Here's our summary of key economic events overnight that affect New Zealand with news the Omicron surge in Australia is decapitating their workforce. It is about to do the same in China.

But first, US jobless claims rose last week and by more than was expected seasonally. There are now more than 2 mln people on these benefits - although on a seasonal and population adjusted basis this is the lowest level in almost 50 years (1973). And below pre-pandemic levels.

US producer prices didn't rise in December quite as much as feared, and the big +9.7% year-on-year was lower than the November level. Both results suggest that there is some topping out in the wholesale price pressure.

Meanwhile, a top Fed official confirmed they are fully engaged in fighting the inflation threat, confirming they have abandoned the 'transitory' view. And that may mean three rather than two rate hikes in 2022, with the first in March when their bond buying will probably end. One Fed member sees four increases in 2022.

China's foreign direct investment inflows are starting to slip, according to the December data released late yesterday. This metric is up +14.9% on a year-to-date basis, but that is the slowest rise in four months and indicates the December-alone rise is soft. Having said that, the December rise caps a very good year of inflows exceeding +NZ$250 bln, although this is now being driven by inflows from Belt & Road partners.

Meanwhile, Omicron is spreading in China and another port city is now in lockdown. The global impacts on supply-chains won't be helped by this as congestion is growing at the world's biggest port as shippers try to re-route goods. The threat to global trade from this is actually enormous.

And it is not just Chinese ports that are getting more snarled. The giant US West Coast ports, especially in Los Angeles are still struggling to clear long-embedded backlogs.

Outbound freight rates for containerised cargoes from China are rising again, which is not a good sign. Freight rates for bulk cargoes however are falling again, now down to year-ago levels.

Japan's machine tool orders stayed high in December, up +40% from year ago levels to just under ¥140 bln (NZ$1.8 bln) in the month. This is an historically high level even if it is slightly lower than for the prior two months and is +16% higher than for December 2019. This data is important because it confirm that global manufacturers are investing heavily in productivity again.

Back in 2006, the World Economic Forum produced a Global Risk Report that warned of a global pandemic threatening jobs and disrupted global trade along with social unrest leading to political polarisation and global tensions. They also said climate action was urgent. Guess what happened since. The 2022 WEF Global Risk Report now says extreme weather and climate action failure are the biggest evolving risks. The biggest existential threat over the next decade is the impact of weapons of mass destruction. And the collapse of multilateralism will make responding to these much worse. We ignored the 2006 report; what's the chance alt-reality Trumpification can be rolled back now?

In the meantime, we can note that the copper price has risen above US$10,000 per tonne again, tin is now above US$40,000/tonne for the first time ever, and nickel is back over US$22,000 and a decade high. Lithium carbonate is now over US$48,000 and rising fast. The leap in non-ferrous metal prices is a long-term signal that price pressures will remain tough to mitigate

In a similar vein, we should note that the local price of carbon (NZUs) has jumped to NZ$71/tonne in the past few days. (That compares with the EU's carbon permit price at NZ$133/tonne and flatlining in 2022.) The higher the NZ carbon price, the faster farms will be sold to foreigners to plant out in monoculture pines so they can claim the carbon tax benefit off NZ taxpayers. (And interestingly, it isn't dairy farms that are being converted because high dairy prices make it more economic not to sell them into carbon-credit farms.)

More than 10% of the Australian workforce may be off the job due to Omicron isolations now the Australian Treasury is estimating and that is having a serious impact on basic services, including supplying supermarket shelves. Some say their entire food chain is "out of whack".

In NSW, there were 30,541 new community cases reported yesterday, and a hope that they are topping out, now with 337,818 active locally-acquired cases (and undoubtedly an undercount), and 22 more deaths. Hospitals face serious staff shortages, and they have been told the number of COVID-positive people needing inpatient care could exceed 4500 within the month. They are now up to 2,383 having doubled in a week. Half of all NSW ICU patients are unvaccinated. 20,326 pandemic cases in Victoria were reported yesterday, also similar to the day before. There are now 221,726 active cases in that state - and there were a record 25 deaths. Queensland is reporting 14,914 new cases (lower) and 6 new deaths. In South Australia, new cases have held at 3669 yesterday with 7 more deaths. The ACT has 1020 new cases and Tasmania 1100 new cases. Overall in Australia, 150,702 new cases were reported yesterday. Omicron is hitting Australia the hardest of any country worldwide.

The UST 10yr yield opens today at 1.72% and unchanged. The UST 2-10 rate curve starts today unchanged at +82 bps. Their 1-5 curve is slightly flatter at +103 bps, while their 3m-10 year curve is little-changed at +169 bps. The Australian Govt ten year benchmark rate is up +1 bp at 1.83%. The China Govt ten year bond is unchanged at 2.81%. The New Zealand Govt ten year is down -1 bp at 2.49%.

Wall Street opened today firmer but has since lost those gains with the S&P500 now flat in afternoon trade. Overnight, European markets were mixed in a +0.2% to -0.5% range. Yesterday, Tokyo fell back a full -1.0% after the prior day's large rise, Hong Kong held theirs, up +0.1% while Shanghai fell -1.2%. The ASX200 ended up another +0.5% and the NZX50 ended up +0.2%.

