A significant drop in house prices at the bottom of the market drove a substantial improvement in affordability for first home buyers at the start of the year.

According to the latest Real Estate Institute of New Zealand data, the national lower quartile selling price declined to $580,000 in January from $609,000 in December last year.

That's the second month in row the lower quartile price has declined, and it's now down $36,000 since November last year.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing the most affordable end of the market.

Lower quartile prices declined in all regions except Nelson/Marlborough and Southland in January, with the biggest declines occurring in Auckland -$42,000, Taranaki -$35,300, Hawke's Bay -$35,000 and Wellington Region -$25,000.

Auckland's lower quartile price in January was the lowest it has been in any month of the year since September 2020, while Wellington's lower quartile price dropped to its lowest point since August 2020.

It is probably no coincidence but the latest decline in prices at the bottom of the market comes at the same time as mortgage interest rates have started tracking up.

The average of the two year fixed mortgage rates charged by the main banks appears to have bottomed out in the current cycle at 4.49% in November, rising to 4.72% in December and 4.74% in January.

However the effect of the modest rise in interest rates on mortgage payments was easily eclipsed by the decline in prices.

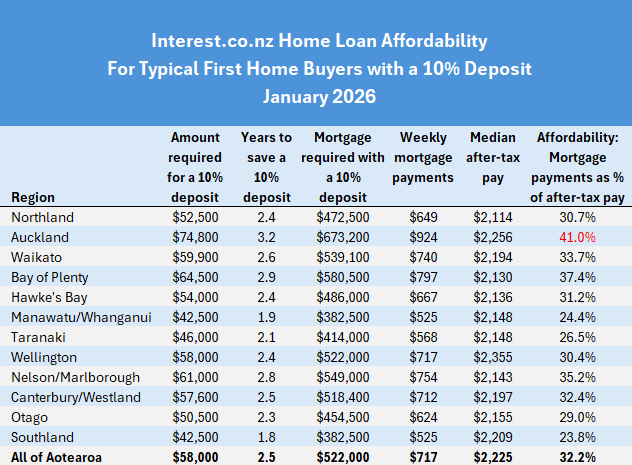

Interest.co.nz estimates the mortgage payments on a home purchased at the national lower quartile price with a 10% deposit would have declined to $717 in January from $751 a week in December, a reduction of $34 a week.

In Auckland the mortgage payments on a lower quartile-priced home purchased with a 10% deposit would have declined to $924 from $974, a reduction of $50 a week.

That represents a substantial improvement in affordability at the lower end of the market, which is even more pronounced when compared to incomes.

Interest.co.nz estimates the combined after-tax pay for a couple working full time at the median rates of pay for 25-29 year olds would have been $2225 a week, so mortgage payments of $717 a week would have eaten up just under a third (32.2%) of their take home pay.

Well within affordable limits

Mortgage payments are generally considered unaffordable if they take up more than 40% of after-tax income. So by that measure, housing at the national level is now well within affordable limits for typical first home buyers.

Using the above measures, housing at the national level is now the most affordable it has been since June 2021.

Even in Auckland, which has long been the most unaffordable region in the country and the one where it has been the most difficult for first home buyers to get into a home of their own, there has been a huge improvement in affordability.

Lower quartile mortgage payments in Auckland were 41% of first home buyer income in January, within striking distance of dropping below the 40% affordability threshold.

Some parts of Auckland are already well within affordable territory such as Waitakere, Manukau, Papakura and Franklin.

Overall, housing in Auckland is now the most affordable it has been for aspiring first home buyers since September 2020.

However there are still challenges to overcome for aspiring first home buyers, including scraping together enough money for a deposit.

