By Kymberly Martin

NZ swaps closed little changed yesterday, while NZGB yields closed down 2 bps across the curve.

Overnight, US 10-year yields traded down from 2.15% to 2.10%.

It remained fairly quiet on the home-front yesterday. NZ swaps briefly pushed a little higher mid-afternoon, along with AU counterparts, after the release of the China trade balance. However, by the end of the day, NZ swaps were relatively unchanged, with 2-year at 2.75%.

The market continues to price almost a 70% chance of a further RBNZ rate cut in the year ahead. We expect, during H1 at least, the market will remain inclined to price rate cut(s), although we continue to believe the RBNZ has a high hurdle for actually delivering further easing.

Overnight, Fed speaker Rosengren captured headlines. Reiterating a theme of Fed Chair, Fischer’s yesterday, he commented that he hopes the Fed does not have to use negative interest rates in the way the ECB has. But he does believe the pace of Fed rate rises will be gradual, justified by tepid inflation. He also said the Fed was “highly attentive” to offshore developments and should “take seriously” downside risks to the outlook.

He acknowledged that the market was currently pricing a flatter rate track than the Fed’s own projections. However he said that market views do not determine what the Fed will do. Currently the market prices less than two 25 bps hikes this year while Fed ‘dots’ imply four.

Today the local focus will be the AU employment report. Ahead of this release the market prices a further 25 bps rate cut from the RBA this year. This would take the AU cash rate to 1.75%. Our NAB colleagues are not expecting a cut.

Tonight the Bank of England meets. It is expected to leave its cash rate at 0.5%. The market has recently pushed back expectations of a first BoE rate hike. It now prices only a 30% chance of the cash rate being 25 bps higher by March next year. The Bank will be the first major central bank to meet in the New Year, so any comments it does, or does not make about recent global market volatility, will be seen as significant.

Daily swap rates

Select chart tabs

3 Comments

He acknowledged that the market was currently pricing a flatter rate track than the Fed’s own projections. However he said that market views do not determine what the Fed will do.

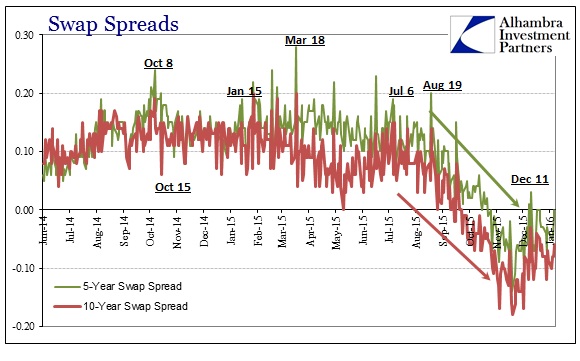

Meanwhile the totally dysfunctional US swaps market took another lurch downward into deeper negative territory in respect of US Treasury yields. View table

{kind=link}

And one hardly dares to mention repo fails in the money market tool most favoured by the Fed to lend a steadying hand to the higher Fed Funds rate corridor.

And meanwhile the US10T entry door is jammed packed while China uses the exit as a net seller.

http://www.bloomberg.com/news/articles/2016-01-10/china-retreat-from-u-…

It's a vicious cycle. The more dollar chasing going on the more China has to sell. Prepare for another Yuan devaluation if this keeps up.

You are not wrong - Scorching Demand For 10 Year Paper: Indirects Take Down Near Record 71%, Bid To Cover Surges Read more

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.