Auckland Council’s Policy and Planning Committee has approved Plan Change 120, which proposes changes to planning rules to allow more homes near centres and rapid transit. It replaces Plan Change 78, which would have applied Medium Density Residential Standards across much of the urban area. This paper presents a forecast of how the changes may affect housing supply and highlights some implications for Auckland. Find out more at: Auckland Council Chief Economist webpage

Capacity versus housing supply

Auckland’s capacity for new homes would be around 2 million under Plan Change 120, similar to Plan Change 78. While that may sound like a lot, capacity counts the number of homes if every site were developed to its permitted maximum. How this capacity will turn into new homes – housing supply – is uncertain. Feasibility matters, as sited zoned for more height may yield fewer new homes than capacity suggests, if local demand is limited. Site availability is also a factor, as some owners may not be ready to sell.

Given these uncertainties, it seems prudent to enable more capacity than projected demand would suggest. An abundance of capacity also increases competition among landowners, which can help to moderate price pressures and encourage responsiveness to demand.

Auckland’s own experience illustrates this. Evidence shows the Unitary Plan, which increased capacity in 2016 by allowing more flexible land use, has led to more new homes and lower rents than otherwise.[1], [2]

A forecast of housing supply

To examine how this capacity could translate into homes over the next decade, the Chief Economist Unit developed a housing supply forecast using a regression approach. The model draws on experience under the Unitary Plan, using data on added floor area given demand, planning rules, and existing land use, to estimate the probability of development across locations. Forecast floor area is converted into homes, without specifying housing type or building height.

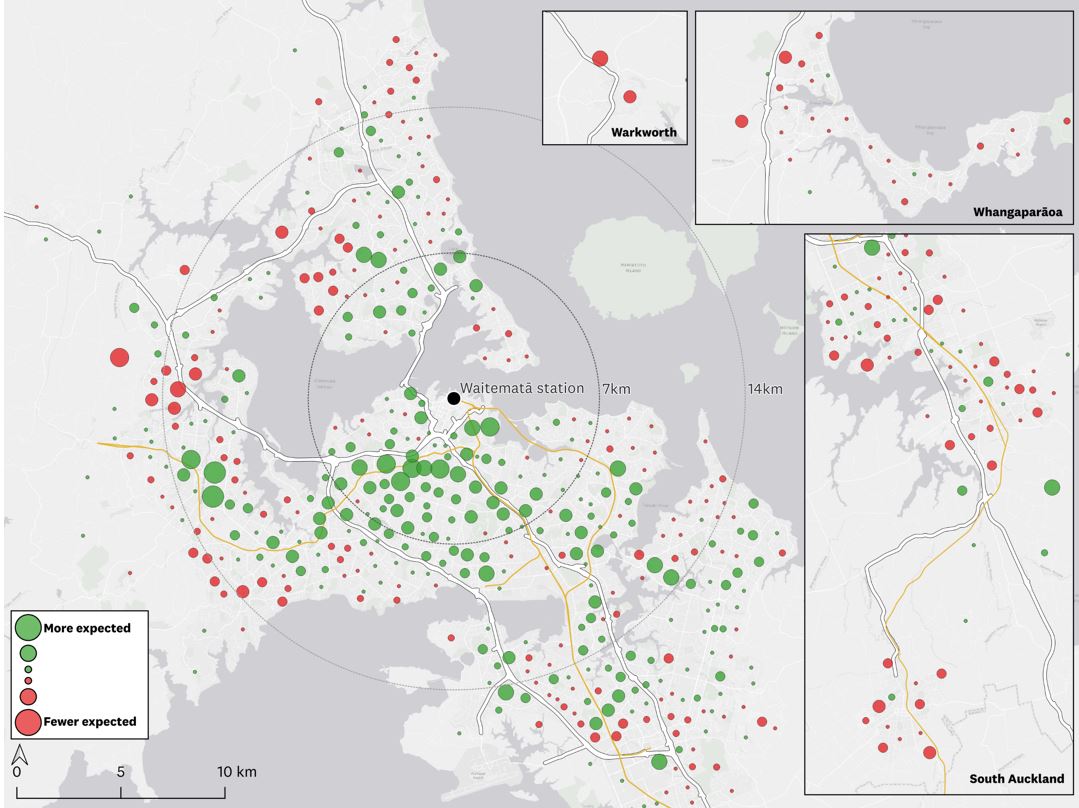

Figure 1: Forecast change in new homes over 10 years under Plan Change 120 relative to Plan Change 78

Notes: results represent SA2 centroids; uses the version of Plan Change 120 approved by Auckland Council’s Policy and Planning Committee on 24 September 2025; includes land zoned Single House, Mixed Housing Suburban, Mixed Housing Urban, Terrace Housing and Apartment Buildings, and Business – Mixed Use.

Source: Auckland Council Chief Economist Unit

Figure 1 shows that, over the next decade, housing supply is forecast to be more spatially concentrated under Plan Change 120 than under Plan Change 78, with more homes near existing infrastructure and services. The following measures illustrate this.

- The share of new homes within the walkable catchments of centres and rapid transit stops is forecast to be 35%, up from 26%.

