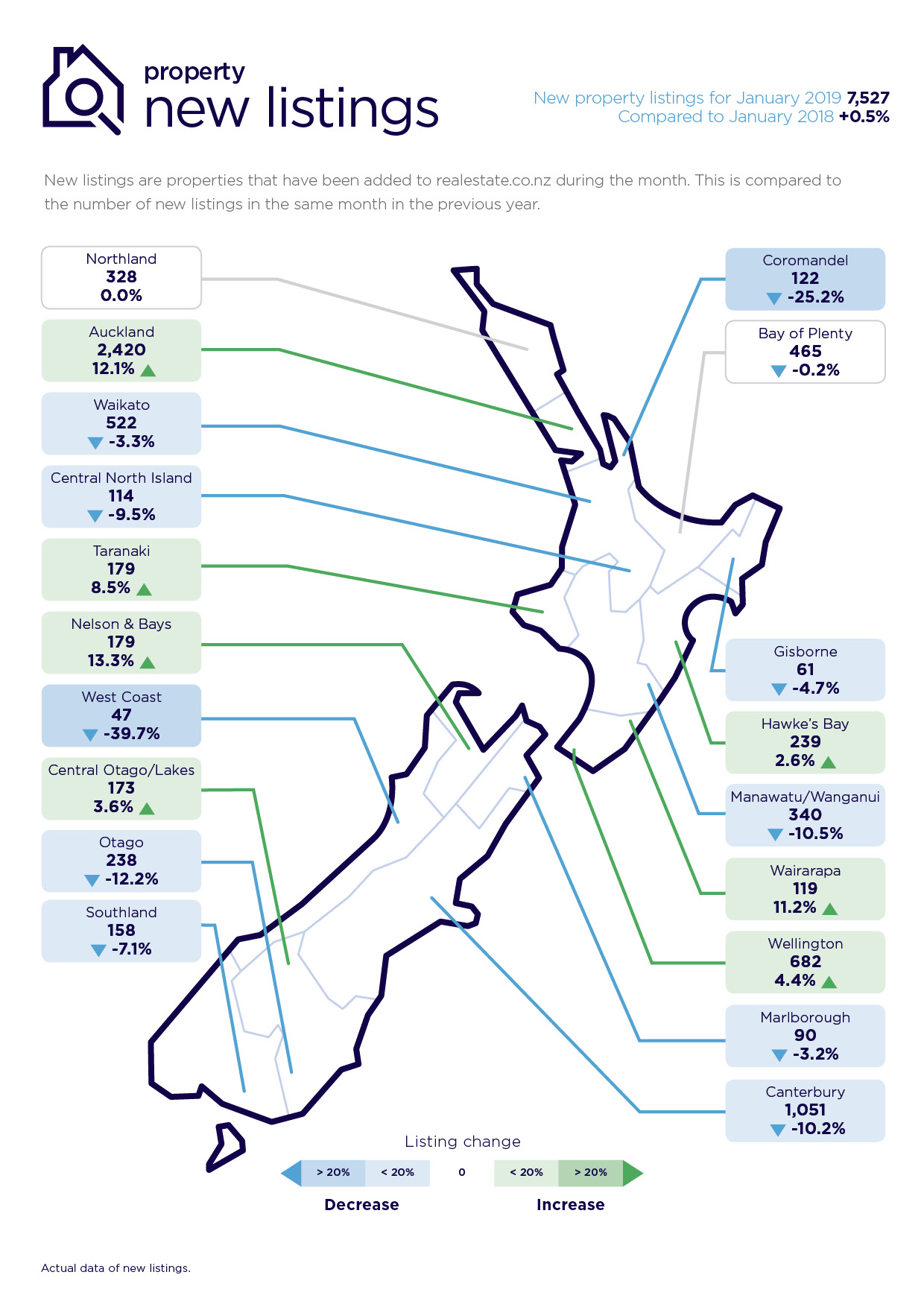

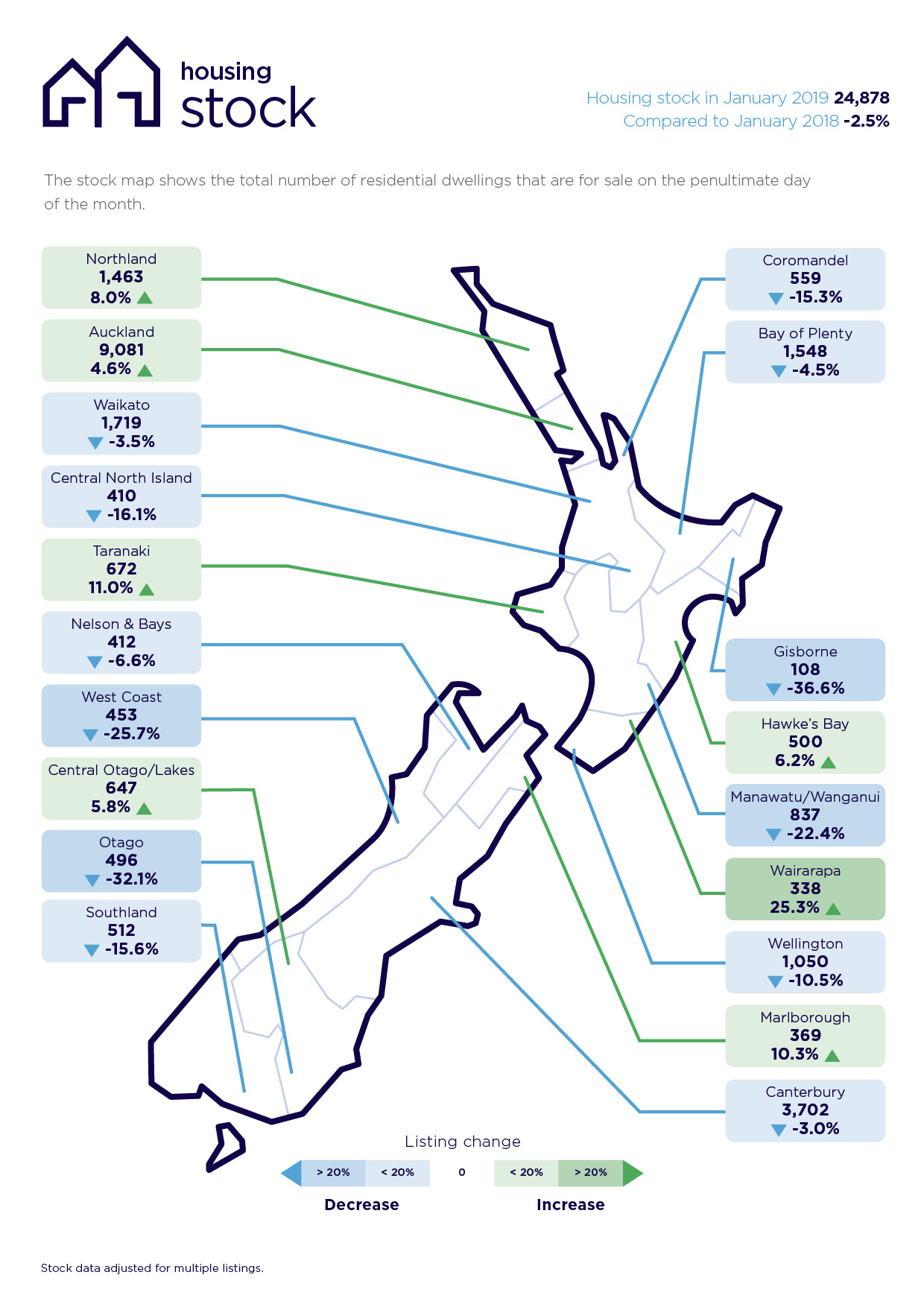

The housing market appears to be starting 2019 with new listings and the amount of stock available at similar levels to the start of last year, according to the latest data from Realestate.co.nz.

The property website reported it received 7527 new listings in January, up just 0.5% compared to January last year.

And there were a total of 24,878 residential properties available for sale on the website at the end of January, down 2.5% compared to January 2017.

That suggests a reasonably steady market, because there hasn't been a rush of new listings and a build up of unsold stock, which could point to a property market downturn.

And there hasn't been a major decline in stock either, which could indicate a shortage of properties and an overheating market.

So it appears to be steady as she goes, although the figures suggest some significant regional differences.

In Auckland, Hawke's Bay, Taranaki, Wairarapa and Central Otago/Lakes, new listings and inventory levels were both up compared to January last year, suggesting buyers in those regions will have a reasonable choice of homes to buy.

That should take some of the pressure off prices in those regions.

