This is the executive summary of the 2026 OECD Global Dent Market report.

Global debt markets proved resilient in 2025, despite borrowing levels reaching historic highs. Volatility has remained limited and corporate credit spreads neared record lows. However, shifts in the investor base are transforming these markets. More price-sensitive investors are providing much needed liquidity but may be increasing market sensitivity to shocks. Governments and companies have been shifting their issuance towards shorter maturities to mitigate the impact of rising long-term interest rates, increasing refinancing risks. These risks must be carefully managed to ensure that sovereign and corporate bond markets, with a combined size of USD 109 trillion, continue to provide stable financing to governments and corporations. This is especially important as they are set to play an increasing role in funding AI investment and defence spending, at a time when decisions on monetary policy, public debt and pension fund asset allocation are coming under growing pressure.

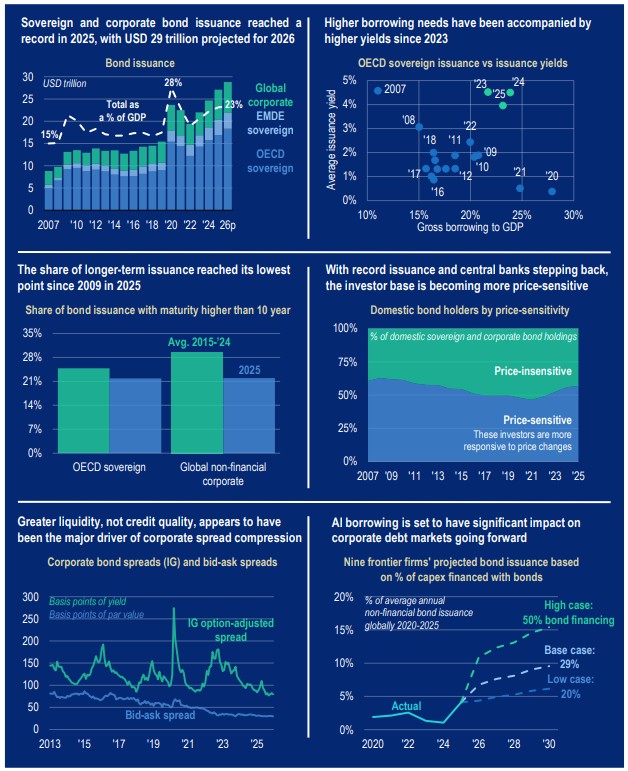

Governments and corporations are expected to borrow USD 29 trillion from markets in 2026, USD 4 trillion or 17% more than in 2024

Central government borrowing in OECD countries continued to grow in 2025, reaching USD 17 trillion, up from USD 12 trillion in 2022, and is expected to rise by a further USD 1 trillion in 2026. Outstanding sovereign bond debt now stands at a record USD 61 trillion, up from USD 55 trillion in 2024. Central government debt relative to GDP in OECD countries was stable at 83%, but is projected to rise to 85% in 2026, 39 percentage points higher than in 2007, before the global financial crisis. In emerging markets, sovereign bond issuance reached a record USD 3.4 trillion in 2025, 21% higher than in 2024, bringing the total debt stock to a record USD 12.1 trillion.

Much of the increase in borrowing is to refinance existing debt. In 2025, sovereign refinancing requirements in the OECD amounted to a record of around USD 13.5 trillion – near 80% of gross borrowing. This is up from USD 12 trillion in 2024, with projections for a further USD 1 trillion increase in 2026. At around USD 3.5 trillion, net borrowing requirements were stable in 2025 but remain substantially above pre-pandemic levels, and are projected to grow in 2026 to the highest level since 2020.

Private borrowing is also increasing. Corporate borrowing from markets reached its highest level ever in real terms in 2025 at about USD 13.7 trillion (USD 6.8 trillion in corporate bonds and USD 7 trillion in syndicated loans). Outstanding amounts reached USD 59.5 trillion at the end of the year, with USD 36.4 trillion in bonds and USD 23.1 trillion in syndicated loans. Given the scale of capital expenditure required to finance the expansion of AI, corporate borrowing needs are expected to continue increasing substantially.

Over the past five years, sustainable bonds have also become a more important source of capital market financing. Globally, the total amount issued through sustainable bonds was three times larger in 2021-2025 than in 2016-2020 for both the official and corporate sectors. Worldwide, companies issued USD 531 billion in sustainable bonds in 2025, while the official sector issued USD 486 billion. This represented a slight decline of 6% compared with the previous year, but was still more than 50% higher than in 2020.

