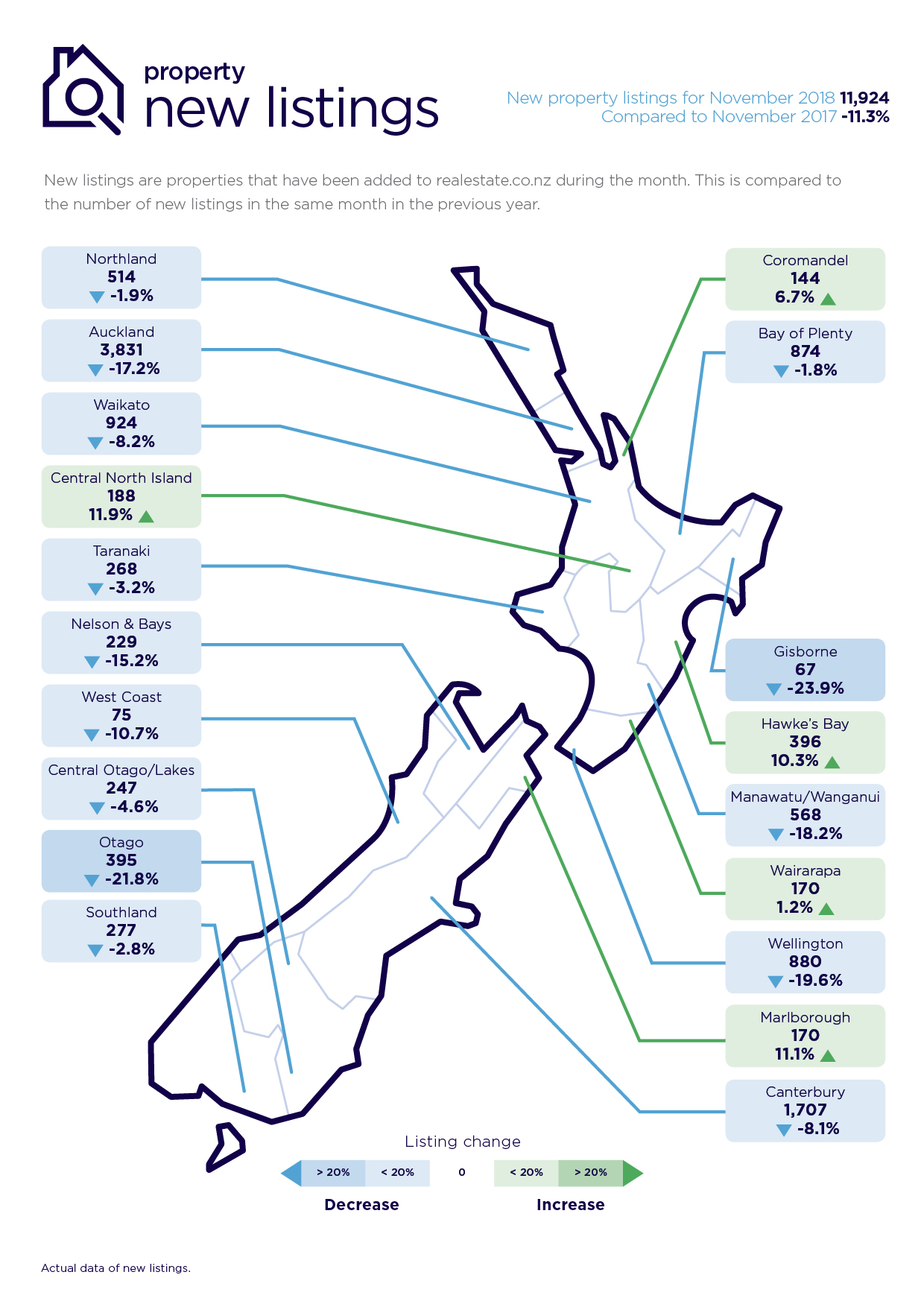

New residential property listings on Realestate.co.nz declined in November, easing fears that a glut of unsold properties could accumulate over summer.

The property website received 11,924 new residential listings from throughout the country in November, down 3.5% compared to October and down 11.3% compared to November last year.

Compared to November last year listings were down in 14 regions and up in five, with the biggest declines in Gisborne -23.9%, Otago -21.8%, Wellington -19.6%, Manawatu/Whanganui -18.2% and Auckland -17.2% (see chart below).

