By Gareth Vaughan

Total credit card billings in New Zealand reached $43.4 billion last year according to Reserve Bank statistics.

The local credit card market is dominated by Visa and Mastercard, who earn fees from the banks that issue their cards, and by processing payments. The bank credit card issuers, of course, lend the money and charge the interest rates which can be higher than 20%.

In October 2016 I had a look at Visa and Mastercard's NZ operations thinking that, given the size of our credit card billings and the two companies' market dominance, they'd have sizeable NZ companies.

But as I discovered that's not the case. The most recent financial statements Visa and Mastercard had filed to the Companies Office at the time of my 2016 story showed combined annual revenue of just $7.7 million, combined profit of $268,647, and a combined tax bill of just $257,109.

Shortly after my 2016 Visa-Mastercard story the London-based Lafferty Group cited NZ as the seventh most profitable credit card market out of 72 countries it surveyed.

"Pre-tax profits reached $275 million in 2015, an increase of 2% compared to 2014. It is forecast to reach $297 million by 2018. Profit per card reached $105 in 2015, compared with $88 in 2010. It is forecast to reach $114 by 2018," Lafferty said in its report. At $105 per card, profitability in NZ was up $17, or 19.3%, over five years.

The small scale of Visa and Mastercard's NZ businesses are because they merely provide "marketing support, client support and relationship and liaison services," and "services to related companies," respectively. In both cases the key relationship is with the parent company, which despite Visa and Mastercard both ultimately being American companies, are both domiciled in Singapore. And they both have subsidiaries in numerous other countries besides NZ.

The activities of Visa NZ's Singaporean parent are described as; "...The promotion of Visa branding in relation to cash payment, network, technology, products and services connecting consumers, businesses, banks and governments across the Asia-Pacific region, enabling them to use digital currency instead of cash and cheques."

Meanwhile, the Singaporean parent of Mastercard NZ's activities are; "Those relating to the payment technology that connects consumers, financial institutions, merchants, and businesses worldwide, enabling them to use electronic forms of payment and investment holding. The company earns fees from customers in the Asia-Pacific, Middle East and Africa region for providing transaction processing and other payment-related services to customers."

Sweetheart tax deals

The Singaporean parents enjoy sweetheart tax deals. The most recent financial statements they've filed show Visa NZ's Singaporean parent paid 4.3% income tax for the September 2016 year, and Mastercard NZ's parent paid 6.8% in the 2016 calendar year.

Interestingly, those Visa and Mastercard NZ financial statements noted above remain the most recent ones they've filed in this country. For Visa they cover the year to September 30, 2014, and for Mastercard they cover the 2014 calendar year.

In December I asked the NZ Companies Office, which operates under the auspices of the Ministry of Business, Innovation and Employment, whether Visa and Mastercard should have filed financial statements since February 25, 2015 and August 5, 2015, respectively.

A Companies Office spokesperson says the two companies were required to file financial statements for accounting periods up to 2014 under the Financial Reporting Act 1993 on the basis that they were subsidiaries of overseas companies. However, for accounting periods since 2015 subsidiaries of overseas companies are only required to file financial statements if they are deemed “large.”

Based on the 2013 Financial Reporting Act, a company is “large” if, in the relevant accounting period, at least one of the following applies; As at the balance date of the two preceding accounting periods, the total assets of the company and any subsidiaries exceed $20 million, or in each of the two preceding accounting periods the total revenue of the company and any subsidiaries exceeds $10 million.

For Visa and Mastercard their 2014 financial statements indicate they didn't meet the above “large” definition for the 2015 and 2016 reporting periods, the Companies Office spokesperson says.

"Accordingly, they were not required to deliver financial statements for registration for the 2015 and 2016 accounting periods. The Companies Office intends to liaise with these companies to confirm whether they have an obligation to file financial statements for the 2017 financial year," the Companies Office spokesperson said in December.

A filing reminder process

Over the past couple of weeks I followed this up with the Companies Office to see whether staff there had indeed liaised with Visa and Mastercard, and if so whether they have received any answers.

This time a Companies Office spokesperson says Mastercard has been sent "a first courtesy email reminder," and Visa Worldwide "its second courtesy email reminder." If it's deemed "large" Mastercard is required to register its 2017 financial statements by May 31 this year, and Visa is required to register its 2017 financial statements by February 28.

"The Companies Office has not yet received communications from the companies regarding their large or filing status," the spokesperson says.

This means the clock is ticking, kind of.