But in the Waikato, Coromandel, Bay of Plenty, Gisborne, Manawatu/Whanganui, West Coast, Canterbury, Otago and Southland, new listings and inventory levels were both down compared to January last year, suggesting the market is firmer in those regions.

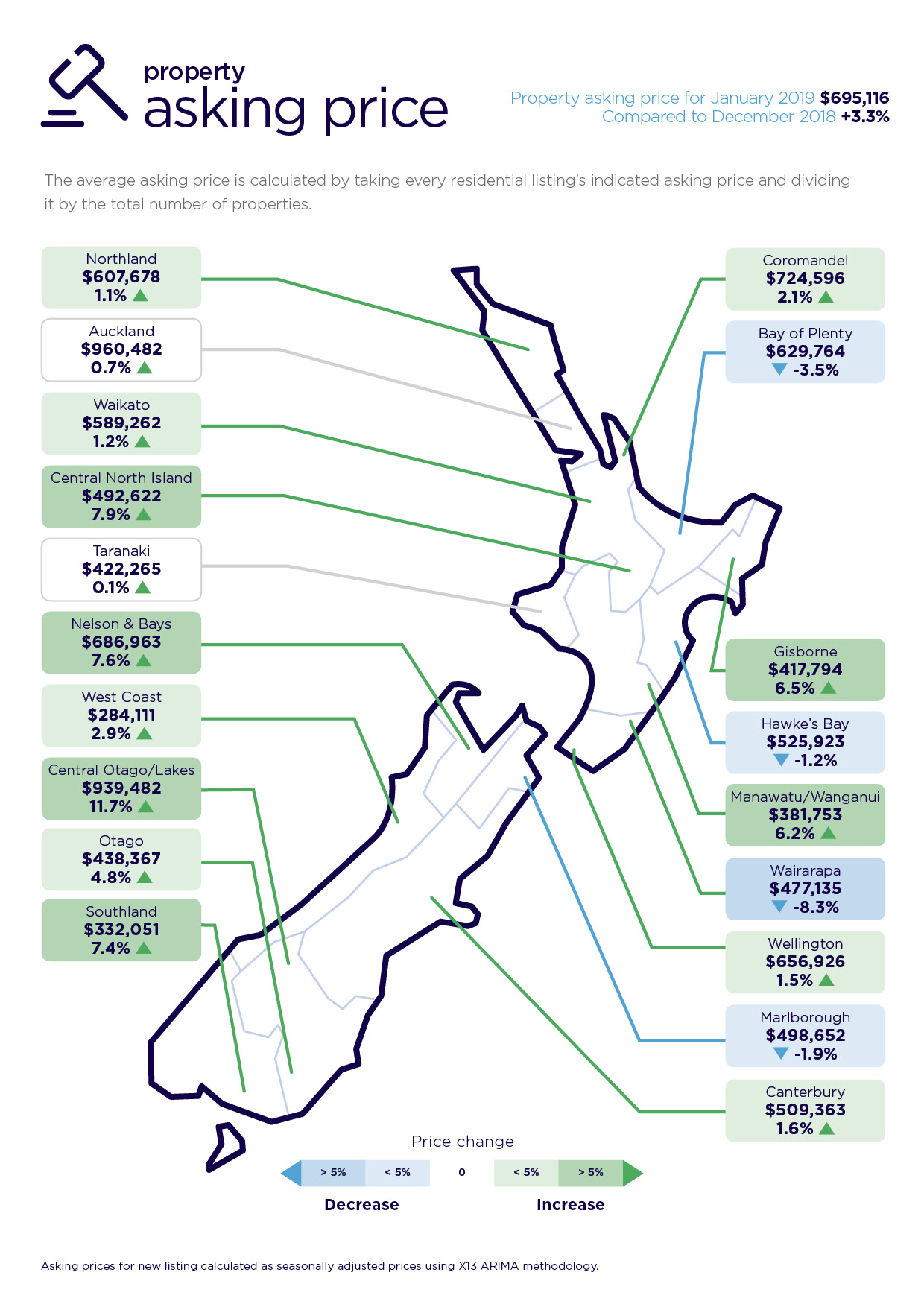

The average asking price of the new listings the website received in January was $695,116, a record high and up 3.3% compared to December.

However in Auckland the average asking price was up just 0.7%, and in Taranaki it was up just 0.1%.

"The Auckland market is favouring buyers, with a fresh injection of new listings, a flattening in the average asking price and a slowdown in the time it takes for properties to sell," Realestate.co.nz spokesperson Vanessa Taylor said.