Sovereign borrowing costs are elevated, and higher interest rates are beginning to impact the corporate debt stock

The post-2022 increase in interest rates continues to impact global debt markets. While shorter-term rates stabilised in OECD countries in 2025, 30-year yields rose significantly across most countries to a median of 4.1%, underpinned by elevated real yields. Concerns about fiscal trajectories are a key driver, but continued high bond issuance and a decline in demand for long-term assets have also pushed up longerterm yields. The expected excess cost of issuing longer-term bonds, which began rising in 2022, continued to increase. At the end of 2025, the average estimated 10-year term premium in the OECD reached 0.84%, the highest level in over a decade.

Sovereign and corporate borrowers have responded to the increase in longer-term interest costs by shifting their issuance towards shorter maturities. The share of issuance with a maturity over 10 years reached its lowest point since 2009 for sovereigns and the lowest on record for corporates in 2025. Another component of this adjustment is a heavier reliance on Treasury bills for funding. Treasury bill issuance continued to account for roughly 48% of total borrowing in 2025, close to a record high, and is projected to remain at this level in 2026.

While lowering current interest costs, the shift to shorter maturities increases refinancing risks. This pressure is particularly acute in emerging markets, where more than a third of the outstanding bond stock is set to mature within the next three years. Low-income countries face an even greater refinancing burden, with more than half of their bonds maturing over the same period.

Interest expenditures for corporates, which have more flexibility to adjust their issuance strategies depending on financing conditions, have not increased as much. However, the shift towards greater interest spending is also clear in this sector. The gap between the lower effective cost of outstanding debt and higher cost of issuing new debt has narrowed substantially. Consequently, for the first time since 2016, securities with an interest rate above 4% made up half of investment grade bonds at the end of 2025. As near-term refinancing needs primarily reflect maturing low-cost debt, this trend is set to continue.

The investor base has changed significantly, and more price-sensitive and leveraged investors could make markets more vulnerable to shocks

Central banks remain the largest domestic holders of government debt in many OECD countries, but as many major central banks have continued to shrink their balance sheets, the market is increasingly dependent on more price-sensitive investors, including hedge funds, households and certain foreign holders. This transition away from price-insensitive demand, in many ways a normalisation of the investor composition, could increase market volatility.

Corporate bond markets have seen a parallel shift in investor composition following the post-2008 regulatory overhaul, with open-ended investment funds, exchange-traded funds (ETFs) and, more recently, principal trading firms, playing an increasingly important role. Changes in the sovereign investor base reverberate in the corporate market. Investors willing to hold riskier securities at a time of lower yields may rebalance their portfolios as central banks withdraw, leaving the growing new corporate issuance to be absorbed by a smaller investor base.

Corporate credit spreads are historically low, but this does not primarily reflect increased credit quality

Despite record levels of borrowing and significant geopolitical uncertainty, corporate credit spreads remain near historical lows. Although fundamental indicators are positive – cash levels are high, earnings prospects are strong, and expected defaults are falling – tight credit spreads do not appear to be mainly driven by improvements in corporate credit quality. Part of the reason is a disproportionate increase in 13 GLOBAL DEBT REPORT 2026 © OECD 2026 benchmark sovereign yields, with some companies even trading at negative spreads to their sovereign equivalents. An improvement in liquidity is another important factor. A significant part of the reduction in spreads since 2013 is the result of decreased liquidity premia, as technological advances and more liquidity-friendly investors have entered the market. Increased investor risk-willingness has also contributed significantly to the decline, but default risk compensation has not decreased. Consequently, expected default losses now account for the largest share of corporate credit spreads by far.

As they shift to external funding to finance the capital-intensive AI expansion, technology companies are set to become ever larger issuers in debt markets

The technology sector has traditionally relied more on internally generated funds and less on external financing than most other sectors. The AI race is changing that dynamic. AI leaders – predominantly US technology firms – are tapping markets, from corporate bonds to private credit, to finance the expansion of the technology, notably for data centres. In 2025, nine major players commonly known as “hyperscalers” together raised USD 122 billion from bond markets, accounting for nearly half of all technology firm issuance globally.

Capital expenditure projections indicate that this is just the beginning. Cumulatively, these nine companies alone have forecasted capital expenditures of USD 4.1 trillion between 2026 and 2030 – about 36% more than total capital expenditure by all non-financial US companies in 2025. If half of these investments were financed through bond markets, these nine companies would account for 15% of historical annual average issuance by non-financial companies globally.