"Before a company is considered as non-filing, the Companies Office goes through its filing reminder process, which includes two reminders leading up to the filing date, then an overdue reminder, and finally a phone call to each company. Non-filing companies are referred to the Ministry of Business, Innovation & Employment’s integrity and enforcement team to consider for enforcement," the Companies Office spokesperson says.

'We comply with all applicable tax laws'

I asked Visa and Mastercard a series of questions about their NZ tax arrangements, whether their local companies are large under Companies Office criteria, and if and when they plan to file new financial statements in NZ.

A Visa NZ spokesperson simply says; "Visa treats its tax obligations seriously and is in compliance with all applicable tax laws and reporting obligations."

And a Mastercard NZ spokeswoman says; “Mastercard New Zealand complies with all tax laws. We have a small office in New Zealand and, as such, we’re not required to file financial statements under the Companies Office size criteria.”

For my 2016 story Visa gave a much fuller answer, which was;

"Since 1982, the headquarters of Visa’s Asia-Pacific Region, which includes New Zealand, has been located in Singapore. Our Singapore Asia-Pacific headquarters employs more than 1,300 people and provides significant activities and key processes relating to Visa’s core business operations and network payment services provided to Asia-Pacific clients, including those in New Zealand. We employ 12 people in the New Zealand office. Visa treats its tax obligations seriously and is in compliance with all applicable tax laws.”

The Inland Revenue Department doesn't discuss the tax affairs of any individual taxpayer.

Fancy a tax holiday? Visa and Mastercard both have one, - in Singapore

The latest financial statements from Visa NZ's Singaporean parent show annual revenue of US$2.3 billion, income tax of US$69 million, and profit after tax of US$1.5 billion. It generated US$1.18 billion of revenue from international transaction fees, US$976.277 million from service fees, and US$739.827 million from data processing fees.

Mastercard NZ's Singaporean parent's annual revenue came in at US$2.2 billion. Income tax was US$17.4 million, and profit after tax US$238.5 million. Key revenue sources were cross border volume fees at US$1.2 billion, and transaction processing fees at US$1.2 billion. (Rebates and incentives cost US$753 million).

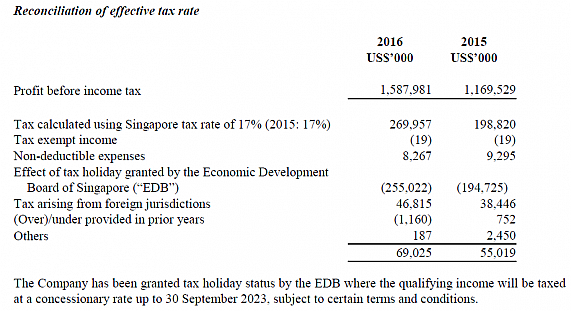

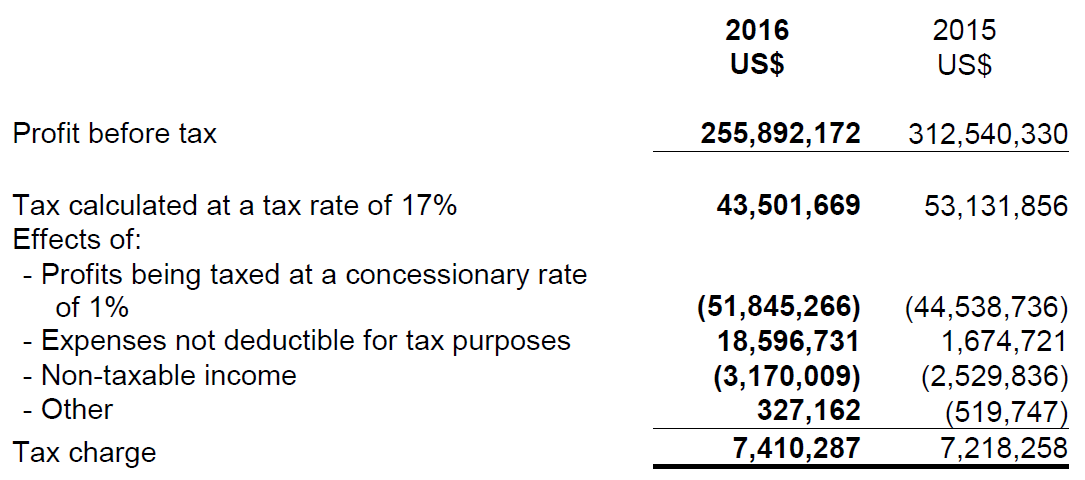

The Singapore tax rates are so low thanks to a sweetheart deal from the Singapore Economic Development Board (EDB). Mastercard notes it got an incentive grant from the Singapore Ministry of Finance at the EDB's recommendation in 2011.

