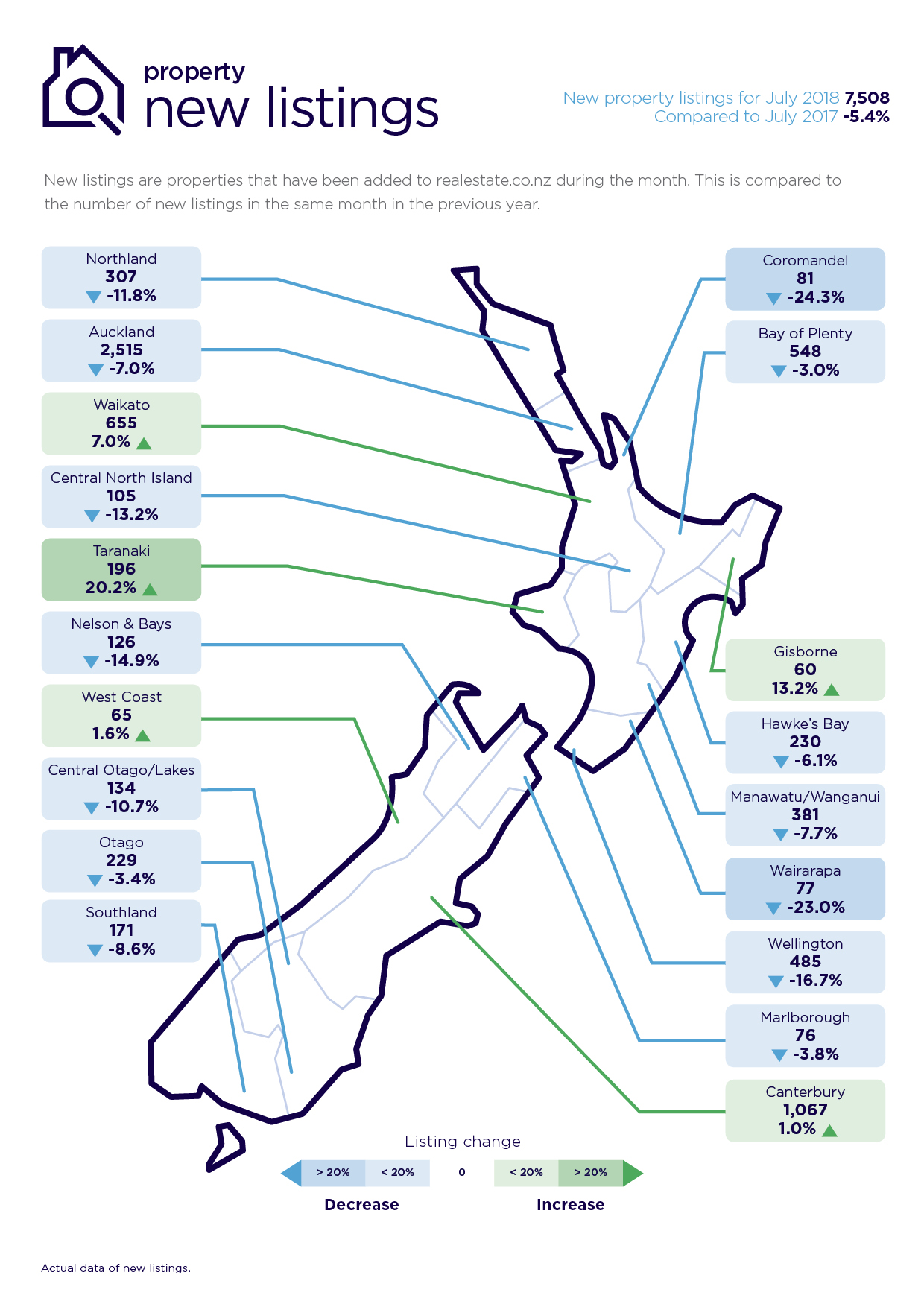

Winter looks to be tightening its icy grip on the housing market with the number of new listings on Realestate.co.nz in July at the lowest point for the month of July since the property website started collating figures in 2007.

Realestate.co.nz had 7508 properties newly listed for sale in July, down 5.4% compared to July last year and down 21.9% compared to July 2016.