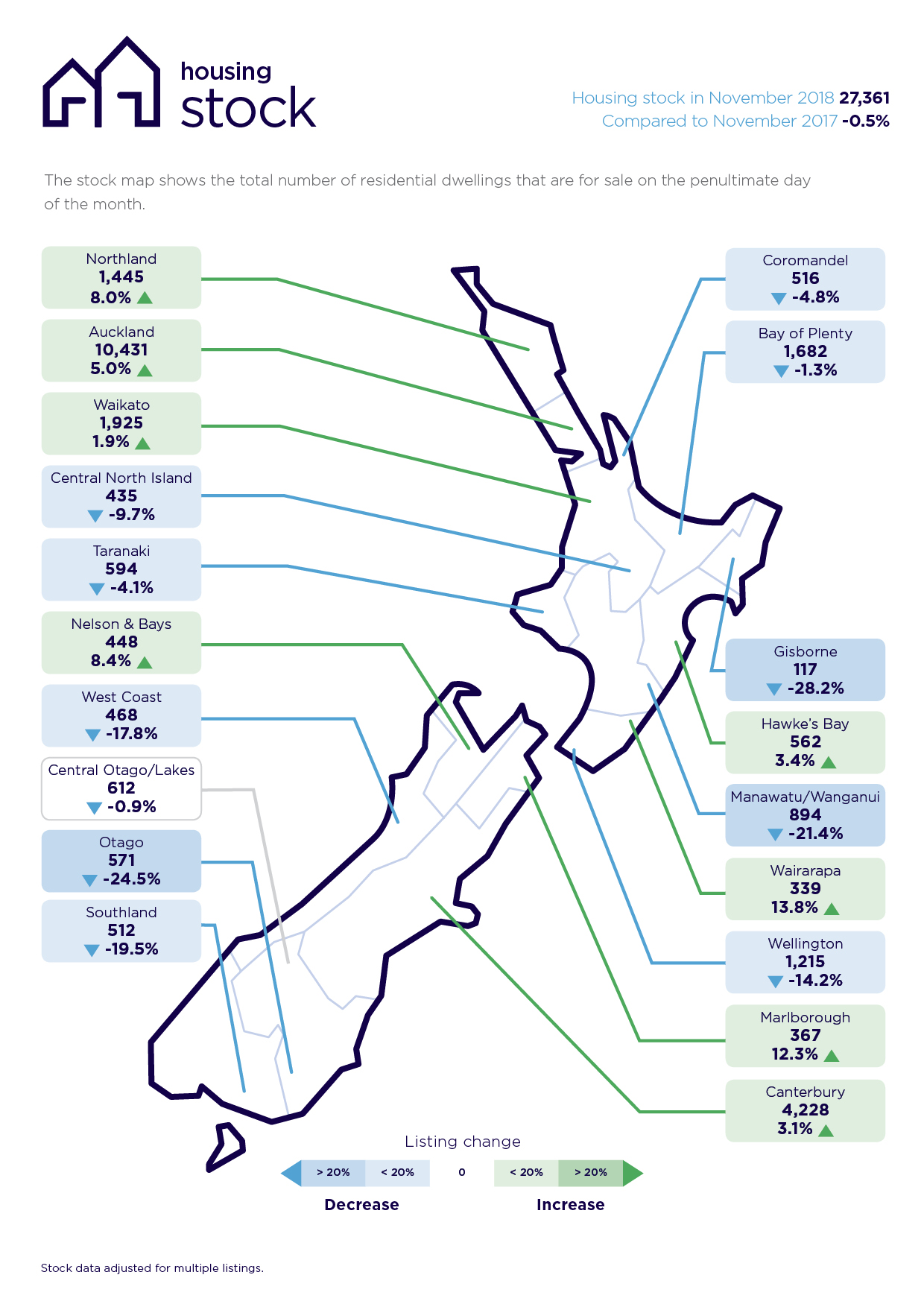

However, buyers should still have plenty to choose from, with Realestate.co.nz having a total stock of 27,361 residential properties available for sale at the end of November, almost unchanged from the 27,488 it had available for sale at the end of November last year.

But total stock levels remain elevated in Auckland, where 10,431 residential properties were available for sale on Realestatae.co.nz at the end of November, the highest it has been for any month since April 2012, suggesting the Auckland market is softer than other parts of the country.

Overall, the figures suggest the market is following normal seasonal patterns for the first part of the summer selling season.

The average asking price of properties available for sale on the website dropped back from its record high of 704,002 in October to 671,528 in November (-4.6%).

There was a particularly large fall in the average asking price in Central Otago/Lakes which dropped from a record high of $1,047,938 in October to $888,088 in November (-15.3%), although the figures for Central Otago/Lakes can be more volatile than other regions because of the relatively low number of sales in the district.

Compared to October, average asking prices in November were down in 14 districts and up in five.

Those figures suggest vendors are adapting to the generally softer market conditions and being realistic with their asking prices but do not suggest any panic selling.

However Auckland remains a buyer's market.

Realestate.co.nz said the introduction of restrictions on foreign buyers purchasing residential properties did not appear to have affected the pattern of people visiting the website, with 65.2% of traffic on the site coming from within New Zealand in November, followed by Australia 8.6% and the US 9.6%, with site visits from all other countries making up just 7%.

There was no evidence to suggest that visits to the site had dropped or lifted as a result of the foreign buyers restrictions, Realestate.co.nz said.

156 Comments

Everything is strangely normal.

ZS - Well that certainly won't make the DGM's on here happy will it ? The Auckland market in particular is more resilient than I thought it would be for this part in the cycle.

Wow, this plane seems fly well with no fuel....everything seems strangely normal, just no engine noise.

I hope we have some thermal up-draft. How long can we glide for?

Please don't delete this one before looking at it, it's not linking to another financial site, it's just an explanation of why the listings are a bit lower at present.

Agree with you, Zach.

The housing market remains steady.

2018 has been a year of consolidation - with no great highs or lows.

I'm picking a slight uplift in the New Year.

TTP

Do you also have a twitter account?

Agent TTP, I spoonfed you the following locales where prices have dropped at least 5%. You replied as follows; by tothepoint | Wed, 21/11/2018 - 17:29 "most are small nondescript localities that few people have even heard of"

Why are you commenting when you have such limited understanding of Auckland?

How can you assume Aucklanders have such limited knowledge of their own city?

Since April 2017, Albany Heights – down 7.74%, Lynfield – down 6.86%, Albany Heights – down 7.74 %, Lynfield – down 6.86%, Pinehill – down 5.84%, Waiatarua – down 5.54%, Golflands – down 5.53%, New Lynn – down 5.41%, Totara Heights – 5.34%, Flat Bush – down 5.26%, Sunnyhills – down 5.05%, Henderson Valley – down 4.92%, Pinehill – down 5.84%, Waiatarua – down 5.54%, Golflands – down 5.53%, New Lynn – down 5.41%, Totara Heights – 5.34%, Flat Bush – down 5.26%, Sunnyhills – down 5.05%, Henderson Valley – down 4.92%.