The price of gold starts today at US$1819/oz and down -US$6 since this time yesterday.

And oil prices start today back firmer, up +US$1.50 to just on US$82/bbl in the US, while the international Brent price is now just over US$84.50/bbl.

The Kiwi dollar opens today firmer again at 68.8 USc and a further +¼c rise. Against the Australian dollar we are firmer at 94.3 AUc. Against the euro we are firm at 60 euro cents. That means our TWI-5 starts the today up at 72.8.

The bitcoin price has essentially moved sideways since this time yesterday, down a bit less than -1% to US$43,179. Volatility over the past 24 hours has been modest at +/- 1.8%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

148 Comments

Re Supply Chain & workforce constraints: it’s like the entire world has a restraining order on it.

And finance continues with its restraining order:

https://www.nzherald.co.nz/nz/dunedin-woman-says-urgent-extension-to-mo…

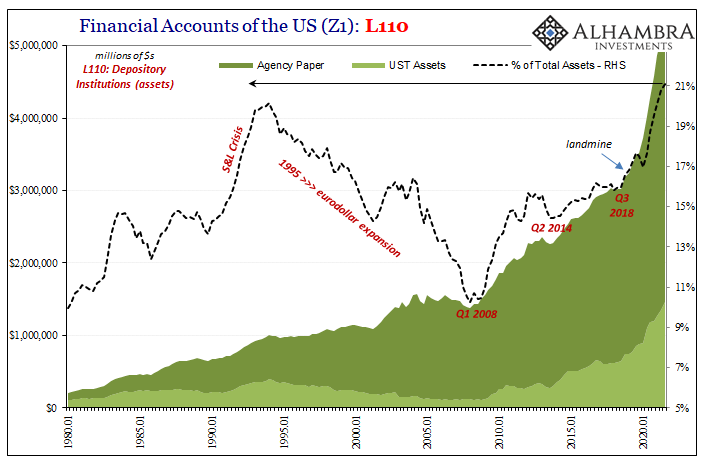

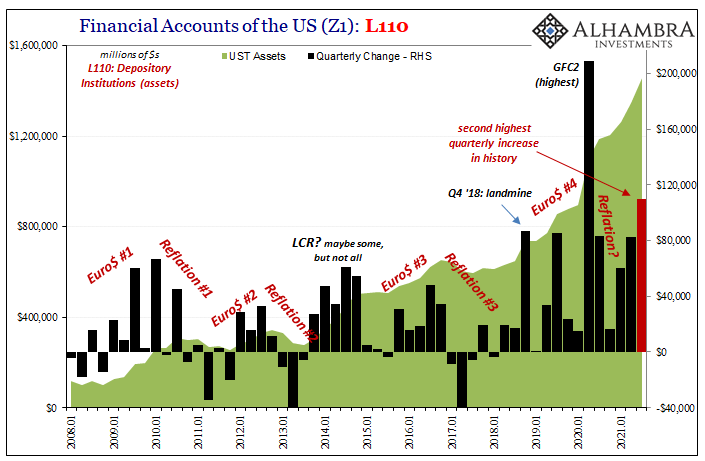

There’s (still) A Ghost On The Monetary Throne

Buying only safe and liquid as the banking system has done the past few years (as the decade before them), and without any change in derivatives offered, in fact fewer since Euro$ #4 in 2019, there was never any money for inflation in 2021 or beyond. The balance sheet constraints, the real if fictional currency behind the ledger, are as imposing and irreducible as ever; if not more so.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

This isn’t strictly about the profit potential and risk characteristics of individual positions, nor portfolios of positions. Banks work as any real economy business does on a budget; only theirs isn’t just about payrolls costs and operating expenses. Their entire output – this ledger of money/credit – is likewise governed by a budget predicated largely on computed risks.

How much in assets can a bank stuff onto its balance sheet? Theoretically, the amount is unlimited, infinite. In the ledger system, there’s no need for real physical money like bullion or vault cash since convertibility isn’t actually an issue for fictional currency and ghost money. Therefore, total systemic “money” supply for the entire global reserve (fictional) currency system is what’s added up from all the balance sheets on the shared ledger.

However, for every asset you do add to the asset side of the balance sheet (setting aside the liability side) you incur risk. Thus, the effective limit to balance sheet space is the likelihood of future losses wiping out the accounting fiction of capital reserves or ST borrowing capacity (if we’re being more realistic, that’s the endpoint real constraint); when booked losses are greater than a bank’s retained equity or repo viability, really long before then, it’s game over.

Any chance of deciphering this article/quote for the layman, Audaxes?!

No - it's as simple as it gets

I get it, Ok ,I am a gardener by trade , keeping all those central city residential grounds ,looking fine and dandy,to help support the extreme valuations but ,simple as I am ,and un-propertied,yeah ,I get it. And yes ,I feel the manufactured inequality ,from trading bank and reserve bank action ,very directly. I get it. For everyone of you ,that have gained more in effortless capital gain ,in the last two years ,for which similar sum ,I could not save in 50 years of sweat and toil, I get it. Very directly.

yeah , its a great feeling doin work for people getting all those tax free gains. Then they screw you down , as the ones with the most money always do .

