Auckland’s housing market could be facing a long, cold winter, the latest figures from Realestate.co.nz suggest.

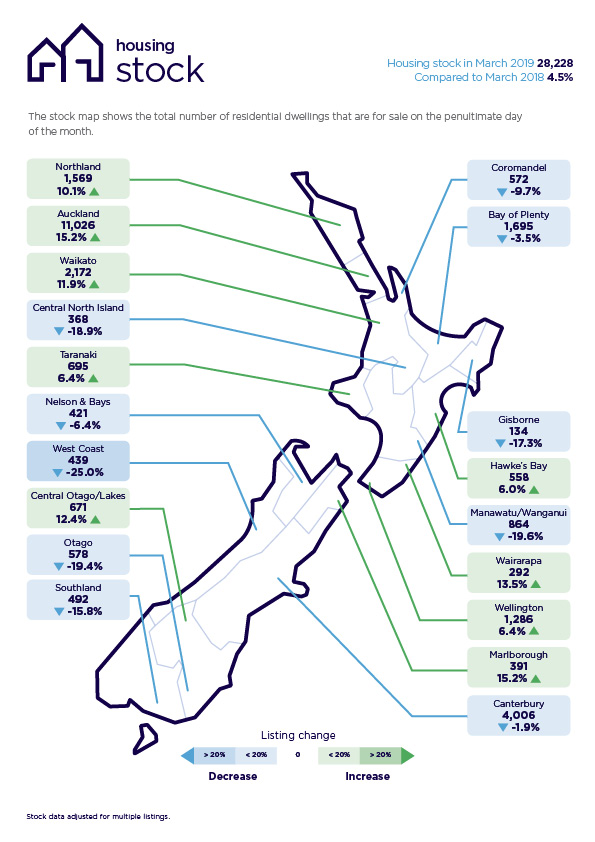

The property website had 11,026 Auckland residential properties available for sale at the end of March, up 15.2% compared to March last year.

Just as important, it was the most Auckland properties Realestate.co.nz has had available for sale in any month of the year since April 2012.

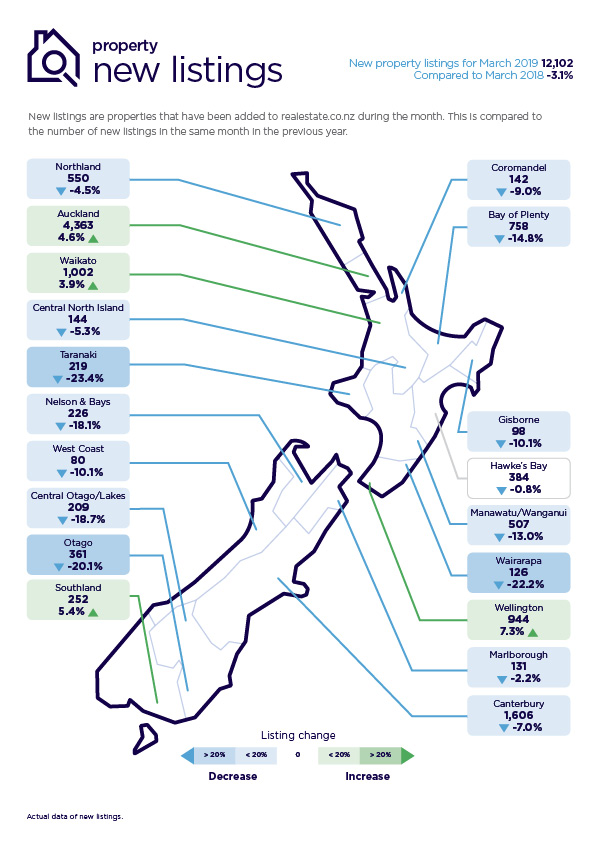

The website received 4363 new listings in March, which was up just 4.6% on March last year, which suggests that the rise in total stock has not been caused by a sudden rush of new listings, but by properties taking longer to sell and remaining listed for sale on the website for longer.

At the same time, the average asking price for Auckland properties listed on the website was down significantly.

The average price of Auckland properties listed on Realestate.co.nz in March was $952,749, down from $996,301 in February (-4.4%) and down 1.2% compared to March last year.

The combination of the rise in new listings, falling asking prices and a build-up of unsold stock does not bode well for the Auckland property market as the summer selling season comes to an end and it heads towards winter.

Realestate.co.nz spokesperson Vanessa Taylor said the figures suggested Auckland was becoming a buyer’s market.

“While these are classic indicators of a buyer’s market, it has potential upside for both buyers and sellers,” she said.

“That’s because sellers are also typically buyers looking for their next home.