Hi Crash-Crusader (formerly Retired-Poppy),

You have loudly proclaimed here that Auckland's median house price will fall by at least 5% (year-on-year) by the end of 2018.

When the official data for 2018 becomes available, we will be happy to judge you on your prediction......

In the meantime, I suggest you start bracing yourself.

TTP

... chirp chirp ...

Ahhh-yes:), you mean the dubious (median) dataset derived from a buyer's market?

Coming up next, Master of Disguises, retired-poppy, will try to amaze his audience when he attempts the triple back flip somersault while grasping at straws....

Houseworks, if you can't handle intelligent dissection of REINZ spin, just leave the room ;-) Is the whole of Auckland a nondescript locality to you? If so, are you qualified to be making judgements?

Try not to be so easily duped by what you read in the REINZ reports dude. It's the growing backlog of what's not selling that matters here.

Tooo predictable!

The average asking price dropped 4.6%. I would love to see the data on any change in Auction/Negotiation/Asking price advertised split to tell us if more properties are being advertised with a asking price now or if its a smaller pool as the top end is going towards auctions. Just stating the asking price dropping is not giving us the full picture.

"The average asking price dropped 4.6%" - I wonder if you'll see this in the mainstream media, stated as it is. Can't wait to see what spin they're gonna end up putting on it.

Trapped Millennial - great questions. But dont hold your breath for those answers, that may tell a story much to telling. Total properties for sale at the end of November this year for NZ is 38,162. Auckland is 14,128, Hawkes Bay is 728, Havelock North is 86. This is from realestate.co.nz at 5pm on 30 November 2018. Worth comparing them to the article above . Total is the key word. Hawkes Bay is now moving towards Asking Prices, this is easy to see on Realestate.co.nz. I will follow these homes to see how these asking prices may change. Would be helpful if others choose an area as well.

Wow what would be reason be behind the difference in numbers, and by such a large amount?

Hi Trapped Millennial, I started collecting that data recently.

The change in listing type (Auction/Asking/Negotiation) is plain as day, with over 1000 auction listings in Auckland when I started now down to 600. The number of asking prices / price by negotiation has increased over the period as well - the total number of listings is roughly unchanged.

Table with numbers below, apologies but the formatting doesn't come through very well.

record_date | auctions | enquiries | tender | deadline_sale | asking_prices | price_by_negotiation | total

-------------+----------+-----------+--------+---------------+---------------+----------------------+-------

2018-11-03 | 1007 | 250 | 71 | 136 | 3405 | 2538 | 7456

2018-11-05 | 726 | 141 | 42 | 86 | 1790 | 1577 | 4393

2018-11-06 | 1014 | 240 | 72 | 141 | 3423 | 2553 | 7493

2018-11-07 | 1056 | 248 | 73 | 144 | 3434 | 2580 | 7582

2018-11-08 | 1073 | 253 | 69 | 151 | 3465 | 2610 | 7668

2018-11-09 | 1058 | 240 | 64 | 150 | 3506 | 2611 | 7676

2018-11-10 | 1049 | 239 | 63 | 150 | 3525 | 2603 | 7676

2018-11-11 | 1042 | 241 | 63 | 151 | 3524 | 2609 | 7677

2018-11-12 | 1023 | 240 | 59 | 148 | 3498 | 2604 | 7619

2018-11-13 | 1039 | 240 | 55 | 147 | 3510 | 2590 | 7630

2018-11-14 | 1047 | 247 | 57 | 153 | 3526 | 2581 | 7659

2018-11-15 | 1000 | 247 | 62 | 150 | 3615 | 2623 | 7744

2018-11-16 | 999 | 248 | 61 | 142 | 3643 | 2624 | 7766

2018-11-17 | 994 | 248 | 62 | 139 | 3657 | 2611 | 7759

2018-11-18 | 992 | 247 | 62 | 137 | 3662 | 2605 | 7754

2018-11-19 | 963 | 247 | 60 | 132 | 3684 | 2602 | 7734

2018-11-20 | 943 | 252 | 58 | 134 | 3707 | 2608 | 7746

2018-11-21 | 912 | 244 | 65 | 133 | 3706 | 2621 | 7725

2018-11-22 | 887 | 242 | 62 | 123 | 3715 | 2671 | 7744

2018-11-23 | 851 | 246 | 58 | 127 | 3745 | 2680 | 7756

2018-11-24 | 454 | 94 | 35 | 57 | 1342 | 909 | 2919

2018-11-25 | 838 | 251 | 58 | 129 | 3749 | 2688 | 7757

2018-11-26 | 799 | 257 | 56 | 127 | 3737 | 2666 | 7686

2018-11-27 | 764 | 250 | 56 | 124 | 3756 | 2671 | 7666

2018-11-28 | 720 | 253 | 54 | 124 | 3770 | 2676 | 7642

2018-11-29 | 662 | 256 | 50 | 111 | 3760 | 2710 | 7594

2018-11-30 | 610 | 261 | 46 | 107 | 3798 | 2727 | 7593

2018-12-01 | 607 | 261 | 46 | 106 | 3783 | 2707 | 7555

2018-12-02 | 604 | 262 | 46 | 105 | 3779 | 2709 | 7550

ShoreThing - Great Work. The spin doctors will be spinning when they see there are people who dont buy into there spin.( I feel my head spinning.)

