Back in the good old days, recessions were simply the unpleasant part of the business cycle. Consumer choices, exuberant businesses, and monetary policy would periodically generate growth contractions. We debated the timing, but recessions didn’t come out of the blue.

Then in 2020, a recession did come out of the blue, or nearly so, when COVID unexpectedly changed behavior. Working from home, avoiding travel, etc., caused a sudden drop in services demand, and thus recession. This wasn’t part of the business cycle.

Now it’s 2022 and another strange recession looms. That’s right, I’m calling it: Recession is here, or will be soon. And unfortunately, it will be a global recession. Like the COVID recession, this one has little to do with the business cycle. It’s a recession of choice - not your choice or mine, but Vladimir Putin’s. He clearly miscalculated how hard capturing Ukraine would be and how the West would react.

Most recessions are preceded by an inverted yield curve, when long bond rates drop below short bond rates. Further, the inversion had to go relatively deep and last for some time to really be reliable as a recession predictor. When I called a recession in 2001 and in 2007, those conditions existed. Like a fever indicates something is wrong in your body, an inverted yield curve tells us there is something wrong in our economic body.

In this case, the economy was already slowing down and at stall speed. We’ll look at some data to demonstrate that. But this war will make it worse and the longer it goes the worse it will get. I don’t see the sanctions ending as long as Putin stays in power. Further, I think Western countries will change who they rely upon for energy in any event.

We always get through recessions and there will be a recovery. It’s not the end of the world, just a readjustment. But regardless, we’re here. And I think we’ll be here for quite some time.

That Seventies Show

This recession is strange for another reason, too. Most recessions are de flationary. Negative growth and rising prices don’t normally occur together. Unemployed people have little choice but to reduce spending, so most businesses lack pricing power.

However, a recession can be inflationary when accompanied by a supply shock in essential goods. Then you get falling growth and rising prices at the same time—an especially miserable combination. We call this stagflation : stagnation + inflation, and it last occurred in the 1970s. And for similar reasons: higher energy prices. In that case they came from the Arab oil embargo. This time it’s a buyer’s embargo as Western countries stop trade with Russia. Since most of that trade is energy-related, energy prices are rising.

But it won’t be just energy prices. Benchmarks like the Consumer Price Index report something called “core inflation.” This is the full index minus the food and energy categories. We laugh at it because actual consumers don’t have the option of omitting food and energy spending. But this figure actually has a point.

Food and energy are the starting point for almost everything else. (Food is a kind of energy; it just powers humans instead of machines.) Louis Gave likes to say all economic activity is simply “energy transformed.” We pull coal, oil, etc., out of the ground, process them, and after several steps we have cars, computers, and all other goods. Without energy it never gets that far.

We expect volatility in food and energy prices. At some point, it seeps into the price of other goods and services. That is a sign of more serious inflation, which is why the Fed watches core PCE. We have a problem beyond just normal volatility if it’s rising.

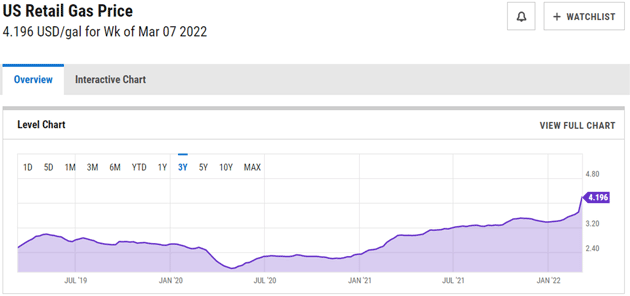

Functionally, higher energy prices are similar to a tax increase. Yes, we can do things to reduce the burden, but it’s hard to escape. We have to keep the lights and heat on, have fuel to drive to work and so on. On a percentage basis, a 1 cent rise in gasoline costs the US economy $1.4 billion. That means we have the equivalent of a $200 billion tax increase hitting the economy this year. That’s not including the food costs and other energy increases that work their way through the market. By the way, the $4.19 gas price this chart shows is a national average. My eight kids in Texas, Oklahoma, Colorado, and Florida tell me they see much higher.

The macro effects of all this take time. At first people just grumble. But eventually, they start changing their behavior. They stop taking the boat out on weekends, don’t drive to the beach as often, look for jobs closer to home. Maybe they try to sell the giant SUV and find it’s not worth as much as they thought. This affects their confidence so they reduce other spending. And because inflation is higher than their wage increases, they feel even more pressure.

