By Jarrod Kerr*

Paying Kiwi rates still feels alien to this old “receive everything” warhorse, but I refuse to fight the flow. One cannot be a warhorse without a few battle scars. The stitches of recent received positions have yet to be removed. But I’ve changed sides.

Have no fear, I have avoided my scheduled lobotomy to support the Wallabies. I still support the All Blacks. But I have switched to calling Kiwi rates higher.

I did so after the Trump victory “Kiwi interest rate forecasts revised higher on Trumpification”.

My worry now is the weight of money, switching and fixing. We have already paid the 1y1y rate from 2.39% (now 2.43% so not a big move). We want more exposure. So today we pay to 1y2y rate from 2.65%. The same idea but with a bit more curve.

We also recommend a received position in OIS. I just couldn’t help it. Old habits die hard…

To any balance sheet, corporate or trader with the ability to pay a fixed rate in Kiwi, now is still the time.

It is easy to look at current levels in disbelief compared to where they were. The US election has catapulted rates into another league. Strategically, there are plenty of risks that could bring rates crashing back down. Tactically, there are plenty of mums and dads willing to lock in safety at a cheap price.

If you face a variable rate 50 to 70 bps above 1‑to‑3 year fixed rates, what would you do? And you’ve just been told the RBNZ is done cutting and next move may be a hike. Even if the RBNZ cuts once more, the banks didn’t lower the variable rate following November’s cut.

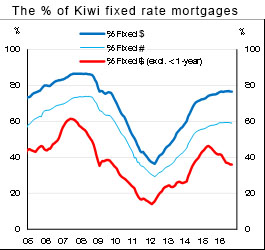

Bank funding costs continue to rise. Fixed rates offered are priced off the swap curve. The swap curve is higher, and only the 3 and 5 year rates have lifted (to a lesser extent). No matter how you slice or dice it, paying fixed rates versus floating in Kiwi is a compelling argument. But we’re not interested in the argument. We’re interested in how banks hedge the flow. They pay fixed.

Jarrod Kerr is the director of interest rate strategy at the Commonwealth Bank of Australia, based in Sydney. This piece is an extract from this daily publication. It is here with permission.

6 Comments

If a recession is on the way where do you see interest rates getting up to?

Not a recession , but as serious adjustment when rates do go up . The fact is rates will have to increase very slowly and in smalll bites to avoid recession or shocks to the system

I'm sure there's some useful information in here but too much jargon for me. Can anyone translate? Does OIS = interest rate swaps?

Overnight Indexed Swap

(PS: This strategy is all 'simple' banker stuff - "lend" long and "borrow" short. Once it looks like the interst rates scheme is heading up, it all gets a bit tougher for bankers. "Any fool can make money in a falling interest rates environment" is what we used to say. Doing the reverse is the hard bit!)

How many remember when the media widely used the terms "soft landing" or "hard landing" when describing how the Reserve Bank would try to protect us from an economic downturn ?

Everyone is flying high on the low interest rate opiate , but when the fuel runs low , land they must .

Hold your seats everyone its going to be hard

I think what many forget when they state comments like rates will have to move slowly or many will get hurt and threaten a recession, is that througout history, that's exactly what has happened - something happened (e.g elevated inflation or too high debt) where rates have been taken higher to do exactly that, hurt people and stop a particular behaviour - the skill/discipline is in not being too being too exposured and thus being one of those.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.