Thanks Tony. My plan is to pull all of the listings and all of the sales information in NZ, and present it nicely for anyone to view, no spin involved.

ShoreThing - I would love that. Maybe interest.co.nz would make that info a feature article !

Good man.

Looking at Auckland, the number of *new* listings down by 17%, total number of listings up by 5% compared to 2017. Could this be the result of more properties rushed into the market pre-FBB as opposed to previous years? I.e. properties that would have been put on the market in November under normal circumstances were hastily put up for sale a few weeks earlier.

I make the increase in AKL total listings 11% over last year

Also a huge increase in homes not selling. When a home doesnt sell it is not included in the data that makes up the average amount of days on the market to sell. The facts can we twisted to look however the media/banks want. Coaxing in a few more loans before the bubble bursts.

As the year's foreign buyer stats suggested would be the case, looks like the only noteworthy effect of the ban will be on Queenstown.

Damn it, I was really hoping the property market would just collapse.

Hi Nzdan,

Me too!

I’d love to pick up a sunny villa in central Auckland for a song........

TTP

TTP - Well the DGM's certainly want the market to collapse some back to 2002 levels so they can buy at those prices that they wished they had bought at back then. Then of course they would be quite happy about the market rising........

Yet instead of learning from past mistakes, they advise prospective first home buyers to follow in their miserable footsteps and not buy, even in a "buyers market". Misery loves company after all.

Well given that I was 12 years old in 2002, the only mistake I made was not being born a decade or two earlier.

We can all say that. I should have bought the 5 acre section next door to me back in 1990 for $60K when I was 20 years old but I preferred cars and a new motorbike .No point looking back on what was.

But I thought it was only Millennials who were frivolous with their finances.

Are you Tony Alexander ? He was saying the same thing on a one roof video. It Tony says it - IT MUST BE TRUE !!

"Well the DGM's certainly want the market to collapse some back to 2002 levels......."

Some DGM's would like to see house prices fall back to 1902 levels.......

But even then, I reckon that some of them couldn't afford a house.

TTP

But they wouldn't want to live in a 1902 house.

Housing market is down and will remain so for sometime to come.

What has to be seen is how much it can and will fall.

My friend is a buying a house in Pakuranga Heights - earlier free standing house were going between 900s to a million and now can see asking of mid 800s so have changed from 900Plus to 800Plus ( fall of minimum 10%).

Same in Bucklands beach, Sunnyhills, Farm Cove, Howick and near around area - can see fall of minimum 10%.

Never mind the data Richard1965, just believe what you want and proclaim it to be the truth, cult like

Yvil - Never mind the data Yvil, just believe what you want and proclaim it to be the truth, Sheep like.

Sheep like behaviour is to do as others do, like regurgitating their posts

Ground reality is that good houses are getting sold if reasonably priced to match the market expectation (That is atleast 10% to 20% below RV as of now depending upon the house with few exception).

Going forward for short term all indicator is that will go down further as one has to wait and watch the effect of the law changes from 1st January 2019.

I'm guessing you've just pulled those figures out of thin air?

Auckland RVs are based on the re-evaluations that were done in July 2017. The REINZ median for Auckland in July 2017 was $830,000. The latest REINZ data we have is for October - the Auckland Median is $865,000.

Auckland market prices (median) are 4.2% higher than when RVs were done

https://reinz.co.nz/Media/Default/Statistic%20Documents/2017/Residentia…

https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2018/Reside…

Out of thin air.....

My friend just go on trademe and see the properties listed in Manaku and can compare asking price or price expectation to RV and can also check with real estate agents.

But do you not think there might be a bit of a shortcoming with your approach of looking at just a select few Trademe asking prices in just one part of Auckland? Or just asking some random agent? Not the most scientific approach, especially when we have comprehensive sales data available that paints a very accurate picture of what is actually going on.

..."But do you not think there might be a bit of a shortcoming with your approach" given you are quoting a median index?

Median indices don't "paint a very accurate picture of what is actually going on."

If you want to do that, quote constant quality indexes. Not medians.

Greetings, word salad man.

Median is a very good measure, which is why it is so widely used. Certainly paints a more accurate picture than mean. Every measure has its strengths and weaknesses. HPI for October 2018 is marginally higher than July 2017 when RVs were done.

Today's word salad tip - no need to add "indices" after "median" to try sound smart. It's superfluous and technically speaking the REINZ median data isn't an index, unlike the HPI. When talking property values, an index measures price changes from a specific starting point.

Nope.

It's widely used because it is simple and has low data reliance. Because of that, it is very crude.

A good summary of why the REINZ went through the process of finding an alternative is here.

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Analyti…

"HPI for October 2018 is marginally higher than July 2017 when RVs were done."

Okay, so now when using constant quality, we don't need bold font.

Neither of you were right, but you were both making points as sensationalised as each other.

"Today's word salad tip - no need to add "indices" after "median" "

Sorry. The 3 syllables threw you again, right?

Will avoid using anything more than 2 syllables in the future.

Why are you lecturing me on the advantages and disadvantages of different price measures all of a sudden? Everybody knows this stuff already.

"low data reliance" . Sunshine, what the heck are you talking about, just more word salad out of you. The HPI is 100% reliant on "data".

"Everybody knows this stuff already."

Well, you and the others obviously don't.

Sorry. "re-li-ance".

3 syllables, again.

Low data reliance means that it doesn't rely on access to detailed sales data.

It needs but two bits of information; the transaction price and the sales date.

I mean this in all seriousness, based on clear evidence in your past comments, so it isn't ad hominem - You are not an intelligent person.

