By Martin Foo*

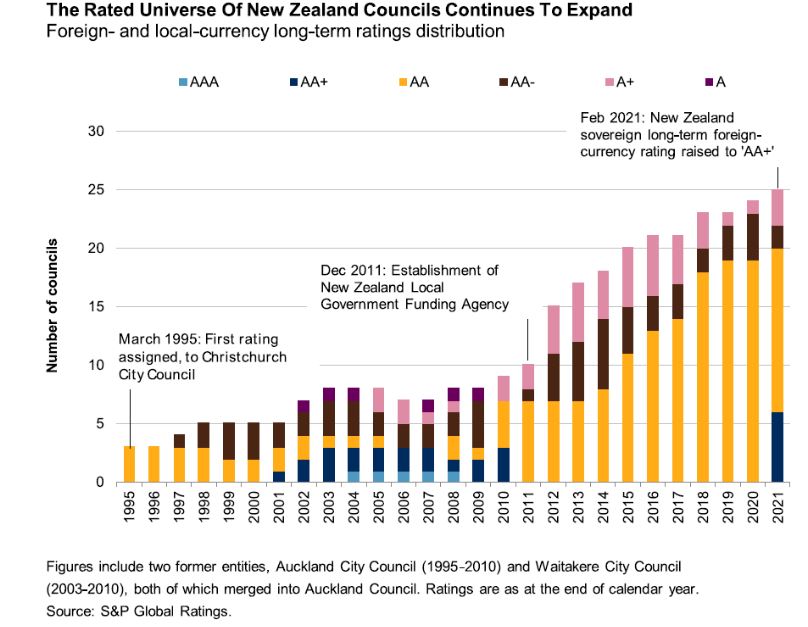

Much has changed since S&P Global Ratings first assigned credit ratings to Christchurch City Council and Dunedin City Council in March 1995. New Zealand’s population and per-capita GDP were both 30% smaller than today. Net government debt was on the decline. Overseas, the country had just joined the fledgling World Trade Organization, and the Hollywood thriller “Outbreak,” about a deadly airborne virus, was a box-office smash.

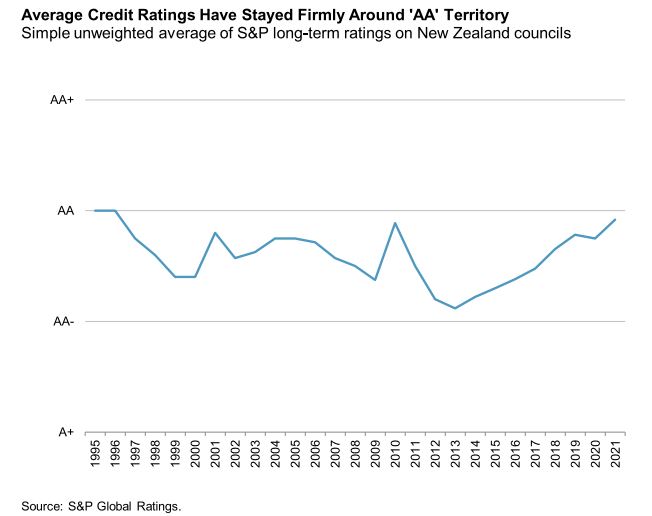

Much has also stayed the same. Local council creditworthiness remains robust. The average rating has hovered around ‘AA’ territory, near the apex of our global rating scale. For comparison, this is on par with the sovereign nations of Belgium, France, South Korea, and the United Kingdom. In a recently published report, we outline the history of our credit ratings on Kiwi local authorities.

During the past quarter-century, more and more councils have sought ratings as they borrow to finance infrastructure and economic development. They have borrowed primarily from the New Zealand Local Government Funding Agency (LGFA) since its inception in 2011, but also sometimes via banks and capital markets. Our portfolio reached a new high of 25 in 2021.

A handful of councils, principally in major population centres, account for an outsize share of economic activity and debt. As such, despite representing just one-third of New Zealand’s 78 local authorities, the 25 councils rated by our firm account for most of the country’s stock of subnational debt.

The COVID-19 pandemic has had only a modest effect on council finances. Recent outturns have beaten early pessimistic projections. Sector-wide accrual revenue in fiscal 2021 (i.e., the year ended 30 June, 2021) grew 3.2% year on year, much better than the 2.3% to 11% contraction forecast by the Department of Internal Affairs in May 2020 during the bleakest quarter of the pandemic.

We haven’t lowered our ratings on any councils as a direct consequence of the pandemic. (The only downgrade in recent years was due to idiosyncratic factors, namely the dismissal of elected councilors and appointment of Crown commissioners to Tauranga City Council in early 2021.) It helps that New Zealand quickly contained the initial spread of the coronavirus, facilitating a V-shaped rebound to above pre-crisis GDP levels. This was an economic snapback without historical parallel.

