New Zealand's bank crisis management framework could benefit from making recourse to taxpayer bailouts a last resort option, a consultation paper issued as part of phase two of the Government's review of the Reserve Bank of New Zealand (RBNZ) Act says.

One potential way to help achieve this floated in the consultation paper is through bail-in powers. These would allow the RBNZ to convert unsecured liabilities into equity as part of bank resolution efforts, or convert or write-down debt instruments when a contractually specified trigger is met. There could be specific exemptions, such as insured deposits.

Bail-in powers were developed overseas in the aftermath of the Global Financial Crisis to help authorities recapitalise failing banks quickly, helping restore viability and capital ratios above regulatory minimums. Although there have been no bank failures in New Zealand in recent years, there have been banking crises in the past.

"Bail-in helps to avoid insolvency and minimises the need for taxpayer bailouts or other taxpayer support," the consultation paper says.

It notes that bail-in should be applied in a manner that respects the normal hierarchy of creditor claims. This means equity, the bank owner's stake, and other ownership instruments should fully absorb losses before eligible liabilities are bailed in.

"Using bail-in is not without its complications. It must ensure that affected creditors are treated fairly - that the bail-in, for example, the value of any securities received, represents fair treatment of their property rights as creditors. Careful valuation work is essential to mitigate the risk of subsequent legal challenges for compensation. Bail-in also requires sufficient unsecured liabilities or other instruments to be available to bail in. The incentives created by prudential requirements for banks to hold suitable quantities of bail-in-able liabilities can potentially determine whether bail-in is a credible option for a given bank," the consultation paper says.

"The availability of sufficient liabilities would therefore become part of a resolution authority’s pre-crisis analysis of whether a bank is in fact resolvable. However, prudential requirements can change over time, so they should not in themselves determine whether bail-in powers should be made available in legislation. Without explicit exclusions, deposits would be ‘bail-in-able’ liabilities alongside other unsecured liabilities like non-covered bonds. A deposit insurance scheme would therefore become an important element to protect depositors from what might otherwise be seen as an unfair imposition of losses on those who are least able to monitor and manage the risk of bank failure."

The Government announced plans to introduce a deposit protection regime in June.

The consultation paper goes on to say that international experience with using bail-in is still in its infancy and has demonstrated both benefits and problems.

"The main benefit is the ability to recapitalise a bank while minimising the need for a taxpayer bailout. The Bank of England has noted other significant benefits, including avoiding operational challenges and legal consequences that can arise when transferring some of a failed bank’s business to a purchaser."

"Issues with bail-in include the need for robust valuations before and after the event, to support the determination of whether ‘no creditor worse off than in liquidation’ compensation is required and to mitigate the risk of creditor litigation. Bailing in foreign-held debt instruments also relies on either a contractual, and therefore enforceable, agreement to the resolution authority’s power to bail in, or recognition of the bail-in power by authorities in the jurisdiction in which the debt instrument is held," the consultation paper says.

"For New Zealand, one option for introducing statutory bail-in would be to provide for the general power in primary legislation, with eligible liabilities and exemptions set out in regulation, while options for the foreign enforcement of the power are developed further."

The RBNZ's controversial existing bank failure tool, its Open Bank Resolution (OBR) Policy, is not being reviewed as part of the RBNZ Act review. Implementing OBR would require government approval. You can see here how OBR might work should it ever be used.

Questions raised in the consultation paper include whether the RBNZ should have the power, in principle, to "bail in" specified categories of unsecured liabilities in order to recapitalise a failing "large" bank after its owners have absorbed maximum losses, and to minimise the need for taxpayer support. Details of eligible liabilities would need to be determined, and be subject to creditor property rights safeguards, the consultation paper adds.

On the property rights issue the paper asks whether the resolution authority should always be required to respect property rights, including the hierarchy of creditors in liquidation, or should it have discretion to override property rights as long as compensation is made available to creditors left worse off than they would have been in a liquidation. Additionally it asks whether no change should be made to the protection of creditor property rights.

Other topics canvassed include whether the recapitalisation of a failing large bank should be funded through industry-wide levies, and whether any other aspects of cross-border bank resolution need to be considered in the design of New Zealand’s crisis management framework especially given four Australian owned banks account for 82% of New Zealand’s banking system.

