NZ swaps and bond yields closed 1-2bps higher yesterday. Overnight, US 10-year yields traded up from 2.04% to sit at 2.07% currently.

It was a very quiet day in the NZ market. It continues to price around a 70% chance that the RBNZ cuts rates by year-end and a 2.43% trough in the OCR by mid next year.

This is a fair representation of risks around our central view the Bank cuts the OCR to a cyclical trough of 2.50% (from 2.75% currently) by year-end.

The Bank of Japan left its monetary policy statement unchanged yesterday. It voted 8-1 to continue to increase its monetary base by ¥80t annually.

Average remaining maturity of JGBs purchased will be 7-10-years. It will continue this process to achieve its 2% inflation target for as long as necessary.

BoJ Governor Kuroda emphasised the Bank would ease further without hesitation, if needed, to secure its 2% inflation target.

However, he didn’t sound in any rush, pointing out Japanese consumer prices trends were improving and corporate sentiment was at a favourable level.

Overnight, in the absence of key US data releases, US yields drifted higher along with US equities. However, the move in both ran out of steam in the early hours of this morning. From intra-night highs above 2.08%, US 10-year yields now trade at 2.07%.

There are no key domestic data releases today.

Tonight, the BoE and ECB meet. The US Fed will release the Minutes of its Sept meeting. However, markets may view these as having been superseded by the subsequent disappointing US payrolls report.

Kymberly Martin is on the BNZ Research team. All its research is available here.

Daily swap rates

Select chart tabs

5 Comments

The Bank of Japan left its monetary policy statement unchanged yesterday. It voted 8-1 to continue to increase its monetary base by ¥80t annually.

Working for money is a loser's game in Japan. It's surprising the taxpayers haven't revolted to demand real stores of value in return for their efforts. Discounted Nikkei 225 call options would not be a bad bet.

My comment below was meant to be a reply to your comment...

Hmm, not sure about that, I think something has changed, although I'm unclear exactly what it is. The sudden jump upwards in the Yen at the last market fall was a surprise to me, but it suggests that carry trades are unwinding. Money seems to be folding back into itself worldwide as far I can tell, as debts taken out for speculative purposes are repaid. Could be a major trend change is taking place to give rising Yen and falling Nikkei.

There is a tendency amongst the Yanks to view Japan as a basket case, "a bug in search of a windshield" seems to be the phrase. I think they are probably wrong, as Richard Koo points out Japan in fact managed the collapse of their major boom rather well - the economy would have fallen 30% (maybe 50-80%) if they had not spread out the readjustment over 25 years. They have some of world's best manufacturers (Toyota, Nissan, Mazda, Subaru, Fanuc and a host of others) and are world leaders in all things robotic.

Japan will rise again, they are just monetising the legacy government debt (ie writing it off, without actually making the final ledger entry), makes sense to me.

Interested in your thoughts.

All trades are unwinding.

DEUTSCHE BANK SEES 3Q NET LOSS EUR 6.2 BLN

DEUTSCHE BANK TO RECOMMEND DIVIDEND CUT OR POSSIBLE ELIMINATION Read more

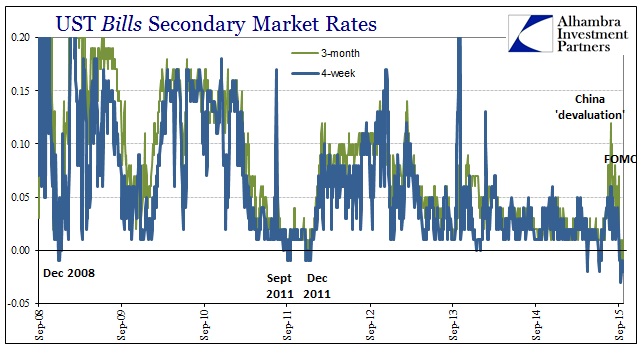

Now we know why players are scrambling for US TBill collateral.

{kind=link}

Negative t-bill rates, the 3-month most especially, represents only great stress. The number of times that those rates have been negative (bill prices at a premium) is inordinately few and particular: Read more

Japan will rise again, they are just monetising the legacy government debt (ie writing it off, without actually making the final ledger entry), makes sense to me.

I addressed the BoJ missing ledger entry speculation when replying to Stephen L. Read more

Thanks Stephen, it never ceases to amaze me how simple arithmetic of pluses and minuses on balance sheets can get so unfathomably complex. I particularly liked this chart:http://www.alhambrapartners.com/wp-content/uploads/2015/10/ABOOK-Oct-20…

{kind=link}

Ha, that's why I got into business too, in early 1980's Britain with 3.5million unemployed: “Becoming a salaryman wasn’t an option,” a relaxed Tomita, clad in a black polo shirt, said from Dip’s headquarters in the Roppongi area of central Tokyo. “Starting my own business was the only choice.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.