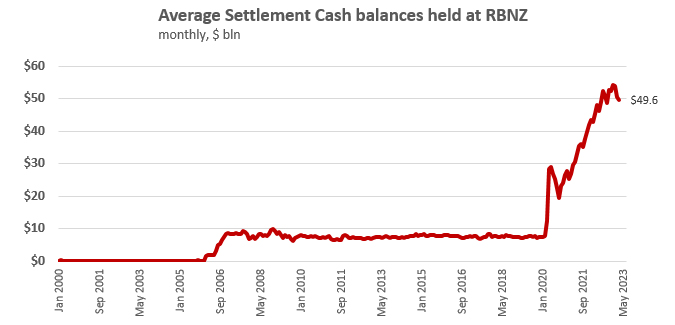

The RBNZ is ending March with fat balances from its depositors. They have been substantial for many months now.

These balances are known as Settlement Cash. And they pay interest on them, at the OCR level.

The owners of these balances are the Government (Treasury) and the banks.

These balances have swelled sharply as a result of outsized fiscal and monetary support policies during the pandemic.

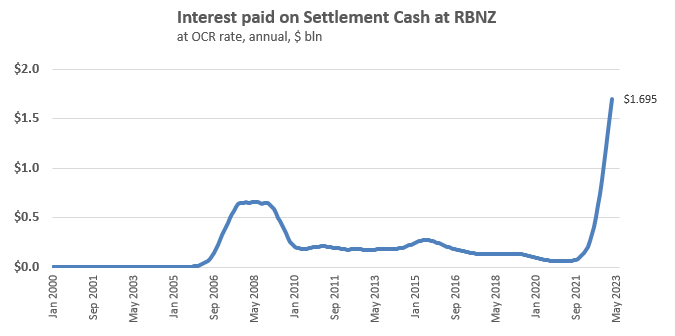

But when the OCR interest rate rises fast, the amount of interest being credited to these account holders has been turbocharged.

When the OCR interest rate was just well under 1% in 2020 when these balances started to rise quickly, the amount of interest was hardly significant.

But the combination of very fast rising balances (now $48.5 bln) and a fast rising OCR (now 4.75% from a rising trend that started in mid 2022) has turbocharged these interest payments by the RBNZ to its depositors.

It is hard to see these balances receding now that the 'reservoir' has been filled. It could (and probably will) recede if the economy stays positive. But that is a brave assumption at this point in the economic cycle.

And that means, if the OCR rises to 5% next week, and the Settlement Account balances stay over $48 bln, that annual cost will keep on rising to about $2.4 bln (from the $1.7 bln in the chart above).

Settlement cash balances are funds used to settle transactions between financial institutions. When one bank owes money to another bank, banks will use settlement cash to settle the transaction. Settlement cash can also be used to settle transactions in other financial markets, such as the foreign exchange market.

The Reserve Bank plays an important role in managing the country's payment and settlement systems, and settlement cash is an important tool for ensuring that these systems operate smoothly and efficiently.

Settlement cash balances can rise quickly due to several reasons involving the economic cycle.

If lending activities decrease, banks and financial institutions will have more cash on hand, leading to an increase in settlement cash balances. Reserve Bank policies can also affect settlement cash balances. For example, when they buy securities for financial stability reasons or lower interest rates, that would increase the amount of cash in circulation. And economic uncertainty plays a role too. If there is economic uncertainty, banks and financial institutions may hold more cash as a precautionary measure, which would result in an increase in settlement cash balances.

None of these reasons suggest settlement cash balances are about to decline significantly. And there is little expectation the OCR is about to be cut. So, so long as the RBNZ pays the OCR rate on these balances, the cost to them will be high. And you have to wonder, in a recessionary or low growth period, perhaps earning 5% on these balances at no risk is better than lending. Certainly high earnings on settlement cash balances will encourage banks to be very conservative in their lending policies.

Not that this final observation is anything more than a thought-experiment, but if the banking system can make $2.4 bln (before tax) on these balances, that would represent $1.7 bln after tax, and a quarter of their 2022 tax-paid profits.

Finally, it is probably worth pointing out that at 4.75% the current OCR that the RBNZ is paying its depositors, Treasury pays Kiwi Bond holders only 4.25% for terms of one year and longer. The RBNZ paying +50 bps more (also for zero risk) is a premium Kiwi Bond holders would love access to.