In summary the consultation paper chapter on bank crisis management suggests a range of changes including:

* Making resolution powers directly available to the Reserve Bank as resolution authority;

* Clarifying the objectives for which the Reserve Bank would be held accountable in exercising resolution powers;

* Less involvement of the Minister of Finance in routine matters and more involvement when public funds are at risk;

* Enhancing the ability to allocate losses from, and recapitalise, a failed bank without relying on taxpayer support. And;

* Providing creditors with greater certainty as to how they will be treated and comfort that their property rights will be protected.

The deadline for submissions on the consultation paper is 5pm on Friday, August 16. The RBNZ Act review is being overseen by a team jointly resourced by Treasury and the RBNZ. Finance Minister Grant Robertson announced the RBNZ Act review in November 2017.

“The current Reserve Bank Act is now nearly 30 years old. While it has served New Zealand well in general, now is the right time to undertake a review to ensure our monetary policy framework still provides the most efficient and effective model for New Zealand," Robertson said in 2017.

Phase 1 of the RBNZ Act review focused on monetary policy.

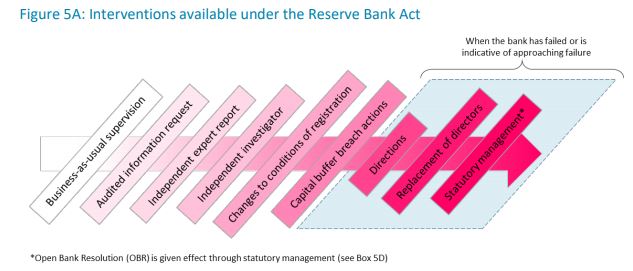

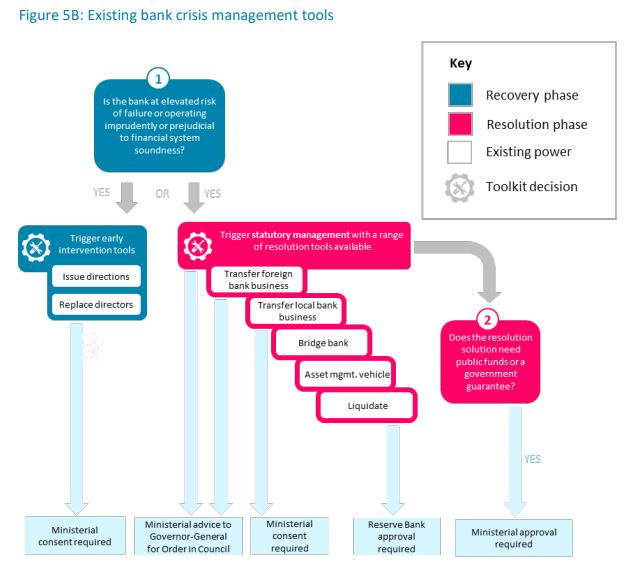

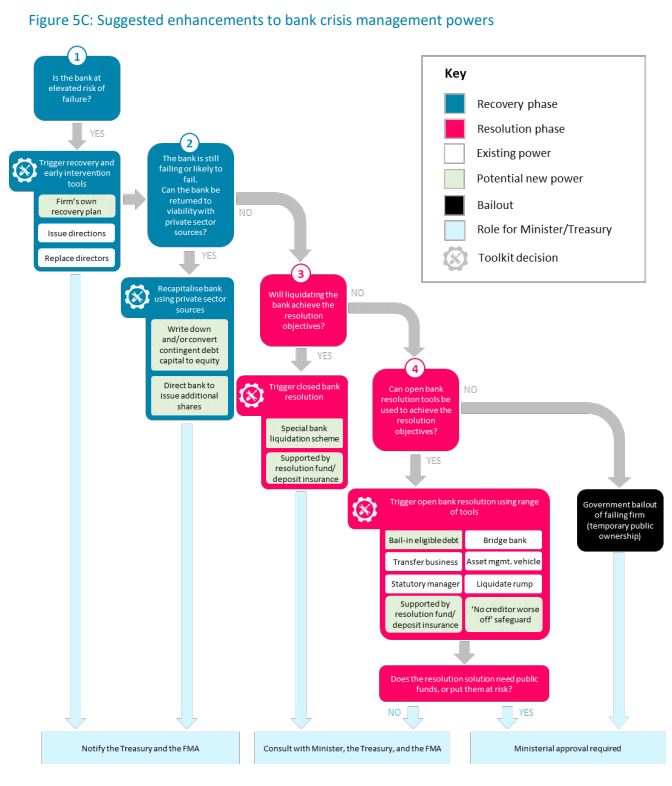

Figures 5A, 5B, and 5C below comes from the consultation paper.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

