xmas as a casual let, because they were more local than where we were and the cost was on,y one weeks rent anyway.

Yes they obtained the tenant and we did the relative checks and they checked out fine and they were From Auckland, coming down for a better lifestyle.

Thing is that the paperwork and other bits was very substandard compared to what we do!

People use management companies because they don’t want the hassle but if you want the best job done and you have the time then self management is the way to go!

You sound like you are really on to doing things well and right. I tend to rush around anything "urgent" :)

We do consider that we are very professional and don’t take short cuts or it will come back to bite you.

We are forever learning how to do things better.

Fortunately we have never lost money from a tenant and we have had a helluva lot, because we always do the checks properly although it is never a guarantee.

Providing you get the 4 weeks bond and do the quarterly checks and run it professionally then you should not get caught out!

Yes tenancy Maybe once every few years but providing you have done everything right and documented then the landlord will always win.

We do consider that we are very professional and don’t take short cuts or it will come back to bite you.

We are forever learning how to do things better.

Mowing the lawns will keep you sprightly and a little extra money for a set of happy meals at McDs.

Sometimes don't even get my bonds lodged which I realise is a huge no no although I know I'm not alone in this transgression. It can be expensive if pinged touch wood.

Its not just a "huge no no", its illegal. If that's your attitude about something as simple as lodging a bond it makes me wonder what other legal requirements you're avoiding. By this statement alone you're a shining example of why there needs to be better protections for tenants and harsher penalties for transgressors.

Hi Pragmatist,

Sorry - but you're unconvincing.

Well located houses in Auckland sell for a lot more that $1.0million. That amount doesn't buy much in Auckland these days.......

Suggest you take the time to acquaint yourself with the Auckland market.

TTP

So you're saying yields are even worse than the ~2.5-3% (before expenses) that pragmatist is indicating?

.

The cracks are starting to appear, its just a matter of time now

The extension of the bright line test to 5 years might be the straw that breaks the camel's back

Yep this is exactly what happens just before the market declines to more realistic and affordable prices. Once those properties still there for another six months to a year prices will soon start to slide.

I heard an "interesting" take on this stat on the "news" this morning. They said it was harder for buyers due to the number of new listings being down in Auckland. Um, I think they forgot to read the total listings stat.

MisterB, they conveniently omitted the word "affordable" listings which again points to there being little support from buyers at current levels......

A fresh wave of listings come spring will further pressure prices. Price falls are an encouraging sign for FHBs who are saving hard, earning interest while all those debt junkies out there pay it. There is no hurry ;-)

Same broken useless record, but last consumer confidence says it all:

"A net 39 percent of those surveyed said it was a good time to buy a major household item, down from 40 percent in February, which ANZ said suggests robust durables spending.

Respondents expected house prices to rise 3.5 percent per year over the next two years, up from 3.1 percent the previous month, with Wellingtonians expecting house prices to rise 4.4 percent. Prices in general are expected to rise 3.4 percent per year over the next two years, from 3.4 percent in February."

http://www.sharechat.co.nz/article/73966025/nz-consumer-confidence-stea…

Most people here seem to be shouting in the wrong valley ...lol

ANZ Survey over the actual stat? Who's fooling who?

.

Echo Bird, with 1002 cherry picked respondents from only ANZ knows where, it's a safe bet there weren't many farmers amongst the responders. Just weeks ago you commented now's a good buying opportunity and several properties were on your shopping list. How many have you bagged thus far?

Expectations and Reality are not the same thing. Just like eveyone wears their own personal filter that reflects their upbringing, religion and socio economic status, even their own culture and ethnicity. So tell me again why house prices are going to rise?

Ask the people who responded to the survey, everyone must have his/her own reason as you say. However, they all agree that it will result to higher prices.

Needless to go through the fundamentals again, we have been repeating that for ages and nothing has changed thus far ( in fact its getting worse).

So far prices everywhere are rising and that is the proof in the housing pudding !

Maybe read the survey: https://www.anz.co.nz/resources/0/a/0af49d05-6a83-4051-910b-3b277682d55… (Question 7)

59% expected prices to rise... that is far from "they all agree" and well down on the 81% equivalent result in

June 2016 and 69% in March 2017. The 3.4% figure is ONLY those that said 'up'.