The number of new listings in July was down compared to July last year in all regions except for Waikato, Gisborne and Taranaki, where they were up compared to a year ago, and Canterbury and West Coast where they were virtually unchanged from July last year.

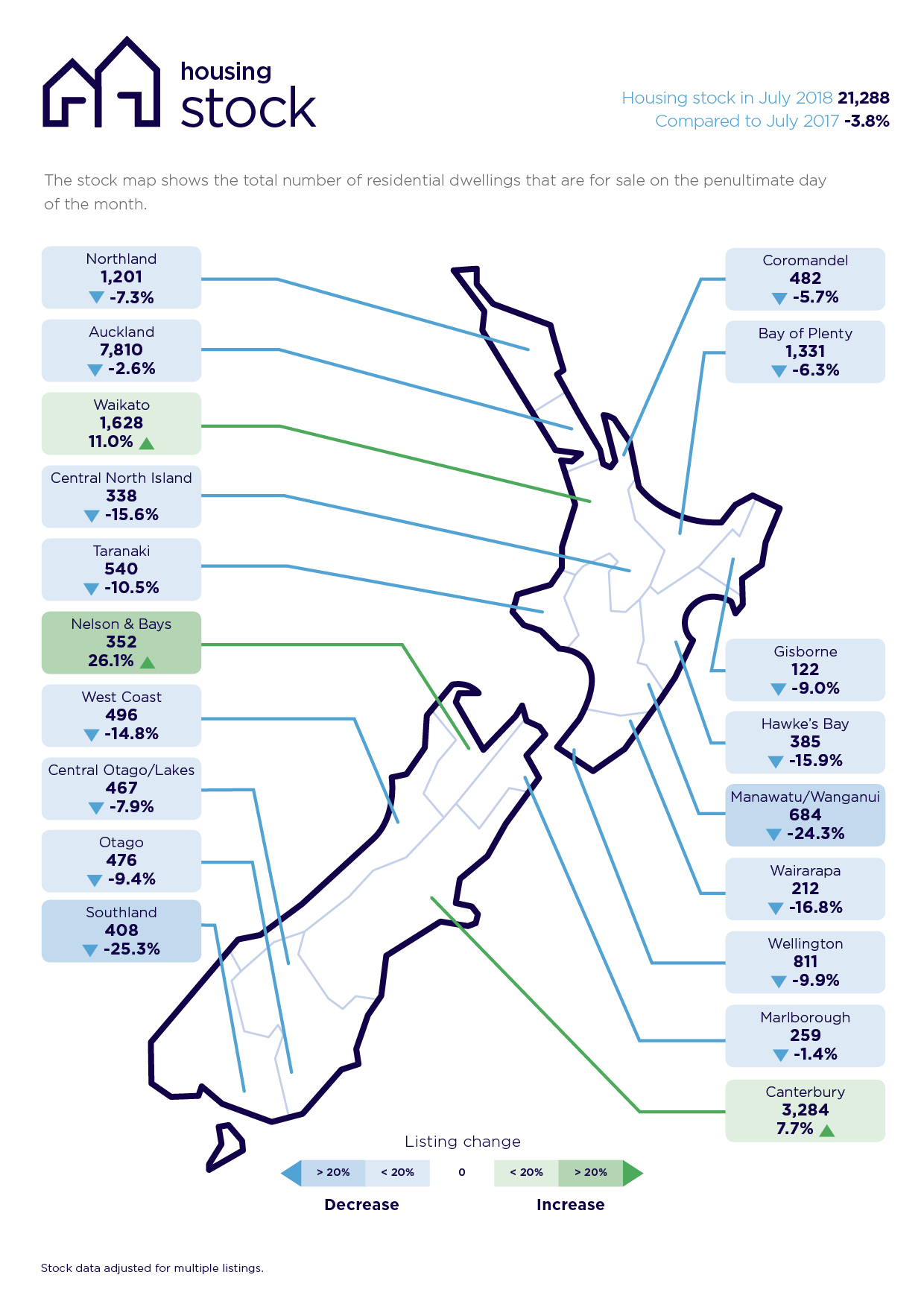

At the same time the total number of homes the website had available for sale on its books in July was down 3.8% compared to July last year, but up 2.9% compared to July 2016.