See the charts below for the full regional listing, stock and asking price figures.

86 Comments

There is a reduction on buyers available this year, but only by around 3% so as you say steady as she goes.

All those cash stuffed briefcases all but gone, all Spruikers are left with is this song...........https://www.youtube.com/watch?v=y3KEhWTnWvE

Those were the days my friends, you thought they'd never end ;-).

Question, will "those" glorious enriching days ever return?

Answer, since you're deep down wondering why the exit door looks so easy on the eye, you already know the answer to this question.

At times I catch myself wondering what it must be like to suffer debtors paranoia.

Ok so you are saying in a rather ambiguous (look it up) way that the growth property market is over and will not recover ... ever. There you are readers, in returned poppys world the curtains are shut and the lights are out...and....the enquiry into establishing a capital gains tax is a huge waste of time and money because the market has either been scared into obedience or is completely exhausted. GR and JA please take note and adjust your budgets accordingly to remove any prospect of tax revenue from the capital gains of properties.

...never ever - ever you say? Sounds frightfully gloomy. Are you okay? I tell my kids that many opportunities await their expanding deposits and longer term it always pays to own your own home. Its liberating, especially when your past the milestone of not having to pay dead money in rent or mortgage interest.

Anyway, its you thats on record as having recently sold your only Hamilton rental. If something good has come from debtors paranoia, its you've left it to the professionals. These same professionals think nothing of providing healthy and warm accommodation to the masses. Well done you ;-)

After the decline, when the media headlines start saying it looks like the property market will never recover, THAT’S” the time to buy, not now.

yeah :) When it looks like things could not possibly get any worse - buy.

OR buy when you're ready, when still young and before starting family. Get an inheritance advance from Dad

Houseworks, did you demand an inheritance advance from your Dad? ---cringe---

When my kids want to settle down, I will offer further financial assistance, if needed and without obligation.

Well actually my father, good man he was, was a baker so when he retired he had no dough :) unfortunately

That's a a lot to chew on - spending the flour of your youth earning a crust and having nothing to show for it. I can only hope the work was filling - but sometimes you can't have your cake and eat it too.

Well put sfah hahaha

Get an inheritance advance from Dad

You realise the working class exists, right?

We have an egalitarian classless system here in Aotearoa. Classes were left behind long ago in the old country.

The older I get the more I think class is a good thing. When you have more money you should be expected to better your conduct as well, too many trashy boagans with late model holdens and speed boats - they should be going to the opera damn it.

Anyway substitute 'poor' for 'working class' if it bothers you that much.

I agree, a lot of people encounter problems when they don't recognise and accept their place in society. People should endeavour to be the best in their "class" before moving up a level. This is how the corporate world works. You can also have real pride in being at the higher level within your class and may be happy to stay there. I have largely followed this track in my career.

Great comments sfah and zs. Welcome distraction from the commonplace rubbish claims and personal insults

P&T Edu

I doubt you are proficient in Python or Tensorflow or even Swift

I've watched a bit of Monty Python and read some Jonathan Swift. Wouldn't waste my time with Tensorflow, sounds foreign.

There he is

The voice of spruiking

It must be very dull in the Bahamas. Not my cup of tea at all.

"But in the Waikato, Coromandel, Bay of Plenty, Gisborne, Manawatu/Whanganui, West Coast, Canterbury, Otago and Southland .... the market is firmer in those regions."

.... says it all

Surely as the boomer wave starts to retire sales in areas outside the overcrowded joy that is Auckland will increase. That along with economic refugees (cant own a house) will surely see other areas continue to grow.

As the Boomer ( and the War Generation, which is in full swing) waves start to die off ( and they have) their stock will come to market, one way or another, across the country. An judging from what I see those 'investments' outside of Auckland are not only in Christchurch, Tauranga and Hamilton, they are in Waipu, Monganui and Twizel.

If Greg sees a build-up of unsold stock as a precursor to a downturn, perhaps he should specify 'where' that happens? Is unsold deceased estate stuff in Twizel it? (NB: The answer is probably...yes!)

Its ok. The Bulls can buy everything at ask and rent it to....oh all the DINKs have left for Australia.

Exactly!