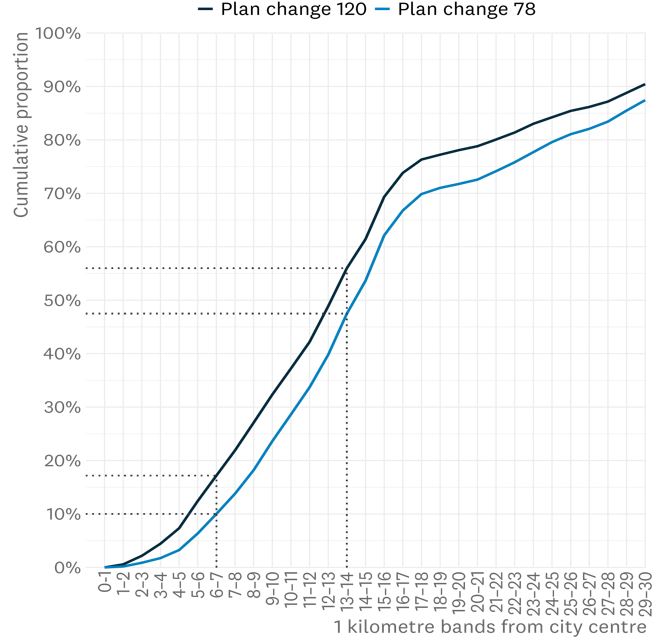

- The share of new homes within 7 km of the city centre is forecast to be 17%, up from 10%, as Figure 2 shows.

These findings reflect the greater capacity enabled by increased building heights near centres, rapid transit stops, and frequent transit routes. Many of these locations have relatively high land values, signalling demand for access to services, jobs, and transport – factors that support development feasibility.

In terms of quantity, the forecast shows more new homes, though the scale is uncertain. Under Plan Change 120, housing supply is forecast to be 6% to 20% higher than under Plan Change 78. The increase reflects the strong supply response that followed the easing of land use constraints under the Unitary Plan, an effect captured in the model.

This additionality could arise if planning rule changes allow higher yields per site, so that fixed costs can be spread across more units and average development costs reduced. In turn, this could enable developers to offer more competitive prices, meet more of the demand for housing, and maintain profit margins.

Figure 2: Forecast new homes, by distance from city centre

Notes: data covers residential and business mixed use zones; chart is truncated at 30km from the city centre to fit space. Source: Auckland Council Chief Economist Unit

Acknowledging uncertainty

The easing of land use constraints under the Unitary Plan and the resulting supply response1 has likely met some of the pent-up demand for housing, potentially moderating the effect of Plan Change 120. If so, this suggests the forecast could be somewhat overstated. The central forecast – around 22,000 new homes per year – appears high by past standards. On the other hand, ongoing affordability pressures indicate high demand and potential for a strong supply response.

These uncertainties mean the forecast should be seen as indicative of the likely direction, with more weight on the spatial pattern than the overall level of supply.

Implications and trade-offs

The forecast spatial shift in housing supply under Plan Change 120 implies several potential benefits.

- Choice. More opportunities for people to live near services, jobs, and transport through higher-density housing that uses less land per home

- Infrastructure. More homes in areas with existing infrastructure can make better use of capacity and reduce pressure for network extensions

- Productivity. More homes in accessible locations can reduce travel times and support job matching, knowledge sharing, and skill attraction – factors associated with higher productivity

Change involves trade-offs. Development can result in shading or reduced privacy for nearby properties. A more concentrated growth pattern under Plan Change 120 may mean fewer properties are exposed to these effects than under Plan Change 78, although larger developments could intensify them where they occur. The overall impact on local amenity will depend on the location, scale, and design of future development.

Removal of the special character overlay from some locations near rapid transit stops is another trade-off. While that would enable gradual redevelopment and support more homes, it may alter the appearance of these areas, which some people value.

A new chapter in Auckland’s growth

The housing supply forecast model is a key step in understanding trade-offs in land use, providing a structured way to examine how some significant changes to planning rules may affect housing supply.

Over the coming months, public submissions and independent hearings will help refine Plan Change 120, with the final version shaping Auckland’s urban form for years to come.

[1] Ryan Greenaway-McGrevy and Peter C.B. Phillips (2023), “The impact of upzoning on housing construction in Auckland”, Journal of Urban Economics, Volume 136;

[2] Ryan Greenaway-McGrevy and Yun So (2024), “Can zoning reform reduce housing costs? Evidence from rents in Auckland”, Economic Policy Centre Working Paper 16, University of Auckland

* Gary Blick is the Chief Economist at Auckland Council. This article is here with permission. Find out more at Auckland Council Chief Economist webpage. The original article is here.

5 Comments

Anyone who has a team named after their role should be taken very seriously. If they then use a regression model in relation to housing supply they should probably be considered beyond repute.

Needed allowance for increased density, but no mention of housing quality - such as minimum floor areas, outdoor spaces like balconies, variations in the numbers of bedrooms, local services and amenities, soundproofing standards, ownership models and the rest.

Are the build regulations in place that are going to allow, and drive, the creative creation of interestingly designed, good quality homes that support community?

Or are they going to facilitate building insta-slums of minimally sized apartments for rental that people tolerate because they are near to things, but there's huge resident churn as tenants get sick of living in a hutch?

It sounds like NIMBY voters may have the PM's ear; https://www.thepost.co.nz/nz-news/360931482/controversial-auckland-intensification-plans-could-be-watered-down

so much room for price appreciation when another 2 mil are going to be built...... <SARC=off>

Sorry about that guys living in cars. Remember to pay your carbon tax when you fill up - we only have room for trees, not new sections.

It is, incidentally, only a radical enabling of greenfields development that would sharply and sustainably reduce real urban land prices (the largest single component of city house prices)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.