So right Sloarb, in fact i was gardener( until this election ,)to a certain recent central city LABOUR LIST MP , and when i said that labour were just SHILLS, firstly She said she didn't know what a shill was ,and i told her to get up to speed as she would soon be in the job in parliament, and secondly ,i got dumped ,no more work for me, from the Chardonnay socialist , Speak truth to power? Cost me directly.... but anyway, shills they are ,and they do not give a fck,really.True story ,but really they are clueless on both sides.

Let me see if I understand this correctly. You insulted someone you were doing a job for, they fired you, and you're surprised?

Kjeldorian ,i fire every d!ckhead,i encounter, maybe your sort wouldnt even get a returned call,who knows? It is what i would call a constructive dismissal of a dckhead client in fact ,and i call out hypocrisy wherever i find it. Being overwhelmed with work orders ,without advertising, in fact 200% over-subscribed now ,and most main clients with me for over 10 years, i find the ignorant shallow quip..just that ignorant.

So oversubscribed with work that you spend your days commenting on interest.co.nz

Do I?.. just dropped in to shed some light.

Ah I see, you insult everyone not just your customers.

I nhave a business theory that has stood me in good stead over many years, and which I have tried to instill in all my staff members. Not always successfully. " Be nice to people that give you money."

And then they expect to take young people's wages as their pension benefit too, the only universal non-means-tested benefit of the lot.

I remember a time when a Labour Govt would have supported you. Now all Govts support the bankers and asset classes.

Rastus fully agree ,see my comments above. New added.

Lol. I wouldn't call digging weeds and mowing lawns "a trade".

Clearly very ignorant on at least two obvious counts. Firstly ,mowing is not even 5 % of what we do ,and " digging weeds" wtf? Who digs weeds ,you do not even know the basics , mate.

Secondly you do forget that the source of your greens and fruits is entirely ,either home grown or commercially grown , by "Gardeners' of various sorts. Just try going without that for a year or two im protest, It would please me.

Okay okay settle down there Green Thumb, or is it Tom Thumb?

I did not find it simple.! For me , the quote/article feels a little confusing.

Simple as it gets.... might have been to just say that a Banks ability to expand its balance sheet is actually constrained.

It is constrained in the same way that any business that uses "leverage" is constrained.

eg. If u have Capital of $10 and assets of $200, you are in a far more vulnerable position to me if I have $100 in Capital and $200 in assets.

( A 5% fall is asset values wipes out your Capital... and makes you , almost, insolvent )

To be more "prudent", is to use less leverage, ... which is what the RBNZ is wanting for our Banks., in regards to Capital ratios.... "Prudential Policy "

explaining in your own words requires brainpower, something bots don't posses.

It's not rocket science.

You've changed name from a few years ago, what was it before stephen? But i still think posting random unrelated alhambrapartners blog post in reply at the start of every day is a bot trying to generate clicks

Do please explain what that article https://alhambrapartners.com/2022/01/12/theres-still-a-ghost-on-the-mon… has to do with a couple getting a mortgage extension declined due to the CCCFA changes?

My difficulty with the extracts from these articles is that they seem to be written in a way that only people who already understand can understand - things are not spelt out for the rest of us to catch up, and there is no attention to grammar.

For example, the first sentence has no object for the verb "buying."

"Buying only safe and liquid..."

So what are they buying (that is only safe and liquid?

{kind=link}

{kind=link}

"This raises the risk of an economy-wide downturn if it creates a positive-feedback loop in defaults through the process known as a deflationary spiral. In this case, because the liquidation of defaulting business and consumer debts involves lenders writing down loans and wiping the corresponding liabilities (bank deposits) off their books, the total volume of credit in the economy contracts. This contraction in the volume of credit in the economy then feeds back into more downward pressure on prices and wages, which puts more borrowers in distress, renewing the cycle."

you can always just look at the pictures

Of course, most of the powers that be are on holiday while many of us either worked through or went back to work a week ago. So no one around to comment or face some degree of scrutiny for what is an absurd situation, where aspiring first home owners are forced to continue renting and fall further behind and stretch even further to get a deposit together. And this protects them how?

If you make credit so hard to get that people have to keep switching jobs to chase higher pay packets and totally wind back on spending, that's going to create instability, not prevent it.

What's the difference between " credit so hard to get" and replacing that with "prices so high"?

Other than they will need to pay more in both price and interest?

Because making credit hard to get means people aren't more likely to get approvals they're not getting, even if it is for a lesser amount. When prices drop, you'll have fewer owner-occupiers buying and people with equity to leverage/sell down in their additional properties in the box seat. You're basically handing the market back to the people who got us into this mess.

So continuing the ponzi with ever more credit is the only way?

Think again.

We have just had the loosest credit cycle of all times....how good was that for the asset less class?

"Think again" Yea I'm sure that's comforting to those paying more in rent than their planned mortgages would cost for a house they would actually own. In the absence of a long-term plan to make houses more affordable, it's just telling young Kiwis that NZ isn't a place for people without family money to fall back on.

There's no long-term future for young people in NZ if aspiring FHBs are the ones told to live with a problem they had no part in causing, and I can assure you we'll go back to 50,000p.a. migration as soon as Omicron washes over us. So those people just stay frozen out forever? That's not a viable long-term solution.