25 Comments

They should only consider a bail-in if they want mass protests in the streets. Bailouts are vastly unpopular, but taking depositors funds is worse, considering the behaviour of the banks in Australia and New Zealand.

for god's sake... please try and keep up with the conversation... it is not talking about bailing in deposits.... what this is referring to is having specific securities nominated as 'bail-in-able'. Should senior bonds gets bailed in?... subordinated bonds?... noone is talking about deposits.

andyb it is you who has missed the plot; the article specifically states"These would allow the RBNZ to convert unsecured liabilities into equity" and guess what? Depositor funds are right at the top of the unsecured liabilities list! And further more; "Without explicit exclusions, deposits would be ‘bail-in-able’ liabilities alongside other unsecured liabilities like non-covered bonds."

This move is concerning, because while it talks about property rights, it clearly appears to be subordinating depositor property rights to those of the bank, in that it says the "equity, the bank owner's stake, and other ownership instruments should fully absorb losses before eligible liabilities are bailed in" meaning that the bank itself can take depositors funds rather than being allowed to fail.

As depositors funds are recognised as the property of the bank and that the depositor becomes an unsecured creditor, the conversion of these funds to equity could be interpreted as effectively meaning that the liability to the depositor no longer exists! This goes a long way beyond the "haircut' provisions of the OBR to total theft of the depositors funds.

Another way of looking at it is; it appears that there may be some tension between the 'deposit insurance' and the 'conversion to equity'as well. This ostensibly is designed and intended to protect depositors funds, but reading the whole article suggests that any payout from an insurance scheme may still go to the bank and not the depositor. This needs careful scrutiny.

I actually think we are on the same page Murray and there is no way the public would permit deposits to be converted to equity. Besides, do we honestly believe a bank will realistically be able to convert deposits to equity and remain a 'going concern'? No... its gone. Even it was deemed solvent there would be a queue out the door and around the street of depositors wanting their money out.

My point is the whole argument of bail-in deposits is a moot point. It simply wont fly and is completely pointless.

What we are seeing more of in global markets is senior non-secured issuance which looks and feels like senior debt but actually sits behind depositors (effectively making depositors 'super-senior' and only subordinated to covered bonds). That to me is a more feasible proposal however will come with a slightly higher cost of debt for the banks.

I accept your sentiment, but do not agree. I doubt the authorities, the RBNZ or Government, or the banks give a fat rats about the depositors and will not care if they are left in the cold. They only truly care once every three years, and they want to push that horizon out too! I do agree politically it would be fraught, but for the average Joe Cabbage on the street, something like this would slip past without even being noticed, so it would be highly unlikely that a Government would be brought to account on it. The mere fact that it is in a discussion document reveals they believe that most won't pick up on the implications. Most people do not realise the implications of the OBR, and haven't squealed about that, they equally don't understand that the money they believe they own, on deposit in the bank, is actually not theirs - they've given it to the bank! And if there is a bank crisis they are very likely to lose it, possibly all of it. This document is aimed at them losing it all!

The RBNZ should do its job and plan to take responsibility in the event its regulations and its regulatory oversight fail.

There is no need for taxpayer funds, the necessary equity injections could be done by the RBNZ alone (if given the powers)

Confused.... "no need for taxpayer funds ... the RBNZ would inject the equity". Huh?

Let's take a step back. If the RBNZ believe there is even a remote chance of the capital of a bank being wiped out they need to act to increase the required level of capital ~ irrespective of the "cost" on reduced depo rates.

Regarding "what if" scenarios, absolutely the RBNZ should have the ability to bail in all unsecured debt. However there is a question mark about deposits over the proposed insured amount. Presumably these should be treated the same way as normal debt ?