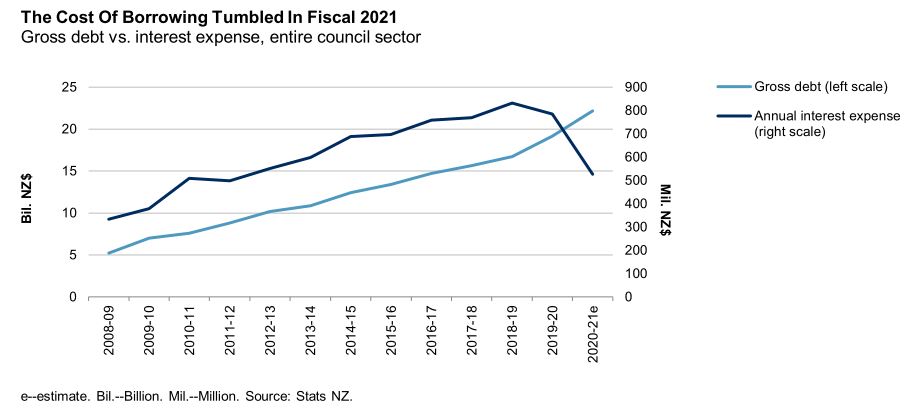

Interest expenses should remain manageable even as the monetary cycle turns. Councils are refinancing more expensive debt incurred in the past, and their interest-rate hedges will mature over the next few years. The cost of borrowing nosedived in fiscal 2021. This was aided by Reserve Bank of New Zealand policy rate cuts and a quantitative easing programme that included purchases of LGFA bonds.

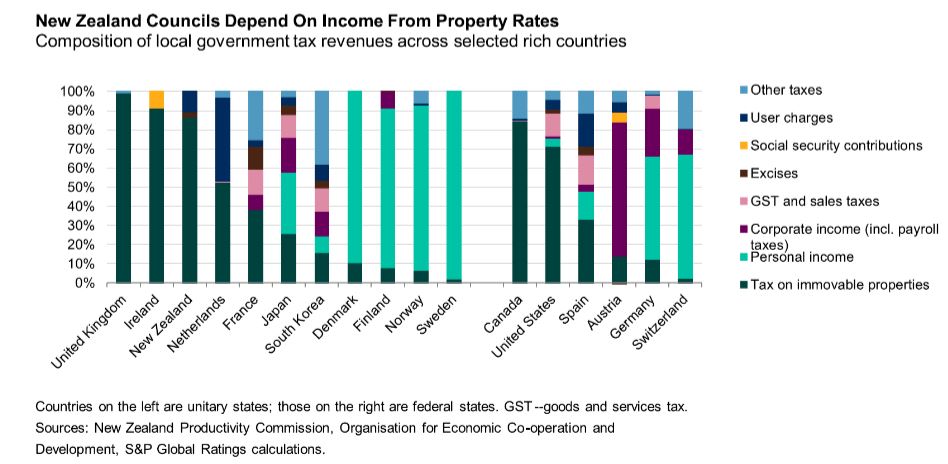

One of the key reasons for their solid financial performance is councils’ reliance on revenue from property rates (i.e. recurrent taxes on immovable property). Rates are an efficient, transparent, and a cyclical income source. Some subnational peers in other jurisdictions have tax bases that are inherently more volatile. These include consumption, transaction, corporate income, and personal income taxes.

However, recurrent property taxes are a double-edged sword. While robust in downturns, councils’ revenue bases aren’t very buoyant in economic upswings. Councils complain that they lack adequate funding tools to respond to population growth and pay for greenfield infrastructure.

While operating performance is strong, a rise in debt-financed infrastructure investment is now putting downward pressure on some council ratings. The latest round of 2021-2031 long-term plans, released in mid-2021, signal an uptick in capital expenditure. This is necessary to comply with new Crown government regulations, meet the demands of growth and housing intensification, improve resilience to climate change and earthquakes, enhance quality of life by building ‘nice-to-haves’ such as new sports facilities, and plug substantial infrastructure deficits.

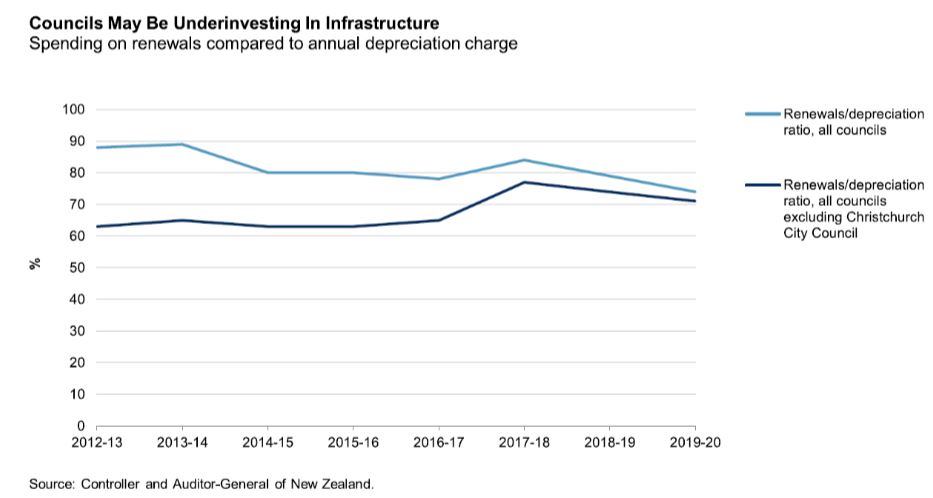

The last item is of particular concern. Much of New Zealand’s public infrastructure, built in the 1950s and 1960s, may be approaching the end of its useful life. Many councils appear to be inadequately replacing assets as they are ‘used up’. The Auditor-General has found that annual investment in renewals over the eight years through fiscal 2020 was insufficient to match depreciation. This shortfall is even more acute when excluding Christchurch City Council, which has spent big on reconstruction from the 2010-2011 Canterbury earthquakes.