Everyone on this site will already know what the HPI is and the advantages that it has over mean data. You preaching about this rudimentary information as if it is complex and needs to be explained does you no favours.

Oh god. Cmon, man.

The median index and HPI (SPAR) are different, mate.

Median (what you first quoted and I was contesting and you commented on): relies on transaction and sales date data, only.

HPI (SPAR method): relies on transaction, assessed value, sales date, and assessed value date data.

The median index is not the REINZ HPI, which is not the REINZ Hedonic HPI.

EDIT: thank you for editing your comment in acceptance of your misunderstanding.

I already know all this! You're not smart for pointing it out!

Oh. I'm sure you do.

Yet you literally just consciously typed out a comment confusing the two before editing it upon your realisation of how incorrect you were.

nymad, a cornered Spruiker is easy to find. Just follow the trail of insults.

Ahhhhhh the property bear has woken up, just in time for summer.

Time to go back to sleep, housing market is still in winter

.. a long winter it's been, but the smart squirrel can still find a hearty meal

You think I don't know the difference between median and the HPI? Do you realise that even a monkey would know the difference between these? I only edited my comment because on first glance I thought that you said that the HPI is reliant on only two pieces of information, which it obviously isn't. On second reading I noticed that you must have been referring to the median.

What is really interesting is that you think parroting information about the HPI that everyone already knows makes you smart.

Not so sure median is the way to go, if there are lots passed in or sitting in stock.

A straight median on completed sales (REINZ data) is arguably not really better than data based on all stock (say, something like an AVM).

Riddle me this - if 100 properties are for sale, and only 30 sell, the median would be the 15th property value. But imagine the other 70 properties failed to sell due to low demand or unrealistic expectations .. under a median sales figure, we just imagine they aren't there. This can paint a misleading picture, especially if the 30 that did sell were upper end and the 70 that didn't wished they were. Now, in all likelihood, the 70 who didn't sell probably still want to, but there may be a lag.

Thin Air is what happens to our comments when we mention a certain youtube website.

@ TTP, "The housing market remains steady". Captain of the Titanic said "steady as she goes" when it hit the berg..

More noise to prove otherwise.

In this case everyone know that the current boom is over but will hear lot of noise from people / so called experts, who are not ready to accept the reality. By shouting are not trying to convince other but themselves by giving some hope.

I don't think anyone is disputing that the boom is over, it is. What TTP and others you call spruikers are saying is that the housing market is not "crashing", "falling off the cliff" etc

And most peeps that TTP disparagingly refers to as DGM's are saying that the fundamentals still indicate house prices are overvalued as an asset. Increasing stock and days to sell in the largest market (which set the speed on the way up) are a worrying lead indicator.

Of course, some others wave more vigorously on 'crash signals' and make out interest rate competition is less about free market measures and more about conspiracy theories.. but I, like most on the site prefer data science and more robust measures.

Hi Chairman Moa,

That's a very odd comparison....... and rather short on veracity.

Titanic was a ship - not a house.

TTP

TTP - yes but both thought they could not go underwater !

I can confirm that Auckland is under several mm of water today. Do you think this is a sign?

Agreed. So much for summer, kind of like the massive Chinese and summer boom that all the Bulls quoted up until recently. Consider for a moment that the last of the Chinese, and the usual summer bull run is happening...right now. What will Q2 and Q3 next year look like?

Hi tothepoint,

Look up "analogy", most kids learn this in primary school. However not all, it would seem.

MTP

Hi Mrs The Point,

Look up the word "veracity".

A good analogy should NOT mislead or deceive.

TTP

out of interest, in what way does this specific analogy mislead?

Are they not free to draw analogous inference:

1. Both Auckland housing and Titanic assumed to be solid and dependable

2. Right up until it sunk, Titanic was referred to as unsinkable. If the same was to happen to Auckland house prices, the same would be said

3. Right up until it sunk, Titanic was observed to be unaffected by the iceberg/s, until it hit it.

To be clear, I am not personally the one drawing the analogy and make no inference as to whether it is fitting, but it is in fact misleading to say that such an analogy is misleading.

"Titanic was a ship - not a house" fair call ! But one is about to be sunk to the bottom like the other one!

For a quick comparison, in Sydney over the weekend, the auction clearance rate was approx 40%. What was more interesting is that the median price of houses was down 22% compared to the year before. Of total sales (houses and units), the total monetary value of auction sales was down over 70%. The average sales price was down over 50%, which probably means that only the "cheapest" properties on the auction market are selling.

Make of it what you will.

For the 65204 homeowners that have purchased an Auckland property ( about 12 percent of all stock ) since March 2016 , how do they currently view their asset, given that the median price (the metric without all the bells and whistles) has flatlined for 30 months . Without sales volume prices will continue their descent .

It is hard to poke a hole in that cowpat.

I can;

Quote: "given that the median price ... has flatlined for 30 months . Without sales volume prices will continue their descent"

How can "prices continue their descent" after you say "the median price has flatlined for 30 months"

Yvil, median price peaked March 2017. Prices have been descending for 1 month short of 18. Interest co,supply plenty of very informative charts,RBNZ supplies hugely important credit data, and a brisk walk around the block provides a few visual clues.Nothing amiss with my comment.,don't stand in the shit.