Businesses experience similar changes. Those in fuel-intensive segments (airlines, delivery, construction) see their costs rise quickly. At some point they have to raise prices, which makes their customers look for alternatives—or stop buying.

All this continues until something ends the supply/demand imbalance that caused the initial energy shock. That could be new supply, reduced demand, or a combination of both. One thing that makes commodities different from other goods is their fungibility. Oil is oil, wheat is wheat, regardless of origin. (Yes, I know there are different grades and varieties. They matter but we’re talking macro here.)

So if, as happened this week, the US and UK ban imported Russian oil, the global oil supply may not change much. Russia will sell that oil to someone else while the US and UK find other sellers. Everyone typically is still buying and selling the same amounts they were before, just from different counterparties.

But it’s not clear this will go that way. The economic sanctions disrupt the financial mechanisms that permit Russian trade. And even if they didn’t, it may not be possible to deliver the oil to other buyers. Pipeline and shipping capacity have limits. China buys a lot of Russian oil now, but they get it from eastern Russia. The oil produced further north and west? There are no pipelines to get it to China cheaply. It will take years to build the infrastructure to redirect not just Russian oil but grain and everything else.

Another open question is how long Russia can sustain oil and gas production at the current amounts. Much of it is (was) operated by Western companies that have now left, using equipment and technology that sooner or later will need maintenance and spare parts.

Balancing that is the possibility of increased production from elsewhere. OPEC has unused capacity it could bring online fairly soon. US officials are reportedly talking to Iran and Venezuela. Some US shale companies might be able to produce more. All those would help, but we don’t know how much or for how long. Fully replacing Russian energy exports seems unlikely—which means energy prices will stay elevated for some time.

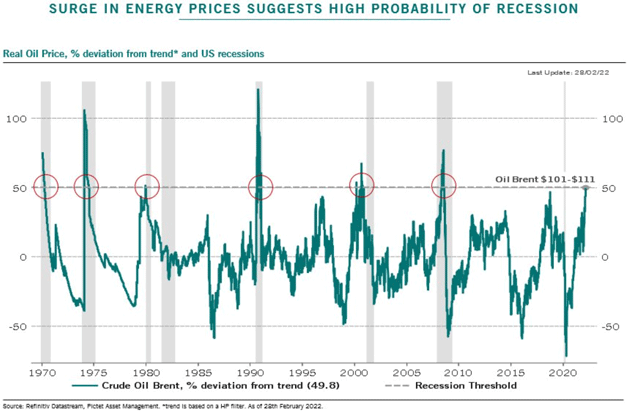

Long story short? Energy spikes preceded almost every recession for the last 80 years. We now have another one.

Toxic brew

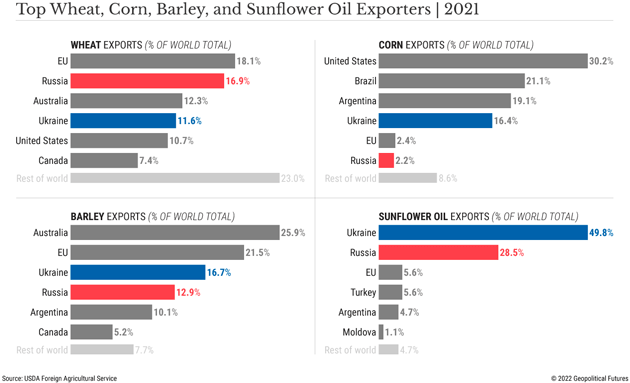

The other aspect of this, not yet getting as much attention as it should, is the very real possibility of global food shortages. Russia and Ukraine are both major grain exporters. Spring planting season will be difficult for farmers in the battle zones. Meanwhile the same economic sanctions that hinder Russian energy exports will have a similar effect on agricultural goods. That’s why wheat futures prices have been hitting their daily limit. This next chart shows you the importance of Ukraine and Russia to important grains and oils.

Last week we sent Over My Shoulder members a fascinating and somewhat terrifying report about Egypt’s food crisis. The staple diet in that nation of 105 million people relies on large imports of wheat and sunflower oil. Some 85% of the wheat comes from Russia and Ukraine, and 73% of the sunflower oil.

No surprise, Egypt’s government is not aboard the sanctions train. It has no choice. Food is first, particularly in a country where food inflation has brought down more than one regime. The opposite is more normal; Cairo heavily subsidizes food prices to maintain order.