"The incentive had provided the Company with, among other benefits, a reduced income tax rate of 1% on excess taxable income of a fixed base amount commencing 1 July 2011 and continuing through 31 December 2025," Mastercard says.

The table below comes from Visa NZ's Singaporean parent, which includes detail on its "tax holiday status" courtesy of the EDB.

The table below comes from Mastercard NZ's Singaporean parent.

The Singaporean parent of Visa NZ has a foreign currency risk section in its financial statements. This shows a 10% strengthening or weakening of the US dollar against the NZ dollar would have shifted its 2016 profit up or down by US$2.964 million. The Australian dollar equivalent provided is US$3.715 million.

Market power

In 2009, when Visa and Mastercard settled legal proceedings with the Commerce Commission over credit card interchange fees, the Commission estimated transactions on the two firm's NZ cards had totalled $19 billion in 2004. At that time there were about 2.1 million Visa cards and 900,000 Mastercard cards in use in NZ, giving Visa 61% of NZ credit card billings, and Mastercard 29% of the market. Their market dominance is only likely to have increased since then.

The latest financial statements for the NZ operations of American Express show 2016 calendar year revenue of NZ$73.9 million, a tax rate of 28% with tax of $1.32 million, and after tax profit of $3.34 million. Diners Club NZ was bought by The Warehouse from Diners Club Singapore for $3 million in 2014. The Warehouse doesn't separate Diners Club's financial results out in their own right.

Media coverage of international efforts to crackdown on tax avoidance and tax minimisation by global companies, through the likes of the OECD’s Base Erosion and Profit Shifting (BEPS) initiative, tends to focus on the likes of Google, Facebook and Apple. But surely Visa and Mastercard have earned a place at that table too.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

12 Comments

Introduce a banking transaction tax on money transfers leaving the country. Could go one step further and pay a rebate on money coming in?

@ Nzdan. Probably the only way Dan. Forget all the fandangled accounting because that just becomes an endless game of cat and mouse. But it works well that when they move the cash they pay.

It's about time we force the banks to offer open banking APIs so we don't have to use these ticket clippers or clunky systems like POLi. Labour are pushing for it but my guess is the banks will try and make it as clunky as possible.

So the smart guys in Singapore run rings around New Zealanders and mostly the government and it's civil servants don't even know it's happening. And are even less capable of dealing with it.

It's a hard mean world out there and New Zealanders don't even get it they are being shafted.

I don't think we should even try to compete with Singapore Governments low tax incentives. That's just a race to the bottom. Inter-government agreements are not going to work for us either.

Best just to have a hard arse regime internally in New Zealand. " If you want to do business here you pay the tax. Otherwise leave. Now."

I would like to see more companies doing what the likes of PB Tech do: offer a cash/EFTPOS price and credit card price that adds the commission on top. This addresses our in-person spending but doesn't resolve the online cut issue and payment of tax that's more inline with what your average Kiwi is forced to pay due to their inability to profit-shift.

We could remove the exemption for financial transactions from GST, that would catch a some of this and simplify our tax system at the same time.

So if you are a small operator, you pay tax. But if you're big, you give the finger to NZers.

If I was American I would be pretty annoyed that those big American companies aren't paying tax in America. But as a New Zealander I don't really expect an offshore company to pay tax here when they sell something here (other than GST where applicable). If they are adding value here, they should pay tax (as it looks like they do), but if they are just selling something here, why should they pay tax here and at home?

If the money isn’t collected by the govt as tax, it doesn’t mean that it ceases to exist. The money will remain in the economy enriching everyone within the economy ( albeit some more than others ) unless it is incentivised to move overseas by things like high domestic tax rates or lots of locals choosing to holiday overseas. Singapore is actually doing really well for itself, especially given that 60 years ago it was essentially a collection of fishing villages. I reckon that there is a lesson to be learnt from all this and that it is to lower tax rates (enough to attract multi-nationals) because a smaller slice of a bigger pie can still be more than a larger slice of a smaller pie. With a larger pie there is also more pie to around :)

I like pie.

But not that pie. It's a pie race to he bottom.

I paid proportionally much more tax than Visa and Mastercard last year so that should mean I get more voting power than them, or something surely?

Either that, or if I don't make a profit this year can I just not pay any tax?

Seems like there is one rule for multi-nationals and one rule for wage earners and I know who the schmuck is....

Like GST, financial transaction tax is the only way for the Government to clip off something from these type of activities. But may be the lobbies are too strong or the Government doesn't want to interfere with these big wigs' income/profit for other reasons ? Who knows ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.