It is a myth these types of changes hurt FHBs disproportionately. FHBs need to save massive deposits - $200k+ - if you’ve saved that your expenses will look pretty tight relative to owner occupiers who have just been doing min repayments.

Also mortgage debt is an arms race. If you lower the standards to get debt it changes nothing about who gets the house. All that happens is the person who does win it takes on more debt and pays a higher price.

Tighter lending standards help FHBs by cooling the debt arms race and lowering the prices paid. Now an individual FHB may feel prevented and that they would have won if only they got more debt approved but they need to remember the person they were competing against might have also paid more if only they could get more debt approved.

Debt is not your friend. Nobody is helping you but letting you dig a deeper financial hole.

The market is not just made up of owner-occupiers - there's people out there with huge equity to leverage across multiple properties that have rocketed up in value in the last 18 months.

Mortgage debt might be an arms race, but in the absence of any actual, clear path to increased supply (unlikely given land costs, construction materials issues and a likely return to high migration post-Covid), all you're doing is ring-fencing one group of buyers and excluding them from the market, with no credible pathway for them to actually realise home ownership at any point - all the while those aspiring FHBs have to keep paying rents to someone else, in a market structured so that prices can only go up and their deposit requirements grow faster than they can save.

Your point would have more merit if there was any proof that restricting FHB credit did anything for price action, instead of just making it harder for them to buy in isolation. Politically, economically, the whole country is set up to grow house prices, not make them more affordable. Are FHBs expected to just sit there and wait for a 30 year trend to suddenly reverse while the party continues for everyone else?

Well the hypothesis will be provided in the next six months one way or the other won’t it?

We'll see. Migration announcement (or lack thereof) is incredibly telling in the short term.

I get your frustration. Your solution (i.e looses n credit) is not the answer. Its tightening credit and removing the policies that promote the ownership of more than one home.

And to this govts credit, they have moved in this direction - non ded of interest, ring fencing losses, bright line, tenant rights, standards etc. Given time (and I suspect we are entering this stage now) these will encourage the land lording classes to invest elsewhere.

(if you purchased in the last year or so you will be in the hole already - real estate commissions making sure of that the day your signed up).

I think you touched on the real reason there rastus...where else would property investors put their money?

Agreed. Where to seek a return is a challenge. The lazy answer is housing and to date it has worked.

A tipping point will be reached when these 'houses' will cost more to own than they return - cap gains included.

Or do we think this will go on for ever?

Yes, good point redcows, which is worse for FHBs ? Escalating prices or lack of available finance?

Which one actually lets them become home owners at some point?

The only way out of this, as I have said many times, is to take it out of the private market debacle, and get out of the speculative circus.

With the government building both social housing and affordable housing FHBs en masse.

Unfortunately, we have a government and bureaucracy both unwilling to do this, wedded as they are to neoliberalism and reliance on 'the market', and also being incapable of executing it even if they did commit to it.

For example, what ever happened to the large scale housing development at Unitec that they announced 3 or 4 years ago????

The other way out of this mess is by a 777-300ER. Why waste our lives paying twice as much for a rot box than we would have paid two years ago when mortgage rates are the same, wages are the same, costs have gone up and work prospects are riskier? Why would we stay here?

Definitely. NZ is a financial basket case for most young kiwis, and many should seriously consider emigrating.

The only reason I returned from Aus some 7 years ago was because of my mum's failing health. My brother has been in Europe since 1998, and he couldn't get back as readily as me.

The more the Govt. place restrictions on true free market ability for supply to meet demand at the rate of demand, the more unaffordable it has become.

That is what the theory tells us will happen and what the evidence is showing.

This is leading to an increase in supply and an increase in prices.

The only way prices can decrease under this system is a market crash.

Best for FHBs would be house prices half what they are now. I would happy to see that and I am a property owner.

The recent house price explosion in New Zealand's greatest social disaster.

The ramifications of that would be immense, not "great depression" more like "greatest depression"

The majority of property investors, speculators, and even owners don't accept that there is any risk in owning houses. Now that some serious risks are developing these groups are looking at every possible way to avoid losses, including to government and the RBNZ. "Property prices only go up", "when was the last time we had a serious drop in property prices". The amount of times I have heard these comments over BBQs, at work, on the TV and Radio!

As Dalio and Grantham have been harping on about, we are in for a real surprise. There will be a lot of pain and it's likely all assets will take a hit.

Yes, I agree.

Wishing for a house price drop of 50% is wishing pain on everyone. Pretty sadistic really.

Prices have gone up 30% in a year. As an investor you have to expect recent gains can be suddenly removed.

And building materials have gone up the same amount if not more, and wages have gone up too.

If house prices halve then building a house loses money.

They're too used to being coddled by tax-exemption, subsidies, and protection in hard times.

Then they rock out the crocodile tears for FHB on this credit issue.

The greatest depression would be expected since we have also had the greatest boom in prices.

Tit for tat.

That NZ Herald story doesn't sound like the full picture and no doubt this couple has alot higher expenditure or external debt...

It's like hearing that's someone was declined a loan because they bought coffee twice a week.... Bullsh*t.

No doubt we'll see more of this putting pressure on CCCFA changes...