I am not sure why they don't net that off like they do the other questions... the net would be 43%. In June 2016 it was 74%. March 2017 it was 57%

Hi Eco Bird,

Many (most?) of the doom and gloom merchants (DGM) will never own their own home.......

They simply don't understand the way things work. (But that's no fault of ours.)

TTP

Many of the dgm-ers would be too indecisive. Buying counter cyclical when the market is on the back foot is Always best and is richly rewarding.

Counter-cyclical... that would be selling when there is still a positive perception of the market. To be a bit more technical, one should sell when the sentiment is still positive but decreasing (maybe close to crossing to negative sentiment), and buy when sentiment is highly negative but increasing positivity.

In other words, one should have bought around 2000, and sell about now. If one was in the US, the buy date was similar, but there was a clear sell date of 2006, and a new buy date of early 2010.

Some of you have called me a DGM here in the past. My experience suggests that I am instead either an astute real estate market sentiment evaluator, or really lucky. I bought my first house in 1987, and sold it in 2006 (this was in US). For the places that I lived, the best possible financial outcome after this had me renting for a decade. A bit more than two years ago I purchased as it became better to own than rent here in Hawkes Bay. I have successfully bought and sold at the respective peaks and valleys in the real estate market, in both the US and here in NZ. But, maybe I've just been lucky, and my market evaluations were more luck than skill!

I did get in a couple heated discussions with real estate agents when I put forward my conclusions about the upcoming decline in the market, and they countered that the prices at the time refuted my conclusions. My stated opinion from last year was that the overall market in Auckland became a poor investment around a year ago due to poor return potential. I still see nothing to change my view, and in fact, it seems that the signals are becoming more obvious.

I am not quite sure why you think that people who want house prices to be lower are doom and gloom merchants.

I would suggest that for everyday young kiwis continued escalation of our ridiculously high house prices is indeed doom and gloom.

I guess doom and gloom is in the eye of the beholder. Like you, I think it's doom and gloom to have the basic need of housing completely unattainable for everyday folk. The long term outlook for Auckland is terrible unless the income v debt re-balances... attracting and keeping teachers, nurses, service workers etc is already verging on impossible.

Thats a total exaggeration housing is not completely unattainable. The opposite is true in my opinion you just have to want it enough and that has Always been the case. I have seen and read many recent examples of young people buying first auckland home despite being on medium low income. Achieving success by their own determination not by high income.

“You’ve just got to believe Peter”

Seriously “you’ve just got to want it”... really

If success is debt 12 times your income, who wants success. If you’re a teacher in Auckland then I am sorry, it is unattainable on a normal wage with a normal lifestyle that one should live in work life balance. Bank of mum and dad doesn’t count and neither does getting in 3 boarders. Forget about having a family too....

But you’re right. You just have to click your heels together and think positive things.

Looking past the quips and reading what you actually think you basically agreed with me that someone could buy a house as long as they made some sacrifices. Except that you think someone should not have to make any sacrifices at all, and therein lies the problem.

If your over 40 then that's ingenuous, as houses were quite a bit lower to incomes only 8 years ago. Houses that were 600k are now over 1 mill in Auckland. The cost of a deposit is the cost of a house when I was a teenager starting out. There is no way someone on an average income can buy an average house in Auckland. While renting in Auckland. Sacrifices you must be talking about not feeding your kids and selling the youngest.