How is that going to work now, with dramatically higher import prices and a worldwide recession to boot? If Egypt continues subsidizing food, which is likely, it will cost the country multiple billions of dollars that it really doesn’t have.

Now, multiply this challenge by dozens of other developing countries. On top of the human suffering and possible starvation, the economic effects could be giant. Governments that have to subsidize food prices may have to skimp on servicing foreign debts. Lenders could receive rude surprises, which leads nowhere good when financial markets are already overleveraged and overvalued.

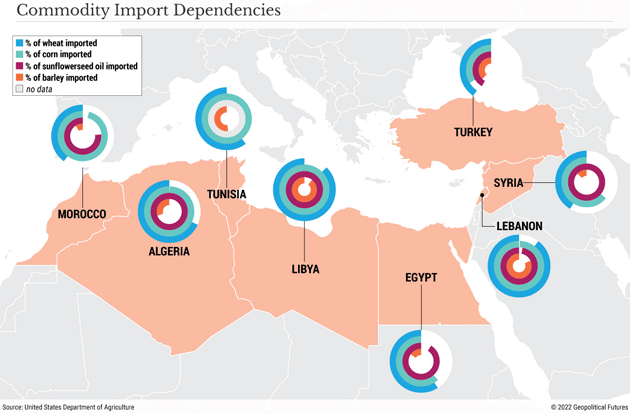

Look at how important Ukraine and Russia are to these Mediterranean countries:

It gets worse. The money governments redirect to basic needs is money that won’t be spent on infrastructure, education, and other productivity-enhancing projects. This will further reduce growth.

Now imagine you are a US tech giant that does business in all these markets, and has been counting on growth there to justify your stock valuation. How will that go? You can see the toxic brew before us.

And there’s yet more. “Normal” recessions end when consumers and businesses make adjustments sufficient to restore growth. That hope is slim this time, at least in the short term. As I noted last week, this is change squared. The entire world order is experiencing a shock adjustment—economically, geopolitically, and otherwise. We are not going back to January 2022. That world is gone—even if Putin and Zelensky reach some kind of cease-fire agreement soon.

My friend Vitaliy Katsenelsen (whose Coming to America story I sent you in December) has been following Russian media and talking to friends who still live there. He is not optimistic about Putin losing power. More the opposite: In a chilling tweet , he said “They are preparing to turn Russia into North Korea.”

That parallel, if accurate, is economically problematic. North Korea has been cut off from most of the world economy for decades, yet the regime survives. The sanctions we have placed on Russia, while necessary (and certainly preferable to a wider war), could last a long, long time.

I think we can adjust to a world split between two blocs with limited interaction. I don’t see how we complete the adjustment this year, though. Shifting supply chains takes time, and creating new production facilities takes even more time and money.

Misery index

All this is happening as the economy and markets are already on thin ice. In my annual forecast letter I called 2022 A Path-Dependent Year, with Jerome Powell’s path being the one that would matter most. As of last week, he was still saying the Fed will likely raise rates this month. That is unfortunately the right move. I say unfortunately because he might not now face the prospect of tightening as we enter recession if the Fed had started this process a year ago, as I and other observers called for. But here we are.

We learned this week the Consumer Price Index rose 7.9% in February. This data is pre-war, and doesn’t reflect the latest food and energy spikes. They will certainly drive it far higher. That means, unless the Fed shocks us with a far bigger hike than anyone expects, real interest rates will get even more negative than they are now.

One way to bring this kind of inflation under control is to sharply reduce aggregate demand. Higher interest rates are the Fed’s only tool for doing that. Will two or three percentage points spread over a few years suffice? That is a long time to suffer very negative real rates.

The other way is to increase supply, but the geopolitical circumstances plus the significant headwinds from government permitting in key industries make it difficult in the short term.

Moving on, we may see something I’m not sure has ever happened. Usually an inverted yield curve signals impending recession. As of now it’s getting closer but not yet fully inverted. That’s not surprising if, as noted, this recession is not due to the usual business cycle.

The Fed may have to intentionally create an inverted yield curve to keep inflation manageable.

Would Powell actually do that? I think the answer is yes because he does not want to go down as former Fed Chair Arthur Burns, who allowed inflation to get out of hand in the ‘70s. That doesn’t mean he is Paul Volcker, though. I think he will likely proceed too cautiously, but there is a real possibility for him to surprise on the upside in terms of interest rates. I don’t expect to see an easy monetary policy until inflation is under control.

