By Terry Baucher*

Inland Revenue is currently consulting on how New Zealand will implement the OECD’s Automatic Exchange of Information (“AEOI”) initiative.

As the OECD and Revenue Minister Michael Woodhouse claim, “AEOI is aimed at countering tax evasion and will be an important new means for recovering lost tax revenue.”

Perhaps. There is no doubt AEOI will be a useful tool, but even though it has yet to be fully implemented it is already having some unintended consequences. And those are separate from the problems of its broad sweep which will apparently affect even “ordinary” New Zealand trusts.

AEOI is a grand solution for a big problem. Nobody knows how much tax evasion is involved around the world. Recently researchers at the Centre for Economic Policy Research estimated the total of unreported financial assets as between US$6 trillion and US$7 trillion as at the end of 2013.

Based on those amounts the related tax evasion on could be as much as between US$2 trillion and US$2.6 trillion on personal income. Given the state of public finances generally in the wake of the Global Financial Crisis (“GFC”), it’s hardly surprising governments around the world are keen to clamp down on tax evaders.

Until the GFC, tax havens such as the British Virgin Islands, Lichtenstein and the Channel Islands were regularly used to hold funds both legally and illegally acquired. Switzerland with its banking secrecy laws was another popular location. The OECD viewed bank secrecy and protection against information exchange as a form of harmful tax competition.

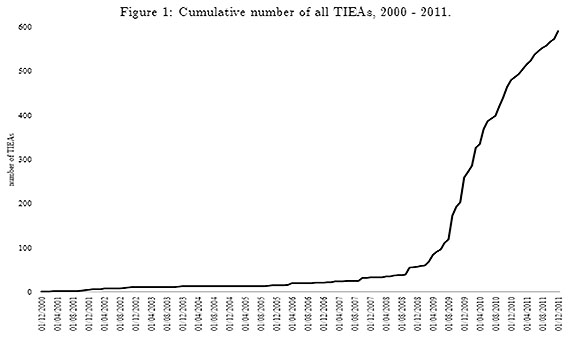

Accordingly, even before the GFC, it had been applying pressure on tax havens to make greater disclosures through entering into Tax Information Exchange Agreements (“TIEAs”). In the wake of the GFC, this pressure ramped up following the G20’s declaration after its London summit in April 2009:

“We call on countries to adopt the international standard for information exchange...We stand ready to take agreed action against those jurisdictions which do not meet international standards in relation to tax transparency.” The result was an explosion in the numbers of TIEAs signed as the following graph illustrates;

Between 2000 and 2011, 590 TIEAs were signed, most after 2007 in the wake of the GFC. Of that total, 555 involved at least one tax haven.

New Zealand signed its first TIEA with the Netherlands Antilles in March 2007 which came into force on 2nd October 2008. So far it has signed TIEAs with 20 tax havens, 11 of which are currently in force.

FATCA goes global

After the GFC the USA cracked down on overseas banks, particularly those in Switzerland, for assisting US citizens evade tax. The US Department of Justice imposed fines and forced the banks to hand over details of their US clients. (Although it’s worth noting that Credit Suisse, the second-biggest Swiss bank, told investors that the US$2.6 billion in fines it paid in 2014 when admitting it had abetted tax evaders was not “material”.)

As a deterrent to future tax evasion, the USA also introduced its controversial Foreign Account Tax Compliance Act (“FATCA”). Under FATCA non-US financial institutions are required to provide details to the US Internal Revenue Service about US citizens and tax residents who have specified foreign financial assets that exceed certain thresholds. Failure to do so will mean payments to the account holder are subject to a 30% withholding tax.

Despite its enormous compliance cost (estimated at between US$10 and US$20 for every single dollar the IRS gained), financial institutions and countries fell into line and implemented FATCA.

With FATCA as an example, the G20 launched an initiative in September 2013 to develop and implement a global standard for the automatic exchange of information. On 15th July 2014 the OECD Council approved the Common Reporting Standard (“the CRS”).

Three months later, on 29 October 2014, 51 jurisdictions signed the initial Multilateral Competent Authority Agreement to automatically exchange information under the CRS. New Zealand, together with Australia, Canada, Chile, Costa Rica, India and Indonesia, signed the Multilateral Competent Authority Agreement on 4th June 2015. In February 2016 Kenya became the 94th jurisdiction to sign up.

The G20 set a deadline of 30th September 2018 as the latest date for the first exchanges of information. A group of “Early Adopters” are already collecting information with the intention of making first exchanges of information next year. New Zealand proposes to require financial institutions to commence applying due diligence procedures from 1 July 2017. Inevitably, given the speed with which AEOI has been implemented, problems have emerged. One is that jurisdictions might attempt to use information provided to impose Value Added Tax (GST) on cross border transactions.

New Zealand has a thriving trust industry and trust practitioners are particularly concerned at the reporting requirements for trusts. AEOI is required in relation to a “Controlling Person” and under the CRS in relation to trusts this term means:

“the settlor(s), the trustee(s), the protector(s) (if any), the beneficiary(ies) or class(es) of beneficiaries, and any other natural person(s) exercising ultimate effective control over the trust. The settlor(s), the trustee(s), the protector(s) (if any) and the beneficiary(ies) or class(es) of beneficiary(ies) must always be treated as Controlling Persons of a trust, regardless of whether or not any of them exercise control over the trust.”

A tailor-made recipe for chaos

This is an extraordinarily broad approach, not consistent with general trust law principles. Its implications are enormous because under the CRS information might be required to be provided to several different jurisdictions in relation to each class of person. This could also affect “ordinary” New Zealand trusts as well as those with overseas settlors.