15 Comments

The way to reduce the settlement cash to about 10 billion - which is about where it needs to be for liquidity in the banking system - is to undertake quantitative tightening (QT) at a much more rapid rate. That requires Treasury and other bonds held by RBNZ to either be sold back into the open market or sold to Treasury Debt Management Section.

Reducing the interest paid on settlement cash is one of those ideas that is appealing but would lead very rapidly to lower term deposit rates. And that is not what we need right now.

There has been a lack of commentary on the need for a rapid QT to counter the inflationary impact of QE. The current RBNZ QT policy is at a paltry annual rate of $5 billion sold back to Treasury.

KeithW

Is there a direct link between rate paid on settlement deposits by the RBNZ, and retail TD rates? Banks need to raise funding at whatever level they can get away with. Everyday depositors can't access the RBNZ facility so there is no price tension.

The banks need to hold deposits matching their lending and it is the act of lending which creates these deposits in the first instance but their reserves are not a part of their deposits or their lending. Standard and Poor's explains things quite well here. https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

Thanks for the link.

Do banks need to match deposits matching lending?

I thought capital requirements is the only limit for lending??

It's just a matter of maintaining their balance sheets with assets matching liabilities. They will also loose reserves to the other banks through the interbank payment system if they don't maintain their deposits.

How does Risk Weighted Assets and capital ratios fit in this explanation?

Also this settlement cash or reserve expansion was never needed I feel sometimes. FLP was just a new acronym added to show people that the banking system is helping the country in the pandemic. The banks could always get money from central bank by pledging assets for interbank settlement

It comes down to what what works out as the lowest cost to a bank I suppose. Borrowing back reserves from other banks or from the central bank carries a higher cost.

Australian economist Steven Hail has several useful lectures about banking on YouTube. https://www.youtube.com/watch?v=zXMdugbKh4I&t=19s

Ooh.. will bookmark and watch his perspectives.. is he mainly talk about Aus banking sector?

Got so many in the list.. Richard Werner is the one who surprised me with the money creation theory. I guess initially this was considered just conspiracy theory, but now Bank of England, RBNZ are approving it.

He still thinks everything happening in banking is conspiracy.. which I'm not sure is true. I think bankers are doing trial and error and in the process making huge money..

He was originally from the UK where he worked in banking and he now lectures at the University of Adelaide. Economist Steve Keen is also well worth listening to and can be found on YouTube.

NZ Treasury buying RBNZ QE bond inventory extinguishes outstanding government bond issuance. QT involves the sale of RBNZ owned QE bonds back to the market place until they are redeemed in the future.

"If lending activities decrease, banks and financial institutions will have more cash on hand, leading to an increase in settlement cash balances".

Totally incorrect as banks don't lend out the reserves held in their exchange settlement accounts and so lending has no effect on them. Settlement account balances increase due to government budget deficits and they decrease again when bonds are issued or the government runs a surplus.

Reserves are made up of the governments own currency and have nothing to do with bank deposits which are generated through lending.

Question? How does the Reserve Bank generate the income to pay the $2.4 Billion in Interest-or are those just more QE dollars?

It's the same place that the government gets all of its money from, its just typed into existence from a computer keyboard at the RB. Only MMT accurately describes how the governments finances operate. If you study orthodox economics it soon becomes apparent that it lacks credibility.

I'm guessing it's $2.4 Billion that is in a roundabout way diverted from being spent elsewhere, like on hospitals or roads.

The RBNZ is ending March with fat balances from its depositors. They have been substantial for many months now. These balances are known as Settlement Cash. And they pay interest on them, at the OCR level. The owners of these balances are the Government (Treasury) and the banks.

If a syndicate of banks underwrites a NZ Government bond issue, the created out of thin air credit is lodged at the RBNZ's Crown Settlement Account. Simultaneously the Bank Settlement Accounts are debited the same amount for the participating underwriting banks, since they are in receipt of the accruing coupon payment from the issued bond. Once the government disburses the underwritten bank credit to eligible beneficiaries' bank accounts, the banks are re-credited the deposit credits since they have an obligation to reward the new private bank deposits. Taxes collected from depositors' bank accounts are lodged at the RBNZ's Crown Settlement Account ledger which causes the Bank Settlement Accounts to once again be debted. There is hardly any need for the RBNZ to credit OCR to the Crown Settlement Account.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.