These developments may be setting corporate debt markets on course to become more equity-like. At 12% of global market capitalisation, these nine companies are already a core part of global equity markets. Given their current generally low levels of leverage and massive upcoming financing needs, they are shaping up to make a growing imprint on debt markets as well. Combined with the enormous AI-related financing needs of other sectors, from energy providers to construction companies, AI financing is set to transform these markets.

As pressures mount, sustaining the resilience of debt markets is essential for long-term growth

Debt markets have functioned with relative calm in 2025 despite growing pressures. The macro-economic environment is characterised by higher tariffs, heightened geopolitical tensions, and significant policy uncertainty. There are also internal pressures. The long-term stability and resilience of debt markets ultimately depend on governments and companies ensuring the sustainability of their debt.

Stronger efforts to promote fiscal prudence and to enhance the efficiency of public sector spending would not only help manage the current elevated debt burdens, but also create space for investment in infrastructure, digitalisation, and defence. It would also reduce the risk of crowding out corporate access to financing, which will be critical at a time when investment in AI is set to absorb a substantial share of corporate debt flows.

Debt markets are key to enabling investment in long-term growth. They have proved resilient to challenges thus far, but their resilience is not guaranteed. A strong and credible monetary policy framework, along with effective public debt management, has provided an essential foundation. Preserving that foundation will be crucial for maintaining investor confidence and ensuring the continued smooth functioning of these markets.

1 Comments

Here's a Perplexity generated AI summary version of the article for lay persons like me-

'Global governments and companies are borrowing more than ever, and they’ve mostly gotten away with it so far, but the way they’re doing it makes the system more exposed if something goes wrong.

Big picture

-

Total government and company bond markets are about USD 109 trillion, and borrowing keeps rising.

-

In 2026, governments and businesses together are expected to borrow USD 29 trillion, about 17% more than in 2024.

-

Markets have been calm and investors still willing to lend, but this calm depends on confidence staying high.

Governments: more debt, shorter terms

-

Government borrowing in rich countries hit USD 17 trillion in 2025 and is expected to rise again in 2026, with total government bond debt at a record USD 61 trillion.

-

A lot of this is just rolling over old debt, not new spending: around 80% of 2025 government borrowing in OECD countries was refinancing.

-

Because long-term interest rates are higher, governments are issuing more short-term debt (like Treasury bills), which is cheaper now but must be refinanced sooner, increasing the risk if rates spike or investors get nervous.

-

Emerging and low‑income countries are especially vulnerable because a large share of their bonds will mature in the next few years.

Companies: cheap money era ending

-

Corporate borrowing hit record levels in 2025, with about USD 13.7 trillion raised from bonds and big bank loans, and total outstanding corporate debt near USD 59.5 trillion.

-

Firms also shifted to shorter‑term borrowing to keep costs down, so they too face more frequent refinancing.

-

Interest costs on company debt are starting to rise as old cheap debt matures and is replaced by new, more expensive debt; by late 2025, half of investment‑grade bonds paid more than 4% interest.

Investors: more “nervous” money

-

Central banks are slowly shrinking their bond holdings, so more debt is now held by investors who care a lot about price and can move quickly (hedge funds, households, certain foreign buyers).

-

In corporate bonds, open‑ended funds, ETFs and trading firms play a bigger role; these can sell faster in a panic, which could increase market swings in a crisis.

Credit spreads and AI’s impact

-

The extra yield investors demand to lend to companies instead of governments (“credit spreads”) is very low by historical standards, even though borrowing is high and the world is geopolitically tense.

-

This doesn’t mainly reflect safer companies; it’s more driven by higher government yields, better trading liquidity, and investors being more willing to take risk.

-

Big tech companies, especially US “hyperscalers” investing in AI and data centres, are becoming huge borrowers: nine major firms raised USD 122 billion in bonds in 2025 and plan trillions in capital spending through 2030.

-

If they fund a large share of that through bonds, these few firms could account for a major chunk of global corporate bond issuance, making AI a central driver of debt markets.

What needs to go right

-

To keep this system stable, governments need more disciplined budgets and better‑targeted spending so their debt remains manageable and doesn’t crowd out private borrowers.

-

Central banks need to keep credible, predictable monetary policy, and governments must manage their debt carefully so investors stay confident.

-

Debt markets are still working smoothly, but with higher rates, shorter maturities, and more skittish investors, resilience can’t be taken for granted.'

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.