Long-term rates are still relatively low despite the Fed tapering down its bond purchases. But that’s been under the assumption this inflation would recede in the next year or so. We are now in a significantly different environment. If bond investors come to believe inflation is shifting permanently higher, long-term rates will rise. As will mortgage rates, which won’t be good for housing and all the jobs and economic activity that sector represents.

Finally, let’s note the economy can cause a lot of pain even if not formally in “recession.” I’ve written several times about GDP’s flaws as a growth indicator. The COVID era’s wild swings further prove the point. I can imagine plenty of scenarios where GDP growth stays slightly positive but we are still in a world of hurt.

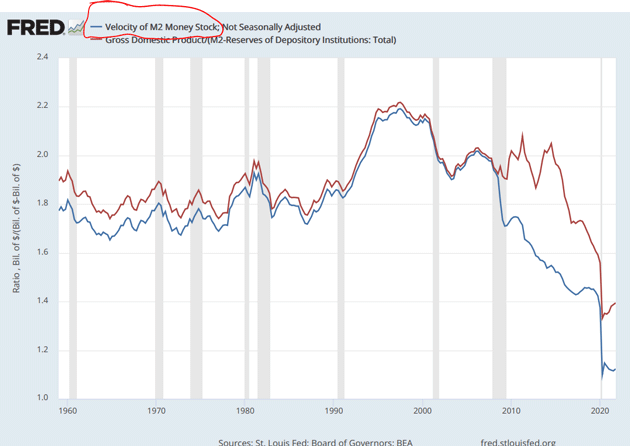

Velocity, banks, and the dollar

The velocity of money is now back at Great Depression levels. This is due in part to an overwhelming debt burden. We run massive deficits, increasing our debt, and somehow think we won’t turn Japanese.

Contributing to this is the inability of banks to find creditworthy borrowers even though they’re awash with capital. Banks shouldn’t lend without reasonable certainty of being repaid, and in today’s environment that’s difficult.

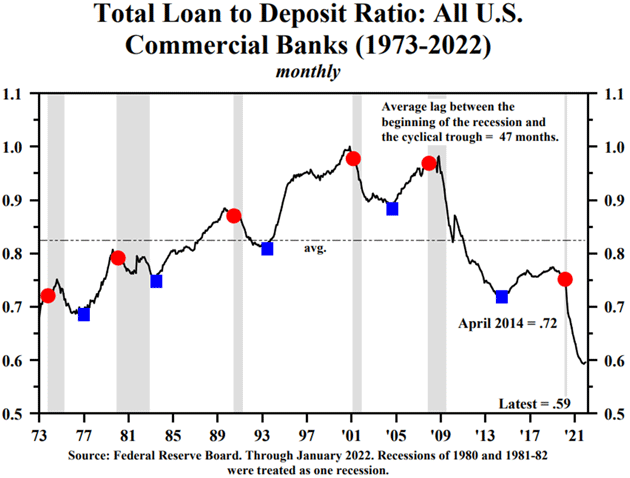

This chart from Hoisington Investment Management illustrates the issue. Note how far the loan to deposit ratio has dropped in the last two years. Previous drops of this magnitude were all in periods of uncertainty.

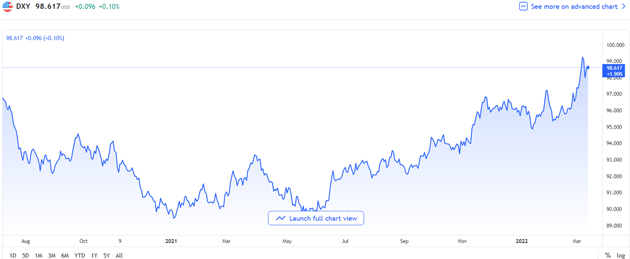

The dollar has risen over 10% in less than a year. The Federal Reserve is going to raise rates which should further strengthen the dollar. This actually helps US inflation, but it makes dollar-denominated debt troublesome in other countries, especially emerging market economies.

When Russia defaulted on its debt in 1998, there was a flight to quality and the dollar strengthened. But that put pressure on Asian countries that had borrowed heavily in dollar-denominated loans. They couldn’t repay, which created a crisis that ended up sinking Long-Term Capital Management.