And here's the thing. Those who inherit a portfolio of, say, 4 properties aren't inheriting the assets as such, but the fixed costs. The Rates and Insurance etc that could be another $20k per annum that they don't currently have to pay. "But they can borrow to cover those!": Can they? Banks have gone to DTI, even if it's not official, and if the income isn't there, neither is the borrowing. So given the extra costs that have been inherited, what to do?

Sell !

"Banks have gone to DTI, even if it's not official"

So true, only way to top it up is the bank of mum & dad and what happens when they get wise?.....

bw, I didn't want to get involved but your comment is just plain wrong at several levels. It's not good to post fake information that some on this site could believe and use to make important decisions.

1) "Those who inherit a portfolio of, say, 4 properties aren't inheriting the assets as such, but the fixed costs"

That's wrong, you inherit the assets, the liabilities, the income and the expenses of these properties.

2) "The Rates and Insurance etc that could be another $20k per annum that they don't currently have to pay"

Yes and they also inherit the rental income to cover the rates and insurance and more

3) "Banks have gone to DTI, even if it's not official"

That's absolutely NOT true, banks assess a borrower by comparing their assets with their liabilities and their income with their expenses, NOT their liabilities (Debt) with their Income.

bw, it's wrong to post completely untrue statements that others could use to make very important decisions

Yvil, anyone who is making important decisions from the comments posted here is in serious trouble. Several people here are in the category of "The lights are on but nobody is home".

BW,

you raise an interesting point.

It depends on the unique circumstances of the property owners of multiple investment properties.

1) are the investment properties owned in the name of an individual or are they owned in the name of an investment vehicle such as a company, or family trust?

2) is the investment property portfolio cashflow positive or cashflow negative?

3) is the LVR of the portfolio high?

A) The most vulnerable are those who own property that is cashflow negative in their own names with high LVR's. Beneficiaries are likely to want to sell down given the required cashflow contributions to maintain ownership of the property.

B) Those that are in the strongest position to hold on are those with a positive cashflow property investment portfolio owned in an investment vehicle with a low LVR. Beneficiaries are constrained by the instructions controlling the investment vehicle (e.g trust)

The interesting question is how many are in category A vs category B.

Seen some fairly big growth in the Wairarapa over the past couple of years. Homes.co estimate has our property at 25% above purchase in 18 months, but anecdotally similar properties in our area have been fetching 5 - 10% more than that.

I think having access to a regular commuter rail service into Wellington has certainly helped drive the demand, despite the ongoing performance issues with the rail network.

There are plenty of houses in Wairarapa been on the market for months only to be taken off and relisted aswell

Nzdan, Auckland's expanding equity gave equity and prosperity to the regions, shrinking equity will take it ALL back.

It’ll take it all back and then some, as new builds are sold quickly by Aucklanders ditching, and some new developments left unfinished.

Exactly, just look at the Coromandel, 25% less listings, 15% less stock and rising asking prices

I know Schadenfreude is a big thing with you, and you enjoy frequently making unsubstantiated claims that people on here (myself included) are well over leveraged and on a highway to a hiding....equity has no real use for me as an owner occupier but if the bottom fell out of the market and my house was worth what the previous owner paid for it in 2007, i'd still be well over 20% equity.

Nzdan, again, I have never said you personally were over leveraged because you repeatedly out how successful you feel having a mortgage of just $160K. I will admit to having floated the possibility you might be suffering debtors paranoia?

Its a sound approach not hanging ones coat on unbanked equity.

Let's leave it to rest there shall we?

It's cool I don't take it personally, but you are all over the place. Try to be a little more consistent and throw out a few less assumptions at people. I don't normally go into the specifics but I mentioned my mortgage in response to your claim that I will wish that I held off on my purchase and that I have a relatively enormous debt. But yes, you were wrong so let's move on.

by Retired-Poppy | Tue, 29/01/2019 - 08:47

up0

Nzdan, in depth analysis has revealed its cheaper to rent right now revealing your views as being somewhat uninformed. An abundance of opportunities awaits those who watch this debt fueled unravel. As you witness this, I'm guessing you'll wish you had waited and patiently saved (a form of buyers remorse)Interest, insurance, rates and preventative maintenance are dead money too. Your precious capital gains are also unbanked and can be taken from you tomorrow whereas you still have your relatively enormous debt.