There certainly is something amiss, you say

"given that the median price ... has flatlined for 30 months"

that means prices are flat, as in not going down, yet above you say

"Prices have been descending for 1 month short of 18"

Do you not understand that you are contradicting yourself? Prices cannot be flat and descending at the same time

Yvil, take the second letter of your name, flip it over, draw a horizontal line thru it ,anywhere.The horizontal line is your time axis,you can work out what the vertical axis is. Oh,the pointy bit on top ( no ,it's not too pointy) ,that is March 2017.As of today ,that horizontal line will go lower. Go get some crayons, colour it in if you want,frame it.

Glad to see you admitting that you were contradicting yourself

The way I view it is that those new homeowners will have different perspectives based on their reason for buying. Those that bought to live in the house and make it a home are probably fine with flat prices. Those that have been speculating and planning on flipping the house are probably more concerned as a flat market means a definite loss.

People could also ask why current house prices are so secretive. When prices go up they get discussed loudly.

Actually very well!!!! Doing well with our purchase May 2016 and no complaints, thanks for asking.

Hahahahaha.

The house is in ellerslie, a favourite middle-class Auckland suburb, house value up over 50 percent from what we paid. Howszat!!!

I noticed quite a few Auckland listings being pulled from mid to late November when they weren't selling and the December Xmas period was looming. Watch many relist in February with a surge of listings coming on to the market. December and most of Jan are usually bad periods to sell in for Auckland.

Adam BNZ - Good point. Old stock coming back on the market, ( mutton dressed as lamb). New Stock rushing onto the market ( 2 months worth ) . 2019 will be the year of fighting !

Yes, they usually dump them on the rental market in order to cover the mortgage over the holiday period then relist them with tenants in place. I feel sorry for the tenants.

The old saying, one swallow doesn't make a summer, but data suggests catch-up here in the Hawkes Bay may becoming to an end after period of sustained double digit growth over past few years.

The Auckland influx fuelled a lot of that growth rate. Is exodus from Auckland slowing as Auckland FHB start to look locally as affordability improves in Auckland? Or is that too big of an assumption leap?

printer8 - you only need to look at the advertising is moving to an Asking Price ! Not to mention the 450 sections privately coming onto the market in Havelock North alone. And then there is a huge amount coming onto the market in Hastings privately. And Clive privately. And Napier privately. realestate.co.nz. wont show this, interest.co.nz wont know this. Very interesting to see the cracks happening before the Avalanche.

People I know who have left Auckland arent FHB's, they are the Mum and Dads cashing up the over priced house, buying a less overpriced house in the provinces. Then looking to buy themselves a job by buying a business. They also put in a pool (I have a customer in HB with 2 years of pools ahead of him - mostly to people I describe above).

They are the Marginal buyers in the provinces.

dp - apologies poor internet connection (island resort)

I hope you're frying, (frying the fresh fish) haha

How can this below data be correct

https://www.newshub.co.nz/home/money/2018/12/prices-plummet-in-queensto…

It says is derived after adding all the asking price of properties listed (Not sold price) and dividing by number of property.

Earlier during boom properties were sold at asking price, if not more but today properties are sold much below asking price or price expectation SO in reality if the properties are being sold below the asking*price, the FALL is much greater in actual term when comparing price of properties being actually sold.

May be that is one of the reason their is a difference between data which says 1.8% in Auckland but in reality is much more of houses being sold.

alittle - The most simple advice I can give to anyone right now in regards to getting correct information is , FOLLOW THE MONEY !!! Is it in there financial interest to spin ?

Correct Tony Turner

Hi alittle, you need to remember that Realestate.co.nz is a property listing website. It advertises the properties that are for sale, and aggregates their asking prices for its reports, but it isn't advised of the selling price once a property has sold. So it can't provide details of the difference between asking prices and selling prices. Unfortunately it has always been that way. But movements in average asking prices are still a worthwhile market indicator to have.

Hi Greg, Thanks and I know but when the market has just changed (Since last month) - Asking price will always be high as it takes time for the vendors to realize and drop the asking so the actual fall may be much bigger than the hint that such data produces.

Asking prices are like farts... merely a prelude to something more significant.

Except that a fart often precedes something more substantial.. Selling prices are rarely more substantial than asking prices.

Pragmatist - Maybe he means a substantial clean up in ones pants ! When denial turns into reality.

from across the ditch

"Sydney property values have now fallen 9.5 per cent since they peaked in July last year and will likely surpass the largest downturn on record, according to CoreLogic's head of research Tim Lawless.

The slide in prices accelerated in November, with national dwelling values falling 0.7 per cent, the weakest monthly result since the global financial crisis, led by a 1.4 per cent decline in Sydney and a 1 per cent drop in Melbourne, CoreLogic's latest home value index showed.

"For Sydney, 1.4 per cent is the biggest monthly fall we've seen so far this downturn. The last time we saw a bigger monthly fall was back in 2004 but that was only one month and otherwise you'd have to go back to 1989 to see values falling faster than this," Mr Lawless said.

"If you look at Sydney's largest downturn on record it was 9.6 per cent during the recession between 1989 and 1991. It's likely Sydney will set a new record in terms of the magnitude of price decline and the length of decline," Mr Lawless said."

kane02 - Auckland typically follows Sydney. EEEEEKKKKKK.

yes Tony Turner. That is why Orr's comments last week ring hollow to a lot of us. Of course NZ could continue on its merry way of endless price rises. However we could equally be back 10+% in a years time. Why bother cobbling together a deposit when it could vanish into a puff of smoke. Smart buyers will wait it out.

yes Tony Turner. That is why Orr's comments last week ring hollow to a lot of us. Of course NZ could continue on its merry way of endless price rises. However we could equally be back 10+% in a years time. Why bother cobbling together a deposit when it could vanish into a puff of smoke. Smart buyers will wait it out.