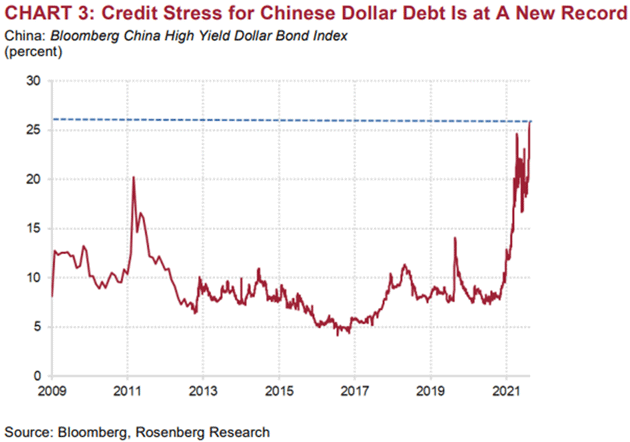

While China is not necessarily an emerging market, it does have a lot of dollar-denominated debt which is under great pressure. This chart from David Rosenberg:

That same phenomenon is playing out all over the world. Similar to 1998, many companies and countries are simply not going to be able to pay their dollar-denominated debts. Not while they’re trying to feed themselves and pay for their energy.

This is not going to be just a US recession. Its will be a global recession which is going to make it worse. For many countries, it will be a depression.

The US may have had a recession in any event because we are coming off a stimulus high. But it would probably have been a milder one. Now? It will likely be longer and deeper, but nobody knows. The world will have to adjust to supply chain and sanction problems. That will take time.

People are trying to deal with 8% inflation. The impact will vary but it will be difficult for many. It is time to get realistic about what we as a nation can and can’t do, what we can and can’t afford. We need an Operation Warp Speed for energy and supply chains and all manner of projects.

None of us asked for this. We’re getting it anyway. The administration and Congress need to start acting like this is a wartime economy. Because unless we work together, it will be.

*This is an article from Mauldin Economics' Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. This article first appeared here and is used by interest.co.nz with permission.

26 Comments

Nice article - and agree. I posted on another forum that I think the central banks now face two options:

1. Save financial markets.

2. Save the real economy.

Speculative investors appear to believe that option 1 is what central banks will do because of the 2008 - now behaviour. But that is only true because we have been in a deflationary environment. Now we are not.

Saving the real economy will require raising rates and forgetting about the financial markets - and hope that we soon experience deflation because in an odd way, deflation has been good for asset prices over that period (allowed central banks to push discount rates used for financial assets to near 0....)

What is the point protecting asset prices if Rome is burning? (and if that is what central bankers decide to do, protect asset prices, then standby for social and political unrest like we have never seen before).

The velocity of money is a very interesting metric to keep an eye on. To a large extent the massive expansion in our money supply (post march 2020) has been absorbed by a large decline in the velocity of money. However the flip side of this is if the velocity of money were to start to trend upwards we could get hit with a surge of inflation that is unprecedented in our recent history.

The only way to counter this would be to raise interest rates and try to contract our broad money supply. This would then crash our housing market. Basically we would enter a period of financial instability.

donny11,

I agree strongly except perhaps the last sentence.

Financial pain for many is inevitable but financial instability of the systems is not inevitable.

KeithW

There we differ, KW.

As the article points out (and as I have hereabouts for years); the 'economy' needs energy. For the last decade and more, there hasn't been enough to underwrite the keystroke-issued debt. A situation which is getting worse, not better. How do you propose dealing with the extant debt overhang, without losing so much faith that the system does indeed crash?

The problem PDK, and IO indirectly alludes to it in his comment is population control. In open and supposedly 'free' societies how does a Government control it's citizens? Debt is one way, where the banks become a tool of the Government to establish and maintain control. It is a means where people are rationed in the amount of spending power they have.

IO says there are two options; saving the financial system or saving the real economy. But bankers are smart people and they will be able to argue that saving the financial system is saving the real economy. If they lose control of the system, they lose their power and prestige they won't let that happen. The debt ponzi will not be allowed to fail. they'll dream up ways to ensure that because they know that any crash will be blamed on them directly.

One thing that interests me is US rig counts have not recovered to pre-crisis levels yet which seems irrational to me. Frackers have years of smooth sailing with Russia out the way it should be "all hands on deck", this is when the money will be made.