For example consider a trust settled under New Zealand law with New Zealand resident settlors and trustees. The brother of one of the Settlors is an appointor of the trust and is tax resident in Australia. One of the adult beneficiaries is on his OE and is now a tax resident of France. Another beneficiary is in the UK on a scholarship.

Under AEOI, Inland Revenue would need to supply information to Australia, France and the UK.

Furthermore, if the trust had reportable assets of say NZ$1 million, then each jurisdiction would receive data indicating the person resident in their jurisdiction “controlled” assets worth NZ$1 million. This is not the position under trust law and seems a tailor-made recipe for chaos as over-eager tax authorities issue “please explain” letters.

The USA becoming 'the biggest tax haven in the world'

Besides its potential overreach, CRS has one major flaw which has had a most unexpected consequence. The USA is not a signatory. It doesn’t need to sign up because under FATCA it gets all the data it wants on US taxpayers.

One reason why countries adopted FATCA was the hope of obtaining reciprocal information about their tax residents’ assets in the USA. So will the reciprocal arrangements under the various FATCA agreements provide the same information as would be available under the CRS? No, because the reporting requirements under the various FATCA agreements are not symmetrical.

For example, Inland Revenue must provide details of account balances held by United States individuals or on their behalf. No such reporting requirements exist for the US, particularly in respect to the controlling persons of any entities holding reportable assets. It’s therefore possible to avoid the implications of AEOI by holding the assets through an entity deemed resident in the USA for CRS purposes.

Consequently, funds have been moving out of traditional tax havens into the US with the express purpose of avoiding the AEOI requirements. In effect, the USA is now “the biggest tax haven in the world.”

Yes, that’s right, having imposed FATCA on the rest of the world, the USA then decided to not sign up to the CRS, therefore handing a massive advantage to its banking sector. Small wonder a lawyer in Zurich remarked:

“How ironic—no, how perverse—that the USA, which has been so sanctimonious in its condemnation of Swiss banks, has become the banking secrecy jurisdiction du jour.”

Ultimately, FATCA, a measure designed to stop tax evasion, has had the unintended consequence of making the USA the largest tax haven in the world. What’s more there seems little the rest of the world can do about this. This does not bode well for the future of the OECD’s Base Erosion and Profit Shifting (“BEPS”) initiative which must tackle the highly politicised issue of profit shifting by major corporations to tax havens. It’s likely to get ugly.

----------------------------------------------

*Terry Baucher is an Auckland-based tax specialist and head of Baucher Consulting. You can contact him here »

17 Comments

Good article Terry. It;s about time somebody woke up and smelled the coffee about the true nature of the US FATCA agreement and the costs that it will impose on New Zealand (and all other countries). The carrot of reciprocity was never going to happen and, as you point out, it is easily avoided anyway by serious players.

What is not generally realised is that the so-called US "Citizenship based taxation" applies to Kiwis who were born there or simply have a US parent. They are on the hook for taxes to the US on self employment income, capital gains on the family home, Kiwisaver, and a raft of other taxes not considered by the dual tax treaty. All this on income earned and assets with zero connection to the USA.

That sucking sound will be the US hoovering up income from New Zealand (and worldwide) that it should have no claim upon. By signing the FATCA IGA, the NZ government agreed to assist them in this extortion, all paid for by our banks and NZ taxpayers. Good job, way to go.

How far back does that go? Hypothetical scenario: My dad was an American GI who got mum pregnant in 1945, then shot the gap back to Ohio. Like a good girl, she put him on the birth certificate. Do I owe 60 years of back taxes to the USA?

Not unless you're a US ccitizen, AFAIK.

If you are, you're doomed. Time to run off to a Ecuador. Or Botswana. Or Te Puke. . .

Not true. If you have ever had a Green Card and not formally terminated it you are also treated as "tax resident in the US". This is great because if it has expired you have no right to live there but they will still tax you and penalise you if you don't complete the mind numbing paperwork. You are also caught if you spend too much time there.

Also, many children of US citizens may not know of their "obligations". In some cases they may have never set foot on US soil but will be hounded for taxes and forms until they die.

Yes you do. If either of your parents was a US citizen you are too, whether you like it or not - according to them.

Doesn't actually apply to me, but think about the mind-blowing implications if that's true. Even if you only consider the impact of US military, and all the places they've been stationed, presumably fathering piles of children along the way. Germany, all over the Pacific, all over France and Belgium, Kosovo. Somalia. Vietnam. Korea. Middle East. Afghanistan. Iraq, wherever the Navy have been on shore leave.

No as I assume your parents were not married.

That sounds like a veiled insult. ;-)

yeah well not your fault you are 1/2 American I suppose.

:P

American?? How dare you. I thought you were only calling me a bastard.

Nothing wrong with bastards.

New Zealand is clever at signing agreements without ever looking under the bonnet

FATCA is a blatant and disgusting piece of bullying by the US - but what was the NZ Government supposed to do?

If they don't cooperate with the US requirements, non-US financial institutions with any kind of asset in the US get a 30% withholding tax slapped on those assets.

The Government can leave each of the NZ financial companies to find their own way of dealing with this, or they can try to reach a national-level arrangement which will enable them to comply more efficiently and effectively.

Yes, it sticks in the craw to comply at all. But the cost is still less than not complying. And companies aren't entitled to be principled, bold and defiant with their clients' money.

"If they don't cooperate with the US requirements, non-US financial institutions with any kind of asset in the US get a 30% withholding tax slapped on those assets. "

.

the 30% WHT applies to interest earned, not on the full value of the assets.

And in the meantime all the American companies avoid paying taxes and get rich by billions of dollars ?

Once again the true colours of Washington shine through. Only interested in themselves. No morals Corrupt! https://www.youtube.com/watch?v=eHgbRYgpGGs

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.