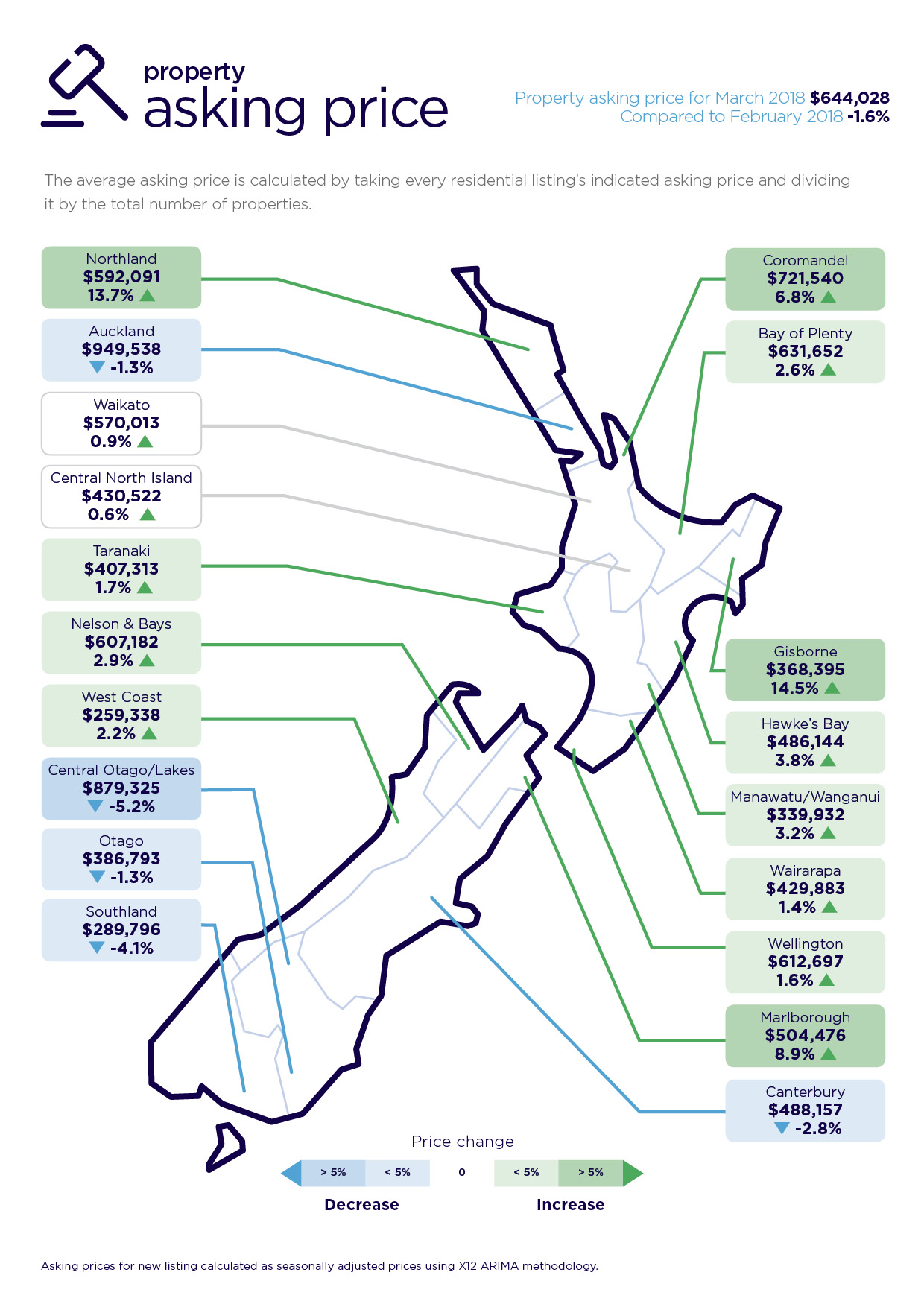

Very interesting to see Gisborne leading the country for price gains (albeit from one data source on asking price, so grain of salt with that)

What's interesting is how many Auckland people with an interest in property keep repeating how the regions, and places like Gisborne in particular, have saying the regions have no property gains. Any genuine look at the data, whether the last few years or the last 20 years, will show you that's just not true.

Keep it up though, all the more money for the rest of us

It is getting close to the time for the regions investors to consider selling to the momentum investors that are leaving Auckland due to the lack of gains. An interesting rule of thumb that I have learned is that the regions do follow Auckland, but with a fairly large lag time. The regions sell trigger hasn't activated yet... but the rubenesque lady is practicing her arias...

The longer the stock rises without a corresponding price drop, the greater the chance of a full blown crash. At some stage some of these people are going to have to sell at whatever price.

Yep. Potential for a real "mommy..the emperor has no clothes" moment, except it will probably be the bank saying it and the words equity margin call will be included.

Govt to hold the course to save us from our fixation with more debt.