Hush! Kiwis prefer to assume immunity from overseas trends, which can be scary.

Adrian Orr is still confident about keeping a low OCR forever despite this chart.

Keep in mind that Adrian 'told' us some time back that if overseas rate rise he'll drop the OCR to balance the effective cost of funds to the local market. Madness, in my opinion, but it makes sense in some deluded way if you think any rise in mortgage rates will bring on Armageddon....

mogador - Argentina has a 60% rate. I guess there R.E Agents are saying now is a great time to buy !

51 Houses in my street. There had been no listings in my street in the two years until October 2018. 5 Houses now for sale. None selling and no-one attending the open homes. Green leafy suburb. Im not selling but friends are selling the house they just built in a hole in the front of their section. Asking $2.5million...no interest for three months.....put a time limit on sale and said it would sell on Nov 10th. Auction then cancelled and back on the market with an asking price of $1.9million. Still no interest. Affluent area. Good schools. Auckland central. Last thing i want is a house price collapse but if the truth be told.......it feels like its sliding and there is a stand off between buyers and sellers .

I had to laugh at the ad showing a 5% cut in asking price on a house immediately below this line:

"The average asking price of properties available for sale on the website dropped back from its record high of 704,002 in October to 671,528 in November (-4.6%)."

The only people that will do well out of this cycle is the home staging business. In the hay day, any old sheds can be sold for good money regardless of the look and feel.

Now, you have to go one step further to be better than other properties in the area and to attract buyers.

If you can see a rat's nest for $500K, there's every reason to be happy. From a buyer's POV, it's only worthwhile if luck plays a part on its future value.

Chairman Moa - Home staging business, well that may look like a murder scene soon. Hang a few corpuses around the place, maybe some blood up the walls, plenty of cob webs from days on the market.

Resident Spruikers are clinging to a dubious (median) dataset. Mounting evidence that a growing line of disillusioned Auckland vendors are unable to realize their 2017 CV, makes a complete mockery of the REINZ median.

Like it or not, Auckland IS going to follow Sydney down. Additionally, the FBB ban has quickly made its presence felt, first in Queenstown, and through 20 percentile results with Auckland's biggest agent B & T.

Agreed. The significantly increased money laundering disclosure comes in at the start of January 2019 to boot. What - I cant use a local Lawyer to front my company or trust....well yes but your name and registered address must be listed as the ultimate owner/beneficiary and the source of your money.

History shows that Auckland lags Sydney by up to a year. A lot can happen in that time. Aussie clearance rates are being cited as a disaster at plus or minus 50%. Are we still calling 25-30% "stable"?

i have family in perth that brought in 2009 that have been trying to sell for six months to move back, being a jaffa he refuses to sell for less than what he paid so his family have returned and he has stayed until house prices turn and he can sell for what he paid.

my guess i will have a few more years of cheap holiday accomodation yet

https://thewest.com.au/business/housing-market/more-perth-property-pain…

He might be in luck! WA mining boom is about to start again, although this time there will be less FIFO so he might be ok.

I thought Iron ore prices were heading South again ?

I can confirm thats its starting to pick up significantly. Phone calls for roles in the mining sector has increased exponentially. Double the wages then in NZ, half the price to live...btw need a brand new 4x2 near the beach for less then $350k? NZ is terrible if you want get ahead for a young family... thats why we had to return...

than...

So long as the Median buyer in the Auckland market has around $865k to spend then the reported Median sales price isn't going to fall. Real house prices could in theory fall 10% as vendors compete for buyers with no change to the median house price statistics. If there's no change to the reported statistics then buyers won't adjust their spending downwards.

Infact, if potential buyers are starting to see some more valuable properties within their affordability range, it might be easier for REA's to condition them to extend to the upper limits of what they have to spend.

E.g. Someone with $865k to spend could have settled for a 2.5 bedroom place on a 300m2 section 12 months ago might now be able to pick up a 3 bedroom place with a 500m2 section in school zones. They're still spending $865k, there's no change to their position in the median price distribution.

The vendor is happy, they only paid $450k for the property 10 years ago so they've made $800 per week, it doesn't matter to them that they could have sold for $950k 12 months ago.

"The vendor is happy....it doesn't matter to them that they could have sold for $950k 12 months ago."

What could that tell us? That the vendor doesn't expect prices to recover to $950k and they are getting out before they see the price deteriorating further? After the '10 years and it's tax-free period ( NO, it mayn't be!)" why wouldn't they hold on for another year or two if they thought they'd get another $100k out of it?

Answer: They don't. In fact, they see this as 'it' - the best they are going to get before it gets worse.

I'd say the vendor is (most vendors are) unaware that they could have banked extra for their homes 12 months prior, they're choosing to sell when they think is best for them. Before anyone jumps on me, I am talking hypothetically.

People get so hung up on median sale prices/% over CV, cheering for the resilience of the "housing market" when infact these statistics probably speak more for buyer's access to credit than stability in value of the housing stock. The only pricing guides we have for housing is sales averages/medians and RV. There's no floating market "spot price" above every house, with month on month historical data behind it.

I think there could be an improvement in buying power happening but no certain way of measuring it, except anecdotally. But only a fool would provide anecdotes to support this argument, they'd be labelled a cherry picking DGM.

Excellent example (hypothetically) on the dangers of median measure with limited or lower sales numbers.

"Westpac has a new Division called “Expenditure Verification Team”. They have investigators following you around to see where you spend money"

(Comment from Australia, and I'd guess they follow your electronic trail to make sure that what you have told them about your expenditure, matches what your actually spend.)