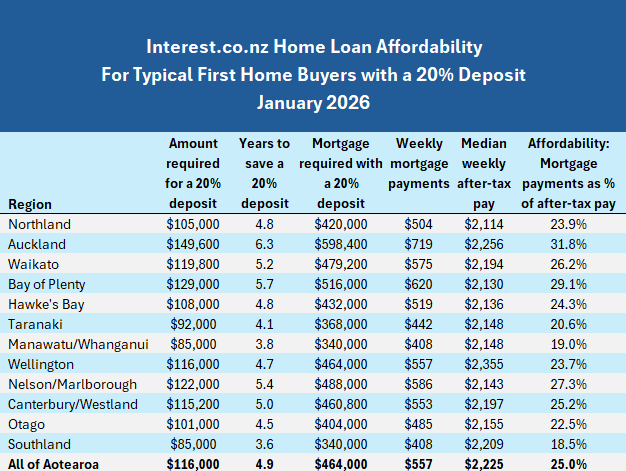

They would need to find $58,000 for a 10% deposit on a home at the national lower quartile price, or $74,800 for one in Auckland. And of course you can double those figures for a lower risk 20% deposit, which would avoid having to pay low equity fees on the mortgage.

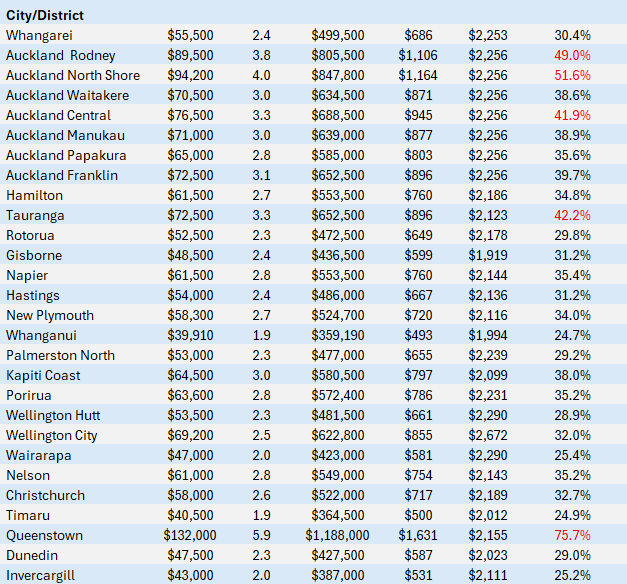

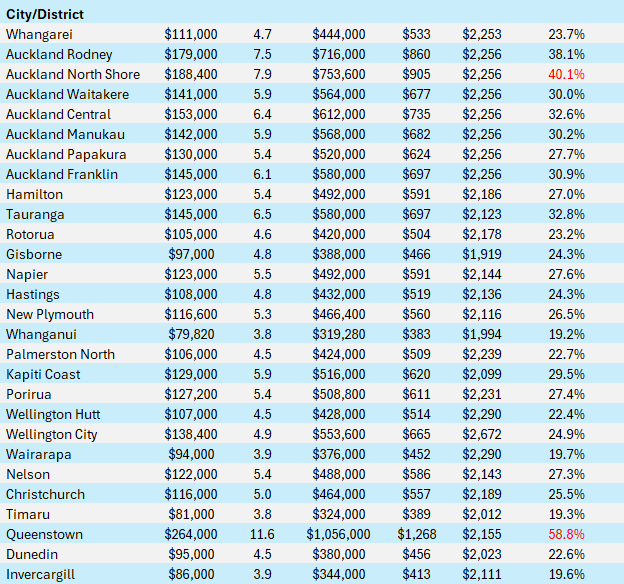

The tables below show the main home loan affordability measures in all urban centres around the country, for buyers with either a 10% or 20% deposit.

The comment stream on this article is now closed.

34 Comments

Let the home value slide continue, so a more healthy, less than 25% of income goes to service, much lower mortgages.

Great to see NZ ditch the forever more expensive housing mindset.

Many home hoarders will get burnt and financially fried. Thats what buying on speculation gets you - A great financisl lesson!

The value slide should slow once rental yeilds hit the 8 to 10% levels

You know, that old fashioned "income thing".......something totally ignored over the last 20 years of the 40 year NZ Housing investment frenzy. Glad this frenzy busted in 2021 and it continues to deflate for many years still.

Thanks for confirming NZ has gone from abysmal to poor yields.

Some idiots think 2 or 3% yields are great......waiting for the capital gains gravy train to roll up.