Where do you get this idea of an 'equity margin call'? Almost all loans in this country are fixed term contracts, not on demand loans...

.

I'm not sure why people think Banks can't do that. They have lent money against value of asset. If value of said asset goes down, risk goes up. To mitigate risk and restore equity ratios, exposure must come down.

It might be fair to say it's not a common occurrence now, but that is no predictor of the future.

Thats completely incorrect. The bank cant 'decide' that you cant repay the loan. Nor can they change a loan term at will. Bank loan agreements, master facilities etc are subservient to CCCFA, you read must read the CCCFA and then you read a master facility or loan agreement as a subservient function to the CCCFA that is how T&C work in NZ. Once you have done so you will quickly realize banks cant recall a loan unless its on-demand.

If I got myself buried in consumer debt and was struggling then sure. If i blew up my house they can request i post new security etc.

They can not however treat me unfairly and call in my loan if im diligently making my payments, regardless of what they 'believe'.

There is no such thing as an equity margin call on fixed term contracts in this country.

.

Thats wrong. If the value of your property fell because of the market, and not because of negligence, they can not recall the loan. The bank can not operate oppressively and known risks when they sign the contract are not grounds to recall loans. You would have to have caused the loss to your property.

A bank can not recall a term loan in NZ, its strictly forbidden under NZ Credit Law. You can not contract out of CCCFA and so all T&C are subservient to CCCFA.

You must be treated fairly, you can not be treated oppressively. Fixed term contracts in NZ and not re-callable, only on demand facilities can be recalled at will.

(e) ensure, in the case of an agreement to which Part 5 applies, that—

(i) the agreement is not oppressive:

(ii) the lender does not exercise a right or power conferred by the agreement in an oppressive manner:

Meaning of oppressive

In this Act, oppressive means oppressive, harsh, unjustly burdensome, unconscionable, or in breach of reasonable standards of commercial practice.

Interesting.

If oppressive loans or terms are not allowed, can you explain how companies such as Pretty Penny loans are doing business in New Zealand? They charge only 1% per day interest, and have ~20% loan origination fees, which could be larger if the loan amount is smaller.

Interest rates are covered under specific disclosure requirements in the CCCFA and have never received the scrutiny that I think they deserve under the more general requirements of the CCCFA. However i suspect they are given a wide birth because they are seen as preferable to loan sharks.

Its possible that no one has court tested ultra high interest rates. Fee gouging was recently court tested in Australia and found in breach on almost half of the claims.

Sometimes things just fly under the radar for a long, long time.

Jimbo the market merely requires a catalyst now like recession & or

Interest rates climbing.

The Auckland property market still hanging in there with sellers still optimistic

I cannot see Auckland ever dealing with its enormous $6Billion debt so infrastructure will remain an issue for funding. The government uses Auckland like a cash cow & should be supporting it like they did ChCh after the earthquake but that won’t appeal to many complainers south of Bombay

Again, 'Prices WILL Vs WON'T drop' battle here. The facts are the

1. Prices are NOT affordable

2. Stock for sale is increasing

Unless you are not a speculator whose life is dependent upon capital gain, you should hope for the prices should drop to affordable levels. As a FHB, I will wait; NOT for the prices to drop ; but till find a good quality home, in my affordable range.

Well said Greg, ... however sorry to hear about the 9.5% increase in your rates for the next 2 years ..that will make it more difficult to own a property and wonder if it will push the more expensive and new built house prices down while increasing the lower decile ones.

Yeah.Rates increase add to the overhead. Its so messy out here. But I don't think entering this messy world of housing will only make it irrecoverable.

In the meantime lets support the government and council who proposes solutions to this mess; NOT to discourage by scaremongering about any 'unintended consequences'

@Greg Hamilton You think there are only two facts :-)

The inventory is going to pile up as investors exit the market. Due to increased landlord costs, the new 5 year brightline test, and high LVR limits, there is little incentive for people to invest in rental properties. Instead of buying a cheap rental property, you are far better off selling your current owner occupied dwelling, leveraging to the max and buying a bigger and more expensive house to live in. That way you get to borrow more, and you get the same capital gains without having to pay any tax on it, which is the whole point of the investment property exercise in the first place.

For the specuvestor completely agree. There are some yield focused investors playing the long game as well.