Government is supposedly to relook at the legislation:

https://www.odt.co.nz/business/fears-impact-new-housing-rules?fbclid=Iw…

“When contacted, a spokeswoman for duty minister Stuart Nash said officials were aware of concerns and were assessing the impact of the new requirements.

"Officials from MBIE will be engaging further with lenders and consumer advocates once the new law has had a chance to bed in."”

Yeah I can see it happening soon, the first piece of legislation that might really impact the property market and they'll back track on it...

#transformational Jacinda & co

It's another piece of poorly thought through and rushed legislation with unintended consequences. This mob are becoming masters of this.

#worstgovernmentinlivingmemory

Its not meant to impact the property market, its meant to stop lenders taking advantage of vulnerable people. Instead it is stopping normal people from getting credit they can afford. In my opinion people should have a right to negotiate with their bank without government interference.

More scrutiny of a DINKY's takeaway spending than the actual money printing and asset-purchase program that blew prices out of the water last year, which from memory the RBNZ was still trying to understand the effects of after they'd started it.

I think its been pretty well proven that if you leave banks to their own devices, it becomes a taxpayer issue in the washup.

I'm happy for the RBNZ to ensure that banks are stable. But Joe Bloggs that has 50% equity in their house is never a bank stability issue regardless of how much they spend at K-Mart and coffee shops each week.

They are trying to protect Joe Bloggs from losing his house, but what if he doesn't want to be protected and is an adult that can assess his own risk?

JimboJones - how do you know these people can afford the lending? Now their expenses are really being looked into the banks systems suggest they can't.

This just seems like a good exercise for people to know what they're spending their money on... and perhaps - if they can't get a top-up start saving for what they need...like the good old days?

Which good old days are those? When you could a house that cost 5x one single-earning income per household? When you could actually pay rent AND save money? Gosh, could there possibly be a reason that might not be relevant or viable in a market where prices increased by 30% in one year?

That depends on whether you think the government / banks should be deciding that for you based on some formulas. What if you know for example that your current expenses are high and that you will decrease them accordingly with the new debt? What if you know that next year your partner will get a job after being a stay at home mum? Or what if you want to invest in a productive business knowing that the worst case is you lose your house but you are prepared to take that risk?

Why stop at debt? Should the government be involved in every financial decision you make? Should they be checking you can afford everything you ever buy?

A lender should be required to have regard for the well-being of the person being lent to and not just their own financial interests. Otherwise you get scenarios where banks are making loans they know people can’t pay back with the knowledge they will liquidate the asset to get payment. That sounds predatory to me.

JimboJones you sound entitled...to debt.

No I'm good, I don't think I need any more debt these days. But there have been a few times in the past where the bank was a bit skeptical about lending us money as we were temporarily a single income family with a stay at home mum (even though we had very high equity and are of no risk to the bank). Under these new rules they would have almost certainly said no. In that case we would be in a much worse situation than we are now. So you can say it is for people's own good, but I would say in the majority of cases it makes sensible people worse off.

Define well-being? Missing out on buying a house, starting a business, falling through your broken deck, is that well-being?

Sure if people can't possibly afford the repayments then fine, the banks were already checking that anyway. But going through every expense with a fine tooth comb is crazy stuff. And either way at the end of the day it should be "hey we really don't think you can afford this, you may lose your house, are you really sure you want to" rather than "no", because adults should be allowed to make such decisions for themselves.

Look I agree about the fine tooth comb bit. This is why we need more information about what the banks are actually doing. Because all we are getting is the mortgage broker industry spin laundered through the media.

I don’t think the expenditure type should matter. It’s not the banks business if it’s a coffee or takeaways or whatever. But they should be looking at your income and expenses in aggregate to see if there is enough left over to pay them.

And what if the applicant tells the bank they will reduce their spending but then find it too hard to do so?

And what if the applicant says the wife will get a new high paying job but then she finds she can't get that job?

The media will be piling on with stories about the poor couple and how the vulture banks were taking advantage of them, lending to them when the knew they couldn't repay and how imorral the whole situation is.

It would be helpful if the two newspapers that are printing stories for the mortgage brokers and their interest group actually investigate what is going on. At the moment we have selectively releases personal information. I can see the benefit for the interest groups in publishing, I’m less sure about the newsworthiness.

A couple of the stories today are just <20% equity - well that makes sense as banks are trying to pull that back.

In the renovation example, if I was a lender I’d be wondering why they needed an addition to the mortgage and couldn’t save the money.

The shock here for people is the new law seems to force banks to consider whether people can actually repay the debt thereby covering their personal risk (and not just the banks risk). This is a good thing, we just need to adjust to the new normal.

I’d be interested in learning more about how banks are actually doing this - which isn’t covered in detail in any of these stories.

This paragraph from RNZ is interesting:

’Everything that was deemed regular outgoings had to be put through the debt calculator now. He had one client's regular car parking spend pulled up.’

A lot of the stories make it seem like the bank is critiquing the expenditure - e.g. you shouldn’t be buying coffee or takeaways.

But I read this as saying previously the bank might have looked at core expenses and discretionary expenses and only factored core. That meant there was some optimism that if needed people could pair back discretionary.

Am I right that what is occurring now is if you regularly spend it they are assuming it is locked in and not available for servicing - ie no assumption you will cut back under stress?