The asking prices of properties advertised for sale on the website were also softer, with the national average asking price falling for the third month in a row to $635,020 in July, down by $38,639 (-5.7%) from its February 2018 peak of $673,659.

In Auckland the average asking price rose slightly to $921,205 in July from $912,071 in June (+1.0%), but that followed four consecutive months of declines, with July’s average asking price being $72,970 lower (-7.3%) than its February peak of $994,175.

Ironically, while new listings and asking prices are soft on Realesate.co.nz, the number of people visiting the website is on a high.

The website said 846,818 unique browsers visited the website in July, which is more like the traffic it usually sees in the summer months.

So whether they are keen on buying or selling there are plenty of people looking at property. But for the time being it appears a lot of them are just window shopping.

75 Comments

Seasonal variation, with a side of debt stacking reality. Nothing else to see.

"largest regulatory credit crunch in 30 years" (is) the cause for the slide in property values." GIven that Their Banks are substantially Our Banks, any fallout is likely to be similar.

" house prices could fall .....in a repeat of the late 1980s and '90s"

https://www.afr.com/business/banking-and-finance/credit-crunch-to-hit-h…

Interesting piece.

I have been amazed how easily I have got some loans in the last few years,m. There seems to be a real lack of due diligence around some of the finance companies

similar behaviour was displayed right before the GFC

A case of history repeating itself

Auckland listings might be slightly down but Waikato's is surely up. Could it be that Aucklanders want to exit their once beloved playground? Come spring thaw, there will be listings abound, driven by a deeper anxiety that the housing shortage was just driven by loose lending standards. The market of yesteryear was dictated by a buyers fear of missing out. Now, as the spring months tick by, indications are, it will be driven by vendors fear they'll not get out.

I'd have thought lots of listings would indicate lots of people wanting to bail out, and a lack of listings meaning more want to remain. My guess at the moment is a bit of shell shock in Auckland, people hoping like crazy this is just temporary, and getting in while the getting is good in the Waikato (which I believe with the phenomenally rapid expansion going on now, is in very serious risk of overshoot).

How wrong you are, let me enlighten you.

If listings decrease it means vendors are in deep trouble and have taken their property off the market to renovate to try and sell again at an even lower price. If listings are up then those vendors have completed their renovations and are now trying to sell at a lower price.

In an "end of days" market that we are currently in basically any listing increase or decrease, or even average price increase or decrease is an indication of vendors crashing and burning.

Therefore, even if average prices are increasing (as Auckland did by 1%) they are in fact going down.

Not sure if you're being sarcastic or ...

'just really stupid'

FONC- Fear of no chair...as the music stops, which it is.

Eternally optimist RP of something really bad happening again as usual. Auckland is just like all big cities they get bigger and more expensive, Sydney 3 times the size and lots of bluechip suburbs average price 3,4,6 even 10 million . We don't set the rules or influence the market. Having said that you can still get house and land packages for $550 - $650 at Pokeno or Te Kauwhata which great. It's not all bad if property is not your thing that's fine let it go move on.

Are you talking about this Sydney? https://www.businessinsider.com.au/sydneys-housing-market-downturn-hist…

tgcam4, Auckland's just like Sydney on trip up, bears no resemblance on the way down ;-) I think Shoreman just found out Sydney prices are falling, Auckland is following.

"bears"- i see what you did there ;-)

All so true: Sydney and Melbourne drag house prices to first annual fall for six years

https://www.theguardian.com/australia-news/2018/jul/26/sydney-and-melbo…

Market looking frosty this winter.Sellers may emerge from the winter with frostbite,.Solution ? Stressed sellers may unload what's causing them the frostbite.Otherwise gangrene may set in.Option? Chop off the affected limbs

Is "Chop off the affected limbs" code for "please sell me a house at 10% of it's market price now or you'll be sorry in the future... Woooooo (ghostly sound to scare skittish house owner)"?

If so keep dreaming sunshine.

HeavyG, I think you may be find the expecation of buyers is for more than 10% off already. I went to an Auction today and would advise everyone to take a look at a few for themselves. take a newspaper along because there are some very quiet spells where nothing is happening.