I think the issue with the rigs is the initital investment outlay is significant and becomes a massive "sunk cost" you have to wear if oil prices dip. Fracking requires a fraction of the cost to get going even though the marginal cost of production is higher.

I understand 'capital discipline' but I also understand 'lost opportunity cost.' The break-even on fracking will always be higher than offshore drilling so they have to react to market cycles to make money.

Fracking has NEVER made money. Too low an EROEI to do so; so it's been a combination of subsidies and number-injection (unrepayable debt issuance).

Good article - but: 'We always get through recessions and there will be a recovery.' is a linear comment. Our energy-extraction, of a finite resource, has been exponential. So the word 'always' - while it made a memorable song in the 20s for Irving Berlin - is not applicable.

Otherwise, he picks it well.

Haven't most or all of them been global in nature, especially when it involves major countries like the US, Russia, China or blocs like the EU? i.e. Turkey in recession won't cause a global recession.

And as always, the energy vulnerability solution comes down to building running and maintaining dispatchables like hydro, nuclear and geothermal. The Ukraine Kerfuffle is clarifying a lot of minds in this respect.

Very informative article thankyou. Enjoyed it a heap, and I agree.

We've landed in hot water alright. I don't think there is a way out this time.

Very good article and nice to see something on here besides housing. The FED announcement is in a matter of days and should provide a clear call for the direction things are heading. I see a lot of pain coming but as usual it will not affect those at the top.

Excellent article, thanks.

Great article. I think inflation is the root cause why governments and central banks can no longer "kick the can", it's finally time to do what has been needed for a long time, namely increase interest rates and we will have to learn to deal with the painful consequences of over a decade of exuberance and excesses

You must be like me Yvil, in a good position to weather the storm. I've had my wagons circled for over three years now. I've mostly just observed people in the distance having quite a party. Dark clouds gathering now. Seems less festive out there. Finally my wife may have some respect for my cautious decisions!

Ha, listen to both of you - pathetic.

You two have been two of the most pro -property guys on this website.

Now suddenly it's all darkness and gloom?

I can't recall Yvil ever saying prices can't go down, but he's certainly never hinted at anything more than a small dip, and has always talked up the mid to long term prospects.

Do you guys think we have the memories of goldfish?

That sounds like the old Fritz!

Unlike Yvil I wouldn't write "over a decade of exuberance and excesses", I would write, "the exuberance and excesses of the last couple of years"

I was only ever an observer of the facts as they were on the ground at the time. I would go to auctions and analyze results to try and detect which way property was moving. Occasionally I would write that it was actually rational because there were valid reasons for prices going up (basically Globalism and the concept of Global City - Elysium). For this I was usually accused of being a "spruiker".

You, not having the memory of a goldfish, will have noted that I haven't tried to justify price rises over the last couple of years. I have kind of been shocked and a little embarrassed by what has happened to be honest

In my comment above I was trying to be a little mocking of Yvil's comment. He does seem a little too eager for a correction. However I have given a reason why I wouldn't be totally against it.

Why do you write about property in your reply ? The article is not about property, nor is my post, having a a bit a of a slow day HM?

'Painful consequences of rising interest rates'?

So what would those 'painful consequences' be if they are not property related?

Rising interest rates are good for savers.

There's more to the economy than just real estate HM. To answer your question specifically, painful consequences such as:

A recession

Businesses going bust

People losing their jobs

People having less money left for essentials

Families going hungry

Etc

" Like the COVID recession, this one has little to do with the business cycle. It’s a recession of choice"

I beg to differ.....it is indeed a business cycle recession. One that was always going to occur as excess debt servicing sucked demand from the productive economy.

History may not repeat, but human behaviour does.

I totally agree. It was about to occur then covid happened, and it kicked the can down the road a few years.

As of the news tonight it appears the Ukraine war has upped the stakes of risk of a wider conflagration with the strikes a few km from Poland and Russia asking China for assistance in weapon supply . China is now in a difficult spot on the one hand Putin is a like minded autocrat on the other hand the economic threats from the USA will be worrying them having witnessed the sanctions against Russia. This should be watched with concern by nz if economic sanctions are enacted by USA against China and we are asked to join as an ally we are in trouble deep .

Is it time to revert to being a non-aligned country and become the Switzerland of the South Pacific again?

Apparently all you need to do is declare yourself an "Independent Nation" and everyone leaves you alone.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.