Certainly those deposits were receiving a fair premium over the govt bond rates so why shouldn't they be considered the same as other debt ?

Global sovereign interest rates are depressed because those with the resources to create credit (banks) are buying these bonds as a hedge against an imminent liquidity crisis. Thus, they no longer represent a realistic "risk free" benchmark to measure heightened corporate credit risk, More so when central banks are cutting short term official rates with the devotion of religious zealots in their endeavour to repeatedly fail to raise inflation.

{kind=link}

Thanks Gareth

How many people in NZ are really aware that the banks in Oz and NZ were recapitalised by the reserve banks during the GFC? Not many I’d guess. Bail-in is a real issue, the new depositor insurance and guarantee needs to be clarified properly so consumers (depositors) are aware at what point it would kick in... will customer deposits be safe? Will shareholder equity be bailed in first? Then bond holders? (Lots of banks selling bonds at present in small doses of hundreds of millions $800 million Westpac bond recently - $200 million ANz bond too). Will the legislation be published by the main media outlets with a simple explanation of what it means? Because the reality of the situation is that not enough people read interest.co.nz to know what’s going on.. even the recent tax changes to loss making properties (whilst anticipated) was not reported by our mainstream press.

Fully support you bringing some important information to light... in amongst the general ‘all blackout’ of important information we seem to have in NZ.

"the banks in Oz and NZ were recapitalised by the reserve banks during the GFC"

Are you referring to the Wholesale Funding Guarantee scheme? If so, this was not a recapitalisation of Banks. It lasted just 18 months. Treasury charged the banks for this scheme, and came out with a sizeable profit. At no point did the NZ (or Aussie) Government take any equity position. It is quite wrong to characterise this as a "capitalisation". A temporary protection yes, and confidence booster, yes. But definitely not a capitalisation.

Also, OBR clearly states who goes first in any rescue. No mystery there.

There's more detail on the wholesale guarantee scheme for those interested below (from Oct 2014 https://www.interest.co.nz/bonds/72629/curtain-fall-crown-wholesale-fun…). For a more generic look at the NZ GFC response see this one https://www.interest.co.nz/banking/95821/collapse-lehman-brothers-gfc-and-all-it-spawned%C2%A0-sub-prime-mortgages-donald-trump%C2%A0plus

And for details of how OBR might work, if ever used, see this - https://www.interest.co.nz/bonds/64411/if-bank-failed-and-open-bank-resolution-policy-was-implemented-how-would-it-affect-bank

Curtain to fall on Crown wholesale funding guarantee in November when US$71m ANZ bond is repaid

By Gareth Vaughan

It may be a tiny sum in the context of New Zealand banks' overseas borrowings, but when a US$71 million (about NZ$90 million) ANZ five-year medium term note issue matures and investors are repaid on November 19, it'll bring the curtain down on a major, albeit low profile, part of New Zealand's response to the Global Financial Crisis.

The ANZ medium term note issue is the final piece of bank borrowing carrying the Crown wholesale funding guarantee. This was put in place at the height of the GFC by then-Finance Minister Michael Cullen on November 1, 2008. The wholesale scheme has been used by ANZ, BNZ, Westpac and Kiwibank, but not ASB. Taxpayer liability peaked at $10.7 billion in November 2009.

The scheme was initiated as an opt-in wholesale funding guarantee facility. At the time Treasury and Cullen said the objective was to facilitate access to international financial markets by New Zealand financial institutions, in a global environment where international investors were highly risk averse and where many other governments had offered guarantees on their banks’ wholesale debt.

Although the scheme was closed on April 30, 2010, bank debt issued under it continues to carry a taxpayer guarantee until it matures, with the last of this - the US$71 million ANZ deal - maturing on November 19.

"Like all our maturing debt, we will repay it on the due date," an ANZ spokesman said yesterday.

Kiwibank's’s A$250 million kangaroo bond, the second to last guaranteed deal to mature, matured on October 20, with a Kiwibank spokesman confirming it was repaid in full. On July 28 Westpac repaid, on the scheduled maturity date, its remaining $1.8 billion worth of debt guaranteed by taxpayers through the scheme. And the last of BNZ's guaranteed borrowings, a ¥3 billion, five-year medium term note, matured on June 2.