Observations, there were more vendors in the room than buyers was the first thing that struck me.. In fact there were probably more RE agents than vendors and buyers combined. When the bidding started it was very much like being in an library. It wasn't a successful auction by any means but there were deals done, but none were settled without negotiation having failed to meet the original reserves. The prices however on the few deals done were as if the clocks had gone back. Back to 2014. This is going to happen quite quickly I think.. The information age is speeding up the change in sentiment. It made me think back to the 2008/2009 crash and do you know what back then there were very few I-phones, news blogs etc so the press controlled the relay of information to the masses. This time everything, price data etc etc is there at your fingertips.

This could get very interesting very quickly!

Nic, you've made a valid point. The information age has the potential to make this downturn more acute. It certainly provided added impetice on the ride up.

10% OF not "off"... e.g. $1m house for $100k

10% off this grand old lady "Mainston Manor" will still set you back $5,000,000 https://www.youtube.com/watch?v=F0gRtKpxbsU

Why are so many people on Interest.co so obsessed with what the housing market is going?

Stats can paint a rough picture of what is going on, but why worry about it when there is always good,money to be made.

If people are hoping for prices to plunge then they are going to be sadly disappointed.

While this government has put things in place to make it harder to be a landlord, it is only a small percentage that will be severely affected.

The market in Christchurch is still very good, just rented a 4 bedroom property for $595 a week to a very good long term tenant.

This gives a very good yield on purchase price, so as I say there is always opportunities in real estate on any market.

What I suggest is that if you want to get into the rental business, get alongside someone who knows all about it and is prepared to assist you to get ahead.

Cos most people want to enjoy the benefits and security of owning their own home vs paying a landlord for the rest of their days. Most employers are keen to see this as well as it creates a degree of stability. They are less likely to bugger off to Aussie for example.

And this is where most of you go wrong in your thinking and spreading what you have been told just like puppets.

FACT: Any rent amount today in all main cities is LESS than what you pay as INTEREST if you owned the same house ...!!

do the maths !

Now, whether you pay that to a Bank or a Landlord does not make any difference, does it? .. that is an expense whether you rent or you Own !!!!

Now, whether the landlord was HNZ, a corporation or private mum&dad does not make any difference either !!

But you die green of envy from landlords but not from Banks ... How stupid is that?

As usual , your comments are less than average

For once, I agree with Eco Bird!

In other words, the only reason to own an "investment" property is for capital gains, not for the rental derived return. And when the capital gains drop below inflation (first order assessment, the reality is a bit more complicated as one also needs to assess the costs of rates, maintenance, insurance, etc. for the landlord) there is more benefit to owning a term deposit than an investment property. I've benefited from this assessment in the past three decades while being both a homeowner as well as renter. Sometimes it is better to own, sometimes not. Depends on the capital gains available. The hard part is evaluating future gains available. Been "lucky" now three times on buy/sell/rent choices.

Yankiwi, well said! Looks like Eco Bird unwittingly stumbled on his own comment there! Adjusted for inflation a best outcome scenario of flat house prices for the next ten years makes term deposits look very attractive indeed. With time on their side, first time buyers no longer have a fear of missing out.

I will have to caveat my comment somewhat. It is very location dependent. There are some locations in NZ that still have reasonable investment property returns as compared to TD returns. Unfortunately, Auckland isn't one of them.

Disclosure: I own no investment property and have never owned investment property other that via REITs. I did purchase my first home back in 1987.

Hate to continue arguing about this matter... but you are right in a small time frame window but not on the long term ... Property and Shares are very different classes. I have been investing in both for the last 20 years.

property investors do not sell their investments when there is little or even no CG, Only speculators or developers at a certain window in a boom cycle would do that and move to the next one ...

the fact that you don't own one comes to your defence ... Rent yields are not static, they are adjusted for inflation and increases in rates and other running costs .. so every ( properly run) investment property will start producing a net positive yield after about 5 - 7 years even in Auckland especially in a declining interest rates environment like we had for few years and looks we will enjoy that for the next 12-24 months too --

BTW, RP knows shit all about this ...lol, so don't pay too much attention to his rhetoric, he just has a doo agenda to follow.