Nzdan, I think you just took it personally (sigh). In desperation, it appears making baseless assertions is now your thing. You'll need to be more thick skinned and honest with yourself. The key thing here is that interest.co.nz analysis on (rent vs owning) runs counter to your wishes and you're clearly a little pissed off. Despite your assertions to the contrary, amassing unbanked equity IS your cocaine and you feel by your own repeated admissions 'successful". You go on about your spot price capital gains to ad nauseum, deny it matters, then accuse others of doing the same thing. Unbanked gains on family homes shouldn't matter, but for you, it seems to matter greatly if it all drops. A potential candidate for debtors remorse.

It' certainly is cheaper to rent. Going forward, it's an amazing opportunity for the first time buyer to amass deposits with the backdrop of falling house prices. Just think of all that saved interest! It's better to receive than it is to give.

Nobody is pissed off here, I don't know where you get that idea from? I think you need to up the meds or have a longer day nap or something? You're really coming across more and more deluded by the day, and I'm starting to see why nobody on here takes you seriously.

It is cheaper to rent by 0.5% inclusive of rates, maintenance and insurance, as per the article you previously provided. It's in there, have a look. So technically you are right but by margin of error stuff.

Nzdan, yup, here we go ;-). You're so predictable. I think that four hours daily dose of train ride is taking its toll on your health. You often mention meds when retorting other commentators - why? Something in/on your mind? Again, be honest with yourself, stand back from it all and ask yourself "how can I liberate myself from this "success". BTW, did you factor in the expense of transport costs before you bought? It must be substantial.

Get some much needed rest, you need it. Enjoy your weekend :)

We can go around in circles all day exchanging jibes as a couple of strangers on the internet but it's childish. I did object to your comments and could have misunderstood where they were directed. Yes a four hour daily commute is taxing (but no way is it taking its toll).

I've made the sacrifices to support my family and provide the best for them. I didn't want to raise a young family hopping from rental to rental, and I certainly didn't want to buy into a position where we are over leveraged. I also have an employer that really looks after me who supported me throughout this move. So yes, this mind rotting rut is what I label success in 2019.

You have a good weekend as well.

Fair enough, I agree, its childish. You truly sound like a dedicated father and husband. In my earlier years I did a similar thing from one side of Auckland to the other - no kids back then though. Yes, I feel you did misunderstand me from the outset as my criticisms were aimed at speculative interest only mortgages. That's the point when you first jumped in and had a go at me - lol!

My employer (as much as they look after me) gave me 2 weeks notice to shift from Christchurch, just so I could work the remaining 2 weeks before Christmas. So I gave The Man 2 the keys to his rental and drove to the Wairarapa with the remainder of our belongings and our cat. Slept in the car at Picton with a howling cat in the passenger seat.

Wairarapa was one of the last to rise and fell the hardest in the 2000s. Especially Masterton. So I expect it to drop hard.

""People have placed to much weight on supply and demand imbalance in Auckland. They say there's a shortage of houses so house prices can't fall – that's baloney."

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

I'm sure that where house prices go, rents follow close behind on the back of the resulting economic weakness.

In November / December in Auckland (Was checking in Pakuranga, Howick, Bucklands Beach and near by area) for new listing asking was appox 10% below CV (Who wanted to sell) but in January for all new listing asking is near CV or more so has the market changed again in a month or is it just a shot by the agent / going positive in new year being best time to sell?

I guess will know in a month or two if this positive attitute by the real estate agents gets desired result and market stabilize or goes up (Though highly unlikely) or was it just a try and market continues to decline from where it left as everything depends upon sentimements and if the market falls in Feb /March nothing can save it and if it stabilize or moves up than their will be no further decline atleast sharp decline.

So next few months are interesting for housing market in NZ.

Not much to wait as Auction will start now and hopefully will know the direction.

As I said earlier Wait and Watch.

What reputable statistics do you have to back up your 10% below CV claim?

So many. When was checking the asking price against CV - market was really soft but now when checking with agent story is different.

So am not sure if it is a farce or hope or what but time will tell. If the house start selling at asking or near CV - than chances of deep fall is doubtfull and if the market continues to maintain the downwards movement than nothing can save it.

This is just an observation that have experienced while trying to buy a house for a friend - Take it or leave as is not an so called expert opinion :)

Seeing something similar with the house price estimates in homes.co.nz. I recorded a few for some properties I was watching in December, January estimates were (almost) all down from the December ones, now that I've checked a couple of Feb estimates they are mostly back to the same levels as the December ones.

expect the inventory in Auckland to keep ratcheting up, while sales volumes continue to stay low.