“In the same market, buyers will be able to capitalise on lower prices for their next move, as the majority will be trading up.

“Falls in average asking prices could also possibly assist some first home buyers as these falls are across all price bands,” she said.

Across the rest of the country average asking prices in March were slightly lower than they were in February in most districts (Northland, Waikato, Bay of Plenty, Coromandel, Gisborne, Hawkes Bay, Wellington, Nelson Bays, West Coast, Otago, Central Otago/Lakes and Southland, while average prices in March were up compared to February in the Central North Island, Taranaki, Manawatu/Whanganui, Wairarapa and Canterbury.

The comment stream on this story is now closed.

61 Comments

Well , it was a matter of time before vendors caved in, first signs are visible..

Not sure vendors are caving yet, that's why inventories are up. There are some very greedy owners of renovated 3/4 bedrooms wanting $2.5M+ and big premiums to lofty CVs! They refuse to believe their properties may have peaked in value and will not accept anything less than a 500% tax-free capital gain. Should've sold while John Key was PM, folks! Times are changing and your houses are going below $2m

On the other hand, there are those that have their finger on the pulse, and some of them are working hard to get rid of stock. A developer thats completed 8 houses & apartments at 19 Court Crescent in Panmure, 5 price drops since they listed on 19th Feb, Now they are all 10% to 12.5% off what they went on the market for initially. $12k - 14k/week price drops on brand new homes.

https://i.stuff.co.nz/business/111775296/twice-as-many-aucklanders-losi… ..

More bad news for sellers?

the banks still want all their money though, now people find out the bank is NOT their friend but sees them as their very own piggy bank and once they have squeezed all they can throw it away

https://www.stuff.co.nz/business/111775296/twice-as-many-aucklanders-lo…

Christchurch sellers suffering even more than those in Auckland:

In Christchurch, even more people are losing money - there, 12.1 per cent of sales in the first quarter of this year resulted in the owner losing money on the deal.

I thought the Man said it was going gangbusters.

You can rarely trust the opinions of people with strong vested interests.

Rick, yes it is an interesting fact, that they say that 12.1 per cent have lost money!

Fact is that many people do not make very good decisions, and that is why I say that property investment done correctly is a great investment option!

Personally never ever lost money on property and never will, but the fact that some have lost money, clearly shows that there will be winners as well!

I am well aware that some people do pay overs for property, whereas they should get advice from seasoned successful people in property.

The data in the Stuff article is "based on sales information lodged with the local council". As 'local councils' know Jack Squat about the sales history (that's held by competent hands such as QV and LINZ) I would surmise that:

- The sales are being compared with Rating Valuations (RV's) because that's all the 'local council' can easily access in mass form

- As RV's are generally re-done on a triennial basis, the comparison is with the peak of the respective markets

- So the Stuff article should not be regarded as statistically relevant....

The data is based on information from Homes.co.nz which has access to all the QV information. Its a simple task to match up the current sale price from the Council information with the old sale price from QV. If you go look up a property on Homes.co.nz you will see the prior sale price and date of sale, as well as the current sale price once the information is lodged.

I think you are missing the point - when the sale goes through it is lodged with local authorities so they can alter the rates liability - and that is where QV, core logic etc get their information.

Real estate agents often use contract information which is why their data is more current - but as settlement usually takes a month QV/Core logic is lagged behind market changes.

The other issue with the sales data is that it only shows the price on the front page, and not terms of settlement.

And its not uncommon for developers to give discounts at the back end ie on settlement. This could be cash, whiteware etc.

Idea is to keep front page price up as that is the only part that is given for stats. which then everyone uses to comment on, including valuers.

Truth is people will be quick to tell others how well they did in any money making scheme and very quiet when they are losing money. I was thinking of some big players in CHCH.

Trademe for sale listing for Hamilton now 30% up on same time last year. The regions follow Auck, just as Auck follows Aus...timing differences.

Hamiltons not far behind. Auckland is the truck, Hamilton the trailer....

Wow!!!! Wow wow wow! Hamilton has come of age, your posts are proof. Hamilton is doing well and has shifted up a gear in the consciousness of aucklanders, DGMs included. Until last year Hamilton did not rate and was the butt of jokes. Since then I haven't heard those Hamilton jokes and there is now far more news and comments about growth and people moving there from Auckland. It is great what a housing shortage and expressway can do.

Houseworks, thought you might show up - lol. Please keep telling yourself these kind fluffys. Whatever helps legitimize your one favoured investment ;-)

Drum roll please for Agent TTP to respond with more rubbish contradicting all the evidence of a falling market....

Still trying to figure out which character Agent TPP reminds me of, in the Titanic movie... the Captain stirring his lemon tea, or one of the band members playing on deck as the water ebbs against their feet...!