Investment in Rental properties is certainly much much beneficial than TD or REITs -- there is a whole package of benefits for being in this business that's not available to Index and ETF investments ... However, Share investment and managed funds returns will almost equate to the overall property returns in the long term as history clearly shows.

Eco Bird,

If "very small time frame" means decadal time frames, then you are correct that it can be cheaper to rent than own. I'm pretty sure that this is not your meaning. I am a practical example that disproves your global statement about property investment being the best choice over time frames longer than 5-7 years. I've now owned property for an aggregate of 22 years, and also was a property renter for ten years. After 20 years of ownership I returned to renting and invested my home property wealth in the share market while it was cheaper to rent than own, and returned to home ownership in recent years when it once again became cheaper to own than rent (this decision is strongly location dependent!). This cheaper to rent than own or cheaper to own than rent selection actually compared total returns for the property ownership vs investment in TDs, rather than the share market. The share market has done considerably better than TD during the timeframes I have been renting.

I'm pretty sure that for all meaningful reasonable time periods in the past several decades, property investment has been a lesser performer than the equivalent risk/leverage investment in the share market.

As you have noted, at present the returns for term deposits are currently greater than the returns on housing investment. Until meaningful capital gains return, or the net return for property investment gets above low risk investments, then owning property as an investment is a losers choice. For now, it is better to sell the investment property now and take the larger income from even a TD than to continue having a near zero or even net negative total return investment property. This will continue to be true until either the net property investment returns increase to above that of low risk investments, or when substantial capital gains return.

The idea that my return should be compared to my purchase price instead of the current investment value is silly. The return should be compared to the equivalent return if I sold the asset and invested the proceeds into whatever investment type that I wish to do the comparison with the property investment return. If I wish to compare similar risk level, then maybe the share market. If I want to compare to lower risk, then TD or govt bonds.

I'd suggest a similar risk level for comparison would be to some of the NZ utility shares that are currently returning above 8% even with a capital gain over the last few years of about 65 to 100%% prior to dividend gains. If you wish to compare yield as compared to purchase price, my shares in MCY/GNE/MEL are all yielding about 12% or more as compared to my purchase price... without any rates, insurance, maintenance or rental costs. With a nice 65% to 100% capital gain as well...

Yankiwi,

I somewhat agree but not entirely ... disagree that you should sell a property to invest in the Share Market or TD , you may do that after the age of 70 perhaps - it is not as simple today as you are putting it ( due to LVR revaluations, CGT etc). Timing the property market is very tricky and very expensive too.

The CG realised is accumulated in the property value.

You can alway utilize that improved equity and borrow against it if you find a better investment and returns somewhere else without selling expenses and loss of future CG. My experience so far is a net return of 10% after expenses and costs on that extra borrowed money, in fact much more in $$ value than the total of rents produced by the same properties. So the overall return is compounded.

Almost all my properties have gained over 100% in CG in the last 10 years ... while GNE gained ~40%, MEL ~ 30%, and MCY~ 28% in the same period ... you get 6-7% in gross dividends from these companies in a good year. You pay tax on that and cannot claim your expenses unless you are a trader, you also pay rent which is a significant amount depending on what and where you rent .../ ..

In contrast, I get the rent ( as dividends) , claim my expenses, depreciation, and loses and end up with the CG which in the last 10 years was far superior to the share market CG returns.

I hear what you are saying as I almost have equal values in both classes. my share portfolio returns averaged over 22% last year alone while dividends pay for the cost of money .

I invest in more dynamic and progressive commodity and technology companies alongside the less risky Utility shares mentioned above.

I can say that the returns from my property portfolio were better in the last 10 years given the big jumps in CG. even much more than that if we include the 2003 cycle .... But I decided that I needed to diversify after 2009 and spread the risk, and I am glad that I did....

I guess this discussion will always depend on the measured Window, where the investments are (location), and the timing inside a particular cycle in either asset classes.