No losses & $289m in fees

Unlike the much higher profile Crown retail deposit guarantee scheme that cost taxpayers nearly $1 billion due to the collapse of several finance companies headlined by South Canterbury Finance, the wholesale scheme hasn't lost taxpayers any money. No provision was even made for losses under the scheme in the Crown accounts with Treasury having considered the probability of loss remote.

Treasury says fees totaling $289 million were received by banks participating in the whole guarantee scheme. The Government received a fee from each participating bank based on its credit rating and the term and amount of guaranteed debt issued.

Although the Australian parents of New Zealand's big banks bought back some of their debt guaranteed under Australia's equivalent scheme, the New Zealand banks didn't. That's because the Australian banks have had to pay monthly fees on all their outstanding guaranteed debt. In contrast the New Zealand banks paid Treasury fees upfront when each guarantee was granted, (there were 25 in total), and Treasury said the fees were non-refundable.

Let's hope the righteous claims of moral hazard can once again be suppressed when it comes to extending comfort (rescue) to domestic creditors rather than their foreign counterparts. I am sure local bank depositors would accept a modest fee as a cost rather than an as yet to be determined OBR type capital haircut since ..."transmission of modern day monetary policy works mainly through the asset markets and shifts the balance of risks towards asset cycles and financial stability". Evidence here and here

Treasury is the NZ institution I take it ?

Wilkes was referring to what International Reserve Banks did for NZ and Aussie banks (effectively same thing)

I think an ex governor of the RBNZ wrote a book on this didn't he?

Mike, can you please clarify what you mean here? Which international reserve banks recapitalised NZ banks and when?

Fed I am told

I was told by a now ex-RBNZ official NZ never drew down any of the dollar swap lines offered then by the FRBNY.

The Fed had engaged in, essentially, balance sheet expansion even before QE. These emergency liquidity measures, mostly dollar swaps arranged with foreign central banks, had ballooned the Fed’s asset side, which in turn increased the level of bank reserves (double accounting). Link

Yes agree... NZ never required any use of the swap facility put in place. Not that would constitute 'recapitalisation' as was suggested above by Joe Wilkes.

An accepted USD currency swap deal offered by FRBNY would be registered as their asset, hence a loan and surely a capital injection to the RBNZ? I wonder what the RBNZ would do with the dollars other than lend to local bank institutions' correspondent banks in New York?

How is a loan providing capital? If you don't understand the difference between a loan and capital then please do us a favour and step away from the keyboard.

Hi Joe,

I do find it interesting to note who draws a response from Interest Staff, even where what contributor is saying is not directed to that author.

Joe, I am aware of two Australian banks that took money from the US Fed to help them stay solvent after the GFC. One was NAB and I think the other was Westpac Australia. However it wasn't reported at the time and I only came out, years after the event.

As we are continuously told following hilarious "risk scenarios"and stress tests, our banks are sound, so no need to worry is there? Except you might want to read what the Indian prospect for BoE governor has been saying about the state of bank risk in the world. Mr Bernanke, bless him, told us in 2007 that everything in the garden was just rosy. I am afraid that if you keep redistribution wealth upwards to the top 20% (including all those landlords trying to supplement their pensions) in NZ and elsewhere, and not giving the 75% dependent on wage income any decent rises since 1973 (but rather replacing it with borrowing largesse) then banks are per se given more and more power to make a god-awful mess when the cycle goes bust.

Talk about the tail wagging the dog ?

Who's in charge of the rules here , the Banking overseers in the RBNZ, or the Banks ?

John Maynard Keynes warned us of the systemic risks associated with the creation of money by private banks and how they fell outside the control of Central Banks and Banking Regulators .

We need strong CAPITAL ADEQUACY RATIOS to ensure our banks are safe .

Their activities , while regulated to some extent , are not controlled enough , they have the ability to destabilize the whole economy .

There is a risk Moral Hazard in the banks business model where the Central Bank or the public assume the debts of banks if the collapse .

They are TBTF and neither Central Banks nor Governments can do anything about it, except bail them out when the time comes. That is the strangle hold Banks have over the economies in most of the western countries.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.