HPI for Auckland is already down 1.7% yoy and I can only see that going south

I've decided to take everyones advice here and buy a property in NZ. I'll spend $150,000-200,000 for a fixer-upper in Taihape or Hawera or Pokeno or Kaitaia. I'll drive 2 hours to work in the morning, and drive back to work for 2 hours at night, and in 10 years the place will be worth a cool million and I can put down a 20% deposit for a '3 beddy' in the outer suburbs of Hamilton.

I'd have to be an idiot not to really - thanks everyone for showing me the light!

Retired poppy has been screaming from the rooftops (the scaffold protected and safe rooftops) that the party is over. "those" days of spruikers filling suitcases of cash are over...for ever or for now he has not quite decided...but over they are! Congrats on your courageous decision and good luck.

Houseworks, since talk of the FBB, healthy homes, CGT, ring fencing and the Oz property downturn, your demeanour has made a distinct turn for the worse. Pretty much ever since the last election, you've turned quite negative.

I don't know about you but I think NZ is the best country in the world in which to live and make a decent honest living.

Thank you retired poopy for your "thought-provoking" contribution.

Name calling "poopy" now? Change it back at once or I will also start throwing my toys :-(

Nice work. Couldn’t possibly happen that values could be 30% lower than now in 10 years time, like Spain after their bust 10 years ago. Real estate never goes down, and doubles every 10 years.

Except is is not like that in Spain .. average prices there are only about 10% down on 10 years ago .

https://tradingeconomics.com/spain/housing-index

the very page you linked had their housing index peaking at 2101 (although that was a bit more than 10years ago), and the last value at 1589. 1589/2101 = 75.6%, so down 24%.. a lot closer to 30% than 10%.

Or for another source: https://fred.stlouisfed.org/series/QESR628BIS, click max, and tell me that a drop from 118 to 65 isn't almost a halving.. back up to 79 after a few years growth, so still down 33% by that measure.

Past performance is indicative of future results

Can't happen here

We're duffrunt

Australia has snakes

Nz also has snakes.. but they walk on two legs...

Why Taihape? Tokoroa is a better bet! If you don't want to live there the rental return is as much as 10% courtesy of NZ tax payers.

I haven't driven up to Auckland for a while.. I think I meant Putaruru instead of Pokeno. Pokeno is priced for dentists and cosmetic surgeons I think.

I detect the sarcasm in your comment, but anyway.....I did just that 18 months ago, bought a fixer upper ex-rental in the regions for that sort of money. 2 hour train ride each way to work, you do get used to leaving home at 5:30 am and getting home at 7 pm, but doing work on a train is a heck of a lot different to driving a car for 4 hours a day.

I don't get to see my family much anymore as they're in the South Island so that's a bit shit, but nobody said home ownership was easy these days.

I mean I am glad the decision has worked out for you... but spending 20 hours a week on NZ public transport just to work sounds like hell. I'd have to be truly desperate.

Dan works directly across the raod from the train station, and if his house is similarly close to the nearest station its not so bad. Train is the best form of public transport if it actually lines up like that. An hour a day to read crap on the web before walking 100m to work isn't so bad.

House is 500m from the station so it works out very well, but there’s park and ride facilities if you had to drive to the station.

An hour a day to read crap on the web before walking 100m to work isn't so bad.

He said 2 hours each way. That's 4 fours a day.

Still better than an hour each way on a bus/ in a car in traffic IMO.

Try doing work, reading a book, sleeping or watching porn while driving to work!

"The Auckland market is favouring buyers, with a fresh injection of new listings, a flattening in the average asking price and a slowdown in the time it takes for properties to sell”

Anecdotally I’m seeing that in the streets. I see 9 houses for sale in a nearby (longish) street, which is more than double recent/usual numbers, and some have been on the market for a while. Seems like stock is building, and no doubt some not selling and being taken off the market.

It actually concerns me to see regional areas going up steeply in price to be equivalent with Auckland in terms of income to price. I don’t see a reason to be gleeful about that. The higher they climb, the harder they’ll fall (when people have banked on it and won’t be expecting it).

I own a house outright in Auckland, and I'm factoring on the paper value to drop 25-30% over the next few years, as prices are now expected to do in Sydney and Melbourne. Fine if it doesn't but it's well on the cards and I'm fully expecting it and accounting for it.

Food for thought from a property investor website comment:

According to the Auckland Council there is a shortage of 46,000 residential dwellings.