Enjoy reading this piece by Brian Gaynore

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

Chances are that the property market will rev up again come 2020 when the cycle reverses and the Noobs are gone.:)

Your capital gains evaluation of MEL, MCY, and GNE (NZSE stocks) are completely wrong, as well as your dividends assessment of these stocks. You cannot sort out a 10 year stock value capital gain on these, as they have only been around for four years when the National govt stupidly took them public. I wasn't about to miss that boat, excepting that I waited a few months on Mighty River Power to buy my shares more cheaply on the open market than the IPO. For the other two utility IPO, I purchased the IPO as the probability of gains was far higher than the first IPO. In the four years since the three IPOs, they have gained between 65% -100% in capital gains, and with early gross dividend annual returns in the 12 - 15% range, before the share price increased so dramatically and diluted the dividend returns.

As to the buy and hold property strategy, the house I sold in 2006 was worth about 55% of the sale price by 2009. It has only recently returned to the same price as the 2006 sale price. Including inflation, it has a way to go to get back to the value of 2006. The proceeds from selling that house has doubled in value, even though it was largely invested in NZ TD, with the bits that were invested in the share market doing considerably better than that.

Sometimes market timing is the smart thing to do... I went from shares to bonds first in 1998, but only for a few months to avoid a small decline. Then the same in 2000, and missed the dotcom crash. Went back to fully vested after the crash, and sold out in 2007. I went short from 2007 to 2009 and made a 50% profit during the decline, at which point I had enough, so I went to cash. At present, about 15% of my liquid savings is in the share market (almost all of this is in the 3 NZ utilities), the rest is in TD or cash equivalents as my needs are now oriented towards return OF capital instead of return ON capital. I've enough now to survive to 90 on the principal without any super/pension/social security. All I have to do is keep up with inflation if it once again rears its ugly head, so no need for any risk anymore. I'm comfortable with the concept that market timing can work very successfully if one does sufficient research. Or, maybe I've just been really lucky in both the share and property markets.

Thank you , and Yes you have been very lucky indeed,

My numbers on the said shares are derived straight from my ASB share trading program and it shows the share history and percentage of CG over 10 years... I've been in these shares in and out in the last 9 years, but have held to MEL an SPK in the last two ... could never remember seeing any dividends in 12-15% ...maybe one year from Contact Energy and that was it.

As to your 2006 property which is now at the same value as then, wow, no offence but that must be a hell of a property in a hell of a town !!

Anyway, good on you ... everyone cooks a different meal and there is no one size fit all in this game.

Yankiwi, I am also referring to Auckland. Metaphorically speaking, Auckland's the dragons head, regions are the tail. Where Auckland goes, Hamiltons for example is not far behind. I recall in 2016, a lot of Landlord/Speculators like Eco Bird were denied finance on their own turf so they went further afield and gambled on Hamilton. Inventory dropped considerably. In reverse, its logical Hamilton will follow Auckland close behind. It's just interesting, being that its winter, there's quite a lot of inventory down there.

I think that metaphor isn't a very good match.

Many of the regions didn't materially participate in the large capital gains that have occurred in Auckland, at least that is true for the last dozen years. It has been true that the regions in general have historically followed Auckland, although with a bit less whipsaw action. In other words, less up, and also less down. I would use engineering nomenclature, with the regions being more highly damped and with some phase lag as compared to Auckland. Hawkes Bay didn't have any material capital gains for almost a decade, and finally started to return capital gains in 2015. It is a completely different market compared to Auckland. Other regions followed different paths. Taranaki had quite the boom due to energy, other areas went fallow and suffered a bit during the same time period. Hard to make a blanket statement regarding "the regions".

Yankiwi, fair enough. I agree there are anomalies to the rule. Being there has been considerable run up in house prices in Auckland, I'm thinking many Aucklanders are seizing the chance to lock in gains, move to the regions for lifestyle, be debt free or whatever and contributed to pushing regional values. I suggest that Hamilton, Tauranga and Northland prices in particular have also enjoyed a late run from Auckland based speculators combined with those wanting a change in lifestyle. I recall incidences where Aucklanders were committing themselves to Hawkes Bay and South Waikato properties without proper inspections.

Happy to see that you have learned something RP although messed up with the dates and years ...

What a fool? ... how can an investor buy in Hamilton if he was denied finance in Auckland --- Finance is Finance Poppy, you either get it or you don't .. lol, ..........do you even read what you write ?

And yes RP, "my gamble" in 2013 in Hamilton had positive net yield from day one and now has 95% CG ... Noobs call it gamble, We call it the best business decision ever .... stick with your TD mate, you are incapable of resolving more complex matters than that.

