By Ashley Farquharson*

The recent collapse of Silicon Valley Bank highlights the importance of managing interest rate risk effectively, especially in a rising interest rate environment. This risk is caused by fluctuations in the value of banks’ assets and liabilities as interest rates change. If not managed well, changing interest rates can adversely affect banks’ capital and liquidity positions.

What is interest rate risk?

Interest rate risk is the exposure of a bank’s financial position to movements in interest rates. A bank’s financial position is affected by interest rate movements because current interest rates affect the present value of the future cash flows from their assets and liabilities. Bank profitability can be affected over time if assets with long-term fixed returns (e.g. government bonds) are funded with liabilities that are sensitive to current interest rates, such as deposits. As interest rates rise, the costs of deposits can become more than the returns from banks’ assets, eroding net interest income. Rising interest rates also lower the present value of long-term fixed return assets, which can create potential losses that affect their capital positions. The extent of the impact depends on the magnitude of the interest rate increase and if these losses are offset by having funding with similar fixed returns (which would see equivalent declines in present value), or by hedging with other products.

Interest rate risk can have implications for liquidity as well. For a bank with high exposure to fixed-income assets, rising interest rates may lead to the liquidity problems seen with Silicon Valley Bank. If banks are unable to raise deposits at higher interest rates and pass costs through to loans, this can lead to sudden short-term liquidity problems. Likewise, concerns over the viability of a bank that is heavily exposed to interest rate risk may shake the confidence of depositors in its solvency, potentially leading to increased deposit outflows. In extreme scenarios it can contribute to a bank run.

Mitigating interest rate risk

Banks use strategies such as matching the repricing maturities of assets and liabilities to mitigate interest rate risk. For example, one-year fixed rate mortgages could be matched with oneyear fixed rate funding (e.g. term deposits), so that the impact of rising interest rates is offset. They could also use derivative products such as interest rate swaps, futures and forward contracts to hedge any remaining repricing mismatch in their exposures. These strategies can help banks manage the impacts of interest rate changes on their balance sheets. In New Zealand, both of these strategies are commonly used to control risk.

After the 2008 Global Financial Crisis, additional requirements were implemented in the New Zealand financial system to enhance resilience by strengthening capital and liquidity requirements. We expanded prudential requirements to address capital and liquidity risk by requiring banks to have robust frameworks for managing interest rate risk.1 New Zealand banks are required to hold sufficient capital to cover potential losses arising from interest rate risk, which provides banks with an incentive to manage related prudential risks carefully. They are also required to value their liquid assets at market price instead of book value.

New Zealand banks’ interest rate risk

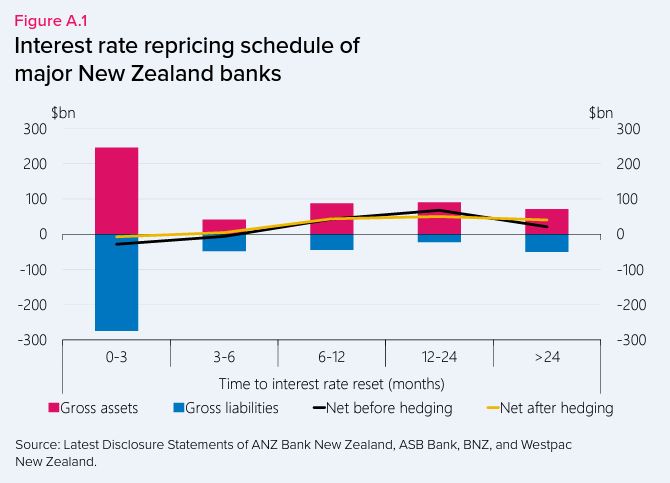

New Zealand banks’ lending is generally at variable or short-term fixed interest rates, which means the potential losses for banks from interest rate movements are smaller. Figure A.1 shows how banks match assets and liability repricing maturities to reduce the impacts that interest rate changes have on their net interest incomes. Additionally, residual risk is hedged to further mitigate the risk of losses. New Zealand banks also hold fewer bond assets than banks in other developed economies, and these bonds are accounted for at fair market value.

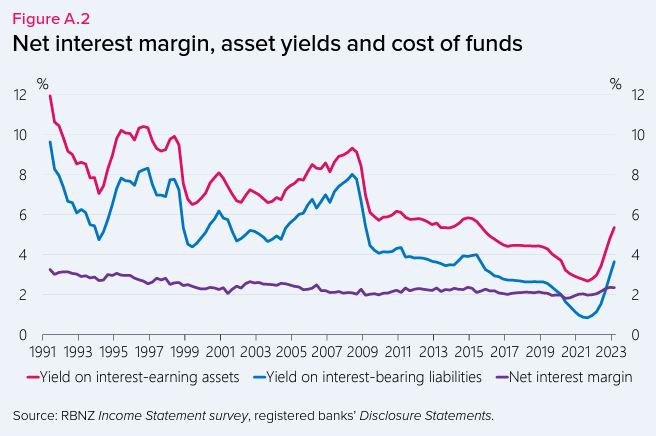

As a consequence of banks’ generally prudent risk management, we see little relationship between fluctuations in interest rates and banks’ net interest margins (figure A.2). This reflects the fact that the yields on banks assets and liabilities tend to move together as interest rates adjust.

1 Banking Prudential Requirements - Reserve Bank of New Zealand - Te PuteaMatua (rbnz.govt.nz).

* This article is an excerpt from the Reserve Bank's May 2023 Financial Stability Report, due for release on Wednesday, May 3.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.