The whole paradigm changed in 2021. A few plebs are still betting it all on leveraged property roulette and will be wiped out.

Those who did not take note of the few here, giving the stark NZ housing Ponzi warnings, well - they will get their financial haircuts.

Thanks for confirmng NZ has gone from abysmal to poor yeilds.

Just highlighting that there's not a lot of precedent for 8-10% yields as a rule.

The whole paradym changed in 2021.

Taking any COVID era trends is fraught with danger. Harley Davidson thought their 2021 sales were the start of a new trend, upped production. Now they have 80,000 bikes sitting unsold. This has happened across many industries.

The paradigm is shifting but it extends far further than property.

Because property is an asset class, yields will always adjust relative to other asset classes based on risk. If prices continue to fall, rents will likely fall with them.

And I believe this is where the recovery will come from: more to spend on anything else.

Are prices sliding at the lower end or simply a greater number of inexpensive town homes being added to the market by Developmers who need to unload their stock and are dropping prices. Would be great if REINZ would inform by doing a split on the bottom end between: Apartments, Townhouses, and Single Family Dwellings.

That'd be pertinent information.

We know there's been a big explosion in intensive house building in the cities

But on the flip side, out on the fringes and jn the regions, older people have been building large, expensive homes, and much of the middle class, greenfields subdivision housing is barely ticking over.

Splitting hairs you mean?

this is why we look at last sale price.... same house sales are 100% important

It's interesting that the average mortgage for investors and first home buyers is continuing to go up despite stagnant / reducing house prices. Also frustrating that folks don't recogise that the real constraint on house prices is the labour market. House price growth relies on family units earning more. Hence, nothing predicts real house price growth like the employment rate.

100% this

Also tells us it's not investors that really drive pricing, but the 65% or so owner occupiers.

And yet, almost all the discussion ignores this.

Can we now stop the nonsense about the ponzi and NZ house prices being unaffordable? 25% of income seams reasonable to me, pretty sure the house I bought 20 years ago was more than that.

$65k USD for a useless bitcoin, and people think houses are a rip off!

If we make a bogeyman though

We can pretend the problems them, not everything else.

And then a golden goodie, that'll turn it all around

Sounds like a scooby doo episode. They would have got away with it if it wasn’t for those meddling kids.

Now that property is affordable, and Bitcoin is boring, time to “invest” in gold and silver. But Bitcoin / gold / silver aren't considered ponzis for some reason, they are at priced at their true value apparently. Good luck with that.

I know some lifelong property gurus now taking a shine, towards gold.

One 40 year Ponzi completely poked, while another, in early bull stage?

I always come back to Warren Buffet's famous investment advice, Geck.

“Be fearful when others are greedy, and greedy when others are fearful”.

Right now, everyone seems to be fearful of property which makes it a good time to invest IMO. Gold and Silver on the other hand is experiencing a greed-induced mega-bubble, which is not going to end well for those throwing money at it.

Right now, everyone seems to be fearful of property which makes it a good time to invest IMO. Gold and Silver on the other hand is experiencing a greed-induced mega-bubble, which is not going to end well for those throwing money at it.

It's interesting as to what people perceive as a bubble. Property provides consumption (shelter, space, status), so the people can rationalize high prices as paying for a life need, not just a financial bet. The ruling elite and media can prey on mainstream attitudes and beliefs to reinforce this.

Gold and rat poison have little or no day‑to‑day consumption value for most people, so attention focuses almost entirely on their price chart, making parabolic moves look inherently “speculative."

Across the Anglosphere, homeownership is socially promoted as the “right” way to build wealth, reinforced by tax incentives, mortgage subsidies, and political rhetoric. That institutional backing makes high property prices feel systemically endorsed rather than aberrant, whereas no government or mainstream bank tells you it’s a civic duty to own something like ratty.

Property price booms are smoothed by slow transaction data, opaque valuations, and long feedback cycles; homeowners see “house prices double every 7-10 years” not “this is a 25+-year bubble.” With property, people invoke intuitive fundamentals: population growth, land scarcity, construction costs, income growth, and “location,” which offer a story to justify high prices even when rent yields are thin. For gold, fundamentals are abstract (store‑of‑value, monetary debasement, network effects), so critics can more credibly argue prices are “unmoored from reality” and therefore bubbly.