You still cannot distinguish between Landlords and Speculators! even your mate PT has learned the difference, didnt you read the memo?

Eco Bird, initial LVR/speed limit restrictions were aimed at Auckland based Landlord/speculators and not the regions initially from 13 May 2015. I recall this lead to some already stretched Auckland based Landlord/speculators searching afield. Now, going by your apparent acceptance that the first 5-7 years of ownership, rentals are usually negative geared, this herd most likely included you.

https://www.rbnz.govt.nz/financial-stability/loan-to-valuation-ratio-re…

Why are you so salty? For good reason, TD's are gaining popularity and like ring fencing, it's caught you by surprise.

My mortgage formula was RENT=PRINCIPAL+INTEREST. It was from the get go and 15 years later on and with my payments increased it was still the case. Rent is dead money, your simply paying off someone else mortgage. 15 years later and I have $1M not zero.

Anyone who is looking to get into residential rentals should avoid The Boy's advice. He has made the mistake of putting all his eggs in one very badly performing market ie Christchurch. He has let his family and himself down by doing that. Probably hundreds of thousands of dollars if instead he had gone to areas outside of where he lives. That is of course if his portfolio in fact exists which I doubt. No one could surely be that silly with their investments.

In the not so distant future, I suspect that due to issues that our government will have little ability to control such as exorbitant amounts of world debt, and climate change etc. Being a member of the rentier class will, at the very least, ensure one is hated and despised, at the other extreme only time will tell. However, after watching recent events in Britain there was very little truth from main stream media about how so many of their peoples felt. Obfuscation rules supreme.

Some people love to watch car races for the crashes. Especially if you can run on the track after the crash and buy you a race car on the cheap.

Many of the commentators have been waiting for a crash for a long time now and are getting more and more worried as it doesn't appear to be happening as fast as they would like (or at all).

Their $200 deposit in their bank account (called the "vulture account") is burning a hole in their pocket and they want that 3 beddie in Auckland for $1,000 they were promised (by themselves) ASAP.

Houses Overpriced has been waiting 7 years. That's like 15% of one's working life as a wasted opportunity for home ownership.

Awwww lol ^^

Nzdan, personally, I can see nothing wrong with people waiting patiently for well documented events to kick out the foundations of this monumental ponzi. There needs to be many willing and financially qualified buyers waiting at the bottom as possible!

I've used my 7 years productively, unlike you who is wasted, illogical and stupid

Interesting to see what will happen once the foreign ban is introduced as in absence of any credible data by earlier national government - the opinion is divided but those who argue strongly that foreign buyer (Non resident is hardly any - 3%) and that the affect will be minimum of the ban, actually are a worried lot or why else would they be nervous if they actually believe that the affect will be hardly any.

https://www.parliament.nz/resource/en-NZ/OrderPaper_20180802/cf5138c768…

20% listing increase in Taranaki. Oil and Gas evisceration starting to bite?

An investors graveyard... wouldn't want to have got in there too late!

"Falling prices, no tenants, the worst is yet to come...."

https://www.afr.com/real-estate/falling-prices-no-tenants-the-worst-is-…

It gets more sobering by the day, and Sydney has the same 'housing shortage' that Auckland does. It's not a shortage as such but an ownership distribution issue - 1 owner with 20 properties and not 20 owners with 1. Rents being below the cost of ownership tends to indicate that.

bw, spruiking commentators, DGZ, Zachary and TTP were quick to point out the link of rising Sydney prices and Auckland's by arguing they are both international cities. Now, on the way down they're quick to distance Auckland. The spruikers have been silenced!

Yep. Argument of convenience. Asset reset is coming.t wish we would get the #@*& on with it.

Like it or not. What has to happen will happen.

Pity if anyone feels that any market is a one way street as they are only fooling themselves.

When they argue and defend that the market will not fall is actually trying to convince themselves.

Gordon, the Christchurch real estate market is extremely stable and that is the way I like it.

Yes the prices are flat but not dropping at all.

We don’t give a rats as to what the prices are anyway as we don’t intend selling as we get good returns and therefore no,point.

You doubt that we have a large portfolio Gordon, and you continually point this out to all!