TTP was the one sitting in the restaurant with a beer in one hand, a smoke in the other. He was yelling out other fleeing passengers 'she'll be right, it's certified as unsinkable".

Id just like to point out how the high immigration and the housing shortage doesnt seem to be having any effect on sales volumes or inventories

Agree, I expected the lack of any (promised) action on immigration cuts to support the market more than this. So apparently we still have a massive housing shortage and high immigration, yet falling prices. I have believed for a long time now that we only have a housing affordability crisis. Take away the funny money and things are slowly reverting to the norm.

Permanent residency is going down. Remove the partners from the stats (since they ought to be simply sharing a bed not buying a house) and that drop may be a quarter. The work visa holders make up much of the immigration figures but they are often very low paid and from countries where living with large numbers sharing quite common. Govt is trying to push immigrants out of Auckland. It must be having an effect.

People seem to forget that most third world immigrants dont arrive with hundreds of thousands of dollars for a deposit, dont have a history of income and savings for the bank to evaluate servicing reequirements, and don't have high income jobs to get mortgages on million dollar homes. Most of them are on temporary work permits or are students who can no longer buy houses due to the FBB. The days of Chinese millionaires laundering their money in Australian and NZ real estate are over.

The days of Chinese millionaires laundering their money in Australian and NZ real estate are over.

That's the key right there....

Yes, a point I've made many times on this website in the past

The people who push the 'immigration boosting housing' narrative are either a bit dumb, have vested interest, or both.

The figure of 12.1 per cent losing money in Christchurch is an interesting one!!!!!!

I would say that this is totally incorrect, as the majority of the sales would be because the properties would have been sold “as is where is” so Without insurance.

The vendors would have had a large insurance payout as well, so they have not lost money on the property whatsoever!

These figures need to be clarified!!!!!!!

There are very few "as is where is" properties on the market. But houses are definitely selling at prices lower than what people paid from 2013 onwards. I've seen at least half a dozen sales below prior sale price in the last couple of months in the area I monitor, none were "as is" properties.

Better get out there with placards on highway 74 and tell everyone the truth.

Good thing you don't pay per exclamation mark. That's quite a few there

Given that sites such as Trade Me and Home.co have in recent times started providing some rudimentary sales/historical data, previously limited to the insiders, how much of an effect will the acquisition of this knowledge for a prospective purchaser or indeed seller have in an Auckland market now unhinged. What will happen , when these sites provide more comprehensive data regarding any listing.

Greater Auckland has approximately 4 times the population of greater Wellington.

But has 8.57 times the housing stock for sale.

NZ has more houses for sale than Sydney, which has a bigger population than NZ. But somehow NZ has an "under supply" of housing while Sydney has an "over supply". Some people need a lesson in economics.

Introductory economics introduces the concepts of supply vs demand which determine market prices.

The issue is that people are mistaking these two definitions of supply and demand with respect to the property market. They may not fully understand how the following numbers are determined, and may be using the numbers in the wrong context

1) underlying supply and underlying demand

2) effective supply and effective demand

Most economists & property market commentators are using the level 1 definition to rationalise and justify rising property market prices. There are groups who use the narrative for their own financial gain

a) real estate agents use this narrative as the reason to convince buyers to buy.

b) property mentors use this narrative to attract students.

c) people posing as bank economists to attract potential borrowers for financial institutions who provide mortgage financing

However, it is the level 2 definition that determines market prices.

Exactly right!

So prices can only go up, ESPECIALLY in the leafy suburbs

- TTP

That's probably nothing...

As equity positions start reducing, keep an eye out for how cautious the banks get about the business they want and the business they don't want. Lower mortgage rates will become the carrot to try and attract the borrowers with better equity positions, I doubt if they will be available for everyone. There will be a necessary risk premium for those who have gone from 15% equity to 5% - will those people get a nice new fixed rate deal or will they be forced to move to the lenders standard variable rate, because of the increased risk and lack of security against the loan. We'll find out how friendly these Australian banks really are over the next few years.

Or investors with a portfolio equity dropping from 40% to 30% with Interest Only mortgages.

At least with an Owner Occupier, the banks may be more willing to discuss some sort of additional payment plan to bring the equity position back to where it needs to be. Even if it means breaking onto the Floating Rate for a couple of years. An investor on the other hand, well that depends on what's owing on their family home and how many Interest Only rentals they have in the portfolio.

Finally more people are starting to see it’s been a massive bubble in NZ, and of course in Australia, and it’s starting to unwind. It’s going to be tough in the property market for a very long time.

...And I’d say there will be rate cuts (possibly to near zero) to try and stop the property value slide, and QE. When it slides, the sharemarket will follow later, hitting the banks especially hard. The NZ50 has gained 300% in 10 years since 2009.