Across the Anglosphere

It's actually everywhere, you just suffer from myopia

You need around 90 ounces of gold to buy the median NZ house today. In 2021 it was 280 ounces. In the mid-2000s it was in the 400s. The last time we saw ratios in the 50 - 100 range was the early 80s when interest rates were sky high and inflation was up around 15%. Unless we experience an unprecedented mother-of-all inflation spike in the next year or so, I'm sorry but I find it hard to see how Gold prices will stay at current levels for long.

You could be right. Aotearoa's broad money supply has expanded enormously since 1980. The earliest available M3 data shows approximately NZD13 billion in early 1981, and by late 2025 it reached an all-time high of approximately NZD 442 billion, so a 3,400% increase over 45 years.

Or perhaps house prices just crashed relative to hard money - ie gold. So now decades of housing mania is behind us and the price of housing is back to a more fundamental value compared to hard money and that we slowly see prices to continue to decline in inflation adjusted terms as prices in fiat currency remain flat or fall while inflation eats away at property prices when viewed in fiat currency terms (whereas houses priced in gold terms has quickly adjusted to the recent inflation or expected inflation in the economy).

In the US, for example, now would be a really good time to sell gold and buy houses when viewed over a 100+ year time frame:

https://www.longtermtrends.com/real-estate-gold-ratio/

But most people were buying houses when the perhaps should have been selling houses and buying gold, so now they have no gold to sell, only houses.

Would take big balls to be a 100% contrarian investor - ie sell houses when everyone else is buying them (eg 2020-2021), and then sell gold when everyone else wants to buy it (now).

History generally favours those who go against the prevailing sentiment and do the opposite of what the crowd is doing.

In NZ if you did that you got ridiculed as a 'Doom Gloom Merchant'.

Alternatively, I find it hard to see how property prices will stay at current levels for long.

That's certainly an alternative theory. House prices will stabilise and begin to rise when it reaches a level considered affordable by first home buyers. Given how active FHBs are right now, I believe we are at that point, or very close to it.

The notion of affordability is skewed due to recency bias.

He also said

"Price is what you pay. Value is what you get" is a famous maxim popularized by investor Warren Buffett. It emphasizes that cost is a known, immediate monetary amount, while value is the subjective, long-term benefit, quality, or utility derived from that purchase. The quote encourages looking beyond the price tag to determine the true worth of an investment or product.

As an owner occupier fill your boots, but as an investment everyone is out to get you.

There are a lot of developers now looking at the 30% off list the desperate $1 reserve guy got and know that their time is now up.

People just stopped bidding at 580 ish

The absolute NZ Property Bubble has since 2021, dropped nationwide by -27%.

In the larger NZ cities, its more than -40% losses from peak.

You think this is over? No way!

Real Residential Property Prices for New Zealand (QNZR628BIS) | FRED | St. Louis Fed

There is a reason some seasoned Landlords are selling up, some are slow to cotton on, obviously!

In Q2 2020, Berkshire Hathaway bought shares of Barrick Gold, valued at roughly $565 million, despite Buffett's long-standing skepticism toward gold as an investment. Berkshire completely exited the Barrick Gold position between Q3 and Q4 2020.

If they had held, the return would be close to 306%.

Are we fearful? Or just less greedy/coming to our senses

Nobody needs BTC, everyone needs shelter.

NZ is the 10th worst in the OECD for increases in house prices compared to incomes. If you look at the graph below you'll see it was a lot easier in the 80s and 90s compared to now. Thanks to the retail banks being allowed to splash the cash for 20 years from 2002 to 2022 then the Reserve Bank adding with icing on the cake in 2020 and 2021 so we have ended up in this situation.

One good thing is lots more new housing stock

But overall this high house price to income ratio has consequences for retaining our youth and in some cases pushing out retirement. I also think graduate salaries are too low

https://db.nomics.world/OECD/HOUSE_PRICES/Q.NZL.HPI_YDH

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.