Look at the housing shortage in Auckland, yet property prices have languished over the last 2 years or so. There is a housing shortage in Auckland and yet there are over 11,000 properties in Auckland currently listed for sale on trademe.co.nz.

If there is a housing shortage, why are there so many properties still listed for sale?

If there is a housing shortage, why are the clearance rates at auctions so low relative to previous levels?

If there is a housing shortage, why is it taking longer to sell a house? (as indicated by days to sell).

If there is a housing shortage in Auckland, why are vendors cutting their asking prices in order to attract buyers?

If there is a housing shortage, then why were the properties at the St James development project in Queen St and Flo apartment project in Avondale not sold out? - these projects were subsequently cancelled.

Most people will continue to believe that there is a shortage of houses in Auckland (as frequently repeated in the media by economists, property mentors, property promoters, etc) , thereby this is the long term reason that property prices will continue to increase. Those using this framework to understand the property market believe that this is a short blip in prices and start buying at these price levels. These people do not understand what a credit bubble is.

Those that understand the credit bubble framework will believe that property prices can see significant further downside. A large number of property market commentators (real estate agents, property mentors, bank economists, property investors, etc) do not know or even understand what a credit bubble is.

Government Shutdown in the US has finished and now we start seeing the data catch up.. New home sales are falling off a cliff. Below are November numbers - December's numbers are due in a few days. Anyone spotted a lot of half finished development in Auckland?

https://wolfstreet.com/2019/01/31/new-home-prices-drop-12-as-supply-sur…

Hmmm. Not really. I am helping a friend buy so do you have any to recommend?

Nice explanation of why bank economists so often get these things wrong..... often the result of toeing the party line so you keep getting your pay cheque. Good to see that Cameron Bagrie has gone rogue and is now telling it as it is.

https://wolfstreet.com/2019/01/31/us-home-sales-to-get-even-uglier-in-n…

Surprise, surprise, they are not predicting a similar fall in NZ:

“ANZ expects peak-to-trough house price falls of 15-20% in Sydney and Melbourne, with prices to continue falling throughout 2019.”..."Of the housing markets ANZ looks at in its comparison, Australia’s is the most correlated with New Zealand’s, with Sydney and Auckland house prices often moving together."..."But Zollner says correlation is not causation and the correlation"..."Going forward, most commentators expect the New Zealand market, and particularly Auckland’s market, to continue slowing but they don’t anticipate price falls similar to that being seen in Australia."

https://www.goodreturns.co.nz/article/976514267/nz-market-out-of-step-w…

nah.. Auckland is different ! And we have Phil Goof to stop all new developments

July 2016, ANZ CEO, David Hisco said (quote) "Auckland house prices and the New Zealand dollar are over-cooked. Having been in banking since 1980 I have seen this movie before. The ending is pretty much the same - sometimes a little plot twist, but usually messy"

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

Yes, a lot of people either missed or ignored his warning. This is a well informed insider of a bank who sees the credit cycle. Very importantly as the CEO of the largest mortgage lender in NZ, impacts the amount of credit availability in New Zealand ...

What was the key word in that whole paragraph poppy? No it is not "messy" or "over-cooked" it is "Auckland". Not Hamilton or the other regions as these had not yet had their time to shine. And since then Auckland has been brought back into line with tighter LVRs and stable prices...

Houseworks, on a gross rental yield measure, and mortgage rates near 70 year lows, Auckland is still "over cooked". By the same measure, the regions (especially Tauranga and Hamilton) have now become just as "over cooked". Minus the RBNZ restrictions, house prices would not have risen indefinitely anyway. The cashed up overseas buyers have all but gone. Now the RBNZ wants to see banks increase capital.

I appreciate you reserve a special place in your heart just for Hamilton, but honestly, me thinks your heart might soon be broken.

When Demographia finger Tauranga as the most expensive city in the world you have to wonder about their sanity. And Hamilton is not the hell hole you make it out as. Between you and me it is a fine city with top people and growing strongly above average.

The exceptionally low interest rates benefit the borrower and not the depositor. That must hurt.

Thanks Greg, for an even keeled article

I do chuckle how those real estate agents who produce their figures only use averages rather than medians.

I wonder why the commentators hardly ever mention Nelson Bays despite it having asking prices only out ranked by Auckland and Queenstown. I would be interested in seeing an article on the difference between asking prices and sold prices. I wonder if the gap between the two varies much around the country.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.