Wait wait.. QE means sharemarket should rally high ,right ?

rates down, prices up ?? Thanks

@Greg-Hamilton, very difficult to time markets of course, because many overseas factors impact our market. Yes, I think lower rates would initially push people into shares if they have money to invest. It generally takes a while for a property downturn to hit the sharemarket, sometimes 2 years or more, but it does. If there's a severe housing decline, the banks (mortgage loans) will get hit hard, when the damage to banks is revealed.

it looks like all those high prices are artificial driven by relatively easy accessibility of high volume of credit, so unless RBNZ ,RBA or FED opens it's tap (money tap , Foreign Buyers Ban, LVR or any other means of property price manipulation technics ) all winters and summers are going to be cold. Unless you truly believe rotten leaky units in the remote suburbs of Auckland should cost what they cost now

based on trademe data, I have listings up 37% since election day, and 8% alone in the last couple of months. "Price reduced" , or "Reduced" featured in the listing has also spiked in last couple of months? .

Watched this one on K road go from auction, to asking price of 1.3 (cv) to 1.2 to just a smidge over 1mil since about September. Expectations are warped.

Saw an odd on the other day..

This one : https://www.realestate.co.nz/3515487

"***VENDOR NEEDS UNCONDITIONAL OFFER BY FRIDAY 5th OF APRIL DONT MISS OUT***"

Unconditional and by a set date seems a wee bit too specific to just be an agent trying to drum up an offer?

That's a nice house. What's wrong with it? Is it not selling because it's plaster on top?

A serious buyer should look at the sales history and make an offer based on that.

Maybe the Vendor had their offer on the next place accepted, but forgot to include a condition "Subject to Sale of Existing Property"?

Kw.there are still heaps of “as is where is” properties still being sold in Christchurch!

Yes it has slowed down a wee bit, but to say there are very few for sale in ChCh is rubbish!!

Could the writer of the article that states that 12 per cent of the homes that sold in the last quarter went for less than they bought them for, please state how many were “as is where is”??????????

The average sale price over the past year is up, so this is very misleading !!!!!!!!!!!!!!!!

Christchurch market is holding up very nicely!

I think you might need a sit down and a nice cup to tea.

He has never sounded so defensive and desperate Solidname. It really is very sad but he has consistently shown that all he cares about is money. People are secondary to him especially those scummy tenants who prop him up. If in fact he has any property all.

Gordon, not defensive or desperate at all!

What I am saying is that it is rubbish that an eighth of all sales over the last 3 months, the vendors have lost money on what they have paid for their property!!!

It is so wrong that this figure can be published without the justification for it!

I can assure you that this is so inaccurate it isn’t funny!

Offer still on the table Gordon!!

Not perturbed at all about misrepresentation of facts!

To say that 1 in 8 properties that have sold in ChCh over the last 3 months is less than the owners paid for them, is rubbish!

Let’s see these examples of these properties, as I can tell you now the ChCh market is as solid as!

Seems very odd that the average is up!!!!!

I have not been seeing these properties selling for less than Owners paid for them, however there are always opportunities around!

Chamomile, with a dash of punctuation should do the trick.

You can buy those "as is where is" properties - getting insurance for them might be another story!

I was told recently about my old family house in Wellington, we used to pay $1200/yr for insurance premium, now it's over $4500/yr, simply because of the earthquake risks.

I'd be interested to hear what people in Christchurch are paying now?

Chairman, you can get insurance for As is where is properties providing they have been repaired and certified!

I purchased one for a good price and got full insurance cover for it without much trouble.

Insurance premiums depending on insurance company are around $1500 per annum for $450k of cover in ChCh! Sometimes can be more depending on add ons!

yup, still enough "As Is Where Is" properties to invalidate this type of analysis in Chch.

Houses are going 20% below CV. One only has to find genuine seller.

Recently a beautiful house in Pakuranga with CV of 1150000 went for 950000 and another with CV of 970000 went for 830000 and am talking abkut good quality free standing house with land size of more than 800 sqmt and house size more than 160 sqmt and in desirable area.

Also saw many houses which were earlier listed for mid to high 900s are now listed for high 800s and may be, will accept offer in mid 800s BUT still those houses are expensive in current market.

Have also seen houses listed with asking of the price that the vendor had purchased few years back (From sell history), and even if they sell at that asking, vendor will pay commison from his pocket but overall many are now ready to sell and take lose of 5% plus and this is Today - going forward will be worse.

Market has changed and still another 10% from here on (which to happen is not much) and will be bloodbath for many and will trigger a chain reaction that for many will be......

Wait and watch.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.