Westpac New Zealand's annual profit is down 43% thanks to a COVID-19 related surge in loan impairment charges, and as expenses rose and income fell.

Westpac NZ's September year net profit after tax fell $414 million, or 43%, to $550 million from $964 million last year.

The fall came as the bank's impairment charge jumped to $320 million versus a net impairment benefit of $10 million last year. Meanwhile, net operating income fell $133 million, or 6%, to $2.282 billion, with net interest income down $24 million, or 1%, to $1.943 billion. Operating expenses climbed $66 million, or 7%, to $1.059 billion.

"We've provisioned for an increase in expected lending losses due to changing economic conditions, largely driven by COVID-19. However, our underlying asset quality remains strong," Westpac NZ CEO David McLean says.

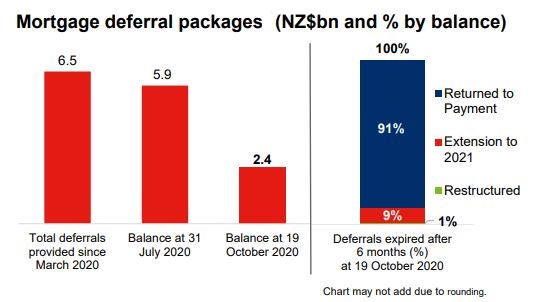

McLean says Westpac NZ has provided mortgage and loan repayment assistance to 21,959 customers, and more than $9 billion of new and restructured business lending. Australian parent Westpac Banking Corporation said as of October 19, 74% of deferred NZ mortgages - worth $4.5 billion - had reached the end of their initial six month deferral. Most had returned to paying with $500 million worth of balances granted an extension.

"Over the past year we've expanded our residential [mortgage] lending by 7% and have helped first home buyers into 5343 homes. We've increased our business lending by 3% and have been one of the few banks to expand our lending to farmers and agriculture," McLean says.

The bank's net loans grew 5% to $88 billion, and total deposits increased 10% to $71 billion. Westpac's KiwiSaver funds under management increased 14% to $8 billion.

Westpac NZ's net interest margin fell 19 basis points to 1.97%. Westpac NZ attributed its higher expenses to higher spending on risk and compliance programmes, including meeting the Reserve Bank's outsourcing requirements.

Westpac Banking Corporation posted a 62% drop in annual cash earnings to A$2.608 billion. Its net interest margin fell nine basis points to 2.03%, return on equity was down to just 3.83% from 10.75%, and common equity tier 1 capital ratio, as a percentage of risk weighted exposures, rose to 11.13% from 10.67%. The bank's annual dividend was 31 cents per share, equivalent to 49% of cash earnings.

Westpac NZ's press release is here.

Westpac Banking Corporation's annual results announcement is here.

Westpac Banking Corporation's investor presentation is here.

And the Westpac Banking Corporation press release is here.

15 Comments

Westpac New Zealand extended 62% of loans to housing to record a $3.727 billion increase from last year, while lending to all other categories combined fell.

Orr and Robberson have told all the banks lend to people with low equity who cant save a 20% deposit and they will back them up.

So that is what happens.

The capital allocation in NZ is so distorted by central government interference via Treasury and the RBNZ and the Income Tax Act!

It's just ridiculous. Massive wealth transfers from poor to wealthy sponsored by the Reserve Bank of NZ, and we head toward results like this.

Audaxes/Stephen, not sure where you're getting that from. The Westpac results show both mortgage and business lending grew.

Those are Westpac Group figures, differ a bit from Westpac NZ.

All bank balance sheets for public consumption are stylised approximations. I could never reconcile my bank's trading room balance sheet with the audited version.

Yet some here keep calling this "responsible" lending.

Is this responsible RBNZ regulatory oversight?:

Banks extending 60 % of their lending to one third of already wealthy households to speculate in the residential property market because the RBNZ offers them an RWA capital reduction incentive, to do so.

Or this:

RBNZ cutting OCR in half five times since July 2008, causing the rich to capitalise rising discounted present values of future asset cash flows.

{kind=link}

{kind=link}

The answer is a resounding no. The RBNZ has, to all intends and purposes, abdicated its regulatory oversight role.

Does the supposed independence of the RBNZ include being free to wreck the NZ financial system ?

Here's an OECD stat from 2016 ranking member countries by proportion of investment (gross fixed capital formation) locked up in dwelling assets (excluding land).

Unsurprisingly, Canada and NZ take the top 2 spots among Western nations.

Hmm I wonder what happened in Ireland and Greece that put them back to the bottom of the list...

They were #1 and #2 in 2007.

I guess their central banks' inability to print currency to protect asset prices may have played a big part in their demise from top slots!

Can NZ join the Euro zone please?

Might be wrong but aren't loan impairment charges actually provisions which can come back to profits when the dividend handcuffs come off?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.