Things are going to get a lot worse before they get worse:

Tony Alexander says it will all be sweet on that video. God bless Tony and his benevolent employers.

Still spruiking the market ... Good old Tony.

But unfortunatley old Tone the 'credit impulse' is easing. Our economy only functions if the banks can sell more than $63 billion dollars of mortgages next year. Not sure if there is the appetite for that at present.

GDP, jobs etc etc all rely on 'The housing market, which is in the hands of people who want to step up and borrow.' (Adrian Orr, November 2018)

Just checked what had happened to some of those places that didn't sell at Auction when I ran that little pool. Interesting thing i noticed was that the homes.co.nz estimated prices for December are mostly lower than they were for the same properties last month.

One example is 29 Codrington Cres. Homes range was $2.465m to $2.915m, this month its $2.3m to $2.7m. RV is $2.9, and asking is still at $2.7m since the auction. But now there is competition, the neighbour is selling too.

A few have gone up, 2/22 Regina in Westmere is up slightly from 1.54-1.845 to $1.6 - 1.9m.

Nic, you haven't given us an update on Trade Me listings for a while, how many are there and how do they compare to previous numbers?

Thanks

Possibly falling listing numbers ... at least not going crazy skyward

Trade me 13207 for Akld

Realestate.co.nz 13916 for Akld

I expect these will continue to fall till late Jan, nothing can interfere with the Kiwi xmas holidays!!!

Thanks theglc

Nic Johnson - People like Tony Alexander should actually be held to account for enslaving a younger generation. Also for destroying young families and recking peoples health. But usually people like that slip out the back door before judgment day.

Tony

We'll see what happens over the next couple of years I guess. JK jumped first and resigned, then Theo did a runner from Fonterra, then Ashley Church resigned from the Property Institute. Be interesting to see when Tony tenders a resignation or retires perhaps!... Time will tell.

Nic

NJ - I think Tony Alexander has more credability than any of us on here, you don't get to be the top economist for the BNZ trolling these columns. I have followed him for atleast 15 years and from my experience he is as accurate as anyone could be. Infact he is directly responsible for adding atleast an extra 2 mil to my portfolio simply by painting a clear picture about what is really happening in our economy. I get you don't like him but I would encourage anyone to follow him over time and make their own conclusions and not follow the rubbish written in the columns here.

Agreed, I have a lot of respect for Tony Alexander

Our most respected commentator has a lot of respect for Tony Alexander. God bless you Yvil, that made me smile. I'm sure Tony will invite you over for a garden party to celebrate his retirement when it comes.

I'd just love to hear Tony A talking about bank 'credit creation' and the 'credit impulse' you know good old economics stuff that you'd kind of hope a good economist would want to talk about.... But is he an economist or a mortgage salesman these days? Anyone ever spotted him at an investors seminar?

Thanks for the compliment Nic

And yet he was sidelined by his boss

Shoreman - The smart money sold up a long time ago because they are getting themselves positioned nicely for the crash. Can you please send me a link of were Tony Alexander is teaching you this ? I do hope that extra 2 mil you say Tony has made for you is not still tied up in perceived wealth, (Real Estate).

Well if it took only a month and a half or so for property prices in Queens Town to fall 20% I think the outlook else where is also a bit grim.

I was looking around Wellington over the weekend and realistically there is room for a lot more houses. Not on the Mirimar peninsular perhaps but there is plenty of room over towards the wind farms. Challanging terrain perhaps but not insurmountable.

Really it's all about making the land available and saying too bad to the encombants.

In the absense of any credit shocks it’ll still be business as usual. House prices are largely inconsequential to the majority of home owners who are buying and selling in the same market. It’s just churn.

"In the absence of any credit shock". What do you think is happening now, and has been for nigh on 18 months?! And...it's going to intensify.

DTI may not be an official number, but go into your friendly lender and see what wringer they put you through before they grant you a(nother) loan or extension.

I was a first home buyer less than 18 months ago, and it was already tight back then due to the Responsible Lending Code hence I'm with a credit union. I never said there won't be a shock to the system, but mortgage lending has still been consistent and interest rates have still been low hence it's business as usual.

If you did a 5 years interest-free, or 2 a years fixed, it will be interesting to see what rate; what amount or if you can refinance. But if it's any consolation mortgage rates will likely be lower then that they are today...

Business as usual? Maybe business the way it used to be - 30 years ago - when lenders looked at the only metric that matters - the capacity of their borrower to repay.

2 years fixed on $165k. Interest rate is 5.5% which is on the high side, but not a huge deal on a $240 per week mortgage. Will look to secure a better rate at the end of our 2 year.

Hi Nzdan,

That's a salient point - but it's often neglected here.

Indeed, investors (and homeowners) are generally in property for the long haul.

On a monthly/yearly basis, yield is typically more of a focus than prices (and capital gain).

TTP

For investors yes, for speculators no. A lot of the posts are directed at speculators, and I think some of the professional investors get their backs up thinking its all bout them, it is not.

Core logic estimated value for my home at 100% of CV on 25/11/18 has dropped to 97.8% on 2/12/18.

That's 2.2% in 9 days!

So can we extrapolate that to an annual figure?

Depends what confirmation bias you are operating on. It was down at that level a few changes back and bounced back to 100%. I suspect it's just noise as there can't be many sales each week to base it on.

I have run a TradeMe and RE.co.nz search for over two years now, and both sites are showing a record number of listings, up 10% from last years peak. This is in Christchurch, and covering 14 suburbs. Not much is selling, but at the same time, prices don't seem to be being reduced. Its a stalemate - and I suspect come next February one side is going to give up.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.