That doesn’t seem like the worst assumption to me. It people want to prove to the bank they can live on less they do three months on that budget and then come back.

A lot of assumptions in the above. I’d be interested in reading what banks are actually doing and not these half stories.

Why should you have to prove anything? If you think you can afford it and the bank thinks you are of little risk to them, where is the issue? The real problem was loan sharks charging financially illiterate people 20+% interest rates, why try and fix other problems that don't exist. Very poor legislation...

See my higher up comment to you.

I do think banks need to assure themselves you can pay the loan under a range of scenarios and looking at incomings and outgoings is an appropriate way of doing this.

One of the issues is the debt that is being taken on has got so big that the stakes are a lot higher.

I don’t think the principle of what is occurring is wrong. It’s possible the banks are being overly conservative due to a lack of clarity about their obligations. But we need a lot more information than is in the media to reach that conclusion.

It’s also true that sometimes banks are secretly or publicly pro this type of change because there is a prisoners dilemma between banks and the only way to solve it is regulation by government. We haven’t heard them complaining which suggests they are happy and may even been accentuating what we see as they drive down their risk and blame the new regulations.

It would be interesting to hear directly from the main banks as to whether they are happy with the CCCFA as it stands. Maybe as Hardly suggests - they are comfortable with a few months of tightening and lessening their portfolio risk.

Why should you have to prove anything?

Why should they have to lend to you if your income and spending don't look great when looked at carefully?

It's lending, not an entitlement.

Agreed. The trivialities being highlighted in the media for mortgages being declined do not tell the whole story. Petty stuff There is much more to it than what the media feeds us. Banks know the actual situation as they process lending with greater diligence, which they should have done in the first place. Its precisely that this has not been done that govt saw it necessary to bring in CCCFA.

Well the Omicron impact, has a fair percentage of mention in all of that. Years ago I endured watching Charlton Heston in the painfully bad “The Omega Man” (only for a similar reprise in the even worse “Cassandra Crossing.” ) Just as well the Greeks had a reasonably sized alphabet to work through before it gets to that then. NZ has had in political speak, the year of covid, the year of vaccine (well half of it) and now dawns the year of Omicron, like it or lump it.

And the arms race is on. Seems humans are hell bent on self distruction. Madness.

..time to re open the Ohu at the Ahu.

Not so sure of that rastus, didn't appear to work out so well last time. Same social issues as elsewhere. Nice thought though.

A year? You'll be lucky to get a quarter out of Omicron at the rate this is moving through the human population. The UK and SA already seem to have peaked just 6(ish) weeks after the first cases.

Understood, but they haven’t got a government like ours, ie a hermit nation suits their control freakishness and agenda admirably.

I don't know how they managed to make 3 films based on Richard Mathesons amazing book "I am legend" and all the films are awful.

The soil moisture map is getting interesting, particularly with Fonterra already have dropped their forecast production. Ex cyclone coming to the rescue Sunday/Monday I hope. Wind the last two days has really dried us out.

Latest forecast is a big event in the eastern midlands of the NI and not much happening from Auckland northwards, where it's also badly needed.

Yep the hills out west are drying out as well now. The problem is if we get a dump of rain the slips start again. I bet hill farmers out east are getting nervous.

Yes been going on for a couple weeks here. Even lost some young trees before I noticed they were distressed.

Not long before the farmers ask for drought relief then...groundswell?

Very dry where we are (Hawkes Bay, on the flat), haven't had a drop since the big dump in early December that wiped out about 20-30% of our crop before it had a chance to germinate. Grazing paddocks are looking thin and struggling to grow. Looks like something coming Sunday/Monday according to MetService but many times we've watched rain go right around us, along the ranges, or just never turn up.

At least it's been under 30 the past couple of days.

Latest modelling shows quite a bit of rain down the East Coast (hopefully not a deluge), but SFA for the western side and north of Auckland.

How are lake levels? We had a close call last year where they had to start cutting load.

The big South Island lakes are somewhat full. Tekapo has been spilling water for six weeks or more. Pukaki also looks full.

"We ignored the 2006 report; what's the chance alt-reality Trumpification can be rolled back now?"

Well, given that the piece avoids (misses?) the bigger picture - CC being merely a symptom of the greater malaise - I'd say none. Because Trump is also a symptom, not a cause. As was the rise of Hitler; both wouldn't have happened if real scarcity per-head wasn't driving the desperate to look for saviours.

The bigger ignorance was by the mainstream media - and it doggedly continues. Myopic concentration on 'supply chain issues', Climate Change, a virus. But dogged avoidance of the existential bigger picture. A remarkable effort.

https://www.monbiot.com/2022/01/10/losing-it/

"And the sector whose failures are most brutally exposed is the media."

Trumpism versus the unholy alliance of Big Tech/Media/Pharma/Govt/UN? That’s a big ask.

That isn’t an alliance. It’s more a convergence of logic and rational thought.

Of course - and we can hear from them via the “one source of truth” podiums.

Wow!

"A plague on both your houses".

Sad comment.

https://www.rnz.co.nz/news/business/459484/banks-undertaking-forensic-a…

Is this the way RBNZ is acting on housing ponzi by hitting the tail end and allowing elephants, only as has no real intent.