Although capital budgets are rising, deliverability is a challenge. In our liaison meetings, councils widely report difficulties in hiring qualified staff and contractors and in garnering competitive bids at public tenders. Compounding the problem is the fact that a relatively small number of suppliers dominate the civil engineering market. Local authorities therefore compete for resources not just with each other but with the Crown’s New Zealand Upgrade Programme, too. We expect councils to execute about 70% to 80% of their capital budgets, on average, though there can be wide variations across the sector.

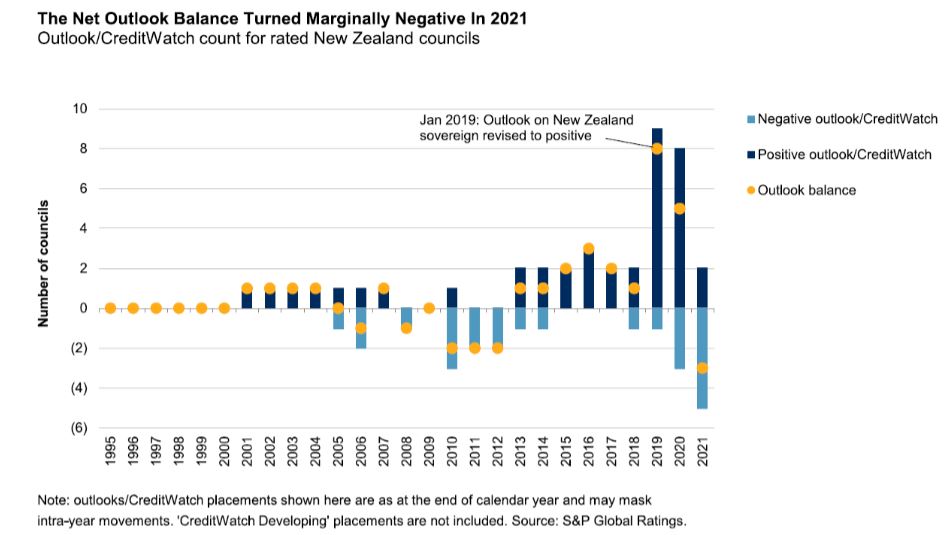

After six council upgrades in February 2021, the ascending trend in credit quality over the past eight years may have reached a gentle inflection point. Our net outlook bias for the sector turned negative in 2021, for the first time since 2012. (For reference, a negative outlook denotes a roughly one-in-three chance of a downgrade over the next two years.)

Here, it’s important to remember what credit ratings are for. An issuer credit rating, by definition, is our forward-looking opinion of an obligor’s capacity and willingness to meet financial commitments as they come due. A negative rating action does not mean it is wrong for a council to borrow. We acknowledge that elected officials face myriad tradeoffs. They may choose to balance a desire to maintain high credit ratings against other political, economic, and community priorities.

On a final note, the emergence of the Omicron variant is a reminder that the pandemic is far from over. In late January 2022, New Zealand announced the countrywide imposition of “red traffic light” rules after confirming the first local cases of Omicron. Recent experience from other countries suggests that the next few weeks will be difficult, with probable disruptions to supply lines and higher workforce absenteeism as the virus takes hold. Economics and epidemiology will remain intertwined for the foreseeable future.

*Martin Foo is an Associate Director at S&P Global Ratings. This article is an excerpt from a report that appears here.

4 Comments

And along comes three waters . Many council beauracracies rely on water charges to prop up other expenses so losing water assets will knock their business models around , and if the ratepayers are expecting rates to drop as a consequence of three waters you are dreaming. This comment includes sewerage and stormwater.

Hamilton City Council Rtes bill came in today:

land and property: ~580,000

rates: 457.35 (x4=$1,830)

Water managment= 30.8%

Transport= 21.3%

Visitor destinations= 15.4%

parks & Rec= 11.3%

My Nelson rates increased 350% since 2008--well in excess of general inflation which was 30%. While council has put essential infrastructure on the back burner during this time, spending was lavish on non-essentials that benefited certain lobby groups. So now we are told that financial management has been pretty good?!

All they need is to sell infrastructure specific bonds to the general public to raise funds specifically for infrastructure work.

Then the funding portion for infrastructure is sorted.

But I must admit it won't be easy to untangle the knots in funding between councils and the beehive before we can make it clean.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.