Back yourself Gordon and take up my challenge to you, but I know you won’t because you have not got the fortitude to invest in anything but shares that other people do the work on, and not yourself.

Loving the property business!

I love property too The Boy but mine is the developing of sections and commercials. Owning houses would be like watching paint dry. Anyone can do that especially cheapies in poor old Christchurch.

The childish bickering in the comments section is very sad and it drags the very valuable reporting form Interest.co.nz downhill

Pot-kettle-black, while I agree with you, suggest before posting such comments, first practice what you preach.

Maybe if your maturity level increases, you will realise how childish your lot of comments are..

That day may never arrive..

Pot. Kettle. Black. HO.

Is that all you know to say.. do you just copy and paste.. or do you get your kid to do it

You freaks are holding this country to ransom with a ridiculous overinflated asset that you mindless jerks have blindly invested in...

So you can post any crap and think that is highly intellectual stuff...

The emphasis is on the bold. Have some taste :-P

You just love proving how pathetic you are

latest information on Overseas investment amendment bill

National shows that they stand with wealthy foreign buyers instead of New Zealanders.

http://www.scoop.co.nz/stories/PA1808/S00018/national-shows-its-true-co…

We have to understand NZ needs foreign capital. Allowing foreigners to buy houses over $2.5 Million in Qtown makes sense to me. It will not outbid the average Kiwi trying to buy a house but it will help Qtown from collapsing, which is very likely to happen if you remove all overseas money.

No, we don't need foreign capital pouring into housing. Foreign capital into productive industry is what we need.

Have you considered that in order for foreigners to invest large in NZ we might have to give something back? Like allowing them a Residence to live in while checking/managing their investments.

"Bring your money to NZ but stay away" might not work so well in the real world

Investors in business do so because the investment is a sound one, not because they think they get a holiday home thrown in. We give them a sound business and political environment in which to invest, and that’s all we need to give them.

This is incorrect. I have foreign investments but I don't expect residency. What the investment gives back is capital growth and dividends. The things a real investor expects.

There are countries that trade citizenship and passports for a specified dollar amount investment. We have a similar scheme here but it is a larger sum than the tiny island nations.

Yes agreed. Queenstown should be exempt from the ban for the sake of crashing their market.

New Zealand needs foreign capital for productive purposes. Not unproductive holiday houses.

The only thing adding in an arbitrary $2.5mil threshold does is bump the prices of those properties worth over $2mil and open the door for further dodgy exchange practices.

Good for any National Party cronies who get an instant price floor on their $2mil+ properties. But apart from that, there is no other wider benefit.

Yes, not only no wider benefit - but in fact setting such a threshold would serve to generate wider negative repercussions for the overall market given everything is relative.

If you artificially inflate from any number - you artificially inflate everything both above and below it.

And most importantly, as I understand it - the foreign buyer can still build new - we're only talking about existing stock, right?

How does it help NZ economy? it'd artificially inflate prices. If you have a house in queenstown, i'm sure you'd want it's CV to soar to 10 million and only way to do it by bringing in drug money :)

Don't be silly. Queenstown's industry is not built on housing!!!!! I can guarantee you that Queenstown will welcome exactly the same number of tourists - no matter what the price of houses are down there.

Most of the properties in the $2.5m range in QT at the moment are just modern, non-bespoke 250-280m2 homes in relatively new (post-2000) subdivisions. Build cost of those homes, around $700K.

I can guarantee you that based on local wages - a 600m2 section, even with a view, isn't worth just shy of $2million.

For goodness sake, Queenstown will not “collapse” if house prices were to fall. Take your speculator goggles off for 5 minutes. More affordable housing will be a big economic plus for Queenstown which is simply failing to house the workers it’s needs to staff it’s real economy (hint: that economy is based on tourism, not property investments). Oversized housing costs are a big drain on that economy, most of the workers servicing that industry do not make lots of money. Anyway, it has a population of only 28,000, it barely moves the needle, we as a nation are plainly able to deal with any adverse consequences flowing from a fall in Queenstown house prices. Our housing market does not “need” foreign capital, we got ourselves in this mess through the uncontrolled expansion of credit. Foreign buyers have been fuel on that fire.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.