Don't worry about the price of those commodities - the mighty RBNZ will crank up interest rates, get unemployment back up to a "sustainable level", house price growth back to normal levels of bonkers, and price increases will be no more.

The soaring carbon price will mean less overseas earnings from meat exports and more overseas payments for carbon credits to foreigners buying up farmland to convert to forest. This is the last thing NZ needs. The country is already spending more than it earns so this just accelerates us toward a lower standard of living.

The carbon sequestered by trees is released back into the atmosphere when it eventually rots away, the only long term answer to prevent rising atmospheric carbon is to stop pulling it out of the ground.

If we don't grow our own carbon credits , we have to buy them overseas.

That's true, but the carbon credits belong to the land owner, and locally owned drystock farms are being bought by foreign owners for carbon farming. See Keith Woodfords excellent article about it a couple of weeks back.

The reason the landowner is receiving carbon credits is because they are reducing NZ's financial obligations under the Paris Agreement. Most landowners involved are NZ nationals; it is very difficult for foreigners to get OIO approval. There is less plantation forestry today than 20 years ago because of dairy land conversion. Carbon forestry only makes sense on economically marginal and highly erodible steep country.

OIO approval is very easy as long as it is said to be for timber with carbon as the add-on.

Carbon farming economics are now sufficiently attractive that it is worth a look on a lot more than just 'marginal and highly erodible steep country'. Those who are interested in forests for harvest purposes are not particularly interested in the erodible hill country - they prefer easier country where costs are much lower.

KeithW

Sounds like the OIO is not doing its job properly.

We could lower the carbon price by building more renewable energy. For example, Genesis could build that nice juicy wind farm consent they are sitting on.

I’d also like to see more collaboration between fonterra and the govt to shift to electric boilers. Even if the govt pays for the retrofit and even if they need a deal like Rio Tinto on the power, it would still be worth it.

Wind farms don't help with the peaks which is where the real carbon is emitted. Wind farms are "must run" assets, which means they bid into the market at $0 /MWh, and usually see their best generation off-peak, like in the middle of the night. I doubt building them will have much effect on the carbon price.

Well you could pair them with batteries (which is what they do in Australia) or you could use them to conserve water in the dams.

I’m not meteorologist but doesn’t the wind blow more during the day? Yes, google is telling me there is more wind during the day.

You're right- according to NIWA the wind picks up at around 9am and peaks at 3pm, dropping off from there until 8pm. That doesn't change my main point - the peak wind generation doesn't cover the peak load times, which is where carbon will be required.

I'm sure if it is worth it Genesis will do something. At the moment it is worth their while to run coal at Huntly.

If you follow their NZX releases, Genesis are scrambling to build their renewable portfolio. Their thermal baseload should be phased out by 2030 as renewables are simply cheaper than coal, even at today's carbon prices.

They are developing wind farms, solar, and are contracting geothermal generation from Contact.

What are the building right now as part of this scramble?

They didn't build it, but they have contracted to buy all the power generated by Waipipi windfarm built by Tilt (now part of Mercury). I believe it's mostly (entirely?) built now and is currently testing and powering up. Similar deal for Kaiwaikawe wind farm which should start construction soon.

Contact have started building Tauhara Geothermal plant - started a year ago, operational mid 2023.

Their solar farms are expected to come online from 2023 - I don't know the details.

They released an investor presentation in November last year showing how they will replace their thermal baseload - most of it will be gone by 2025. Backup thermal still persists beyond 2030 and is still needed for dry year backup if nothing else.

Others are also acting - I believe Meridian are expecting to build a new wind farm every year for the next 5-10 years. All in their NZX releases.

That's not a dumb move. Geothermal has the most consistent generation of all the generation types. I'm still worried about predictable baseload generation in a dry year. #nuclear

As below, this is what the NZ battery project is looking at. Lake Onslow seems to be the main contender, with Meridian and Contact pushing some kind of variable-load Hydrogen plant in Southland which could be turned down/off in dry years.

As I understand it, current Nuclear plants don't fit well in NZ due to the requirements for backup power in case of a fault (there is always generation on standby sufficient to replace the largest currently active generator in case if fails - or the inter-island link if that faults). Even small nuclear plants would be difficult to cover. I'm talking beyond my expertise here though - could be wrong, and perhaps there are smaller nuclear options now.

There are lots of small, even containerised nuclear plants in development by various countries. One of these would replace Huntly.

One Fukushima would cover half of New Zealand's currently installed generation capacity, or 90% of our daily demand, or 4xHuntly's generation (including the decommissioned turbine). A small reactor would meet those requirements. Or, 7 of the small molten salt reactors China is planning would replace Huntly, with less toxic waste and more safety than old tech nuclear like Fukushima.

Absolutely - and once they are developed and proven they could be a great option for NZ, something around the 400MW scale, perhaps even 2-3.

One plant providing half of our generation is a risk management disaster. You need that amount of capacity again to provide backup for unexpected outages, suitably distributed across the two islands in case the cable faults. Very inefficient. Otherwise you just accept island-scale blackouts every now and then, potentially lasting as long as it takes to fix the fault.

Yes, it's typically still conditions from midnight to around 9am, and the wind comes up during the day and evening.

The thing about renewable energy is it is a capital problem - you can solve it if you have enough capital.