@K.W. this is literally one of the dumbest things i have ever seen here and ive seen some pretty ridiculous stuff.

The bright-line test disincentivizes selling, obviously...

Leveraging to the max is simply retarded. What if you lose your job!

If you buy a bigger home you can borrow LESS because you dont get rental income and the vast majority of people are servicing limited, i.e. housing affordability is stretched, equity is actually at all time highs for the same reason.

You dont pay tax on investment property, you pay tax on traded property. People buy rentals in the most part for long term benefits and the gains are tax free as a result of that.

What you are suggesting is extremely risky, mathematically bunk and completely mistaken on how tax works.

Leveraging to the max is indeed 'retarded' and is also precisely why we are in a pickle of a bubble... prices went up because credit was easy and leverage was seen as sweet in the horizon of endless CG

and high LVR limits..

I read somewhere today that more relaxing of LVR to come this month.

Average an, you are totally correct.

Investors are the ones who will do very well with the new policies that the COL are going to bring in!

The capital gains tax will not be brought in because the COL will not be in power next time in.

Investors will also do very well with the new policies they promised but look unlikely to bring in such as restricting foreign ownership and lowering immigration.

You sell me your property! Sell it to me now ha ha ha ha ha.

I wonder if a housing price crash will happen as Kiwibuild really ramps up and is placing houses on the market.. Banks will then be writing more mortgages to first home buyers thus spreading their exposure.

Kiwi what? ..who? ..when? ...housing crash? what crash?

Seriously, you are a bit delusional or extremely hopeful - Stop listening to Tony Robbins and his useless habits of positive thinking messages ...get your feet on the ground for a change and stop dreaming.

Echo Bird, your novice comments are a telling sign a crash is the last thing you'd expect which warns the professionals one is not far off.

Hi Expired-Poppy,

You're like an old 78 gramophone record stuck in the groove........

Constant talk of a crash but never a skerrick of evidence.

TTP

#potkettleblack in terms of stuck

(•◡•) ... perfect description

You are no professional mate and you have no experience whatsoever. Just a typical know it all.

I think Didge was being sarcastic Echo Bird

No, it’s consistent with his other posts.

This is exactly what the government should be doing - flooding the market with rent to buy housing and cutting out the middlemen of the accommodation supplement / working for families gravy train. Shelter is a basic human right that should be available to all without sucking productivity out of society. Landlords can still play in the "discretionary" end of the market.

Auckland: San Francisco prices, without the salaries.

....without the salaries, industry of any note, and rapid transport system

Ive got SanFran median household income at 78K and the median 'house' at 1.3 million. ratio is 12.

Auckland median household income i have at 83K, houses at 900K, ratio 11.

Seems cheaper in Auckland? but more broadly just seems to argue that in the modern interest rate environment the ratio is about 10 to 12 in the most desirable locations.

.

Do you think the us coming out of long recession has anything to do with that low 7.8 multiple? In other words property prices are on the rise in the us and faster than incomes. The nz equivalent would be wgtn. High personal incomes and relatively fast rising property prices off a low base.

.

Also, housing withing commutable distances is more affordable than the same in Auckland. E.g. just across the bridge in Oakland can give you a better salary vs. housing cost than that. And if you head further out to Concord or such like, it's even cheaper...a significantly better equation than Pukekohe or Pokeno etc.

Interesting times but I’m game to make a prediction here right now. I’ll wager a single groat that by this time 2020 the median Auckland house price will have exceeded the highs of last year. I also predict that what happens in Auckland will be quite different to what will occur in the outliers. I also predict that the next election will be decidedly one sided and the winningest party will not be beholding to any casual suitors.

Cue Mission Impossible theme music...

Better put that in an esgroat account. Do you mean nominal dollars or inflation adjusted? Median sales price or median model valuation.. lets be specific eh

I’m a modern day Nostradamus so nothing too specific

Meanwhile in Australia... "Why First Time Buyers will not take up the property slack"... An article by Digital Financial Analytics which has excellent source information. Certainly worth watching and subscribing to this channel, as we share the same banks and therefore the same lending practices occur across all boards.

https://youtu.be/5UcTR3d3jTw

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.