The government has plenty of capital. We are talking about spending $14B on light rail for one line in one city.

Imagine how much renewable energy you could generate for $14B in investment. And you wouldn’t even be spending $14B because you would get a return on that capital.

People are worried about peak/off peak - great, let’s take $2B and ask Elon Musk how many batteries we get for that amount. I’m guessing it is a lot.

And then in ten years we have to spend that again to replace the batteries. Batteries are an operating cost not a capital cost.

We should start hearing from the NZ Battery Project this year - if they recommend developing Lake Onslow for pumped storage it could help with the peak demand issue as well as dry year storage.

https://www.mbie.govt.nz/building-and-energy/energy-and-natural-resourc…

Is there a law that meat farms must have local owners and forests must have foreign owners?

No, but overseas investors prefer carbon farming over livestock. This paragraph from Keith Woodfords article on 5th Jan:

"There have also been significant capital inflows by overseas forestry investors. These investors will now earn profits from carbon farming which will be transferred back overseas. So, not only will we earn no future overseas exchange from these investments, at least until or if these forests are harvested in 30 years time, but there will also be a drain on overseas funds as the carbon-farming profits are remitted."

Exactly The Person, there is plenty of unprofitable land on hill farms. If everyone of them had a bit of forest the carbon money stays in the community, simple really.

Australian covid case numbers above don't add up, I get roughly half of the total in the story when I add the individual states up.

The CCCFA is all about Responsible Lending. And what's wrong with that?? If there are any weaknesses in mortgage-processing, the solution is in improving the systems. Not in kicking out CCCFA. Its no more the Wild West out there with unrestrained lending beyond affordability .We see an outpouring of grief for homebuyers impacted by new lending rules by those whose very livelihood is in arranging mortgage financing!!!! Were they doing some sort of charity work all this while?

What is affordable today may not be affordable tomorrow. You are essentially drawing straight lines into the future on inflation, wages and interest rates etc.

MBIE is sitting back and watching the changes "bed in" before stepping in and providing guidance. That's good at a macro level - get data for better decision making rather than policy making on the fly. On the micro side, we're hearing stories about people who may have been able to buy before but can't now, and by the time the advice from MBIE makes banks act sensibly, house prices could have risen so much that the buyers miss out on home ownership forever.

The micro situation sucks, but the macro situation could end up being a long-term improvement for society. Only time will tell.

Or maybe the tightness on lending (for investors as well as potential FHBs), along with rising interest rates, results in house price drops?

Which surely, ultimately, is a good thing for FHBs.

This times one million.

That would be great. My house could drop 75% and we'd still have nearly 20% equity (and a great place to live). Given I've only been in the market 8 years most people could probably handle that. The rest? Just statistics for the policy makers, and they'd likely switch with the people wanting to buy so all up the country would be better off. Not sure if that's /s or not.

and you can then upgrade for 75% less.

Already have, by moving out of a main centre to the provinces. I intend to be carried out of this one feet first.

Meanwhile, a top Fed official confirmed they are fully engaged in fighting the inflation threat, confirming they have abandoned the 'transitory' view. And that may mean three rather than two rate hikes in 2022, with the first in March when their bond buying will probably end.

The FED are deferring the response for 3 months and retain the option to defer again.

Yes, to maintain the upside risk that inflation dies down after all. I think it will die down, along with growth, and the leaders will go "There, inflation not so bad now - we fix", and another drop in standard of living will be locked in for Everyday Joe.

Anyway, they are only going to raise rates in tiny increments - real rates are way negative and will stay that way.

Australia has worst hit of Omicron because, like China and NZ, it has had insufficient exposure to cv19 overall.

This is a problem induced by over-protection: it makes you more vulnerable to sudden and greater risk because you were not ope to lesser risk over previous time period. Nassim Taleb covered this in his book "Ant-fragile"

But of course the lucky country is lucky because its far milder than delta. NZ will be similarly lucky but because JA is SO risk averse, we will have usual over reaction in Feb and March.

This comment is in a universe where vaccination is not available, and where the US healthcare example cannot be looked at (early, wide-spread exposure, still massive problems now).

However, yes, unfortunately Omicron - helped tremendously by anti-vaxxers - will likely overwhelm the healthcare system. Only x% as deadly, but far more contagious...plenty enough to escalate hospitalisation rates in NSW.

The rate of infection in USA is about 2500/100,000 compared to 4000/100,000 in Australia, even though Australia has much higher levels of vaccination.

But much lower levels of natural immunity from previous COVID exposure.

China probably has had quite high levels of exposure, unfortunately it is governed poorly and so Covid is much more impactful in China.

President Xi officially "defeated" the disease in early 2020 using extremely harsh lock-downs. So now whenever Covid is detected in China the response always goes to extremes to correlate with the original "successful" policy.

The Chinese populace are told the CCP is successfully defeating the virus with high profile measures. In reality the time taken for the harshest Chinese measures to succeed provides no improvement on how the virus behaves in other countries.

I know the pandemic has tested my madness levels and many of my friends too...imagine doing it within China and no end in sight. It can’t make for a happy society. What gives?

I noticed that Chinas producer price inflation was 11-12%. Hope that wave doesn’t hit us?

if I were a bank I’d be a bit concerned about my customers ability to service...in a few years time.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.